Pretty good, a few months ago Fortum announced that their new strategy was to focus on Nordic clean energy production and now they’re already announcing plastic manufacturing projects ![]()

3 Likes

Surely those other business operations still need to be maintained and developed, especially if you want to get a good price for them? Or should Ekokem be left to idle and wither away?

19 Likes

To develop and grow, one must invest in research, innovation, and experimentation—startup activities. If it doesn’t gain traction, then you stop.

Finnish companies have always been plagued by a fear of experimenting; that’s why GDP hasn’t grown for over 10 years.

Fortum is experimenting, but is it experimenting enough? It’s hard to say; perhaps out of fear, they are now in some kind of defensive shell?

There should be investments in wind and solar parks, hydrogen; they should be involved in almost every hydrogen project.

I cannot understand why they stayed out of the industrial hydrogen valley pilot by Neste, Helen, and Vantaan Energia?

(The state is the majority owner of both Neste and Fortum, so it could even be in the national interest)

Fortum does have investments in plastics, e.g., the hard and frost-resistant Fortum Circo, which Fiskars also uses.

Fortum is nicely involved in, for example, recovering waste heat from data centers (Microsoft data centers in Espoo), and even using old car batteries for energy storage.

But even investments like electric vehicle charging infrastructure—buying out, for example, Virta or Kempower.

No breakthrough will be made by retreating into electricity and heat production in the Nordics using nuclear and hydropower.

20 Likes

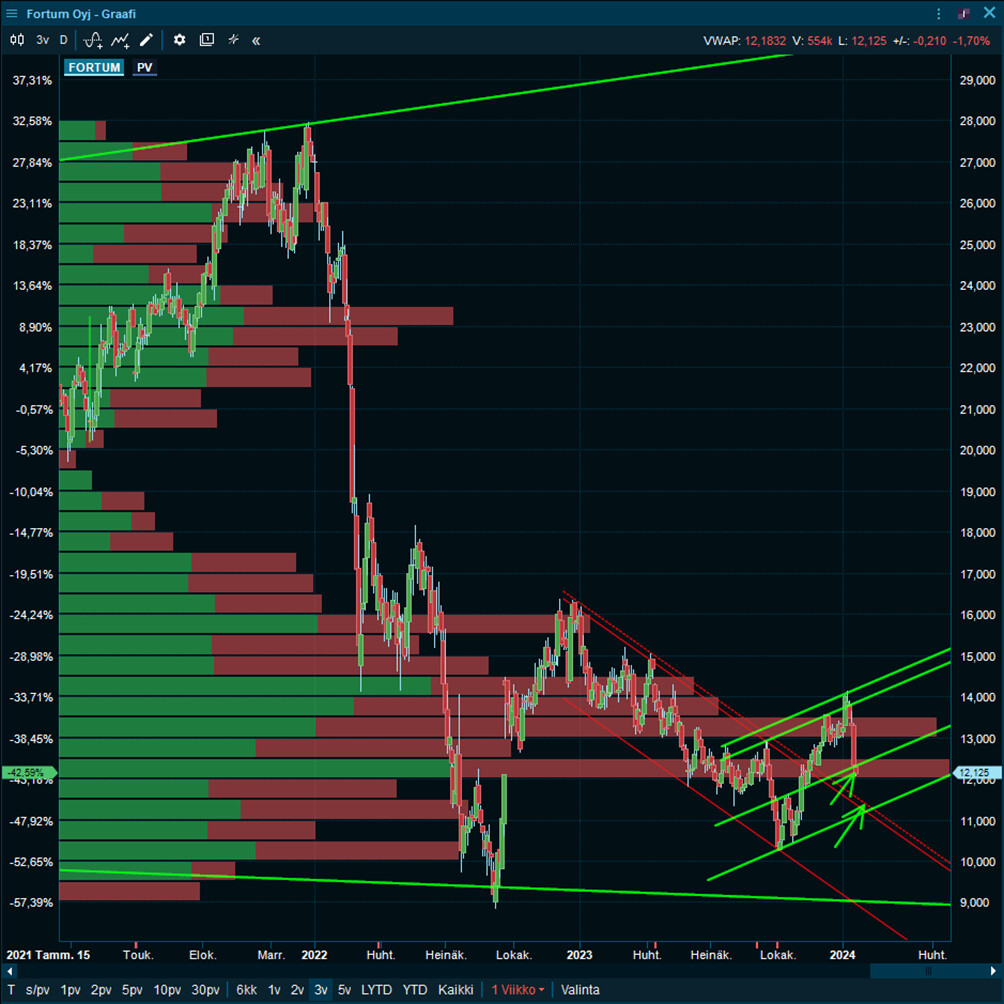

Today I was mapping out a potential buying program for Fortum, while gauging the depth of the current bottom and glancing superficially at the reasons for the ongoing decline. The following factors likely contribute at least to the rapid drop in the share price, and the selling pressure presumably comes primarily from foreign institutional investors, with general market weakness adding its own contribution.

At least Covalis Capital LLP has increased its short position from Jan 15, 2024 (0.56%) → Jan 16, 2024 (0.63%), which creates significant selling pressure for a stock that has risen from its bottom. It is possible the position was increased further today. The upside of short positions is that the rise is also rapid when the positions are eventually closed, as Fortum is unlikely to be played to zero. That is also possible, of course, if Fortum, for example, mistakenly ventures into Germany again.

The reasons for opening the short position can likely be found, for example, in weak growth prospects (e.g., according to UBS, EBITDA will fall 25% by 2025 vs 2023). On the positive side, UBS mentions the sector’s highest dividend. In addition, Goldman Sachs is cutting its recommendation from BUY to neutral due to potentially lower electricity prices. Also, the lack of investments can be seen as a weakness by some, but we Finns especially know how to appreciate the lack of targets after everything we’ve experienced.

Among peers, the US Utilities sector has fallen just over -5% from its January 8th peak. The sector’s decline has been led by, among others, the debt-laden NextEra i.e., NEE (-5.30% YTD) as well as the recent sluggishness of the overall market. In the European energy sector, there are also decliners such as RWE, which has come down -10.07% YTD. Out of 19 analysts, 13 give Fortum a strong BUY or just a BUY recommendation, four are holding, and two believe that Fortum should be sold before it’s too late.

Despite everything, Fortum was one of the best investments for me at the end of last year. At prices starting from €10.30-10.90 last October, the dividend yield rose to a massive level and the risk fell very low when the stock was driven into the ground with somewhat similar intensity to what has been observed now.

The dips of recent years provide clear hints of Fortum’s lowest bottom price: €9.00 is among the lowest fair prices if everything threatens to go to hell, and around ten euros if the market melts away and a recession really hits. As a target, Fortum is an easy target for short sellers because there weren’t enough domestic buyers at €14+ prices this time, and one usually doesn’t want to stand in front of such selling pressure. Personally, however, I already consider Fortum a buy at €11.625-12.500 and the buying program started cautiously today as we reached the area where most of last summer’s trades were made (cost basis).

On Friday, October 27, 2023, we saw the latest bottom in the indices. I noted at the beginning of January that Fortum had beaten all US sectors and gold, and by the beginning of the year (Jan 8, 2024), also the real estate sector XLRE and Russell 2000. It had gained a nice +25% since the end of October (and about +37% from the early October bottom), but now only about +10% remains. Once again, nothing could beat Bitcoin, nor has anything beaten it for over ten years.

Therefore, the timing and price of the purchase matter, and it’s worth trying to practice timing even a little. I aim to scale in with small purchases, but in Fortum’s case, usually slightly early. This reflection is mainly because I wonder if Fortum bought at around ten euros, with its dividends, will beat e.g. the S&P 500 and other US sectors this year, and what is the lowest price to which sellers and short sellers intend to push the stock this time. Short sellers might also well be targeting a small gap, the bottom of which is around €11.265.

The peer discount and reputational damage of Fortum are well illustrated by the fact that when I was asked last October what should be bought for a portfolio and I recommended Fortum at just over ten euros as one option, no one was interested.

Many thanks to those writing in the thread! My own monitoring of Fortum is very surface-level, and Fortum serves as a Nordea substitute in my portfolio when undervalued—i.e., as a “bank deposit” paying good interest and an occasional alternative investment. Additionally, I use the position to hedge my Fortum spot price (pörssisähkö) electricity contract.

144 Likes

Thank you very much for your great analysis! As investors, it is essential to occasionally analyze the share price as well.

The shorters’ algorithm is really easy to see. The price rises slightly until around 10–11 am, followed by a steady decline for the rest of the day. Occasionally, there is a steady rise for the rest of the day, just to have some variation every now and then.

My own investment is also a “bank deposit.” My average purchase price is currently higher than the share price, but if I take net dividends and inflation into account, the situation is okay.

Electricity price futures look rather poor from 2025 onwards, but on the other hand, I don’t really trust them much. Trading volume is still low, and Fortum likely makes direct bilateral long-term commitments with customers.

49 Likes

Indeed, 0.79% is the figure following yesterday. If I calculated correctly, 1.4M shares were added yesterday, which likely explains much of the sharp decline.

Edit: Btw, the volume peak for the last 3 years hits around €12.

24 Likes

Where could I track electricity price trends further out myself? What search terms should I even use?

Thanks @Thiebault and @Pappa_Tunturi for the comments. There is surprisingly little discussion about such a significant company. Probably many people exclude it from their watchlist entirely because of unpleasant memories from past years. As the share price dropped, I started getting interested for a change.

5 Likes

Nordic electricity futures can be found here:

https://www.nasdaqomx.com/commodities/market-prices

From there, just look for “Electricity Nordic” and for the future type, select “Quarter” or “Year”.

9 Likes

I follow these below:

Nasdaq Commodities - Market Prices - Electricity Nordic Market Prices - Nasdaq (nasdaqomx.com)

and

EEX Nordic Power Futures Futures (eex.com)

On EEX, you have to adjust the date at least one day back to see anything.

I’ve taught how to read Nasdaq in some electricity price thread. Can’t be bothered to do it again right now ![]()

![]()

14 Likes

Thanks. I’ll have to look for that thread too.

4 Likes

It’s so quiet on the forum that I’ll pester you even though my fax machine has run out of paper again. It’s so incredibly expensive these days.

After some snow clearing, I was browsing through some new material on Fortum’s website again for fun. I found this summary of the most significant events and decisions from Q4/2023 Summary of quarterly events | Fortum

The text mentions one of the personnel targets: “Other performance indicators include increasing the share of long-term power purchase agreements (PPAs) as part of normal power generation hedging.”

And a bit further down, extracted from the text: “On October 5, Fortum and the Norwegian aluminum and renewable energy producer Hydro Energi AS signed a long-term, 13-year, fixed-price power purchase agreement (so-called PPA) for an annual delivery of 0.44 terawatt-hours (TWh) of electricity in Sweden. The electricity will be delivered from Fortum’s power portfolio in the SE2 price area in Central Sweden. The contract period covers the years 2024-2036. Long-term power purchase agreements are included in the generation hedging for Nordic power production reported by Fortum. Fortum reports its wholesale power hedging levels and hedged prices on a quarterly basis.”

SE2 is typically the cheapest of Fortum’s price areas. Buying EPAD hedges has been very challenging, so this is a significant agreement. I calculated that producing this 0.44 TWh requires a capacity of 50 MW. This capacity corresponds, for example, to 10% of one of the Loviisa nuclear power units. Of course, it’s hydropower from Sweden’s SE2 being traded.

Have a nice freezing day and a great upcoming weekend to all the readers of the Fortum forum!

98 Likes

Yes, along with this perhaps somewhat “oddly” phrased point on the side:

- Net income forecast to grow 142% next year vs 7.2% decline forecast for Electric Utilities industry in Finland…

(=net income is forecast to grow 142% next year vs. a 7.2% decline for the Finnish electric utilities sector)

Reflecting on the recent share price drop…

Though there is still time until “next year”, well over half a year.

Or is there, after all…

![]()

7 Likes

Circular Solutions, which involves waste management/recycling operations, operates under Fortum’s “Other operations” (Muut toiminnot). As I understand it, at least part of these operate under the name Fortum Waste Solutions. In my opinion, one interesting part of these operations is the battery recycling processes that they have invested in over the last few years(?).

Fortum’s website features a story about Battery Recycling, and according to this, Fortum already has the entire “production chain” in hand, from pre-treatment of end-of-life batteries to black mass and the separation and recovery of precious raw materials for reuse:

“Fortum Battery Recycling’s operations cover all the necessary treatment and production steps to achieve the highest recycling rates and provide a closed loop for battery recycling along the entire value chain in Europe: pre-treatment services in Kirchardt, Germany and mechanical process in Ikaalinen, and hydrometallurgical metal recovery in Harjavalta. By combining Fortum’s mechanical and hydrometallurgical processes, 80% of a battery can be recycled.”

There has been a lot of buzz about China having the lion’s share of all the world’s battery material processing. Could this be part of the solution for how Europe and the rest of the world could become more self-sufficient in battery materials through recycling? And even more importantly, could a Fortum shareholder benefit from this opportunity? ![]()

I have understood that Waste Solutions is “under review” and the business is not at the core of Fortum’s strategy. I understand that currently, for a company the size of Fortum, we are surely talking about “small potatoes,” but in the future, say in 10 years, volumes could be in a much more significant class as, for example, EV batteries reach the end of their life and considering the general electrification of society.

If Fortum is among the first movers here, could this be a strategically important asset in the future? And if so, I am interested to see what conclusion they reach in their business evaluation.

Does the forum have information on how many players in Europe already control the entire recycling chain? Does Fortum have any kind of first-mover advantage, or are there already heaps of these players?

From what I have researched, there are at least articles stating that recycling is also concentrated in Asia. So, once we have gotten the battery materials out of China once, we end up sending them back there. Could it be smarter to recycle them ourselves once we have hauled them over to European soil? De-globalization and all that…

25 Likes

53 Likes

https://twitter.com/zijoittaja/status/1749406141182869521?t=FprNEnCF8V2vkRKhSBdTdA&s=19

I wonder if this could be the reason for the slight decline in recent days?

Edit. Oh, I forgot this was already discussed above. The position has grown further, though.

18 Likes

Here is a bit more information on what kind of hye… I mean, investment firm Covalis Capital LLP is; they specialize in the utilities sector, among others:

“Covalis Capital is a global asset manager focused on Infrastructure, Utilities, Renewable Energy, Industrials, Materials and Autos sectors.”

https://www.covaliscapital.ky/

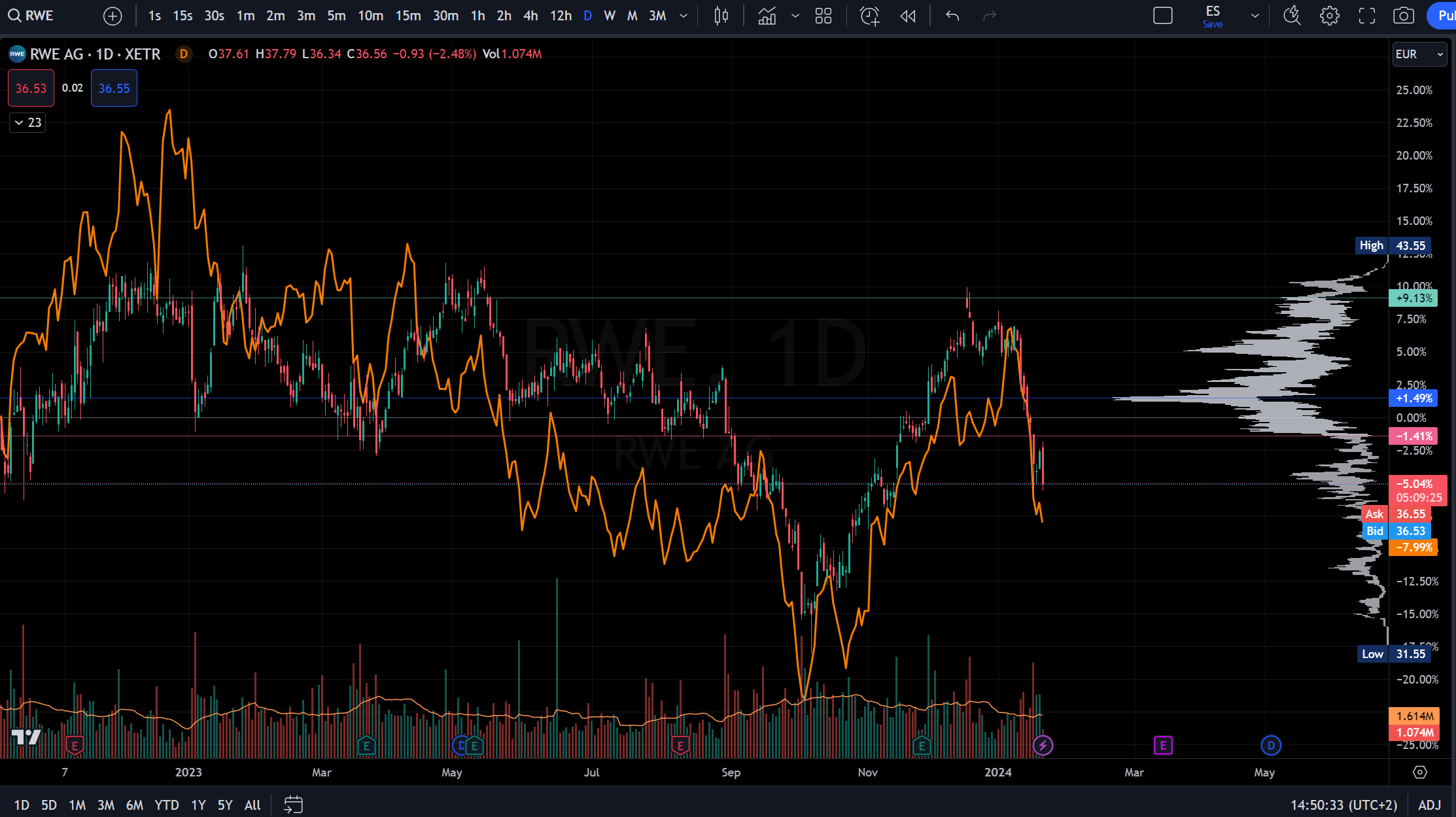

Peer RWE’s share price looks pretty similar to Fortum’s, so it is very likely that the shorts are targeted a bit more broadly at the entire utilities sector and could be, for example, part of hedging. Fortum’s market cap is about 39% of RWE’s, whose decline has been slightly more muted. Although the short position has increased since last week, the further decline will presumably fade slowly or at the latest at zero.

Fortum is yellow

https://shortnordic.com/detaljer.php?player=COVALIS%20CAPITAL%20LLP&land=sweden

11 Likes

Below is a story from Salkunrakentaja about Fortum from today, which mentions Citi’s rating downgrade.

“Banking giant Citi is lowering its recommendation for Fortum’s stock to a ‘hold’ rating from the previous ‘buy’ level. According to the bank, the decline in electricity prices starting from 2025 will limit the Finnish energy utility’s earnings capacity and dividend potential.”

and

Citi also lowered its target price for Fortum shares to 13.1 euros. Citi is cutting its 2025 earnings per share forecast by 14-17 percent to 0.94 euros and the dividend to 0.75 euros.

Subheadings:

- Declining earnings performance in consensus expectations

- Savings through an efficiency program

15 Likes

Fortum publishes a green finance framework. ![]()

https://classic.inderes.fi/fi/tiedotteet/fortum-julkaisee-vihrean-rahoituksen-viitekehyksen

Fortum has published a green finance framework to incorporate its sustainability targets into the company’s financing. The framework supports Fortum’s strategic priorities: delivering clean energy reliably, driving industrial decarbonization in the Nordics, and renewal and development.

Within the framework, Fortum has the opportunity to utilize green bonds and green loans in its financing for projects related to the development of renewable energy, energy efficiency, and/or nuclear power. If funds from loans under the framework are allocated to nuclear power production projects, this will be communicated at the time of the loan issuance. Projects covered by the framework include capital expenditures, investments, and/or operating expenses (including R&D).

16 Likes

Major policy guidelines for Fortum (owns over 60% of Kemijoki Oy’s hydropower shares). Sierilä will be spared from power plant construction, but pumped-storage power plants, capacity mechanisms, etc., are moving forward, meaning those growth investments are apparently on the way.

“The Cabinet Committee on Economic Policy considers it important to improve the conditions for pumped-storage investments in accordance with the Government Programme. In autumn 2023, the Ministry of the Environment included pumped-storage power plants in the priority procedure for green transition investment permitting, so that pumped-storage power plants are entitled to priority in permit processing. The Ministry of Economic Affairs and Employment is investigating the introduction of a capacity mechanism to support balancing and baseload power investments. The Ministry of Finance is investigating the development of interest deduction rights related to baseload and balancing power investments.”

4 Likes

I personally see small-scale nuclear power as the most fascinating “new” form of energy. Fortum has also commented on the subject: Fortum jarruttelee intoa pienydinreaktorien ympärillä | Kauppalehti

It’s not a long article (free to read), but the key points are below:

”A clear observation is that SMRs are at an even more immature stage than we believed. They are not ready, and that is one risk aspect that needs to be considered,” Lundström says. On the other hand, their development is, according to him, ”extremely rapid.” Fortum sees one opportunity for them specifically in nuclear district heating, i.e., producing district heat with a small nuclear reactor.

”Even though there is a lot of enthusiastic discussion about small modular reactors, few would be able to submit a binding offer for them. It still requires work. Large reactors, however, are already finished products,” Lundström says.

”We are trying to take all the lessons from difficult and expensive experiences. We want to avoid a situation where we build a certain reactor as the first in the world. We have seen in Finland as well that new reactor projects are not easy,” he says, referring to Hanhikivi and Olkiluoto 3, both of which were delayed and became more expensive.

”It is a huge turnaround, the speed and emphasis with which the Swedish government has moved the matter forward. There is discussion about various support mechanisms, and large-scale industry has strongly taken a stand in favor of additional nuclear power. There has been talk of a target of 8–10 large reactors.”

I personally see that in the near future, there might be quite good opportunities to carry out investments in line with the focus.

10 Likes