Currently, 28% of respondents plan to hold onto their shares. So the remaining 72% plan to sell a portion. There could be quite a lot of selling pressure due to that news.

12 Likes

We’ll see what kind of partner deal it turns out to be, if it happens, but from what I’ve been thinking about it, I don’t think there will be any +200-300% share price increase due to partnering, because Faron is already priced quite high. However, I answered that at most a third would go on sale, because I am somewhat overweight and since that valuation range was given, at that point I would be ridiculously overweight and no longer in my comfort zone.

We small investors are quite a small factor in this whole picture, and I think that if partnering were to happen now, there might be new funds coming in as funds can adjust their estimated risk levels lower (rules allow investing) and existing ones can increase their positions, so I’m sure buyers will be found even if half of the small investors put their shares on the market.

My own belief in partnering was somewhat tested during the June earnings call, but this latest update raised the probability high, and I’m not worried at all anymore, it’s just a matter of time.

EDIT: The biggest risk I’ve considered is what Rushimato also wrote earlier, that Faron’s management considers this so valuable that they price themselves out. But Juho’s latest interview was already a bit more humble and emphasized the importance of partnering at this stage, and that they are now seriously negotiating. Then just the best available and move forward with that. That would immediately put an end to dilution fears.

28 Likes

More concerning here is that the whole company doesn’t go too cheaply because Bex is at the top in the TAM field. The market can be huge, and there’s nothing to suggest it won’t succeed. Safety and responses are okay.

Comparison of TAM Therapies

| Candidate | Target | Mechanism | Development Phase | Issues/Notes | Status Today |

|---|---|---|---|---|---|

| Pexidartinib (Daiichi) | CSF1R (tyrosine kinase inhibitor) | Eliminates TAMs by reducing CSF1 signaling | Approved for TGCT, did not work in broader cancers | Hepatotoxicity, lack of efficacy in solid tumors | Approved only for TGCT |

| Cabiralizumab (BMS) | CSF1R (antibody) | Reduces TAM population | Phase II, combinations with PD-1 | Weak efficacy, adverse effects → program terminated | Terminated |

| Emactuzumab (Roche/Novartis) | CSF1R (antibody) | Same as above | Early clinical | Good responses in TGCT, but development did not continue | Terminated |

| Magrolimab (Gilead) | CD47 (“don’t eat me”) | Blocks cancer cell’s anti-phagocytic signal → TAM eats cancer cells | Phase III (MDS/AML) | Anemia, safety challenges; efficacy not sufficient | Development suspended |

| Lemzoparlimab (I-Mab) | CD47 | Same mechanism as magrolimab | Phase I/II | Partnership with AbbVie ended | Uncertain |

| TTI-621/622 (Pfizer/Trillium) | CD47 | Fusion proteins, release of phagocytosis | Early clinical | Safety issues | Slowed down |

| Anti-MARCO | MARCO (scavenger receptor) | Reprograms TAM → increases T-cell response | Preclinical / early Phase I | Still in early stage | Research phase |

| Oleclumab (AstraZeneca) | CD73 (adenosine pathway) | Reduces immunosuppressive adenosine in TAM/TME | Phase II | Efficacy not yet a breakthrough | Research continues |

| Anti-CD24 (Merck / OncoImmune) | CD24 – Siglec-10 | Blocks cancer’s “don’t eat me” signal to TAM | Preclinical | Very early | Development beginning |

| Clever-1 (Stabilin-1) | Reprograms TAMs M2 → M1 (does not kill, but changes) | Phase II (registrational MDS) | So far good safety and promising responses | Field-leading “second wave” TAM therapy |

25 Likes

Investing would be quite a bit duller without a forum like this. New perspectives and reinforcement for one’s own views are available in abundance.

The share price increase brought by the partnership agreement is thought to be moderate, because that is already baked into the share price. That’s true, but with the partnership, the next big step will start to be significantly baked into the price. The entire value of the share is currently its expected value, and it will remain so until the end. The end in this case is either insufficient efficacy or the sale of Faron to a major player.

This story wouldn’t make an excellent movie, but it certainly keeps the interest of someone unfamiliar with the field.

I’m calmly drinking my morning coffee again and I wish the management endurance and an effective strategy for the negotiations.

21 Likes

On Views Regarding Partnering

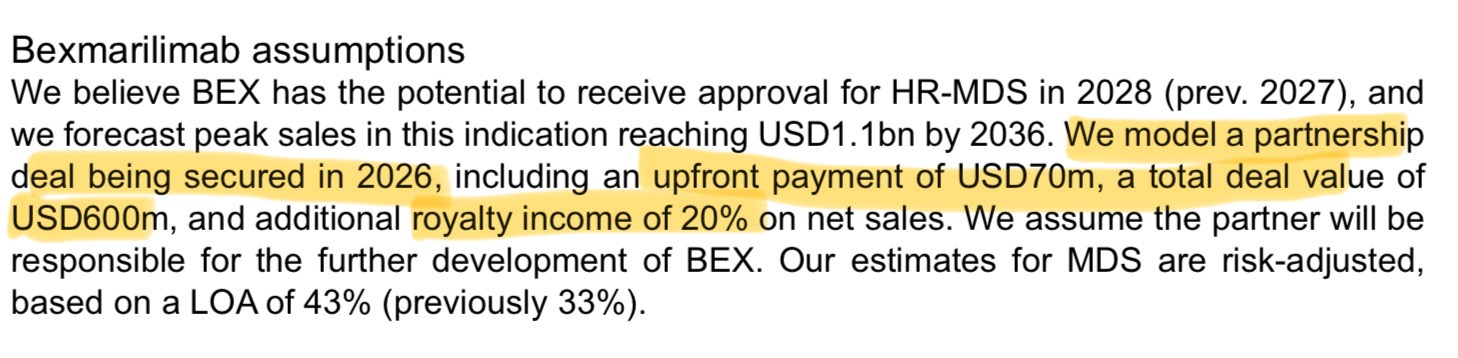

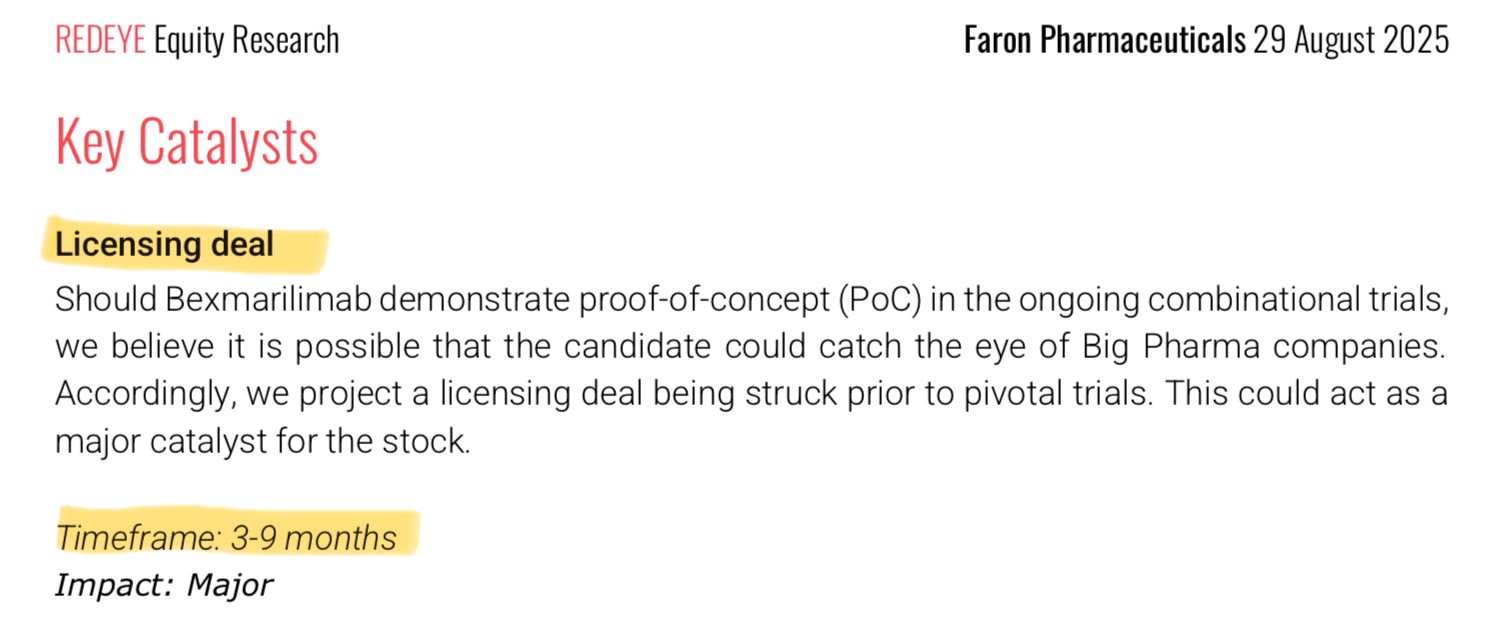

Carnegie (licensing in practice for MDS) 28.8.25:

RedEye (MDS emphasis in licensing) 29.8.25:

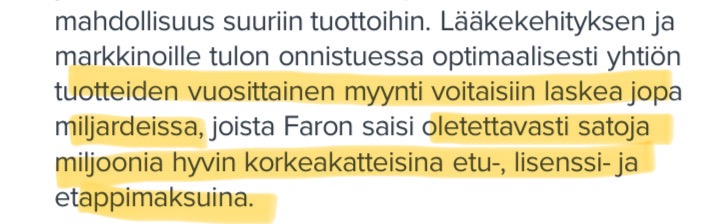

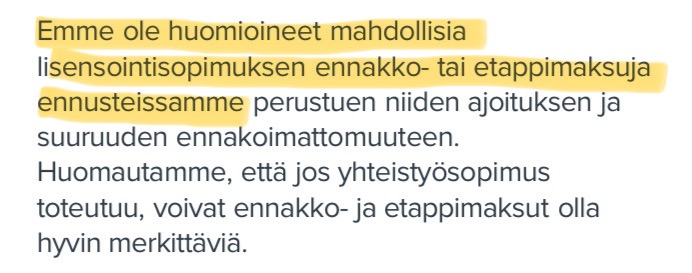

Inderes comprehensive report (takes a stance on everything and nothing except royalties) 13.11.23:

But its probability, by any percentage, is not taken into account. “Because it is not verifiable.”

The cash flow could also include a potential partnering upfront payment. And milestones. These are a critical factor for valuation. There is some probability for some amount. Each can calculate with their own numbers. For example, like this: In Dandelion Yard Capital ![]() we

we ![]() estimate that Faron will receive a 200 MEUR upfront payment for MDS/AML indications with a 50% probability (=100 MEUR, and with it comes the possibility to run the company for several years without fear of dilution). Just as there is some percentage and probability for royalties from some amount. Royalties mean partnering, which means an upfront payment and milestones with certain probabilities.

estimate that Faron will receive a 200 MEUR upfront payment for MDS/AML indications with a 50% probability (=100 MEUR, and with it comes the possibility to run the company for several years without fear of dilution). Just as there is some percentage and probability for royalties from some amount. Royalties mean partnering, which means an upfront payment and milestones with certain probabilities.

28 Likes

Now it’s time to go into hiding for five years and then in 2030 see what the stock price looks like. My own shares are at an average price of 2.01€, and I don’t intend to sell them for hopefully several years. Let the windbreakers flap and keep a cool head when the news comes.

13 Likes

One significant question for me is what happens at Faron while waiting for a partnership, now that Phase II has been completed and Phase III will only proceed once a partner has been secured. How long will Phase III be delayed if it takes months to find a partner (and the goalpost is moved again)? And there’s no time to wait for months, because money is constantly being burned.

Of course, more results are constantly coming in, but time and money are being wasted now while in this interim state. Certainly a normal situation in drug development, but still, if there is faith in Bex and a crying need for the treatment, then these delays are undeniably puzzling.

6 Likes

Preparatory work for Faronilla’s phase 2b/3 is probably underway now; such work is not done in a few weeks. In addition, preparatory work for FINPROVE, Blaze, and Bexar is probably also keeping busy…

9 Likes

The poll didn’t have many options, but more specifically, I might consider lightening my AOT position by 500 Faron shares at prices around 5-7€. These were acquired around one euro before the offering. The AOT would be left with 2000 public offering shares, which I’d hold to the finish line, without pressure, as a loss would no longer be possible. Actions would depend on the situation and outlook; it’s not certain I would even sell at that point.

On the OST (share savings account), I have a larger pot of just over 7k shares; I probably wouldn’t do anything with these. I have cautiously traded with the position, but the direction is mainly to add more.

Faron is an all-or-nothing investment for me; I want its full potential to be squeezed out, and if it ultimately collapses, then so be it. High risk, high reward, and entirely my own choice. My other investments are much more conservative, with lower return expectations and risks.

15 Likes

Speculation around Faron is progressing nicely. I don’t know if Warren Buffett’s view on the matter brings any relief: “An investor is interested in the future of the business. Speculators try to predict what will happen to the stock price.“

4 Likes

Regarding partnerships or the general setup of Faron’s sale: There are certainly hundreds of small pharmaceutical development companies in the world. The exact number is not essential.

Large pharmaceutical companies certainly want to grow their revenue, and that’s why they acquire these smaller companies or the drugs they are developing.

So, a large pharmaceutical company has options and no obligation to cooperate specifically with Faron. Faron, on the other hand, is forced to bring in an external financier or dip into the current owners’ pockets. Of course, there are fewer companies aiming to enhance the effect of certain cancer drugs, meaning if a large pharmaceutical company needs such a thing, there are fewer potential small development companies.

What still bothers me in this setup are the statements made years ago by father Jalkanen, according to which large pharmaceutical companies were practically competing for Faron. Misleading talk, unless they were competing to get it for free or for a negligible amount of money, and that was left untold to us.

It’s unfortunate, in a way, that now son Jalkanen has to bear the credibility deficit from father Jalkanen’s soft talk. And not just regarding partnerships, but apparently also with the shifting of schedules. Although, of course, son Jalkanen was already involved back then.

9 Likes

This also summarizes my own thoughts well and why at this point I have cautiously started to become more skeptical about Faron. If a partner had been ready for signing when the Phase II results were obtained, I would not hesitate at all. Then Faron would have been in the driver’s seat. However, the truth was different, and now if a deal is pushed through aiming for maximum profit, it might not be secured at all. The talk and the facts do not align at this point, and the reason for that lies solely with the company management. If a share issue is needed, money could be really, really tight when faith starts to run out due to endless unfulfilled promises.

12 Likes

The work is now done and it’s time for the deal, which is exactly the point they have wanted and aimed for. The next studies are largely outsourced or done by someone else. Business mastermind Juho really knows his stuff, and in the interview, pride in Faron’s current achievements shone through. Of course, there’s talk of partners and money pots, but surely Bex will be moved forward under another company’s name after some time.

8 Likes

Right. I personally consider one biotech guideline to be: “if it requires a DCF for an investment decision, the upside is not sufficient”. One shouldn’t try to force an investment target to be profitable. Antti models 20% royalties, which could be argued to be at the upper end of the range as a single figure (I’m talking about Faron as a Phase 2 company in this context). But perhaps it is high if the idea is that all cash flows from the partner to Faron are covered by that one figure and a smoother DCF is obtained. If one wants to get fancy, everyone can model, for example, 15% royalties and appropriate milestones.

11 Likes

Perhaps Father Jalkanen was ahead of his time. I would also consider the situation more from the perspective of the big players, not just through Faron’s potential cash flow. So, do the big players really have the option to stand by if:

-

A large part of the revenues and future markets for MDS (perhaps also AML) shifts to others within 5 years?

-

PD-1 antibody patents expire and competitors take over the market with a PD-1 + Bex combo?

-

TAM reprogramming breaks through as PD-1 did years ago.

or, do they invest a few billion now in a Finnish asset whose:

-

Safety has been excellent

-

Phase II responses look like the best seen in the MDS field in decades

-

Scientific background is strong

So what would you do if you were the boss of BSM or Roche? Would you try to secure at least the MDS market/flank and would you want to conquer new areas now at a relatively low cost? Would you go to an auction?

I would. Deals have been made in the pharmaceutical industry from crazier starting points and at a high price.

24 Likes

Many will probably sell at that point, but at the same time, I believe some funds will become interested in Faron, which will also increase buying pressure.

10 Likes

The company has had an overly positive view of promoting the business. Although there have been contacts with big pharma, the message has not gotten through. At least not to the very top floors. There has never been any competition, that should be clear to everyone by now.

Now, in the autumn of 2025, investment bankers have been hired to push Faron for big money. A good move, although these guys could have been put on the task earlier. Now, personal relationships are being leveraged, allowing them to take the elevator a few floors higher when going to meetings. Also at this point, Hughes’ valuable experience from the other side of the table and from lobbying in general is available.

RedEye’s estimate for the lower end of the deal’s time window seems optimistic. If they are only now getting to discuss at a level that has even some power to decide on implementation, nine months is probably a more accurate estimate.

5 Likes

I was left wondering how the FDA’s requirement for the lowest possible dose hasn’t been known or taken into account earlier? Afterwards, however, it seems to everyone to be common knowledge and normal practice, especially with cancer drugs. Weren’t there previously 3mg and 6mg/kg strengths that were used to investigate side effects?

4 Likes

If I understood correctly, the FDA raised this after the phase 2 results because the results were so good. So the idea here is that such good results were achieved with a 3mg dose, that perhaps 1mg would be enough after all. Faron knows it’s not enough, but they don’t want to start arguing with the FDA about this and cause bad blood.

You seem to have very certain information about Faron’s internal affairs. And there’s a certain tone in the text, a hint of bitterness in the air?

Now is exactly the right time to seriously start looking for a deal. If a deal had been forced through a year ago, it would have been significantly worse than what is possible to achieve from the current position. I have been delighted to note that Faron’s management understands how to create shareholder value and does not agree to just any deal. Now they have such a promising drug in their hands that BPs (Big Pharma) take a big risk if they don’t participate in the auction.

17 Likes

There has never been any competition, that should be clear to everyone by now.

That’s a rather strong comment, please elaborate a bit. Competition doesn’t automatically mean that big players would climb on each other’s shoulders, throwing billions here, there, and everywhere. Each of them is certainly sniffing out and weighing different possibilities and business models; the field is huge, and everyone naturally wants to pick the cherry on top of the cake. Of course, the elder Jalkanen’s overly optimistic statements have been quite exaggerated, but “There has never been any competition” is quite a harsh assumption.

Of course, if you are an insider at the company and know this to be the case, it’s good to know as a shareholder.

7 Likes