TL;DR We reiterate our base case valuation of EUR1 per share (0.30-2.30)

We acknowledge the potential market pressure from short-term guarantors until it is digested. We reiterate that the additional directed issue (the side pocket Juho mentioned) will not be carried out in connection with this issue. The conversion of IPF’s old warrants according to the rules to the new price slightly increases dilution.

Let’s see how the meeting decides. Even in Aiforia, the board proposed it, but the general meeting did not allow it, at least not yet at the ordinary general meeting.

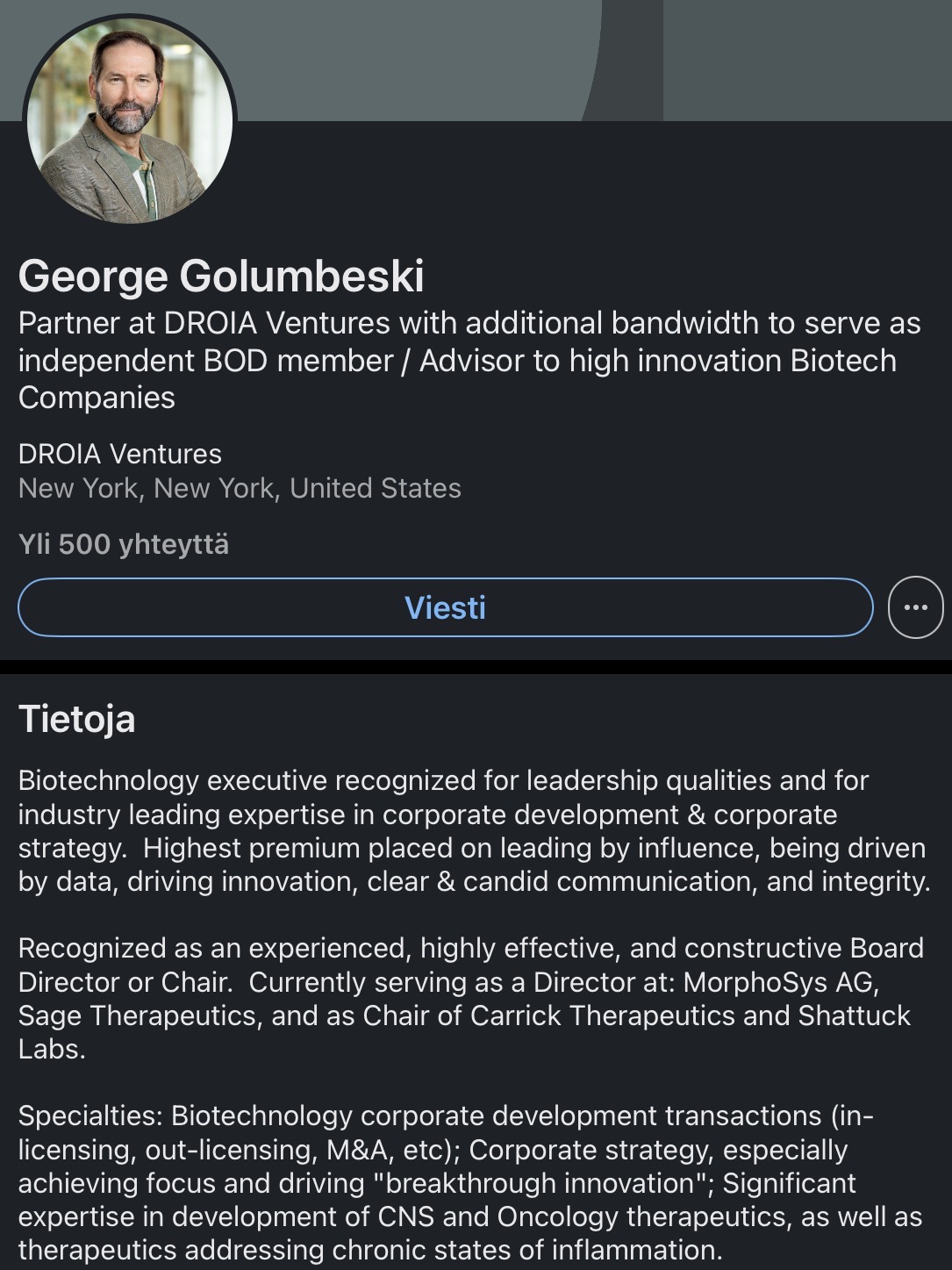

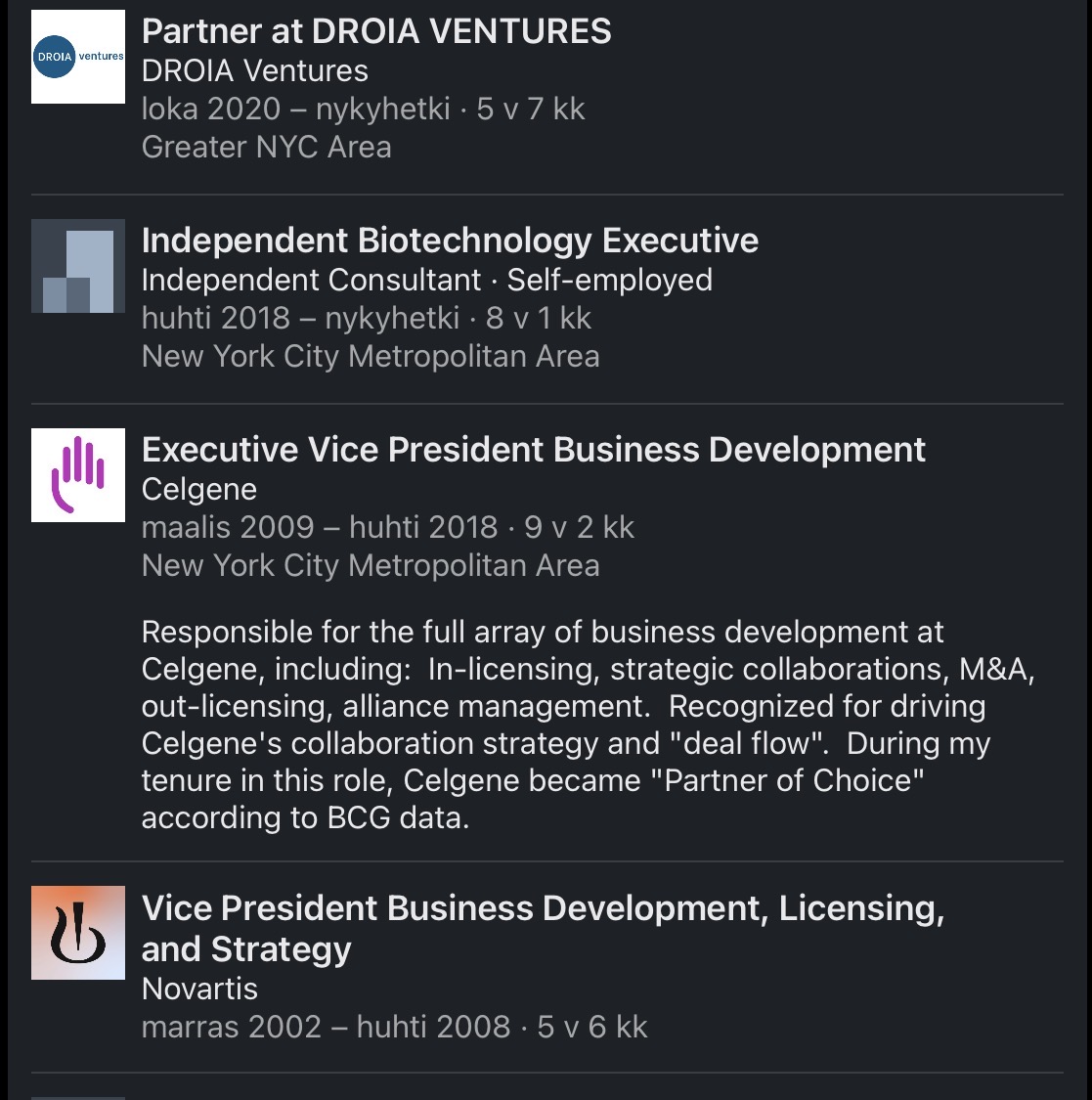

For those for whom Jalkas exposure has been too much, Markku will also be leaving the board. Poulos as well, but they will be replaced by dealmaker George Golumbeski, with a background at Celgene and Novartis. Now the deals are no longer dependent on the people but on something else entirely.

The ERCC6L2–TP53 paper strongly supports the idea that AML (especially TP53) is not just a mutation, but a dynamic stress and evolution problem. The disease is constantly evolving, not static.

This fits well with clinical data, where responses are achieved but OS remains at the 10-month level. Simply killing blasts is not enough; the microenvironment also likely plays a significant role in the duration of the response.

This paper includes Finnish researchers and Mikko Myllymäki, who was just on TV with Juho and is also involved in BEXMAB studies. Of course, this is not proof of anything, but it indicates that the same group investigating the core causes of AML is also involved in developing its treatment.

That article’s references contain a surprising number of Finnish names. I’d like to ask those more knowledgeable if TP53/p53 is somehow a Finnish specialty?

Amazingly, Juho and co always manage to get the best people. A really strong recruitment.

Celgene acquired Azan from Pharmion for 2.9 billion and scaled the drug into a global MDS and AML standard, making it a significant market from a business perspective. Aza + whatever.

Golumbeski wasn’t at Celgene at the beginning, but he advanced and got to develop/acquire the next breakthroughs on top of that… and it seems he found something this time too. Bex is a good candidate, at least.

If a Faron investor attributes any chances for AA approval for r/r MDS (as RedEye’s €1 base case might imply), they should read this CRL that Replimune just received from the FDA. The setup is the same as Faron’s: combination therapy, where a previously approved drug + investigational drug, and although there were 2 studies, neither had a control group.

Bex/Bexmab ticks quite a few of the same boxes that were highlighted as problem areas in the CRL letter. The FDA does not seem to value such applications.