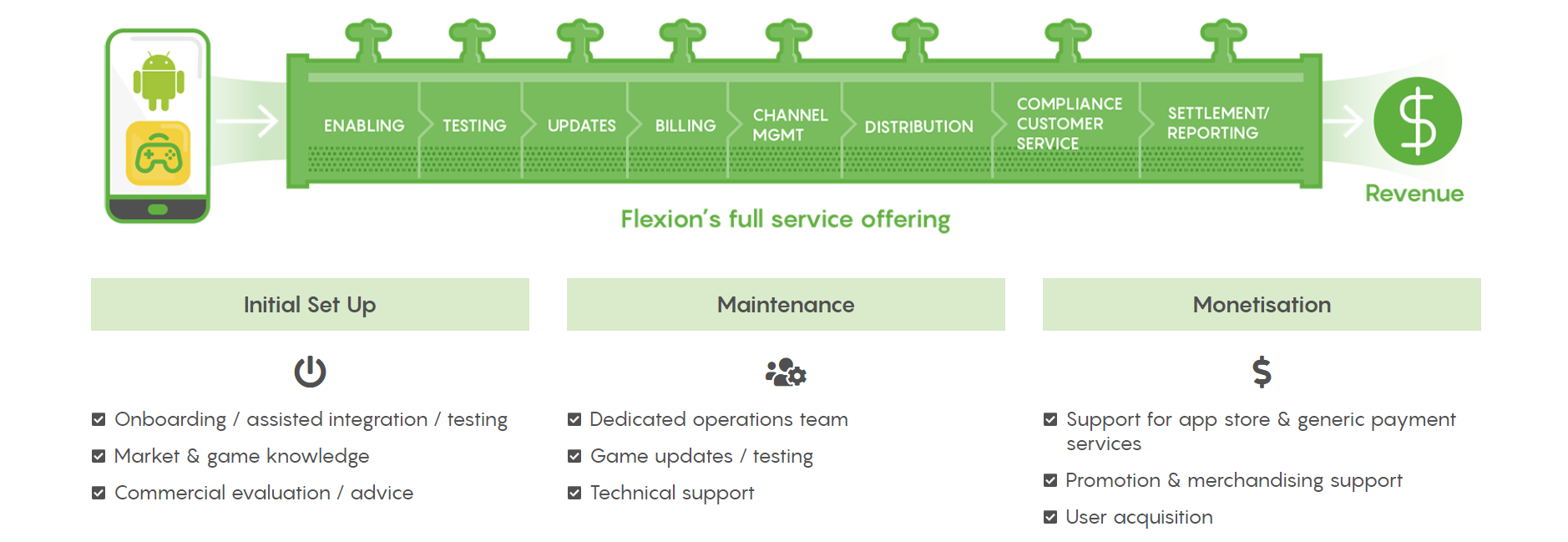

Flexion Mobile Plc is a company operating in the mobile gaming industry listed on the Swedish stock exchange. I am not an expert in the field, so someone can correct me if I write something incorrect in the introduction. As I understand it, the company doesn’t actually produce games itself, but rather provides a platform for their development/publishing, etc.

The company focuses on IT and applications for developing/publishing mobile games on multiple platforms/marketplaces.

Nordnet’s description of the company:

“Flexion Mobile operates in the IT sector. The company has developed various technical platforms for customers in game development. The vision is to offer mobile platforms that the company’s customers can use to more easily distribute games in their sales channels. The largest business is established on the European market. Flexion Mobile was founded in 2007 and is headquartered in London.”

Image from the company’s website.

Q3

Flexion delivers its sixth consecutive record quarter with revenue growth of 138% and EBITDA of GBP 1.5 million

July-September 2022 performance

-

Total revenue increased by 138% to GBP 18.5m (7.8)*

-

Gross profit increased by 196% to GBP 3.0m (1.0)

-

Adjusted EBITDA[‡] increased to GBP 1.5m (0.1)

-

Adjusted profit before tax[#] increased to GBP 0.3m (0.1)

-

EPS amounted to GBP -1.22 pence (-0.07 pence)

-

Adjusted EPS amounted to GBP 0.51 pence (0.08 pence)

-

Operating cashflow amounted to GBP 1.9m (-0.4)

-

Cash and cash equivalents amounted to GBP 10.5m (15.0)

January-September 2022 performance

-

Total revenue increased by 111% to GBP 46.8m (22.2)*

-

Gross profit increased by 166% to GBP 7.4m (2.8)

-

Adjusted EBITDA[‡] increased to GBP 3.2m (0.04)

-

Adjusted profit before tax[#] increased to GBP 0.8m (-0.1)

-

Operating cashflow amounted to GBP 4.9m (1.4)

Important events during the quarter

-

Launch of King of Avalon from FunPlus

-

Signing and launch of Matchington Mansion from Magic Tavern Inc

-

Signing of Call Me Emperor from Clicktouch Co. on the Japanese market

-

Signing of Kiss of War from tap4fun

-

Completion of USD 500k Liteup Media investment for 20% stake

-

Launch of cost-per-install (CPI) service by Liteup Media to target TikTok users

Important events after the quarter

- With Amazon-Windows 11 deal, Flexion can help Android games reach PC audiences

In addition, an explanation of the difference between Profits and “Adjusted” profits:

“Over time intangible assets from new acquisitions such as Audiencly will grow and according to IFRS accounting principles we must amortise these. This negatively affects net operating profit and we therefore decided to introduce Adjusted profit before tax alongside Adjusted EBITDA to better reflect the underlying performance of the business. Essentially, we add back amortization of intangible assets from acquisitions and FX effects to get Adjusted profit before tax. This quarter, the adjustment amounted to GBP 0.9m.”

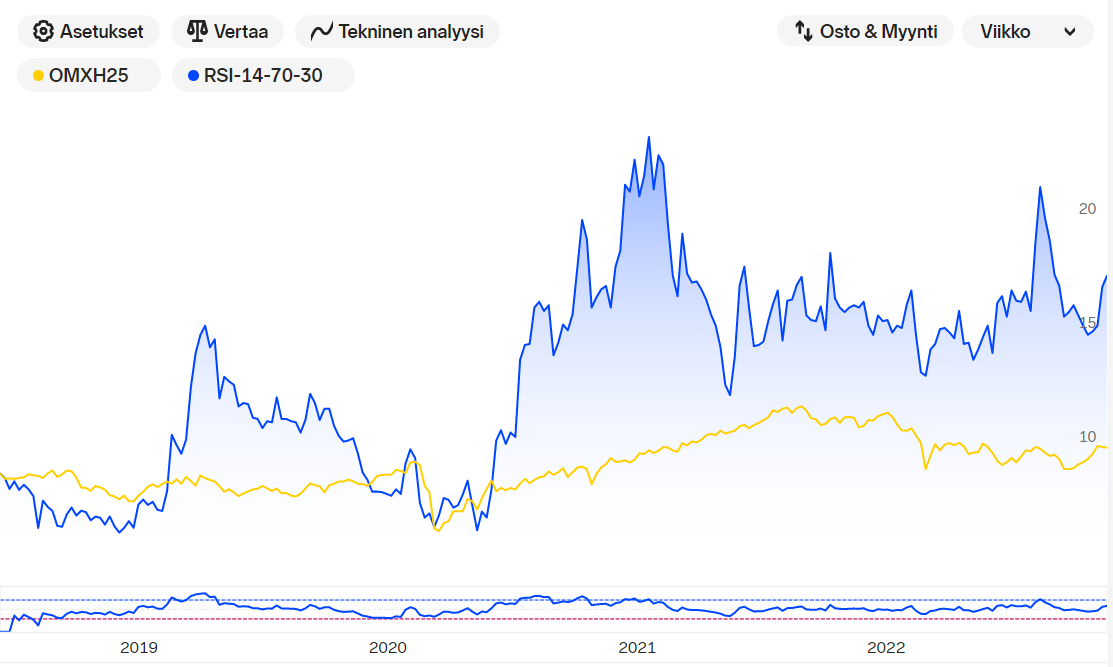

Development after listing (shares listed in Sweden, so price in kronor)

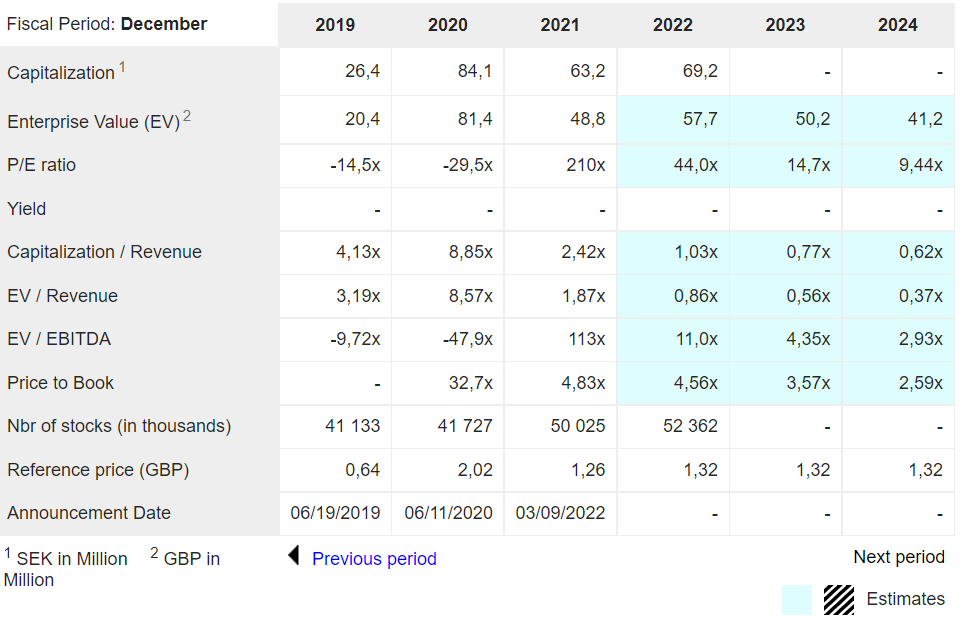

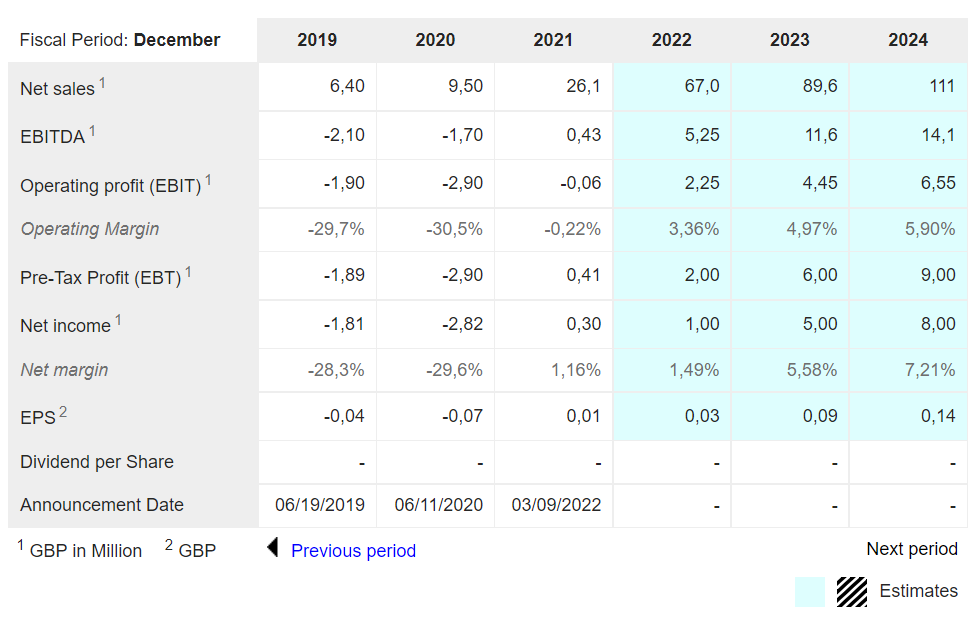

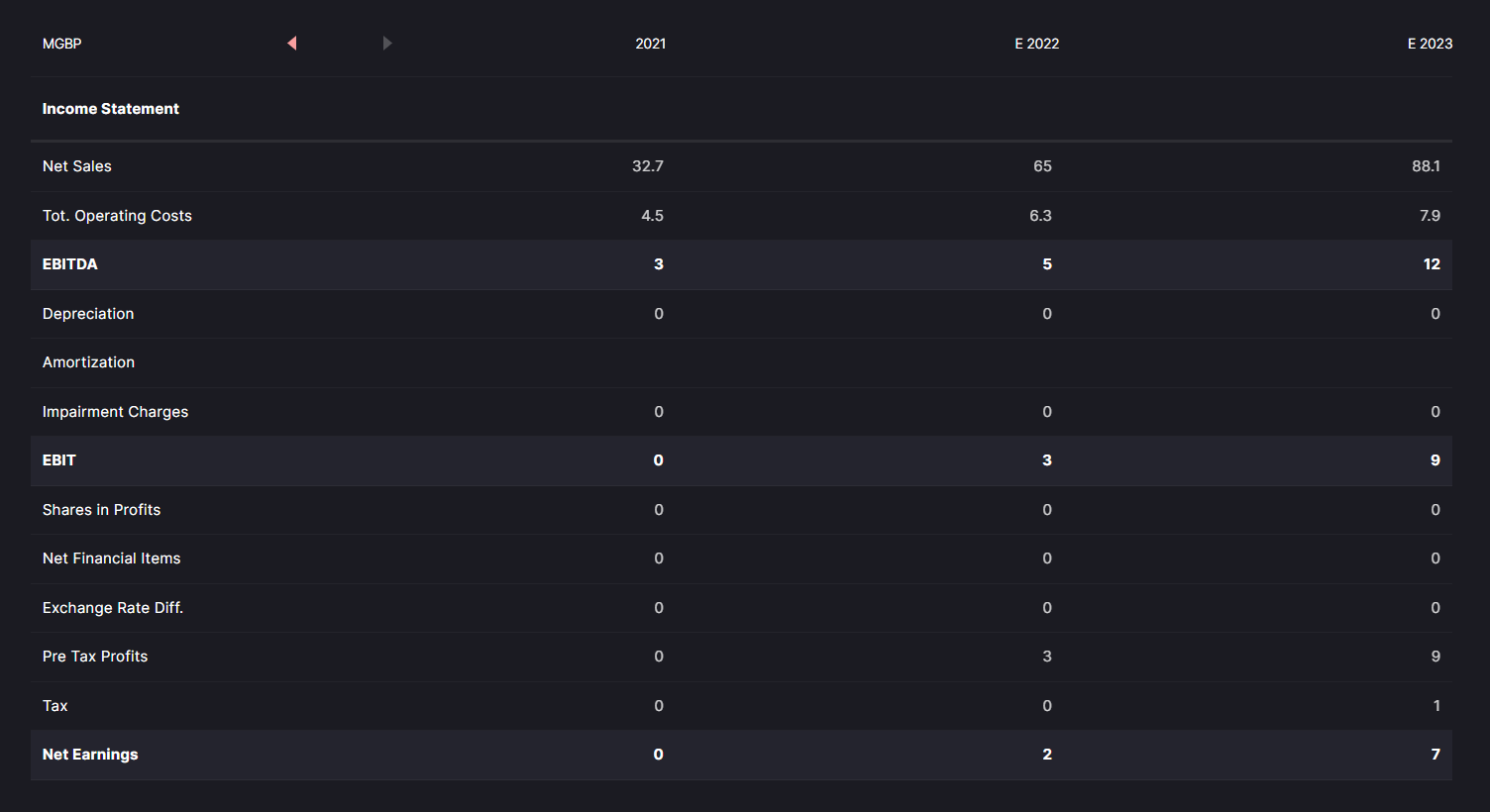

The company is also followed by RedEye. Whether that’s a good or bad thing, at least (revenue) forecasts have been exceeded recently.

Forecasts picked from Marketscreener: