I haven’t bought into the company, even though I became interested a while ago, and this acquisition makes sense. I haven’t gone through the purchase price yet; it would be good to see the views of qualified analysts on whether it was a good price.

BUT: What are your thoughts? Take a look at the presentation about the acquisition from Jan 25, 2019, on Inderes TV. The reason why I’m not buying is clear from the start of the presentation: the CEO. He can’t even present in Finnish without being completely stiff; he probably doesn’t know English at all.

He is definitely not a dynamic builder of company and shareholder value.

More Air orders (more expensive than basic) and the first Heliotrope (smart glass thing) line order was supposed to be known by the end of 2018, and these have a higher price (than basic machines), and now, with the acquisition, Glaston holds more sections in the lines to be delivered exclusively.

Investment in maintenance will increase, and both companies operate globally, so maintenance can be streamlined and expanded.

This caught my attention:

“Glaston has secured financing for the acquisition from Nordea Bank AB (“Nordea”) and OP Corporate Bank Plc (“OP”). Their share of the acquisition financing, which will be used for both the acquisition, refinancing Glaston’s existing loans, and general working capital needs, consists of loans taken under Glaston’s secured senior loans, totaling 75 million euros, composed of (i) a 40 million euro term loan and (ii) a 35 million euro revolving credit facility, both maturing 3 years after the completion of the acquisition.”

These are in addition to the offering (15M€) and pre-emptive rights (32M€), which are used directly to finance the acquisition (68M€-47M€=21M€ short).

So, the acquisition will increase pressure on the earnings side, as the loan capital grows and becomes due on such a short timeline. Currently, the companies together generate 10-11M€ in profit.

From a synergy perspective, it seemed like a good acquisition, and the offering price of 0.405 was also quite reasonable, so there won’t be any direct dilution.

The share price has risen quite sharply, so after the deal is resolved, major shareholders might consider partial cashing out by selling some of their holdings at a higher price.

The degree of dilution is still somewhat dependent on the success of the rights issue. The deal seems quite sensible, at least with the current information. I have been following Glaston for some time, but I intend to wait patiently and see how this case progresses. However, the company’s products are investment goods with significant exposure to macroeconomic developments, and there are still many big unanswered questions from that direction.

Glaston was also going to provide guidance only afterwards, so perhaps in this case, patience is a virtue.

A couple of upcoming events:

“As the project progresses on schedule, Glaston and Heliotrope are preparing for the commercial launch of the first pilot line during spring 2019.” (For the commercialization of a dynamically operating smart glass product based on NanoEC™ nanotechnology)

And the GPD Step Change event in summer 2019. (“The theme of the summer 2019 conference is Smart Cities and Smart Buildings”). What expectations do you have for this trade fair? The purpose of the event is to attract potential partners, investors, etc.; so, with this acquisition, would something else be included, besides the smart buildings concept?

Regarding this Heliotrope collaboration, I’m interested in how the intellectual property rights work. I tried to dig into it once, but I couldn’t find a single word about it. Is there any information? Who owns the rights, and to what?

As I said, I haven’t left yet; the CEO is completely unbelievable. Even the CFO presented much more smoothly in that M&A presentation.

As I understand it, Glast owns a part of Heliotrope and gets the exclusive right to produce all smart glass lines for a long time. Vesala probably knows the specifics. I don’t remember the details. There’s probably only one smart glass line coming in 2019, quite certainly, but their value and margin level should be better/higher than basic products.

I’m a little annoyed that, according to the extraordinary general meeting invitation, only the so-called anchor investors get shares at a significantly discounted price, while the price of shares offered to other shareholders is determined by the board. If I believed I could buy more shares at the same price as the so-called anchor investors, then I would certainly be interested in acquiring more company shares. Unfortunately, I don’t believe that the rest of us will be offered shares at the same price. I will, however, attend the extraordinary general meeting to enjoy the refreshments, if nothing else is offered

The experience/know-how that Ahlström Capital brings to M&A could be the driver that finally brings Glaston back from the dead.

There are not many days left in the first quarter. Information about the Bystronic deal should be coming out any day now if the company is on the schedule mentioned in its press release.

From Inderes’ February report:

Investors’ patience will likely be rewarded

Due to the ongoing Bystronic acquisition, investors will need patience before the necessary additional information is received and a meaningful forecast for the post-acquisition entity can be made. Glaston’s current share offers reasonable upside, but our preliminary estimates for the share’s value after the new entity, based on incomplete information, are significantly, even 30-50%, higher than the current price. [Inderes]

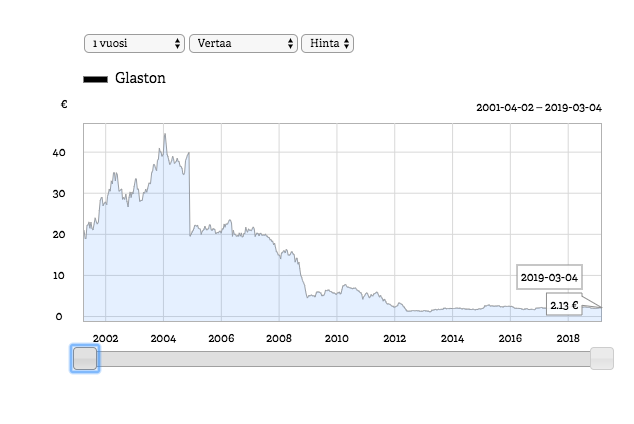

Glaston ended up in my portfolio this week when the share price fell below 2 euros. The initial position is about 1/3 of the planned investment. Before making new investments, I’m waiting for more information on the Bystronic deal and Glaston’s guidance for 2019.

A few things behind the investment decision:

Smart glass and Heliotrope cooperation

New technology and strong growth predicted for the smart glass market

Competitive advantage of significantly lower production costs (glass manufacturing) compared to competitors

No existing equipment base, so revenue will consist of high-margin equipment deliveries

Bystronic deal

Growth to a new size class and strengthening of market position

Complements Glaston’s product range well

Opportunity to increase sales of maintenance and services (Glaston Care & Glaston Insight). Current tempering unit vs. potentially the entire glass processing line in the future.

The biggest risk I see is a downturn in the construction and automotive industry cycle, which could delay stronger growth.

I must say, the share price development has been surprisingly sluggish. I’m considering buying more soon, although I’ve put a bit of a damper on things, just generally speaking.

It should be remembered that already at the extraordinary general meeting in February, it was stated that “The acquisition is expected to be completed in March-April 2019. The directed share issue is intended to be carried out in connection with the completion of the acquisition, and the Rights Issue is expected to start during the second quarter of 2019.” So, we might still have to wait until April before the deal is sealed.

I invested a bit more in Glaston and its long-term share price development again. The demand for smart glass in buildings is definitely a thing of the future.

Still waiting for the announcement of the commercialization of the Heliotrope project, which was supposed to happen around spring. In interviews, the CEO mentioned that the first buyer for the production line would be known once the product is ready.

The price of the smart glass production line will be 10-20 million.