First of all, a great summary of Gram Car Carriers, @WhatTheWACC!

Then, some answers to the questions presented:

- Risks can likely be found in the company material, but we’re talking about shipping, which is traditionally a very cyclical industry. However, ship chartering seems to be on the more stable end of the business. But it’s about leasing equipment to transport service providers. This means the financial situation of the customers is a significant prerequisite for the validity of the contracts. Then it might be good to also consider potential geopolitical risks—i.e., in which regions operations occur and what the possible consequences of conflicts would be. Though, these vessels are also particularly well-suited for transporting military equipment, so even that isn’t quite clear-cut.

- In a way, those customers who acquire their own tonnage are competitors. It’s a matter of balance sheet and risk management for those transport service companies; by using an external tonnage provider, the burdens on their own balance sheet and risks are reduced. And the ship lessor thus shares this risk by taking part of the fleet onto themselves. Car factories are also competitors to a certain extent; the more factories built in different markets, the less need to transport cars. For example, the US Inflation Reduction Act is expected to reduce the need for transporting cars to that market from elsewhere. However, the Gram fleet consists more of distribution and mid-size vessels, which serve distribution from factories to markets at a regional level (but Gram cannot benefit from this within the United States due to the Jones Act, whereas the situation is different from Mexico).

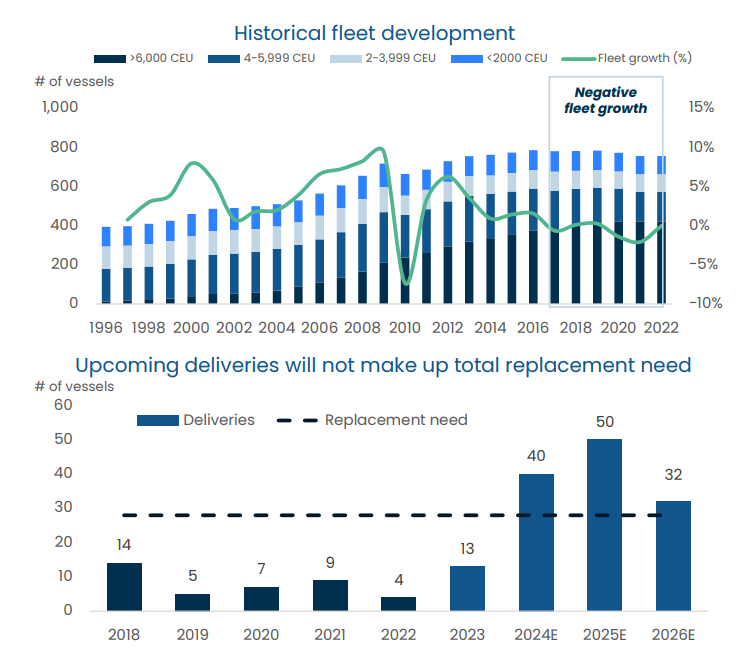

- Gram’s own materials show the image below, which suggests there is growth potential. However, much depends on how car manufacturers design their own logistics networks, as I already pointed out. So, demand is very much tied to how car manufacturers rethink their own distribution networks. Thus, growth potential is linked to the growth in car production, but the connection is not direct.

Generally speaking, I think this market is currently a bit “hot,” which is reflected right now in the available vessel charter rates and the ongoing growth in newbuild orders. As I understand it, shipyards are receiving inquiries for new vessels, and thus order books are still growing strongly. In these situations, it’s easy to end up with overcapacity, which in the slightly longer term leads to a drop in charter rates. Personally, I follow the industry and currently have a small weighting in the sector, as I suspect the market is at its peak.

Regarding the valuation: the NAV likely follows those vessel charter rates quite closely. When there is a shortage of vessels in the market, their prices also rise. And when the markets crash, vessel prices follow suit. Of course, the scrap value of the vessel always acts as a floor, which naturally follows steel market prices. In these tonnage providers, I personally follow more the company’s ability to generate cash flow and how the financing is structured and at what price. Essentially, how much charter rates have room to drop while the company still produces positive cash flow. And of course, what portion of the fleet is chartered out and for what duration.

And you should at least keep an eye on WAWI(OSL) and HAUTO(OSL) for now. These companies are likely the largest transport service providers in this sector and both are significant customers for Gram. This industry is very fascinating overall because the companies are so interconnected. For example, Gram’s major customer UECC is a JV of Wallenius Lines (not that Wallenius Line, which is a significant owner of WAWI) and NYK (NKK). In a way, the whole industry is a kind of ecosystem that organizes the transport of cars (and other Ro-Ro cargo) globally and contains many links between companies.