Fortum’s director Ollus reflects on the irrationality of the current electricity market and hopes for functional capacity markets alongside it.

Fortum: Something is wrong with the Finnish electricity market - Business | HS.fi

No paywall.

Fortum’s director Ollus reflects on the irrationality of the current electricity market and hopes for functional capacity markets alongside it.

Fortum: Something is wrong with the Finnish electricity market - Business | HS.fi

No paywall.

Interesting piece and really well-reasoned opinions. The only thing that remains a bit unclear to me is why Fortum wanted to come out with this? You’d think the current system would be the most profitable for them.

It has been thought that the market directs investments as efficiently as possible.

This, in my view, encapsulates the current problem: when the market is in control, users are at the mercy of these extreme phenomena whenever something happens. I get the sense from that article that Fortum, too, would value stability more compared to the current system, where sometimes they rake in big profits and other times they are scraping the bottom of the barrel. And that is why they are lobbying for a capacity market.

A completely free market is rarely a good solution. Perhaps the current framework conditions are not very good and should be examined with a critical eye. Hopefully, this will be done by the expert group in a way that both electricity producers benefit and investments increase, rather than, for example, for political motives.

“WHAT would a capacity market actually mean then? In its simplest terms, it means that the party responsible for the system’s operation (Fingrid in Finland) would purchase a specified amount of weather-independent production from the lowest bidder for one year at a time.” Fortum: Something is wrong with Finland’s electricity market - Economy | HS.fi

From Fortum’s perspective, the best-case scenario would be for this capacity to be purchased from them. Would there even be any other viable alternatives? This would play directly into Fortum’s hands.

The crux of that story is that investments won’t materialize if there is a fear of unstable electricity supply or pricing. Even Fortum could invest more if they saw growth in demand.

Maybe it’s a preemptive strike. If the price is pushed back to the 1-2 EUR/kWh range again now that the freezing temperatures are returning, there will surely be a political outcry. Then they can say that true, the system is broken and we are ready to change it. Designing the changes could then easily drag on through the next winter as well.

Maybe it’s a preemptive strike. If the price is pushed back to the 1–2 EUR/kWh range again now that the freezing temperatures are returning, there will definitely be a political outcry. Then they can say that true, the system is broken and we are ready to change it. Planning the changes might then drag on through the next winter too.

I was actually thinking the same. It’s quite likely that this system will be changed. The pressure is just mounting and the “market” itself is a bit questionable here. It’s more of a contract system between a few players. It’s better, then, to lead the discussion and try to stabilize the investment environment.

It would suit Fortum very well if a political decision were made to pay a “guaranteed price” for weather-proof production, which Fortum could then invest in with confidence, as it would be easier to crunch the profitability numbers.

In practice, this would mean that, on average, the consumer would likely end up paying somewhat more for spot-price electricity, but this would simultaneously cut peak prices and increase predictability in terms of price. Maybe worth it, depends on the details.

Currently, the only way to get that predictability is to pay a large premium for a fixed-term contract and outsource the risk to the electricity seller. And those premiums are currently unpleasantly high, partly because prices are so volatile. A consumer buying fixed-price would likely see prices drop if such a system were introduced, though again, it depends on the details.

There’s likely a lot of buzzing behind the scenes by lobbyists because it’s quite clear that the system needs some kind of fine-tuning. Politicians get beads of sweat on their foreheads when headlines tell stories of grandmas sitting in freezing cottages, unable to pay their electricity bills while prices go haywire and electricity company salesmen rake in the cash with ridiculously priced fixed-term contracts.

A sure sign that fixed-term contracts are currently expensive is simply looking at the “sales guns” from electricity companies stationed in shopping mall corridors. You have Helen and Fortum and others almost competing over where they can set up a stand to fish for fixed-term customers. For some reason, these are never seen during the summer heat… ![]()

And if you ask them about a spot-price contract instead, the salesperson’s interest in talking to you dies out very quickly ![]()

Fortum executive Simon-Erik Ollus states in the article, for example, that the construction of pumped-storage power plants or new nuclear power would be facilitated by the creation of a capacity market. Looking at it from this perspective, a few players immediately come to mind:

Perhaps the biggest is Kemijoki Oy, which is planning pumped-storage power plants in Lapland worth up to €4-5 billion. Of course, these are not a done deal, starting with the rights of the Sámi people. Fortum owns over 60% of Kemijoki Oy’s hydropower shares.

Small Modular Reactors (SMRs). In addition to Fortum, Helen, among others, has plans for these. However, the technology etc. is still somewhat of a question mark. For example, the leading U.S. project in this field recently had to be halted.

Pumped-storage plants in former mines. The Pyhäsalmi mine is a prominent example. The original party abandoned this, but reportedly several new interested parties have emerged.

And surely other things and other players will appear. For example, Vattenfall would have the resources.

If a capacity market is indeed created in Finland, it certainly offers clear growth investment prospects for Fortum. So, it’s not worth completely draining the cash reserves as dividends for us shareholders ![]()

Supplemented with this news:

If the market functions efficiently (and judging by price fluctuations, one could infer this), no one will be able to make excess returns. It would likely suit Fortum just fine if they were paid for extra baseload capacity.

Just because the spot price hits a thousand on a single day doesn’t mean there are excess returns.

I’ve been in meetings where, among other things, it was stated that the turbine won’t be replaced. Going forward, it will be heat-only, etc., because it’s not profitable… in the coal and CHP sectors, high-priced and profitable hours are often quite scarce… and then the plants are kept idle during the summer…

The public discussion has some strange characteristics.

For example, Fortum and Fingrid are worried about balancing capacity, while at the same time the largest source of balancing power, Meri-Pori, is leaving the spot market at the beginning of March, yet continues as a reserve under the National Emergency Supply Agency (Huoltovarmuuskeskus). One would think that would be an easy solution for the coming years.

Similarly, batteries and pumped-storage plants specifically thrive on price volatility. A capacity market for them sounds strange. There has been no willingness to become investment shareholders in nuclear power on the consumer and producer side (case Hanhikivi). Now subsidies are being called for. Heating companies have invested in electric boilers that thrive on low prices, meaning in practice, price volatility.

Personally, I would start with the idea that the electricity market is nowhere near free. In a globalized world, goods move across borders, but this doesn’t happen to the necessary extent with electricity.

In other words, a couple of power cables to Sweden, for example, would fix the problem. That is, we would be closer to a free market when transmission capacity doesn’t run out during peak consumption; I’d venture to say that this irrational price volatility would end there.

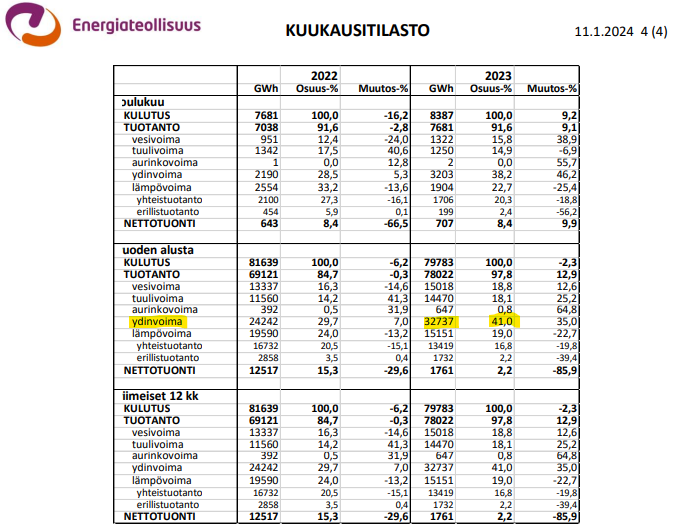

Yesterday, Finnish Energy’s (Energiateollisuus) December 2023 report was released, which also includes the data for the entire year pikatilasto_joulukuu.pdf (energia.fi)

I calculated Finland’s nuclear power production a bit further up, and it seems to be correct when compared to ET’s statistics.

The total of 32.75 TWh from the data sources I’ve collected is close enough to ET’s 32,737 GWh (32.74 TWh) ![]()

What’s interesting here is that although total consumption in Finland fell in 2023 compared to 2022, Fortum’s main production forms, nuclear and hydropower, have grown significantly.

Excess profits are exactly what we’re getting to make here. The production cost is always the same, but sometimes you get 5x the money or 22x the money. Production methods independent of weather variations specifically benefit from this. That’s why they only sell part of their production in advance.

Additionally, they’re pricing in electricity crises even though they haven’t even happened. It doesn’t seem efficient to me, but distorted.

Excess return depends on the timeframe and the mode of production.

For nuclear power, high hourly spot prices naturally generate significant revenue from the spot portion, but similarly, losses are incurred on the spot portion during periods of negative hourly prices. Nuclear power production is not adjusted based on hourly pricing. Furthermore, regarding nuclear power, it must be remembered that very high investment costs need to be covered over time. For this reason, there has been no appetite for new nuclear power investments in recent years. They have not been considered sensible. Existing nuclear power plant investments have already been amortized, which is why continuing their operation for as long as possible is economically profitable. Building new nuclear power would require higher average electricity price expectations to make it profitable.

Hydropower benefits from price volatility and adjustability, and these assets have already paid for themselves many times over—making them a gold mine for Fortum.

The dispute over the costs of the OL3 main grid protection system has turned in favor of TVO and, consequently, Fortum.

https://www.tvo.fi/ajankohtaista/tiedotteetporssitiedotteet/2024/4724047.html

Fingrid will likely now have to procure the 300MW of additional system protection itself, and TVO could now run OL3 at full power without concern.

The tug-of-war continues as Fingrid intends to appeal to the Market Court.

The main reason for TVO’s reluctance in this matter is that the production facilities currently tied to system protection cannot be sold to the reserve market at a higher price. These sites have large motors that can be shut down quickly when needed.

Fortum started a two-year program in autumn 2022 to explore new nuclear power investments, so there is indeed a willingness to invest. Especially in the current political environment, and particularly if it continues to become even more favorable for nuclear power. I see it as very likely that we will see significant investments in nuclear power this decade—still within this decade.

As stated, nuclear power is a massive investment. Furthermore, the political pressure surrounding the issue has been extreme. These factors have led to a lack of investment, and of course, in TVO’s case, the difficulties with OL3 undermined the OL4 project for the time being. There is also an industrial structural change taking place in Finland. While paper companies have traditionally been owners of nuclear power, right now it seems a steel company is involved in the feasibility study.

Additionally, one misleading factor in investment costs is the investment period. As I understand it, the operating life of OL3, for example, is calculated to be 60 years. Currently, a review is underway for OL1 and OL2 regarding extending their lifespan to 70 or 80 years. Of course, these plants cannot be compared directly, but I would assume a newer plant would last longer than those built at the turn of the 70s and 80s. So, if investment costs are paid back in 60 years, but the plant runs for 80 years—this changes the calculations tremendously, even if a billion were spent on modernization projects in the meantime.

There probably won’t be a rush to build another large Olkiluoto-style nuclear power plant, but I believe in the arrival of small modular reactors. That would probably be more sensible, wouldn’t it?