I’m a bit puzzled by Inderes’/Antti Siltanen’s target price setting. Is the target price of €2.5 based on the assumption that Faron will/will not get marketing authorization/a partnership deal for Bex, which is, however, the decisive factor in this story? What would be the target price if it does/doesn’t get it, and if it doesn’t, will everything then go down the drain, or will something valuable remain for the company? This way, one could better weigh the opportunities/risks. What would be the upper bound of a positive scenario/the lower bound price of a negative scenario? I would think that this would be valuable to many investors who are pondering whether this will succeed or not?

7 Likes

In the United States, 12,000–13,000 new STS cases are diagnosed annually, with the corresponding number in Europe being approximately 25,000. An estimated 40–50% of these are metastatic or high-risk patients requiring systemic treatment. Doxorubicin as standard treatment

Responses are poor: ORR ~14–20%, median OS ~12–14 months. Few new drugs have been approved (e.g., pazopanib, trabectedin, eribulin), but they are used later and offer limited benefit. Checkpoint inhibitors (PD-1/PD-L1) have failed in large cohorts → only small benefit in a few subtypes.

Global STS drug market: estimated 1.5–2.0 billion USD/year.

Bex + doxorubicin for STS:

- Immunosuppressive TME (tumor microenvironment) is a problem in sarcomas → TAM-reprogramming is a logical approach.

- PD-1 did not work, but NK cells and macrophages may play a key role.

Thus, there are good grounds for the BEXAR study.

25 Likes

Perhaps instead of just wondering about the target price, one could read the extensive report and analysis to get answers to all of these.

32 Likes

Inderes’ target price is based purely on a cash flow model, which only considers certain and modellable cash flows – and does not include potential partnership agreements or acquisitions.

If one believes that negotiations for a partnership or even the acquisition of all of Faron are already underway, the DCF calculation has practically very little significance. In such a case, a more credible valuation method is to compare completed deals and to assess what kind of terms Faron could achieve in a similar situation.

13 Likes

Faron does not have a single

5 Likes

Let me correct this a bit so that no incorrect impression remains. In our model, Faron’s revenue is based on partnering and consequently on license revenues. Upfront and milestone payments are assumed to be equal to Phase 3 costs. In other words, the model does not include upfront or milestone payments from partnering NOR Phase 3 costs. I think it’s a reasonable assumption that the payments are in the same ballpark as the study’s implementation, especially since there has been no concrete information about Ph3 implementation and costs before the news of recent weeks.

37 Likes

Thank you. So, does Inde’s logic now go like this:

Inderes’ analysis of the future has always been that a partner deal will come, otherwise royalties would not have been modeled. The probability of a deal has been estimated using the probabilities of passing statistical phases, and cash flows similarly.

In a partner deal, Inde assumes that the partner pays for Phase 3, but nothing else comes, no upfront payment and no milestone payments. Faron would thus have to seek financing for all its other operations for the coming years by making additional drawdowns on the already agreed bond and through share issues. This has been a contentious view on the forum. Have such deals, where no one-time payments are made, been done anywhere? Or would Phase 3 financing cover Faron’s operating costs during the Phase 3 period? It’s not entirely insignificant whether “we’ll be in trouble again soon anyway” or “this is how they usually go” is modeled, and with what probability.

Of course, in terms of absolute amounts of money, it’s the same whether financing to secure operations comes at the beginning or later, but it’s probably clear that money in the near future is clearly more valuable to current owners than later money? As I wrote earlier, there is some probability for some milestone payment and upfront payment. Just like for royalties and phase progression.

Antti_Siltanen:

“I think it’s a perfectly reasonable assumption that the payments are on the same playing field as the implementation of the study, especially since there was no concrete information about the Ph3 implementation and costs before these news items of recent weeks.”

This sentence implies that a reasonable assumption was based on the fact that there was no information earlier. Is there now? And what does that lead to?

20 Likes

Indeed. I would also add that Faron is unlikely to accept a partner deal that fully finances P3 regarding the upfront payment, simply because it also secures the interests of key owners and retail investors in the deal – meaning it won’t accept dilution after the partner deal. As development progresses positively, at least one new cancer value stream (P2/P3) should be added to the model with at least a small probability, not to mention the potential monotherapy of clever cancers with different cytostatics. This is certainly taken into account by Faron, already with the first partner/deal in mind. By all accounts, more value streams are therefore coming within a couple of years, at least one if not more, right? Shareholder value must be developed at the earliest possible stage – anything else would be strange. Well, Inderes’ estimate is an estimate, although it does have a guiding effect initially. However, reality will likely be something else.

5 Likes

I understood the part “Advance and milestone payments are assumed to be equal to Phase 3 costs.” to mean that the size of the advance payments cannot be estimated so precisely that it would have a verifiable significance for the calculation. Consequently, it is assumed that the company’s costs can be covered with advance/milestone payments, but it has no significance for the owner’s income (e.g., dividend). Income generation then occurs through the finished medicine (royalties). However, I might be wrong.

9 Likes

Exactly. As I wrote in the last report and on the forum, the near-future situation is quite binary, and in my opinion, it is very difficult/impossible to create added value by taking a stance. I mean that the realization/non-realization of the deal, its schedule, and its size are things that I cannot reasonably estimate in advance with sufficient accuracy. Therefore, regarding financing, the situation is more like “let’s see what comes and go with it.”

This phase 3 modeling reflects the same thinking. That is, to take a neutral starting point regarding the implementation and financing of the study.

18 Likes

This might be over-analyzing it, but one would think that when partnering, compensation would also be desired for the already completed Phase 1 and Phase 2 work, in addition to covering the costs of Phase 3. And then, indeed, flexibility for expanding the use of bex into research for treating other cancers.

6 Likes

I agree. Bex definitely has more value than its third phase costs. Faron would not make a deal where the rights to the drug are relinquished at a so-called “buy-in price” that also includes previous costs. A potential partner will certainly also have to pay some premium for future cash flows. I understand that calculating that “goodwill” is very difficult, but in my opinion, it cannot be completely left out of the equation. Somehow it should be possible to estimate it. Perhaps by benchmarking against previous drug indications?

2 Likes

Could this now be explained in a video, what your analysis actually contains. How are Phase 3 deals generally structured and what size are they, and what is the probability of Phase 3 where drug candidates usually fail, does Faron have better probabilities than average. r/r market vs total pool

Fixed market size, has it been included in the DCF model and the probability of success.

2 Likes

If we flip the way of thinking;

What would be the things that could and should go wrong, so that Faron fails with blood cancer and so that BEXMAB does not become a medicine, or it does, but mistakes are made with contracts, resulting in poor value for the company and shareholders?

Of course, we are now first waiting for FDA approval from the US, but with side effects being so mild and results being good, I expect approval for phase three.

Behind which turns are which crosses?

And what if one dares to start painting with a really big brush, what are Faron’s chances of becoming a truly big product with great significance for the national economy, especially if solid blood cancers start to enter the portfolio?

I don’t know if this is a completely stupid idea to list these in one place. The admin should remove it if so.

A lot of this information is scattered here. Especially since the old forum reached the ‘ten club’ and retired.

3 Likes

Doesn’t the compensation for previous development work come from royalties when the drug is on sale? Of course, there could be some other upfront payment on top of the phase 3 development costs, especially if the agreement also includes other indications.

3 Likes

I’ll answer this now, then I need to focus on other matters. I’m looking at this from a high level, and there are so many uncertainties that I don’t find it meaningful to try to make a seemingly accurate estimate like this. It would go so badly wrong otherwise.

-

Don’t forget the portion of licensing fees, which is equally part of that deal.

-

Faron naturally aims for maximum results in negotiations. On the other side of the table, there are their own goals. An agreement is then reached on these, or it is not.

Extensive report.

Links at the end of this article.

7 Likes

I see it this way: the drug candidate (currently 100% owned by Faron) has been divided into five parts, and four of those are being sold to a potential partner. The fifth part remains with Faron (license fees). Faron does not receive royalties in the deal, but Faron keeps a

10 Likes

I understand Inderes’ starting points and assessment, but for Big Pharma, it probably doesn’t matter what assessments we make right now. Bex has now proven its worth and the FDA has given its approval.

The ball is in their court, and they consider things only from their own perspective:

- Will Bex cannibalize or grow the markets for our existing drugs?

- Is this just a niche addition, or can it open up an entirely new treatment class?

- Is Bex truly “first-in-class” or the next combination component?

- Can Bex become a “game changer” that alters the standard of care?

- Does this fit directly into our current oncology portfolio?

- Can we combine this with our own checkpoint/IO drugs and increase their value?

- How do biomarkers support targeted use and reduce the risk of failure?

- How large is the total market if Bex expands from MDS/AML to solid tumors?

- Is it worth buying now at a lower risk, or waiting and paying a multiple of the price?

- If a competitor snatches this, what does it do to our strategy?

Based on these, an offer will be made/they will participate in an auction, and the price will be accordingly.

40 Likes

And 11: What is the probability that Bex will become an approved and marketed drug for any indication?

This probability is nowhere near 100%, which often gets forgotten in many posts. It wouldn’t be 100% even after a successful Phase III. My own target prices will certainly differ from Inderes’s target prices if risk adjustments are not made ![]()

20 Likes

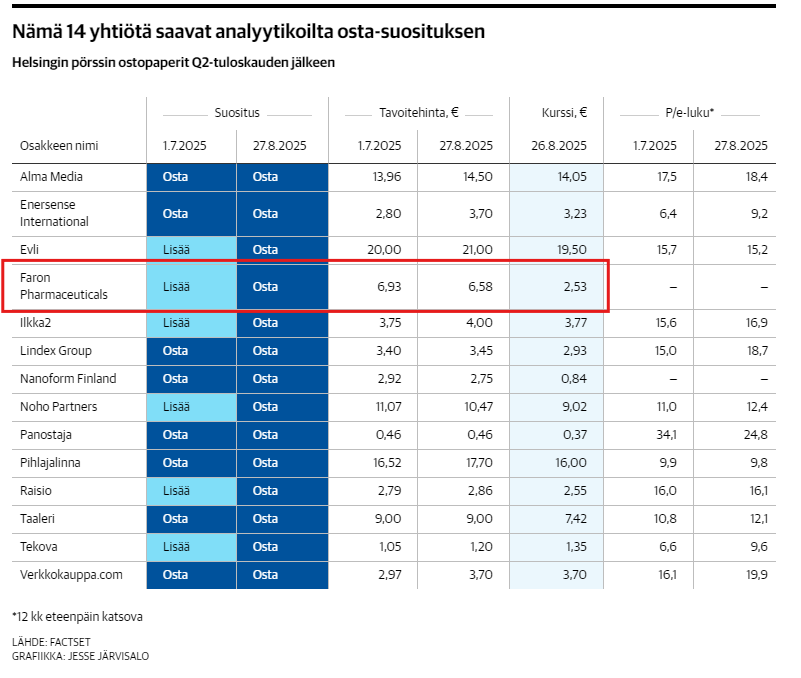

In Kauppalehti’s article, high target prices have already been set for Faron by analysts: https://www.kauppalehti.fi/uutiset/a/241caa86-0da1-438b-9cdc-d44b11acf51c

16 Likes