Just to make sure it didn’t go unnoticed, I opened up a discussion about the impact of tariffs on financial sector companies in another thread: Finanssisektori sijoituskohteena - #671 käyttäjältä Sauli_Vilen - Osakkeet - Inderes forum

5 Likes

CALL: Evli Plc to publish its Interim Report on April 25, 2025

Evli Plc’s interim report for January-March 2025 will be published on Friday, April 25, 2025, at approximately 2:00 p.m. The report will be available after publication on the company’s website at evli.com/investors.

1 Like

Fund Sales Remained Weak in March

Evli’s funds saw a significant inflow of new capital, with net subscriptions ending up at a positive 124 MEUR. Although a large part of this is explained by the sales of the low-margin Evli Likvidi money market fund, the company is a clear success story in the asset management market for the beginning of the year with over 270 MEUR in net subscriptions.

6 Likes

Sauli’s preliminary comments as Evli publishes its Q1 results on Friday. ![]()

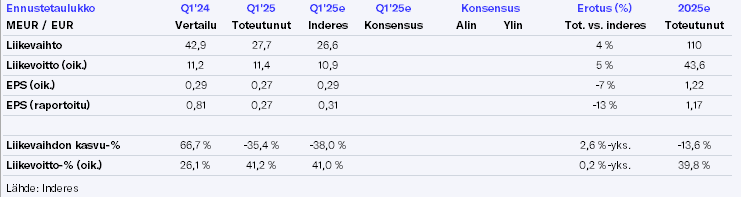

The company’s Q1 has, according to our estimate, gone well, as the market decline fueled by the trade war only properly occurred after the review period. We have therefore slightly revised our Q1 forecasts upwards, but at the same time lowered our full-year forecasts due to the weakening of the capital market. Despite the good result, Evli’s outlook has also weakened due to the weakening economic picture. At the same time, however, we note that Evli, with its diversified product offering, is best positioned for a weakening market situation among the asset managers we follow.

3 Likes

Evli’s results are out. Very well in line with forecasts. That small overshoot came from so-called “wrong places” and, at first glance, operationally this went completely according to our script. Despite market uncertainty, the company is very well positioned for a more challenging market.

19 Likes

Steady performance in my opinion. It’s good that the current “growth drivers,” i.e., alternative funds and foreign capital, were kept growing. The slope of capital growth could always be improved, but fortunately, the direction is right. Traditional products are also clearly in the black (net positive).

6 Likes

Outlook and Guidance

Evli expects a clearly positive result for 2025, which corresponds to the analyst’s estimate. The report emphasizes an uncertain market environment, which may weaken short-term prospects. The threat of trade war and geopolitical factors increase uncertainty, but the general guidance remains unchanged.

Asset Management Success and Challenges

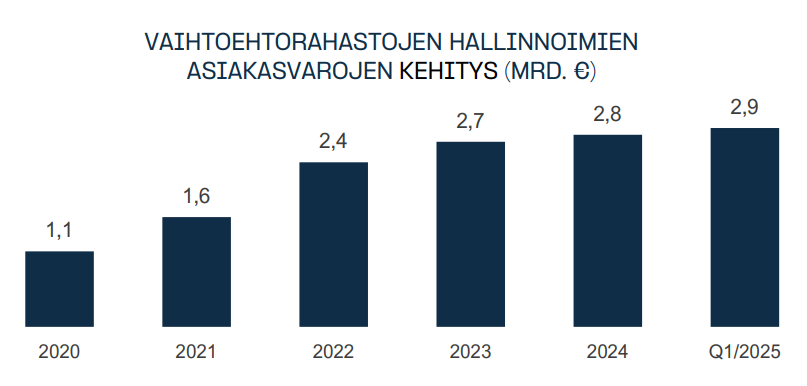

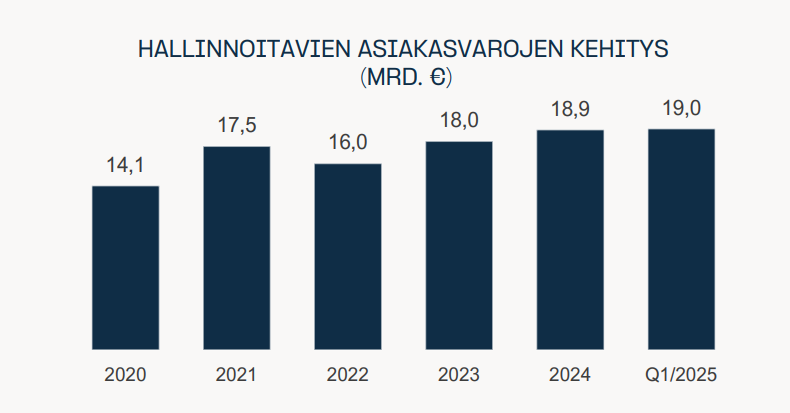

Evli’s assets under management (AUM) at the end of Q1 were EUR 19.0 billion, which is slightly below the analyst’s forecast (EUR 19.4 billion). Market development and net subscriptions increased assets under management, but the weakening of the capital market in April may lower the asset level in the coming months. Evli’s shares in international markets and alternative investment products grew, which supports the future of asset management.

3 Likes

A report from Sauli

We are revising our target price for Evli to EUR 20.0 (previously EUR 21.0) reflecting slightly lowered forecasts. We still consider Evli a clear long-term winner in the sector, and the earnings growth outlook for the coming years remains good despite the short-term uncertain market. The stock thus offers a good return expectation at the current level, and we reiterate our Add recommendation.

7 Likes

Evli Private Capital, focusing on accelerating the green transition, has made a significant investment of 7 million euros in Calefa. The investment consists of both new capital and the purchase of existing shares, making Evli Private Capital a significant minority owner of Calefa Oy.

Calefa Oy

Calefa Oy implements comprehensive energy solutions for industry, energy production facilities, and large properties, based on world-leading heat pump technology. Our heat pump systems utilize waste heat and ambient energy. We create comprehensive solutions that provide our customers with significant energy savings and permanently cut CO2 emissions.

Evli Private Capital

Evli Private Capital Fund I focuses on promoting the green transition. The fund makes significant minority investments in Finnish and Swedish small and medium-sized growth companies that focus on the energy transition, resource efficiency, and circular economy. The fund has previously invested in EWQ Zone, a Finnish company promoting retail digitalization and resource efficiency. Evli’s private equity team’s previous investments include Proventia, Solnet Green Energy, Bladefence, and Elcoline.

6 Likes

April was a somewhat strange month for Evli’s fund sales. Numerically, the month was a kind of defensive victory, as sales remained positive. However, significant allocation changes occurred beneath the surface, with 300 MEUR shifting from equities/HY bonds to money markets. This is quite a big change on Evli’s scale. I assume this is purely an allocation change made by Evli to its TVK portfolios, the impact of which on the group would ultimately be quite limited.

P.S., at the same time, I must remind you regarding Evli’s Private Capital investments that they are made by one of Evli’s funds, not Evli itself from its own balance sheet (cf. how CapMan operates). The fund is small on Evli’s scale, and therefore, even though these Private Capital investments receive a lot of visibility, they are not significant for Evli ![]()

11 Likes

Evli, as expected, launches a new infrastructure fund: https://www.evli.com/artikkelit/evlilta-uusi-evli-infrastructure-fund-iii-rahasto

The fund should have good demand in the current market, and I wouldn’t be surprised if it became Evli’s biggest infrastructure fund.

11 Likes

Evli’s fund net subscriptions remained positive and totaled 98 MEUR. However, the majority of subscriptions were directed to the low-margin money market fund Evli Likvidi (+64 MEUR). We remind that subscriptions to this fund can fluctuate significantly on a monthly basis, as companies, for example, use it as a cash management tool. Measured by net subscriptions, Evli has been a clear success in the sector for the entire year to date, with net subscriptions totaling almost 400 MEUR. However, we note that Evli Likvidi has grown by approximately the same amount during the review period, and this somewhat weakens the success of new sales.

4 Likes

Looks like they’ve set this up.

The Evli Private Equity Co-Investment I fund makes direct minority investments in unlisted companies in Europe and the United States together with leading international private equity firms. A co-investment fund in international unlisted equities with its own specialized team is the first of its kind among Finnish asset management companies.

6 Likes

Minimum investment €100,000. However, it doesn’t state other specifications, such as the fund’s target size.

2 Likes

Recognition for Evli again in wealth management rankings ![]() Evli has been at the top of these various wealth management rankings for over a decade, which is an incredibly good performance. I would like to remind you that even though these might feel like “business as usual” for Evli, this continuous success is vital for the company’s long-term success, and in the investment markets, returns start from zero every day.

Evli has been at the top of these various wealth management rankings for over a decade, which is an incredibly good performance. I would like to remind you that even though these might feel like “business as usual” for Evli, this continuous success is vital for the company’s long-term success, and in the investment markets, returns start from zero every day.

Evli’s press release: https://www.evli.com/artikkelit/evli-arvioitiin-parhaaksi-yhteisovarainhoitajaksi-kantar-prospera-2025

Official ranking: https://www.kantarsifo.se/sites/default/files/f8a778cc.pdf

18 Likes

Q2 preview from Sauli

3 Likes

Evli’s strong sales in the early part of the year continued, and the company collected EUR 37 million in subscriptions in June. For the entire first half of the year, subscriptions now total EUR 428 million, and Evli is a clear success in the sector when measured by net subscriptions for the entire first half of the year. We note, however, that Evli Liquid has grown by roughly the same amount during the review period, and this somewhat weakens the success of new sales. Part of the growth in Liquid is, in our estimation, due to the company’s allocation decisions.

5 Likes

Revenue 27.5 vs. 27.6 forecast (Inde)

adj. EBIT 11.1 vs 10.2

12 Likes

From the link you put above, fair-weather clouds, the half-year review

OUTLOOK FOR 2025

The first half of the year was turbulent in the investment markets, and the operating environment is expected to remain uncertain and difficult to predict for the rest of the year. The expansion of geopolitical risks and concerns about the sustainability of economic growth increase uncertainty in the markets. If investor confidence erodes further and market values turn downwards, it will have a negative impact on Evli’s fee income and the return on its own investment portfolio.

Despite the challenging operating environment, Evli has succeeded in strengthening its position in the market. Growth has been supported by a wide product range and customer base. With a strong market position and growth prospects, we estimate the operating profit to be clearly positive.

ANNIVERSARY YEAR

In 2025, we celebrate Evli’s 40-year journey. Over the years, we have grown into a leading Nordic wealth manager and fund house, supporting our clients in building long-term success and directing capital where it creates long-term value. We are committed to building a more prosperous tomorrow also in the future.

4 Likes

Sale has made a new company report on Evli. ![]()

We revise Evli’s target price to EUR 21.0 (previously EUR 20.0) reflecting forecast changes. We continue to see Evli as a clear long-term winner in the sector, and the earnings growth outlook for the coming years remains good. The share’s valuation is neutral, but if earnings growth materializes as per our expectations, the share is inexpensive. The return expectation formed by earnings growth and a strong dividend is, in our opinion, attractive, especially when compared to the company’s moderate risk level. We are therefore raising our recommendation to Buy (previously Add).

Quoted from the report:

Compared to its domestic peer group, Evli is valued at a small premium. In our opinion, the premium could also be wider than currently, considering the company’s high quality. The entire sector is currently valued approximately at its historical levels, which we consider justified, and we see the valuation of the entire sector as very reasonable at the moment. The valuation of the peer group also supports our view that there is clear upside potential in the stock as earnings growth materializes.

10 Likes