Evli’s month was somewhat subdued, and capital was redeemed from the company’s funds, totaling approximately EUR 42 million net. The redemptions were mainly directed at equity funds with a healthy fee level. However, new capital flowed into bond funds, which balanced the development.

5 Likes

Could someone wiser kindly tell me how these Evli active global equity funds are still operating when they have been underperforming their benchmark indices for years? I opened all the global equity funds on Evli’s website, and six out of seven funds are significantly behind their own benchmark index.

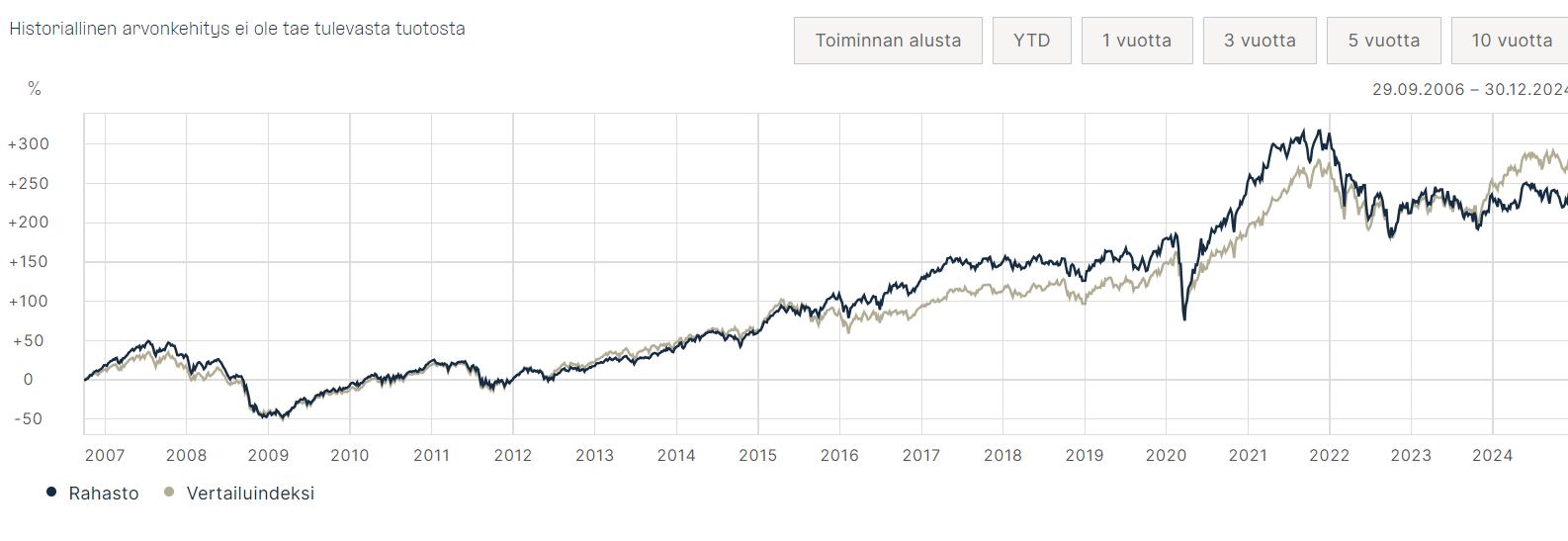

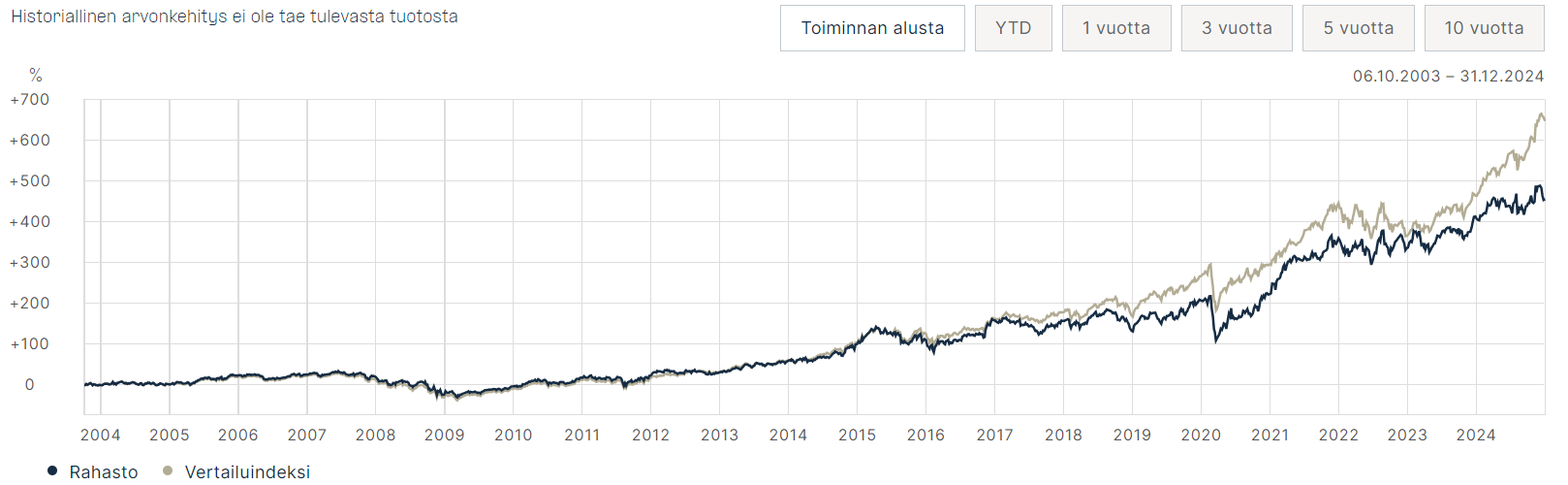

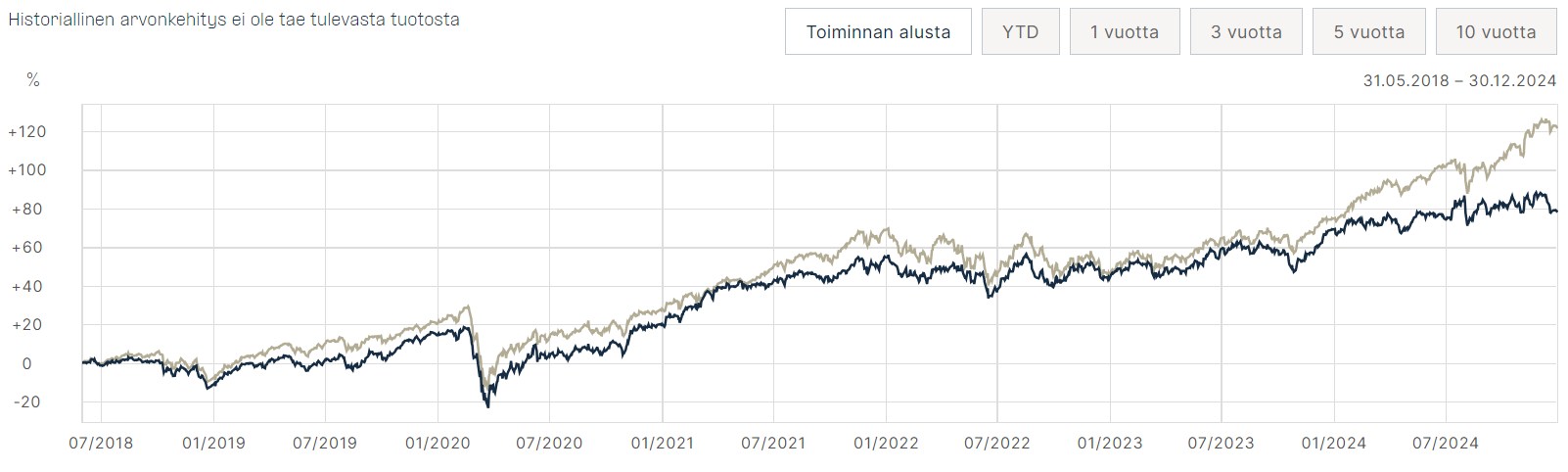

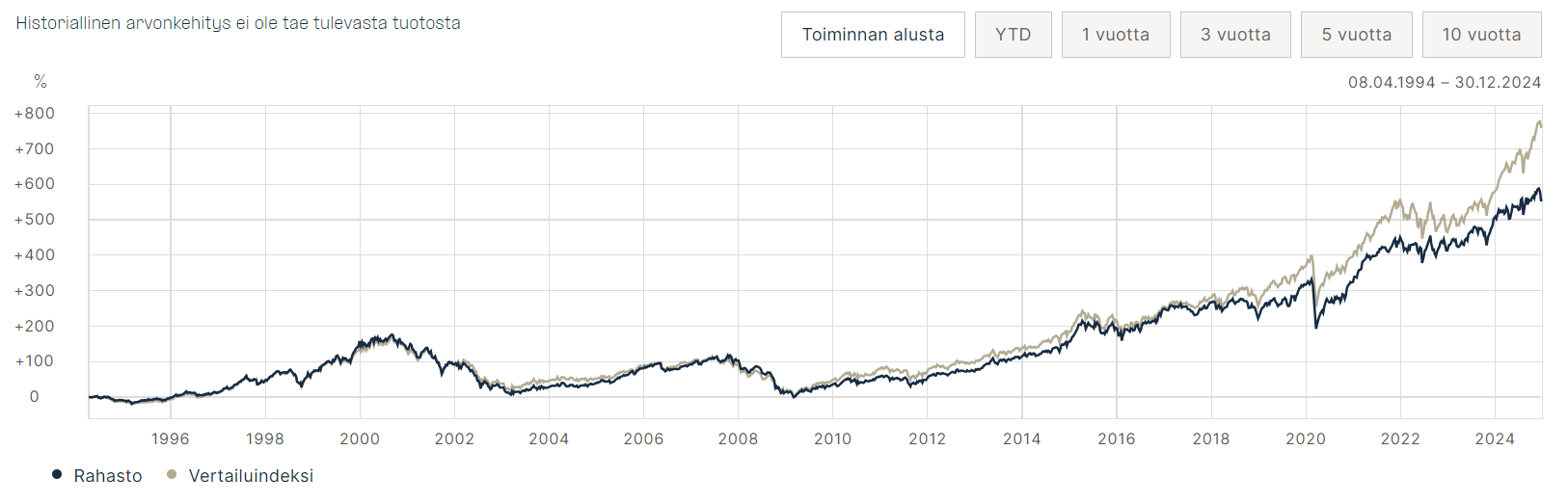

Evli Nordic Countries:

Evli North America:

Evli World X:

Evli World:

Evli Japan:

Evli Europe:

And finally, the only global fund that has beaten its own index is Evli GEM:

Are clients not interested in returns, or how can these continue with such performances?

4 Likes

So, these have done quite well for 20 years, but have now missed the rise of the Magnificent 7 stocks in recent years, as almost the entire return of the US index comes from them. Additionally, funds have fees, while an index does not.

4 Likes

Evli’s month was somewhat subdued, with a net total of approximately EUR 30 million redeemed from the company’s funds. Redemptions were mainly directed at short-term interest rate funds with moderate fee levels and equity funds with healthy fee levels, so the overall development can be considered slightly negative. A positive aspect, however, was that significant new capital flowed into long-term interest rate funds, which, in our view, stems from the company’s strong position in fixed income asset management. The entire calendar year was somewhat subdued in terms of sales for the company, as cumulative net subscriptions were only positive by approximately EUR 110 million (1.1% of assets at the beginning of the year).

6 Likes

Additionally, the benchmark indices are probably self-invented or the easiest ones have been chosen for them to outperform.

Funny thing that this is made into a story ![]()

1 Like

INVITATION: Evli Plc to publish its 2024 results on January 29, 2025

Evli Plc’s financial statement release for January-December 2024 will be published on Wednesday, January 29, 2025, at approximately 11:00 a.m. After its publication, the review will be available on the company’s website evli.com/investor-relations.

3 Likes

Here are Kassu’s pre-earnings comments as Evli publishes its Q4 results next Wednesday. ![]()

We expect the company’s key financial figures to have developed favorably, even though the group-level result is declining in our forecasts due to significant non-recurring income items in the comparison period. Asset management’s new sales, on the other hand, developed modestly at the end of the year, so in addition to the financial figures, our interest will again focus on management’s comments regarding the demand outlook for asset management.

4 Likes

Revenue above forecasts

EPS at Kasper’s forecast level

Dividend below forecasts

6 Likes

The comments of the Rane Robotti type are below. He will soon replace all of us in Ruoholahti. ![]()

5 Likes

Quoted below from Kasperi’s “pen”:

The stock’s expected return is good

We consider a P/E 17–18x range an acceptable valuation level for Evli, taking into account the company’s competitive products, the strong long-term earnings growth outlook enabled by them, and the company’s moderate risk level. In addition, the company’s growth ties up only limited capital, which has a positive impact on the accepted valuation level. Based on the current year’s estimated earnings, the P/E ratio is approximately 16x, which falls below our applied range. We therefore believe that earnings growth (~5%) and an earnings-based dividend yield (6–7%) offer the stock an attractive expected return against a moderate risk level. In addition to this, the expected return receives slight support in our calculations from an increase in multiples, as the stock’s current pricing is moderate.

8 Likes

Evli is a nice stock to own, when even on the Inderes forum, the company’s thread activity resembles this:

Anyways, yesterday was the annual general meeting and today the stock will likely fall due to the ex-dividend date. Unfortunately, there doesn’t seem to be a video recording of the meeting available, so @Kasper_Mellas and other sales representatives still have work to do regarding video sync. My fervent wish is that the company could appear in some Inderes format at least once a year, be it Pörssisijoittajan päivä or something else.

The materials for the annual general meeting can be found here, and the CEO’s review here

In addition, Kasper commented on the February fund report last week. Evli did quite well:

“Evli’s funds saw a significant inflow of new capital, and net subscriptions ended up in positive territory at 162 MEUR. However, there was a shift from equity funds towards bond funds with a more moderate fee level, which dampens the positive impact of sales on fee income.”

16 Likes

It’s good to remember that today we’ll see a dip due to this dividend, as poutapilviä reminded. ![]() I’ve also been focused on other stocks, and this one has received less attention in comments. It’s nice to own this one. ROI over 15% and ROE over 30%

I’ve also been focused on other stocks, and this one has received less attention in comments. It’s nice to own this one. ROI over 15% and ROE over 30%

EVLI PLC STOCK EXCHANGE RELEASE 18 MARCH 2025 AT 1:00 P.M. (EET/EEST)

Resolutions of Evli Plc’s Annual General Meeting and Board of Directors on 18 March 2025

Evli Plc’s Annual General Meeting held on 18 March 2025 adopted the financial statements and granted discharge from liability to the members of the Board of Directors and the CEO for the financial year 2024.

In accordance with the Board of Directors’ proposal, the Annual General Meeting resolved that a dividend of 1.18 euros per share be paid for the financial year 2024. The dividend will be paid to shareholders who are registered in the company’s shareholder register maintained by Euroclear Finland Oy on the record date for dividend payment, 20 March 2025. The dividend will be paid on 27 March 2025.

1 Like

Hey Kasperi

Who will continue following Evli going forward, you, Sauli, or someone else at your end?

Even though I wasn’t asked, I can answer! Going forward, all asset managers are under my monitoring. Mandatum is the only exception that is followed together (Mandatum is much more than just an asset manager). All banks, on the other hand, are with Kasper.

P.S. The analysts following the companies are always visible on the company pages, and under the analysts, you can also find analyst-specific follow-ups. Here is my follow-up: Inderes

11 Likes

Hi, thanks Sauli for the reply, it was hidden-addressed to you. ![]()

![]() Yep, I saw you’re on the company page, I was mainly wondering why the thread has been quiet even though you’ve otherwise become active on the forum since returning to work. Thanks for this, we’re eagerly awaiting your next updates “from your pen” or perhaps keyboard, etc.

Yep, I saw you’re on the company page, I was mainly wondering why the thread has been quiet even though you’ve otherwise become active on the forum since returning to work. Thanks for this, we’re eagerly awaiting your next updates “from your pen” or perhaps keyboard, etc.

We’re living in interesting times in the financial sector, there’s plenty to follow.

1 Like

Happy dividend payment day to Evli’s owners!

When I went through Evli’s figures and the latest analysis, I ran into a dilemma. The company doesn’t distribute all its earnings every year. Here’s what Kasper commented in connection with Q4:

“However, the biggest changes were directed at our dividend forecasts, as the company, contrary to our expectations, did not distribute additional funds from its strong balance sheet (dividend €1.18 vs. €1.38 forecast). Therefore, we estimate that owners primarily value a steadily growing dividend, and we no longer expect additional dividends in the coming years. This clearly cut our profit distribution forecasts.”

The justifications for a steadily growing dividend are understandable. For the coming years, the dividend payout ratio is on average 80-90% of EPS. But the dilemma is that the cash balance is already swelling with cash.

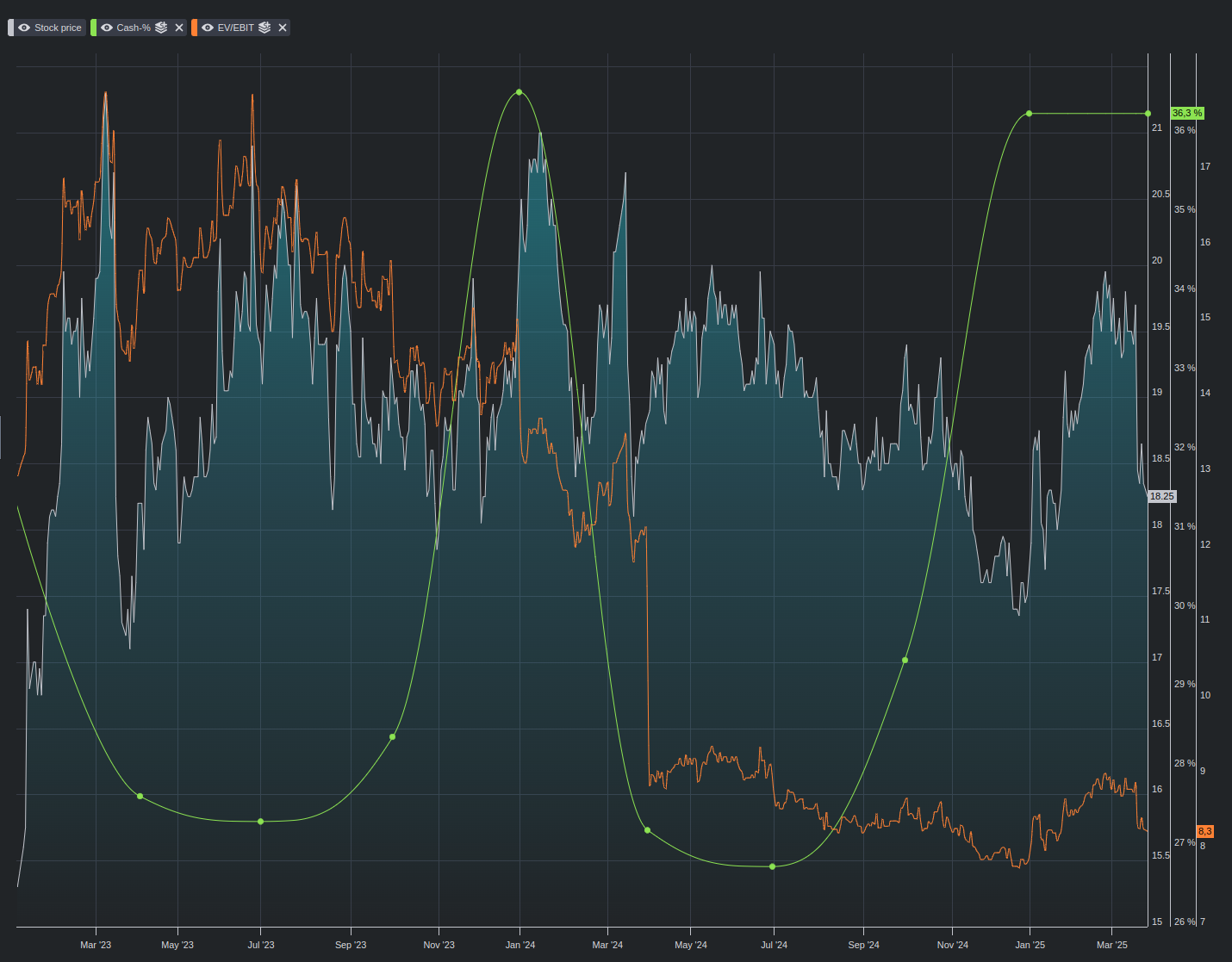

Question for @Sauli_Vilen: What do you think is Evli’s “end game” with that cash? Negative enterprise value? Or the classic M&A card?

In my opinion, last year’s AllShares ownership arrangement proved that Evli is at least not trying to complicate the group’s operations. So, for this already large asset management firm, would acquisitions then be product houses that grow their offering?

The graph shows Evli’s share price, cash % and EV/EBIT à la Börsdata:

10 Likes

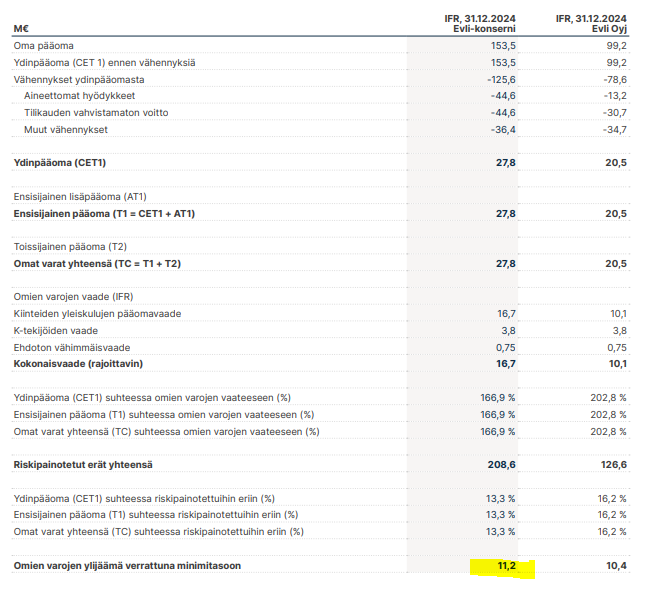

In Evli’s case, simply looking at the cash balance gives a regrettably misleading picture. The cash balance may be very large at times, but there are various liabilities on the other side of the balance sheet. At the end of 2024, cash and cash equivalents amounted to EUR 140 million, but on the other side, there was approximately EUR 100 million in loans. In addition, in Evli’s case, the balance sheet is complicated by the small loan position granted to customers and items related to its own securities brokerage (Other assets and Other liabilities). It requires quite a workout to calculate the final net cash from that EUR 362 million balance sheet ![]() Anyway, it is significantly smaller than that EUR 140 million cash position.

Anyway, it is significantly smaller than that EUR 140 million cash position.

Solvency, on the other hand, is the item an investor should look at. The EAB transaction was very expensive in terms of solvency (a lot of goodwill), and the company doesn’t even have much excess capital within the framework of solvency. At the end of 2024, excess capital was EUR 11 million, or less than EUR 0.5/share.

By deleveraging its balance sheet, Evli could indeed increase its solvency and thereby free up a lot more capital. However, the scale is far from what you’ve drawn, and in reality, we would probably be talking about tens of millions. I would point out, however, that beyond a certain point, this would also affect business operations, for example, by having to limit the activities of its own desk.

Historically, Evli has been a very conservative house and has wanted to keep its balance sheet somewhat overcapitalized. The company’s main owners clearly have the will that Evli can withstand all possible storms on its own. Therefore, no major balance sheet deleveraging efforts should be expected. Against this background, distributing almost the entire profit as a dividend is, in my opinion, a good starting point. Whether the payout ratio is ultimately 90% or 100% doesn’t change the overall picture much ![]()

23 Likes

Sauli has somewhat pondered valuation

1 Like

During these tariffs, I pondered the situation of asset managers, especially Evli. In my opinion, it is the best positioned of all companies in the sector:

-

A significant portion of the profit comes purely from managing funds → Profit is dependent on money flowing out of funds + variation in fund size. A much better situation compared to peers, which are dependent on performance fees.

-

Evli’s largest asset class is traditional funds, i.e., fixed income and equities. According to the latest comprehensive report, their distribution is roughly 60%/30% in favor of fixed income.

-

Thus, the decrease in AUM caused by the decline in equities plays a relatively smaller role compared to fixed income, which is not the worst investment class now, because…

-

With the tariffs, interest rates have started to fall. The primary reason for the decline, in my understanding, is the decrease in global growth forecasts. However, investors get a good safe haven from this, as returns are formed from yield + changes in fixed income securities (=falling interest rates generate a positive return).

-

A negative point finally: fixed income funds generally have lower margins compared to equity funds. So, in my opinion, Evli also deserves a small decline in the stock market in the current environment.

Of course, in the long run, we will drift into a situation where interest rates are close to zero, and thus they are a less attractive investment class. However, there is still time for this. I personally allocated the money from the shares I sold today to Evli at these €15-16 levels. This probably won’t perform the worst?

I would gladly hear counter-arguments.

3 Likes