Here is the company report, posted by yours truly. ![]()

![]()

https://www.inderes.fi/research/vuolasta-osinkovirtaa

P.S. @Verneri_Pulkkinen

Wow, look at the prices in Finland tomorrow. Tabloid headline material..

EUR/MWh

| 05-01-2024 | SYS | SE2 | SE3 | FI |

|---|---|---|---|---|

| 00 - 01 | 87.91 | 88.83 | 88.83 | 169.99 |

| 01 - 02 | 83.15 | 83.09 | 83.09 | 150.07 |

| 02 - 03 | 79.91 | 80.00 | 80.00 | 150.06 |

| 03 - 04 | 78.86 | 80.17 | 80.17 | 150.07 |

| 04 - 05 | 79.94 | 82.49 | 82.49 | 150.09 |

| 05 - 06 | 86.85 | 88.14 | 88.14 | 350.00 |

| 06 - 07 | 98.50 | 109.79 | 109.79 | 999.94 |

| 07 - 08 | 137.06 | 165.01 | 165.01 | 1,478.91 |

| 08 - 09 | 150.08 | 199.27 | 299.01 | 1,251.67 |

| 09 - 10 | 171.36 | 238.31 | 249.12 | 1,000.00 |

| 10 - 11 | 176.40 | 255.86 | 255.86 | 999.98 |

| 11 - 12 | 159.88 | 211.11 | 211.11 | 800.00 |

| 12 - 13 | 151.99 | 203.28 | 203.28 | 999.91 |

| 13 - 14 | 149.92 | 196.98 | 196.98 | 899.06 |

| 14 - 15 | 153.54 | 197.86 | 197.86 | 999.97 |

| 15 - 16 | 200.00 | 299.94 | 299.94 | 1,696.31 |

| 16 - 17 | 254.58 | 449.64 | 449.64 | 1,758.00 |

| 17 - 18 | 247.47 | 526.25 | 526.25 | 1,478.95 |

| 18 - 19 | 199.48 | 349.95 | 349.95 | 1,896.00 |

| 19 - 20 | 165.00 | 181.91 | 181.91 | 1,754.00 |

| 20 - 21 | 142.76 | 149.60 | 149.60 | 990.09 |

| 21 - 22 | 115.96 | 112.82 | 112.82 | 749.95 |

| 22 - 23 | 112.96 | 100.10 | 100.10 | 300.01 |

| 23 - 00 | 95.59 | 92.87 | 92.87 | 200.00 |

Well, time to heat up those Friday saunas tomorrow ![]()

Workers have been recruited for the annual maintenance of Olkiluoto 3 for the period March 2 – April 8, 2024. ( WORKERS FOR OL3 ANNUAL MAINTENANCE AT OLKILUOTO | Oikotie Jobs

Has there been any coverage about this annual maintenance and/or its effects on, for example, electricity futures prices?

Does this annual maintenance, i.e., revision, mean that OL3 will not produce electricity during that time?

It’s an annual thing. It won’t produce electricity then.

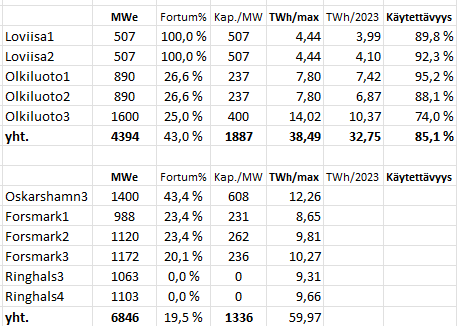

A total of 32.75 TWh of electricity was produced by nuclear power in Finland last year. That is over 40% of the electricity used in Finland. The percentage will rise this year if the pumps keep pumping well ![]()

Fortum’s share of produced nuclear power in Finland in 2023 is 43%. A nice amount ![]()

Swedish figures can be easily obtained from Vattenfall’s and Fortum’s reports once they are released.

EDIT: small formula correction to Sweden’s maximum value

EDIT2: Sweden’s total consumption for 2023 can be found at Bild 1 (energiforetagen.se)

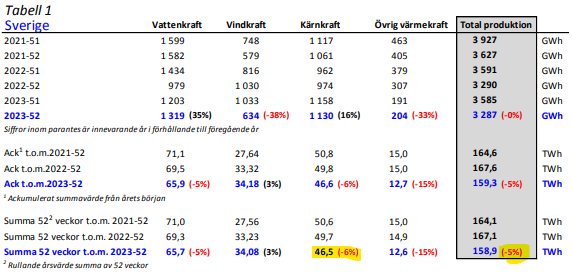

Sweden’s electricity consumption fell by 6% last year compared to the previous year. Nuclear power production decreased by 5%, totaling 46.5 TWh. This results in an availability factor of 77.5%, which is not particularly impressive. There is some minor trouble again in January.

Juha Varis’s interesting highlights regarding Fortum’s 2024 EPS forecasts. ![]()

At the end of 2022, Finland’s wind power capacity was 5.7 GW, and by the end of 2023, it was 6.9 GW. According to the Wind Power Association, with projects currently under construction, wind capacity will reach 8.0 GW by the end of 2024 and 9.4 GW by the end of 2025. The average yield of wind power is around 1/3 of the nominal capacity, so the increase in capacity by the end of 2025 means an expected additional available power of approximately 800 MW. Furthermore, the 800 MW Aurora Line to Northern Sweden’s hydropower area will be completed by the end of 2025. This creates an expected 1.6 GW of additional capacity for the Finnish market area, and at least 800 MW whenever needed. I believe this will inevitably have an impact on futures prices by 2025 at the latest. We already saw in the summer of 2023 that futures hit somewhere around €41/MWh.

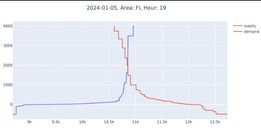

Additionally, those supply-demand curves on the electricity exchange are quite flat before the exchange price truly starts to deviate from zero. For example, today’s peak hourly price would have dropped to a fairly normal level if 1 GW of reasonably priced additional power had been available, as can be seen from the image.

As wind capacity increases, that flat area will expectedly shift even further to the right, and the capacity of the 800 MW transmission line, which is always available, is typically priced quite moderately. Upward price volatility in the electricity exchange will inevitably decrease and downward volatility will increase, which for Fortum means not only lower hedging prices but also lower returns from the optimization of hydropower production.

Demand growth is unlikely to take off for another couple of years. The biggest current drivers are likely electric district heating boilers, but even they effectively aim to utilize the lowest hourly prices. There have been quite a few cancellations and postponements regarding hydrogen investments lately.

I should check how much wind capacity is being built in Sweden during 2024 and 2025.

I consider Fortum a good company, especially now that net debt is nearing zero. It also makes up a significantly oversized portion of my own portfolio according to all investment principles. Because of this, I intend to keep my eyes open around the time of the Q4 announcement and perhaps rotate some of my shares through a potential summer sale.

This continues to puzzle me, at least I assume it’s behind a paywall: Fortumin on löydettävä nopeasti uusi polttoainetoimittaja Venäjän tilalle Loviisan ydinvoimalaan – Ensimmäisiä tuloksia odotetaan syksyllä | Kauppalehti

Does Finland and Russia still have some kind of gentleman’s agreement that Loviisa receives nuclear fuel? There must be some foolproof way to check that the fuel received from Russia is up to spec!? Or has so much fuel been stored that the stocks have lasted since the start of the war in Ukraine? Unlikely, because I remember coming across a story mentioning that shipments from Russia are continuing. Someone who understands the matter better could shed some light on it, @ollikohan is usually well-informed on technical details!? This situation is just quite hard to understand, because Russia specifically has used everything related to energy as a means of pressure.

A few quotes from the article:

“Energy company Fortum is seeking a way out of Russian nuclear fuel to improve security of supply at the Loviisa nuclear power plant. Loviisa’s nuclear reactors are Russian-type VVER reactors, whose fuel comes from Russia from Rosatom’s subsidiary TVEL.”

“Fortum has an agreement with the Russian TVEL group for the supply of nuclear fuel to the Loviisa nuclear power plant until the expiration of the reactors’ previous operating licenses at the end of 2027 and 2030.”

“Now Fortum expects its new fuel partner, the American Westinghouse, to be able to design a new fuel type relatively quickly, as it is based on fuel type E-3, which was used in Loviisa in 2001–2007.”

“Current fuel is in stock for Loviisa, the company says. We did not receive an answer from Fortum as to how long the fuel will last.”

Addition: Here’s a fairly recent story from last November: Raja-asemien sulusta koituu Suomelle rahallisia menetyksiä – Tutkija: ”Pienille yrityksille sulku voi olla kohtalon isku” | Talous | Yle

“By rail, items such as nuclear fuel and metals come from Russia. In the other direction, for example, metals are exported, with an export value of tens of millions of euros per month.”

I imagine there’s enough fuel stashed away for several years’ worth of needs; it’s such a critical matter for security of supply, among other things. Furthermore, more is still coming from Russia despite the ongoing war, as has been reported in the media.

And yes, Russian gas is still flowing through Ukraine’s pipeline network to Central Europe, even though the war has been going on for nearly two years now.

Article in Hesari:

The weather is so cold today too that my fax machine has frozen and the papers in it are somehow stiff. Due to the cold climate, I don’t feel like going outdoors at all today.

To pass the time, I re-read the Q3/2023 interim report. I have a question for the hive mind regarding the optimization margin:

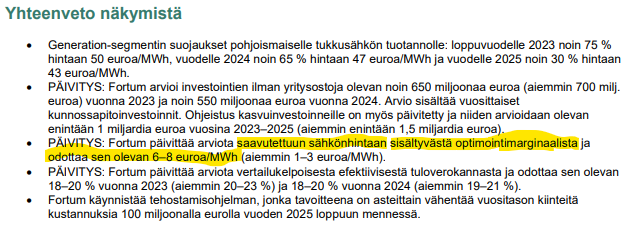

I was under the impression that the 6-8 €/MWh applied only to the hedged portion. Reading through this part marked in yellow, I think it applies to the entire production. I would be very interested in @ollikohan’s insight.

A nice amount of extra cash is flowing into the balance sheet from those other lines as well. Our top analyst @Juha_Kinnunen already promised us a nice dividend, partly thanks to these.

This is going to be good, if not excellent. The short sellers are already feeling the squeeze quite a bit, even though the share price is still in their grip. Now we just need the pension companies to wake up to this sure (“Varma”) return ![]()

EDIT: Fortum is fast approaching a net-debt-free status. In the future, there will be no more investment blunders with “world conquest” policies. This cash will be funneled into investors’ pockets for the coming decades via semi-annual dividends.

Thank you very much for your answer ![]() With these assumptions, the achieved price could be around 60 €/MWh for Q4/2023.

With these assumptions, the achieved price could be around 60 €/MWh for Q4/2023.

At Loviisa, 1/4 of the fuel assemblies are replaced with fresh ones every year. I would believe that the plant has at least two full loads of fuel in stock, simply due to the security of supply factors mentioned. I don’t know for certain, though. New assemblies will surely be obtained from Westinghouse before the current ones run out.

Yes, it applies to all production. For hedged electricity, we get hedging price + optimization margin, and for unhedged production, we get average spot price + optimization margin.

To be honest, I don’t really know anything about such details. But my understanding is the same as the previous commenters: there is likely enough stock for quite a long time. Storing nuclear fuel, even for several years’ worth of needs, is probably not that challenging.

Thanks for the answers, everyone. I understand the storage aspect myself, but indeed, the certainty that the fuel coming from Russia is up to specification was something that made me wonder a bit. There is probably some chemical way to test this; otherwise, a faulty batch could sort of “accidentally” slip through, which in the worst case would cause problems in the reactor.

Russia’s motivation for this kind of action is, of course, difficult to fathom, as they likely receive precious metals and other products in return that are not under sanctions. A sabotage attempt involving nuclear fuel would likely have a global impact on the willingness to conduct any trade with Russia. Details regarding the safety mechanisms of nuclear power plants are naturally kept secret for a reason, so the average person on the street cannot hope to obtain information about them.

Perhaps, for one’s own peace of mind, it is best to just trust the authorities’ and Fortum’s own processes and not trouble one’s own little head. As a shareholder, however, it’s useless to cry once the damage is already done. Even Uniper’s derivative arrangements and guarantees looked like completely normal business when explained in the best possible light by Rauramo, up to a certain point.

Apologies for drifting off-topic a bit ![]()

As a disclaimer, I increased my own Fortum position by 40% immediately following @Juha_Kinnunen’s fresh report. It was quite convincing text indeed ![]()

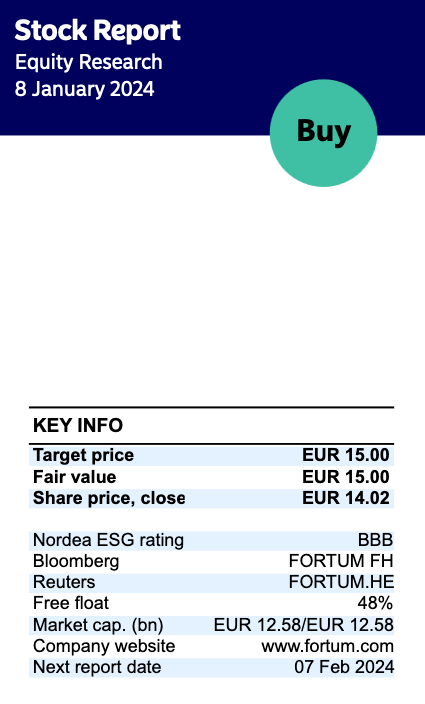

Nordea published its updated Fortum analysis. The recommendation (BUY) and target price (€15.00) remain unchanged. Nordea is raising its forecast for Fortum’s dividend to €1.20 per share and notes that it is higher than the Vara Research consensus of €0.95.

A review of Fortum’s performance and outlook:

"A generous dividend combined with the stock’s current valuation would seem to offer an attractive risk-adjusted expected return. The P/E ratio is around 12 based on next year’s forecasts, by which time the worst of the earnings decline should be over, according to Inderes.

Behind the stock’s low valuation is investor confidence that has remained subdued, driven by billion-euro losses from Uniper and the subsequent controversies surrounding the state-provided emergency loan and executive compensation.

Kinnunen from Inderes states that although reputational damage is still visible in the stock’s pricing, there is no fundamental basis for it, and the undervaluation will likely dissipate over time if the company continues its stable development."

In the Q3-2023 Inderes earnings interview, Rauramo stated that the optimization margin consists of hydropower optimization as well as grid frequency optimization revenues and Guarantees of Origin revenues. Prices for Guarantees of Origin fell slightly in Q4-2023 compared to the beginning of 2023. But it will likely still provide a good contribution.

Fortum to build a new nuclear power plant?

The satraps of Swedish business (Volvo, Stora Enso, Saab, the powerful Wallenberg family, etc.) have today published an appeal demanding the construction of new nuclear power in Sweden. At the same time, they state they are in “constructive discussions” with Fortum on the subject and see Fortum as a key player in the Swedish energy mix alongside Vattenfall.

As background, the Swedish government recently appointed an investigator to make proposals to accelerate the construction of additional nuclear power. The government will likely provide interest rate subsidies and other incentives based on the report. Furthermore, in the aforementioned letter, Swedish industry states its readiness to participate in nuclear power investments together with energy companies.

This letter is highly interesting (and important) from Fortum’s perspective. If successful, this would open up new growth investments, and it must also be remembered that Sweden is more important than Finland as a production country for Fortum. Sweden’s large corporations would be a most solvent customer group for Fortum.

Here is the satraps’ letter: