Syksy näytti suunnan ja kurssi korjasi. Leuka rintaan ja eteenpäin. H2 on lupauksien ja väitteiden lunastamisen aikaa.

Ohessa jälleen päivitystä menneestä ja ajatuksia tulevasta. Kiitos @Antti jälleen hyvästä raportista ja haastattelusta. Se on ollut täällä hyvinkin tarkassa tarkastelussa. Arvostan työtäsi ja myös aktiivista otettasi foorumilla. Tätä ei kaikki analyytikot tee. Toivottavasti vastailet myös jatkossa kysymyksiimme.

Toivottavasti Juhon silmiinpistävä väsymys johtui aamutunneille asti venyneistä (partneri)väännöistä. Jos luet foorumia, etkä muista mitä tuli sanottua, niin ei huolta - ne löytyvät tästä!

Edellinen päivitykseni löytyy täältä. Koosteet ovat erityisesti itselleni (staying on track), mutta jaan ne mielelläni muidenkin kanssa. Saa kommentoida ja korjata.

9.7.2025 – Kaksi tutkimusta hyväksytty esitettäviksi IUIS 2025 -kongressissa (17.–22.8.2025)

- Suullinen esitys (BEXMAB, vaiheet I/II, MDS):

- Bex + Aza (kaksoisvaikutus)

- Kohdistaa Clever-1-reseptoriin ja aktivoi immuunivastetta.

- Parantaa nykyhoitojen tehoa.

- Posteri (sClever-1):

- Koholla oleva liukoinen Clever-1 heikentää T-solujen toimintaa ja liittyy anti-PD-1-resistenssiin.

- Bex estää sClever-1:n vapautumisen – uusi mekanismi, jolla voidaan purkaa immuunisuppressiota (immuunipuolustuksen heikentymistä/estämistä)

30.7.2025 – BEXMAB-vaiheen I/II data hyväksytty suulliseen esitykseen ESMO 2025 -kongressissa (17.–21.10.2025)

- Ensimmäinen kattava farmakokineettinen (PK) (mitä elimistö tekee lääkkeelle) ja farmakodynaaminen (PD) (mitä lääke tekee elimistölle) analyysi Bex + Aza HR-MDS.

- Tulokset:

- Bexmarilimab aktivoi immuunijärjestelmää ja parantaa luuytimen toimintaa.

- Lisää monosyytteihin liittyvää antigeenin esittelyä ja kasvattaa CD8+ T-soluja.

- ORR ensilinjassa 85 % ja 63 % r/r-MDS.

- mOS r/r-MDS: 13,4 kk.

6.8.2025 – Päivitetyt BEXMAB-vaiheen I/II tulokset ensilinjan HR-MDS:ssa

- Täydet remissiot (CR) nousseet 28 % → 43 % (9/21 potilasta – IWG2006).

- 43 % CR on yli kaksinkertainen verrattuna historiallisiin 16–17 %:n tuloksiin (Aza)

- Aiemmin raportoitu 50 % cCR (IWG2023) – yhä useampi näistä muuttuu ajan myötä täydeksi remissioksi.

7.8.2025 – Faron lyhensi vaihtovelkakirjalainaa

- Joukkovelkakirjan haltija voi halutessaan maksaa velkaa ennakkoon (“Accelerated Amortisation”) – enintään 2 kertaa per normaalin maksuaikataulun väli, ja ensimmäisenä vuonna maksuja voi olla enintään 9 kappaletta.

- HCM pyysi ennakkoon lyhennystä (Accelerated Amortisation) 1,682,067 €.

- Faron päätti käyttää Share Settlement Optionia, eli maksoi lyhennyksen HCM:lle osakkeina

- 857 322 olemassa olevaa treasury-osaketta annettiin HCM:lle vastineeksi lainan lyhennyksestä.

- Merkintähinta 1,962e

- Lisäksi yhtiö on maksanut toisen suunnitellun lyhennyserän käteisellä 2.8.2025.

- Joukkovelkakirjalainan uusi eräpäivä: 2.12.2027 (aiemmin 2.4.2028).

8.8.2025 - Uusi US patentti Bex käytöstä Clever-1-positiivisten syöpien hoidossa

- Alkuperäinen patenttisuoja olisi päättynyt 2037 – uusi ulottuu HEL/2040.

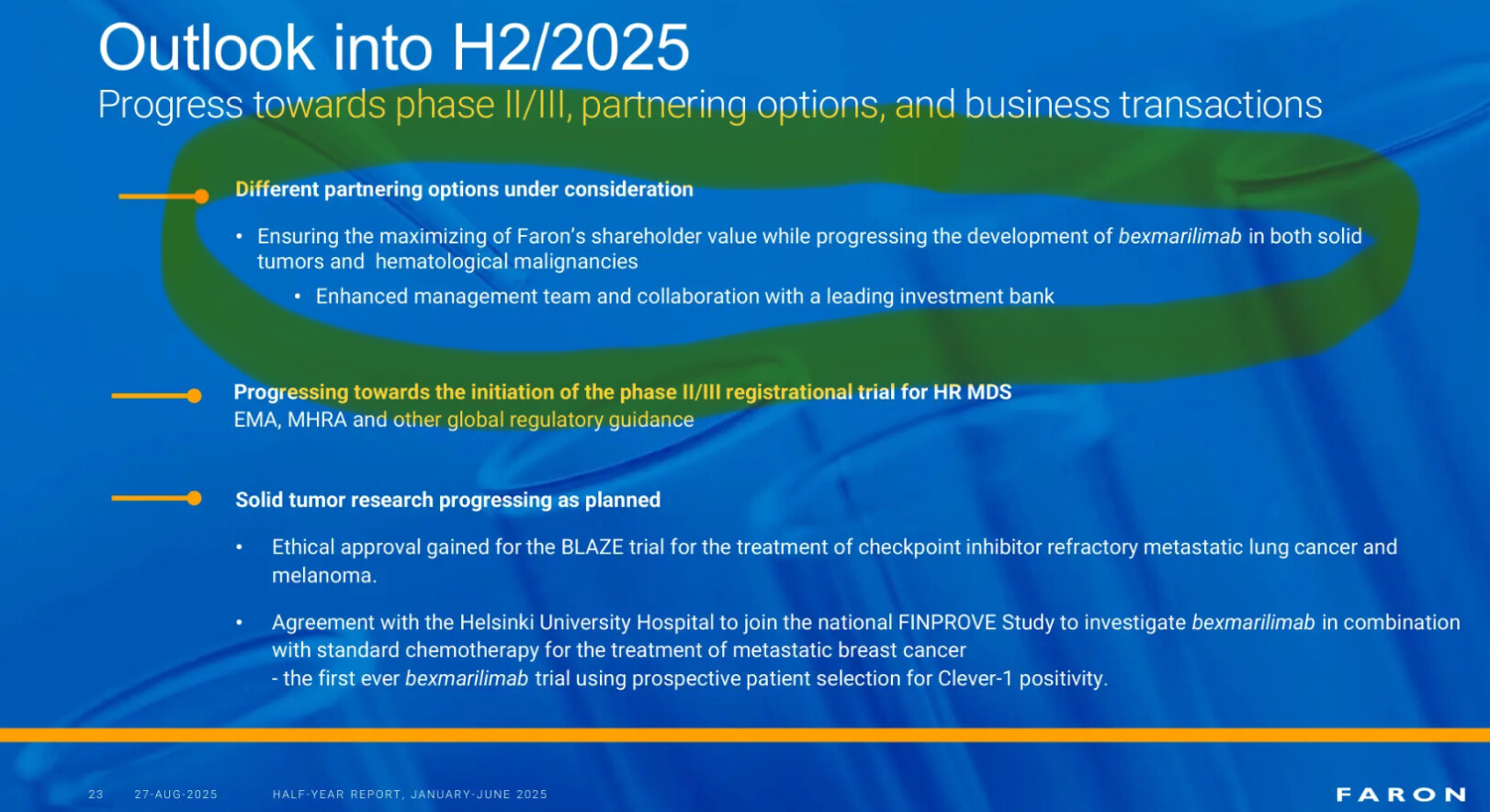

18.8.2025 - Eteneminen rekisteröintivaiheen vaiheen 2/3 tutkimukseen ensilinjan HR-MDS-potilailla

- Tapaaminen FDA:n kanssa.

- FDA vahvisti nopeutetun myyntilupa-polun (AA-pathway) ensilinjan HR-MDS.

- Päätetapahtumat (IWG2023) CR + CReq ja OS (kokonaiselossaolo) - Mitataan yhtä aikaa kahta tärkeää lopputulosta. Molempien perusteella arvioidaan lääkkeen tehoa.

27.8.2025 - Osavuosikatsaus (raportti), puhelu ja Biopörssi-Antin™ haastattelu

Taloudellinen tilanne H1/2025

- Liikevaihto: 0 M€

- T&K-kulut: 7,1 M€ (H1/2024: 6,7 M€)

- Liiketappio: -11,9 M€ (H1/2024: -11,3 M€)

- Tappio/osake: 0,18 € (0,20 €)

- Käteisvarat 30.6.2025: 13,5 M€

- Nettovarallisuus: -16,2 M€

- Business Finland antoi anteeksi 1,3 M€ R&D-lainan Traumakine-kehityksestä - positiivinen vaikutus H2/2025 operatiiviseen tulokseen.

- Ensimmäisen tranchin joukkovelkakirjalaina käytettiin IPF Partners -velan maksuun ja yleisiin yrityskuluihin → kassavarojen riittävyys Q1/2026 asti.

- Jäljellä lisäksi kaksi (10+10M) tranchia joukkovelkakirjalainasta

HR-MDS

- Faron etenee vaiheen II/III rekisteröintitutkimukseen HR-MDS:ssä. FDA hyväksyntä nopeutetulle myyntilupapolulle mahdollistaa koko HR-MDS markkinan tavoittamisen yhdellä tutkimuksella

- Useat r/r MDS potilaat jatkavat edelleen lääkitystä, jonka takia lopulliset OS ovat viivästyneet. Sama pätee ensilinjan potilaisiin, joista monet ovat siirtyneet kantasolusiirtoon.

- Tämän viestin ympärillä asiasta on keskusteltu. Tein väärä johtopäätöksen r/r MDS potilaiden osalta. En tosin vieläkään ymmärrä miten potilaat raportoidaan/tilastoidaan.

- Jos kaikki menee hyvin, niin lopullisia elossaolotietoja ensilinjan HR-MDS:ssa saa odottaa vielä kauan.

- EMA:n ja muiden regulaattoreiden kanssa tullaan keskustelemaan II/III -trialista.

- EOP2-tapaamisen palautteen perusteella Faron käynnistää vaiheen II/III saumattoman, adaptiivisen, satunnaistetun, lumekontrolloidun ja kaksoissokkoutetun tutkimuksen ensilinjan HR-MDS-potilailla

- Tutkimus voi johtaa sekä nopeutettuun että täyteen hyväksyntään koko HR-MDS-potilaspopulaatiossa.

- Noin 400-potilaan tutkimus. Faasin II/III-potilaat sisällytetään (80 potilasta)

- FDA on hyväksynyt IWG2023-kriteerit

- Protokolla on valmistelussa ja todennäköisimmin tulee kattamaan 80-90 kliinistä tutkimuskeskusta (EU/US/Japani).

- Myyntiluvan saaminen viivästyi hieman, mutta vastapainona AA-mahdollisuus koko HR-MDS:aan, jota ei aikaisemmin ollut. ”Isommat myynnit alkavat aikaisemmin ja meidän mallinnuksessa ainakin NPV kasvoi”.

- Rekisteröintitutkimuksen (II/III) päätteeksi tehdään teho- ja turvallisuusarviointi (Risk-Benefit-Ratio tulee tarkasteluun). Tämän jälkeen voidaan tehdä resizing, jolloin potilasmäärä P3-tutkimuksessa voi elää. (Kommentti: Tällöin myöskään väliluennan aikataulu ei ole varma). Tulokset kerrotaan myös ulospäin.

- Jalkanen ei ole huolissaan EMA:n kannasta tutkimusasetelmaan.

- Pharma-sentimentti ei ole muuttanut realistista kuukausihinnoittelua, mutta painetta on.

Aikataulu

- Q2/2026-Q1/2027 - Phase II/III -tutkimus Bex+Aza 3mg (n=40) vs Placebo+Aza (n=40) vs Bex 1mg+Aza (n=40)

- Resizing Q1/2027

- Q1/2027-Q1/2030 Bex+Aza vs Placebo+Aza

- Väliluenta Q1/2028 (AA-mahdollisuus)

- OS-analyysi Q1/2029

- Lopullinen OS-analyysi Q1/2029

Kiinteiden kasvaimien tutkimus

FINPROVE : Bex + standardihoito metastasoituneessa (levinneessä) rintasyövässä, Clever-1 positiiviset potilaat.

- Sopimus HUS:n kanssa, joka on päätutkimusyksikkö.

- HUS hakemassa luvat. HUS (päätutkijat) tiedottavat myöhemmin enemmän.

- Selvitetään mahdollisuuksia Bexin yhdistämisestä tavanomaisen kemoterapiaan

- Ensimmäinen Bex-tutkimus, jossa käytetään prospektiivista potilasvalintaa Clever-1-positiivisuuden perusteella.

- First-patient-in H1/26

- Tutkijalähtöinen tutkimus

BLAZE : Bex + PD-1 estäjä NSCLC- ja melanoomapotilailla, jotka ovat resistenttejä ensimmäisen linjan immunoterapialle.

- First-patient-in H2/25

- Vaiheen 2 tutkimus

- Tutkijalähtöinen tutkimus

- Saanut eettiset hyväksynnän ja sopimusprosessi loppuvaiheessa

- Gilead tuo PD-1:n.

BEXAR : Pehmytkudossarkoomat, tavoitteena muuttaa “kylmät” kasvaimet immuuniherkiksi.

- First-patient-in H1/26

- Tutkijalähtöinen tutkimus

- Frontline trial

- Yhdistetään Doksorubisiinin kanssa

MATINS-02 : PD-1 primaarisesti resistentit kylmät kasvaimet (maha-, sappirakko-, ER+ rintasyöpä).

- Suunnitteilla. Odottaa alustavia tehotuloksia.

- Bexillä on potentiaalia tehdä nämä ensisijaisesti resistentit (“kylmät”) kasvaimet herkiksi PD-1-hoidolle.

- Tutkimuksessa validoidaan myös etukäteen, että kasvaimen Clever-1-positiivisuus voi toimia ennustavana biomarkkerina hoitohyödylle

- Faronin sponsoroima

Traumakine-kehitys lopetettu → resurssit keskitetään Bexiin.

Haastava toimintaympäristö

- Biopharma- ja life science -sektoreilla rahoitushaasteet, lääkkeiden hinnoittelupolitiikan muutokset, varovaisuus yritysjärjestelyissä sekä sääntely- ja makrotalouden epävarmuus tekivät markkinasta vaikean vuoden alkupuolella.

- Suurten lääkeyhtiöiden kiinnostus kohdistuu erityisesti myöhäisvaiheen ja markkinoille lähellä oleviin tuotteisiin.

- FDA on tiukentanut onkologialääkkeiden hyväksyntäkriteereitä: pois yksivaiheisista tutkimuksista ja surrogateista, painottaen satunnaistettuja vertailututkimuksia ja elossaoloa tärkeimpänä päätetapahtumana. Tämä ei ole merkittävästi vaikuttanut Bexiin (toimittu FDA ohjeistuksen mukaisesti)

- FDA hyväksyy vasteeseen perustuvan korvaavan päätetapahtuman välituloksissa, nopeutetun hyväksynnän pohjaksi ensilinja HR-MDS:ssa, mikä osoittaa tämän sairauden suuren hoitotarpeen.

Partneroinnista:

- ”We are now well equipped to enter the next phase of commercial discussions and are continuously exploring different options we have to ensure maximising Faron’s shareholder value while progressing the development of bexmarilimab in both solid tumors and hematological malignancies”.

- Pöydällä on monta vaihtoehtoa ja mahdollisuutta.

- Sopimus tehty (top-tier) investointipankin kanssa perkaamaan kaikki vaihtoehdot omistaja-arvon maksimoimiseksi

- Ovatko yritykset kiinnostuneita yksinomaan BEXMAB-yhdistelmästä, vai ovatko mahdolliset yhteistyökumppanit kiinnostuneita käynnistämään uuden tutkimuksen tai uuden yhdistelmähoidon, joka perustuu heidän omaan tuotekehitysohjelmaansa? – Lähes kaikki nämä. Erityisesti AML on kiinnostanut.

- P2-tulokset (ja tutkimussuunnitelma) olivat puuttuva palanen – Kohti partnerointia. “Now in H2 it´s time for business” – “We´re still well financed with a nice reserve of cash in the back”

- Syksyllä tuli tarjous, mutta se ei miellyttänyt. Päätettiin viedä faasi 2 loppuun, jotta sopimuksen arvoa saadaan kasvatettua. Faasi 2 tuloksien aikaan tuli jo parempi tarjousta – tästä kieltäydyttiin, koska haluttiin päästä tähän pisteeseen.

Seuraavat tapahtumat

- ASH (HR-MDS päivitys)

- ESMO (HR-MDS päivitys)

AJATUKSIA:

Ajurit ja edut:

FDA Orphan Drug status AML (2023)

FDA Orphan Drug status AML (2023)

FDA Fast Track r/r MDS (ELO24)

EMA Orphan Drug status MDS (+Aza) (HEL25)

FDA Orphan Drug status MDS (MAA25)

Patentti (Clever-1) voimassa vuoteen 2040 asti

Rahoituksen riittävyys Q1/2026, selkänoja ja rahoituskuvioiden selkeytyminen

Patenttihakemus (Clever-1 – autoimmuuni- ja tulehdussairaudet) (MAR2024)

UK MHRA Innovation Passport r/r MDS (JOU24)

Sisäpiirin sitoutuminen yritykseen

Scientific Advisory Board ja Ralph Hughes

P2 tulokset ja onnistunut faasi.

– HR-MDS CR 9/21 (43%), ORR 81%

– 5 potilasta eteni kantasolusiirtoon ja kaksi potilasta suunnitteilla (35%)

– Tulokset voivat vielä syventyä

VERONA-trial epäonnistuminen (…as one of the remaining frontrunners)

VERONA-trial epäonnistuminen (…as one of the remaining frontrunners)

Accelerated Approval mahdollisuus vuonna 2028 koko HR-MDS.

Mahdollisuus täyteen hyväksyntään koko HR-MDS-potilaspopulaatiossa vuonna 2028.

Kassavarojen joustavuus?

Yritys vaikuttaa olevan sitoutunut omistaja-arvon maksimoimiseen

Riskit:

Faasin 3 toteutus ja/tai tulokset (byrokratia, virheet tutkimusasetelmassa, luvat ja myynti)

Faasin 3 toteutus ja/tai tulokset (byrokratia, virheet tutkimusasetelmassa, luvat ja myynti)

Geopolitiikka viivästyttää ja hankaloittaa

Rahoitus - Toisen tranchin nostaminen

Rahoitus - kriteerit eivät täyty 2. trenchin nostamiseen – anti

P3 aloituksen merkittävä viivästyminen - P3 rekrytointi ei ala ilman kumppania

Kumppanin löytäminen ja sopimuksen koko (geopolitiikka vs. varovaisuus investoinneissa)

Merkittävää!

- 5 potilasta eteni kantasolusiirtoon ja kaksi potilasta suunnitteilla (35%).

- Partnerointi on annettu ammattilaisten käsiin. Sopimus on tehty (top-tier) investointipankin kanssa

- Yritys vaikuttaa olevan sitoutunut omistaja-arvon maksimoimiseen

- Juhon mukaan kaikki uskovat lääkkeeseen. ”It looks like a game-changing drug” - Onko syytä epäillä?

- Partnerointia on mielestäni turha odottaa tänä vuonna. Due Diligence tulee kestämään.

- Faasin aikatauluun saattaa tulla muutoksia. Realistisesti odotan faasin käynnistymistä Q2-Q3/2026 aikana?

- Tällöin tullaan käyttämään seuraavaa tranchia (10M) – liudentuminen.

- Kuka rahoittaa rekisteröintitutkimuksen? Koska se alkaa jos partnerointi viivästyy?

Auki olevia kysymyksiä:

- Voiko väliluennan yhteydessä vain esim. r/r MDS saada AA:n vai onko kyse kaikki tai ei mitään -asetelmasta?

- Koska kiinteät alkavat näkymään isommin valuaatiossa ja tavoitehinnoissa? Nyt luokkaa 10%.

- Mistä niitä varakippoja saa? Kohta paukkuu vipu!

Jalkasen mukaan nyt ei ole enää auki olevia kysymyksiä – nyt on sen aika – katsotaan mihin tarjoukset nousevat.

Lopuksi totean, että kenen mielestä fundamentit ovat muuttuneet? Tulokset piti, 2. faasi onnistui, tutkimus etenee ja pipeline alkaa hiljalleen täyttyä. Kaikki viittaa siihen, että partneri tulee tavalla tai toisella!

Onneksi olkoon ketjulle jo ennakkoon kohta täyttyvästä 10k viestistä!