Last week, HCM received over 3.5 million shares as repayment for a convertible bond at a price of €0.4516, and in addition, roughly 17 million shares came from the issue at a price of under €0.4, taking the underwriting fee into account.

The share price performance looks quite challenging in the short term, as HCM now appears to have moved to the sell side.

In HCM’s case, it was a flagging notification on April 17th for dropping below 10%. Had they sold 4,453 fewer shares, they would have remained above the 10% threshold.

On April 17th, over 1.2 million shares were traded at an average price of 0.5003 during an intraday rise, with a close of 0.505 and a daily high of 0.515 EUR.

HCM’s reduction was -268,915 shares, so they actually sold very little, and potentially their entire reduction was above 0.50.

If not HCM, then one of the guarantors sold after that, taking the price even below 0.48, but they aren’t all panicking and hitting the bid levels simultaneously.

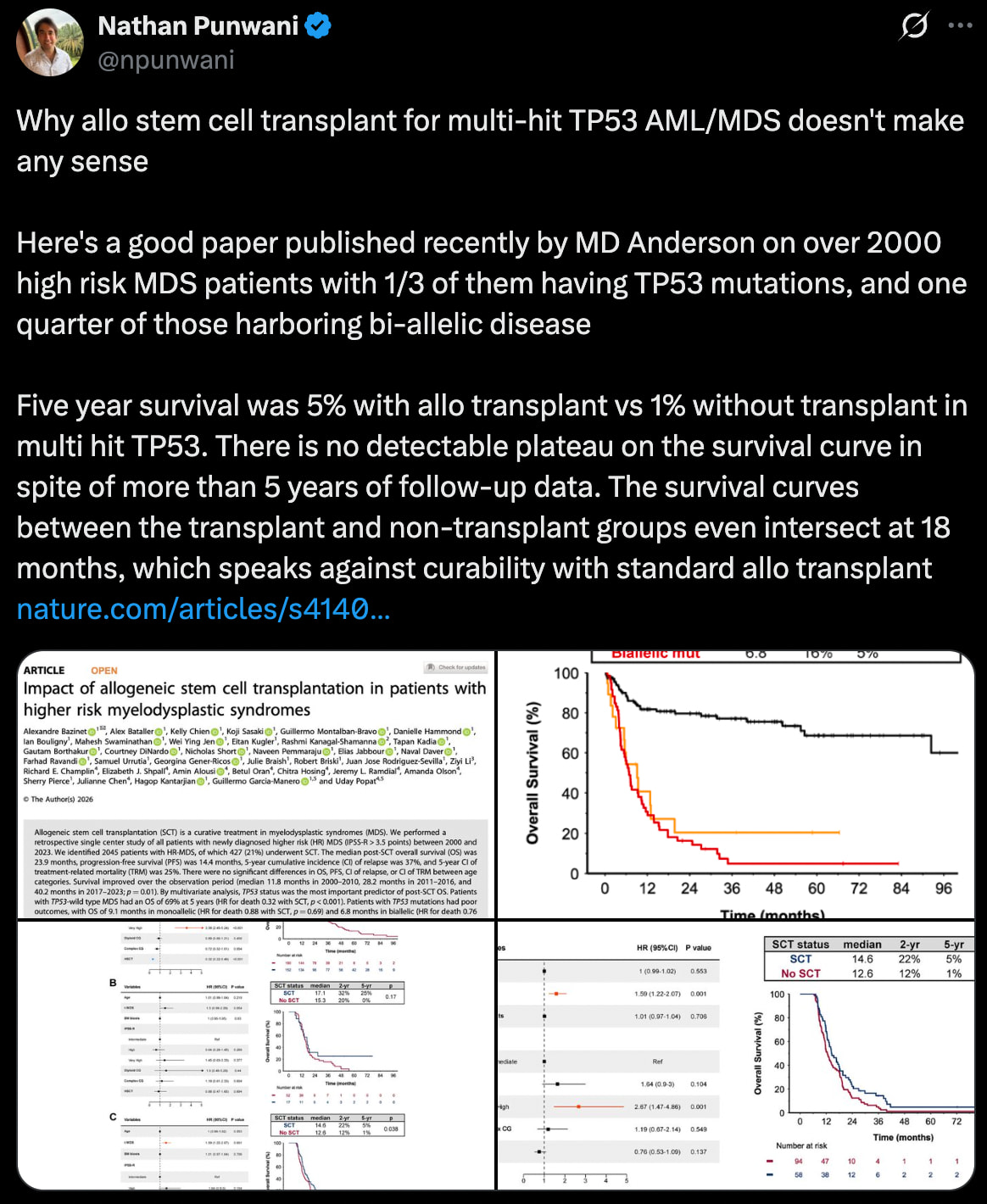

This summary paper of over 2,000 stem cell transplant + (Venetoclax + Decitabine) patients tells a grim story and illustrates well that the problem isn’t even just SCT itself, but what happens after it. Maintenance can clear MRD and improve the prognosis, but TP53 disease is usually not cured… not even with SCT.

Bex is on the right track because it could reduce macrophage-mediated immunosuppression and thus strengthen the efficacy of the graft’s immune cells (GvL effect) while Ven/Dec handles the last remaining cancer cells.

A layman’s attempt to understand: Is it the case that BEX doesn’t bring a better sword to the battlefield, but rather strips the enemy of their shield?

Or at least tries to.

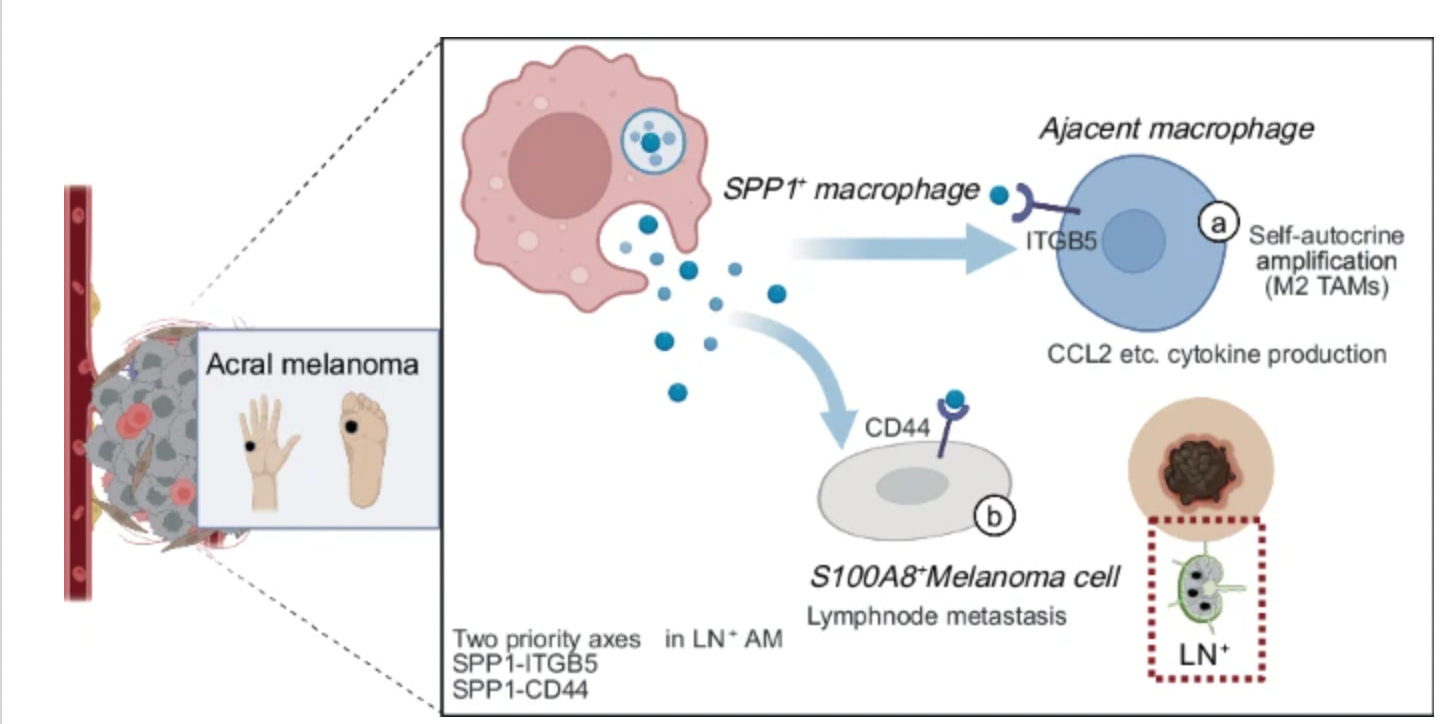

A recent SPP1 paper strongly supports the BLAZE case: SPP1 macrophages drive melanoma metastasis while building an immunosuppressive environment via the CD44 axis. This explains why some patients no longer respond to PD-1 therapy, even though T cells are still present in the tumor.

SPP1 is one of the suppressive signals produced by macrophages, and Bex targets the macrophages producing this at an upstream level.

Faron’s BLAZE trial tests this exact mechanism: PD-1 activates the T cells and Bex can reduce macrophage-mediated suppression.

And once again, a new HCC paper that further confirms the SPP1 mechanism:

High SPP1 is associated with a poor prognosis, increased M2 macrophages, and decreased CD8 T cells, i.e., a classic immunosuppressive TME.

In practice, SPP1 acts as a biomarker for macrophage-driven tumors.

…

Conclusions

In summary, this study demonstrates that SPP1 is highly expressed in HCC and correlates with advanced disease, unfavorable prognosis, an immunosuppressive tumor microenvironment, and distinct drug sensitivity patterns. Functional experiments reveal that SPP1 promotes HCC cell proliferation, migration, invasion, and survival. These results suggest that SPP1 could serve as both a prognostic biomarker and a promising therapeutic target, offering a potential direction for personalized treatment in HCC. Further mechanistic investigations and clinical validation are needed to advance SPP1‑directed strategies toward clinical application.

And another new one. An even stronger paper, this time on lung cancer. I’m sure at least the Chinese are knocking on Faron’s door.

This describes how macrophages are not M1/M2 but are divided along the CXCL9–SPP1 axis: CXCL9+ TAM activates T-cells and is associated with a good prognosis, while SPP1+ TAM inhibits immunity and drives tumor growth. And these are strange dynamic states between which macrophages can transition.

EHA is coming up on June 11–14, and the abstracts will be published on May 12. So, within about two weeks, we should have information on whether any new results from the BEXMAB study might be presented at the congress. According to the clinicaltrials.gov page, the study is expected to be completed in 04/26. At the very least, the mOS would be interesting to know. If it has risen in the r/r population from 14.5 months to, for example, → Not reached, it would be a very positive signal, which would definitely be reflected in the share price as well.

I don’t think this is possible (if I’ve understood correctly). That is, if mOS has already been reached once during follow-up, then 50% of patients have died, and thus a numerical value is obtained for the median(?). During follow-up, that value can then decrease, increase, or remain stable, depending on the remaining patients and their status.

This is indeed interesting. Faron has already communicated previously that the M1/M2 division is too binary, and macrophage immunosuppressiveness is more of a spectrum that depends on many factors. This provides a good understanding of what specifically is happening in the microenvironment. Looking forward to the next research results!

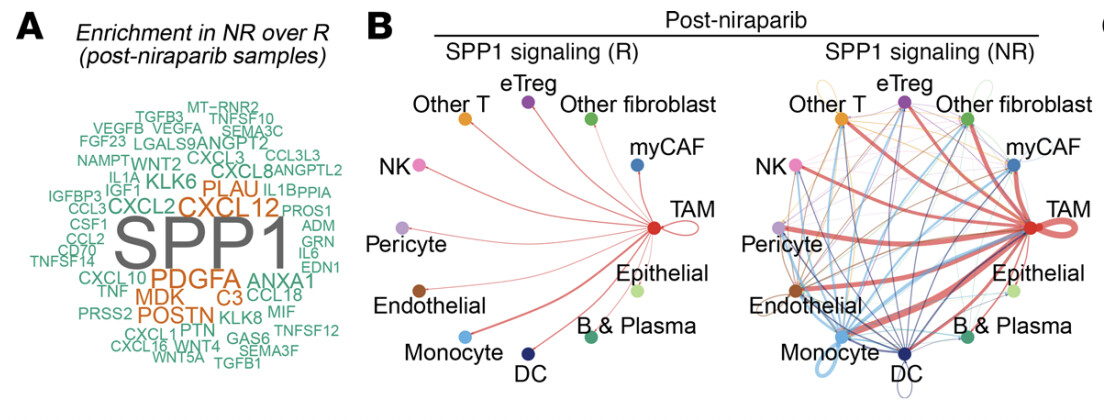

Similar problems with PARP treatment. Initially it works, but the treatment:

Causes DNA stress

IFN signaling up

Macrophages change

SPP1 up

Immune system shuts down

----> Resistance develops

PARP treatment creates an SPP1-mediated macrophage brake, and Bex can theoretically prevent this resistance mechanism. It would be a logical combination for Bex, at least based on this paper. There is no clinical data yet, but mechanistically it is one of the most sensible combinations.

PARP treatment is widely used in ovarian cancer and partially also in prostate cancers.

I have been under the impression that mOS could still increase → not reached. Don’t censored observations affect this? Now, some Kaplan-Meier expert could give an opinion on this.

The author of the chart hasn’t bothered to report the confidence interval of the estimate for the whole population, which would be standard practice (it’s split by TP53 status), but yes, the final result could change in either direction. By a quick count, there are 15 censored cases.

edit: bear in mind that most of the censored cases are on the worse side of the median estimate. So, it’s still wide open.

Of the censored ones, 6 proceeded to bone marrow transplant, so 9 were censored for some other reason. And at around the 1200-day mark, even the last patient was censored. (I wonder if that is the data readout moment 11/2025?)

Follow-up seems to have ended in death for 17 patients (of which 6 were non-TP53 and 11 were TP35).

If there are errors here, feel free to correct them.

Personally, I see a major risk regarding these cancer drugs that extend life expectancy by less than a year on an expected value basis: that they will no longer be purchased with public funds in a tightening economic climate.

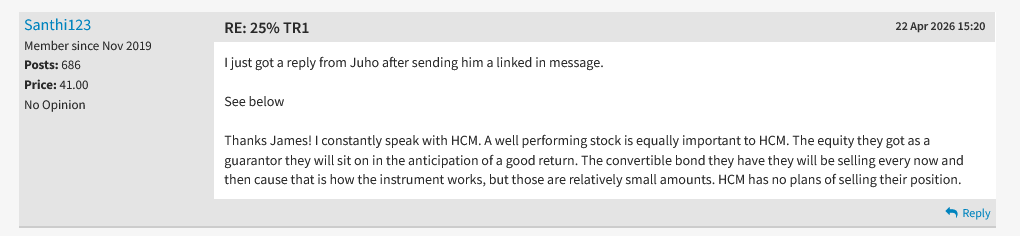

On the Nordnet forum/Shareville, it was reported that Juho had commented on HCM’s sales to some random British investor. A post regarding this can be found on the London forum:

I haven’t seen a new drug in a while that improves survival by more than a year compared to the standard of care.

Daraxonrasib is the biggest news this year, with an mOS of 13.2 vs 6.7 months. And that drug will sell billions.

The biggest risk and expectation with Faron is simply that the drug doesn’t work. Without controlled data in BEXMAB, we are in uncertain territory; there was no monotherapy efficacy in MATINS, and the mechanism of action of the Clever-1 antibody is not convincing.

This is quite extraordinary stuff. Firstly, that is price-sensitive information, and secondly, one would truly believe and imagine that these partners have an NDA. Thirdly, as you state, there are already these disciplinary tickets from way back waiting for a verdict.

When will we hear some good news from Faron? Someone in the know could tell us — it’s been a really long time. IMHO

Even though expensive cancer drugs are rationed in “dirt-poor” Finland, in the USA and elsewhere, (insurance companies) have plenty of money for costly treatments. In this case, too, the goal is likely to overcome cancer in the best-case scenario. And if that is not possible, then to ensure the highest possible quality of life for the remaining time.