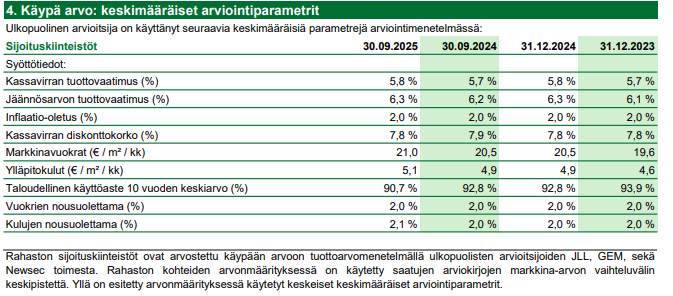

I spent some time digging through the numbers of our open-ended residential property funds  There are five open-ended residential property funds in Finland (OP, Ålandsbanken, Titanium, S-Pankki, and Aktia). I couldn’t find annual reports for Aktia’s fund, so I’ll focus on the others in this post. Unfortunately, materials are generally poorly available for these funds, and thus I have to make many assumptions in my calculations. Because of this, I don’t want to go into individual names here, but rather focus on the average of these funds. Data collected from the fund management companies’ annual reports and the funds’ own materials.

There are five open-ended residential property funds in Finland (OP, Ålandsbanken, Titanium, S-Pankki, and Aktia). I couldn’t find annual reports for Aktia’s fund, so I’ll focus on the others in this post. Unfortunately, materials are generally poorly available for these funds, and thus I have to make many assumptions in my calculations. Because of this, I don’t want to go into individual names here, but rather focus on the average of these funds. Data collected from the fund management companies’ annual reports and the funds’ own materials.

Let’s start with rental cash flows, which is the backbone of all real estate investing!

All funds imply in their marketing that the fund’s return relies especially on rental cash flows. The boldest fund even dares to say this:

Long-term return target is about 5–6 % per year, based mainly on rental cash flow.

I calculated the funds’ returns and expenses, and when looking at the fund’s cash flow after expenses (rental income – maintenance costs – fund fees – interest – other expenses), it’s noticeable that two funds are running quite ugly negatives in terms of cash flow, and two are barely in the black. Maybe 2024 was just the wrong year? For 2023, 3 were in the red and one in the black. Additionally, at least to my eye, it seems that for 2024, at least for two funds, the cost of debt is still too low (they made smart financing agreements back in the day), and when the interest rates eventually reset, that cash flow will turn even worse.

Let’s open up the math a bit:

On average, these funds get a rental yield of just over 5% (3.9-6.0%) on their property portfolio. For some funds, the interest on housing company loans apparently runs in maintenance costs, and therefore a comparison of exact expense lines is not possible. When netting out maintenance costs, other expenses, and interest, we reach a situation where the return based on rental cash flow for the entire property portfolio is on average 0.6%/year (-0.3 - 1.5 %) before management fees. So one fund is already cash flow negative before management fees. In this figure, it’s clearly visible that leverage is currently working poorly, and there are also problems with occupancy rates or rental levels. Naturally, property valuation levels also weaken this return. When management fees are then taken out of this cash flow, the average net rental yield for the property portfolio drops to -0.6 % (-1.7 – 0.2%). So in practice, the funds are on average cash flow negative after all expenses. None of these four generate a proper cash flow for investors through rental income. For comparison, I looked at the same figures for eQ Care (Social Infrastructure) (which btw now reports its information with first-class transparency: https://www.eq.fi/~/media/files/funds/eq-yhteiskuntakiinteistot/eq-yhteiskuntakiinteistot-talouskatsaus-q3_2025.pdf?la=fi), and there the return based on net rental yield is between 3-4 %. Of course, it’s good to remember here that the net yields of apartments are supposed to be lower than social infrastructure properties, but for the investor and the cash flow return they receive, this doesn’t offer much comfort.

What does this mean for investors? For investors, this means that these funds are currently leveraged derivatives of the housing market, and the return relies entirely on the value appreciation of the apartments.  Unfortunately, this part is not found in the sales prospectuses. How would these funds then start producing better for investors? Rental cash flow must be pushed up, with occupancy rates and rent increases at the center. In addition to this, financing costs should be brought down, but this is decided by central banks, not fund managers. Of course, managers’ fees also eat up an unreasonably large part of that rental cash flow (at worst, half of the net rental income), but touching these to improve the return is, of course, out of the question.

Unfortunately, this part is not found in the sales prospectuses. How would these funds then start producing better for investors? Rental cash flow must be pushed up, with occupancy rates and rent increases at the center. In addition to this, financing costs should be brought down, but this is decided by central banks, not fund managers. Of course, managers’ fees also eat up an unreasonably large part of that rental cash flow (at worst, half of the net rental income), but touching these to improve the return is, of course, out of the question.

It looks quite bleak for open-ended residential property funds at the moment if the interest rate level doesn’t change from here. It’s hard to see these instruments collectively being able to make a proper return based on rental cash flow without significant changes in the underlying market. Based on all this, those sales pitches about steady returns based on rental cash flow for investors are quite puzzling, when in reality the whole thing relies entirely on property value appreciation.