In Evli’s case, simply looking at the cash balance gives a regrettably misleading picture. The cash balance may be very large at times, but there are various liabilities on the other side of the balance sheet. At the end of 2024, cash and cash equivalents amounted to EUR 140 million, but on the other side, there was approximately EUR 100 million in loans. In addition, in Evli’s case, the balance sheet is complicated by the small loan position granted to customers and items related to its own securities brokerage (Other assets and Other liabilities). It requires quite a workout to calculate the final net cash from that EUR 362 million balance sheet ![]() Anyway, it is significantly smaller than that EUR 140 million cash position.

Anyway, it is significantly smaller than that EUR 140 million cash position.

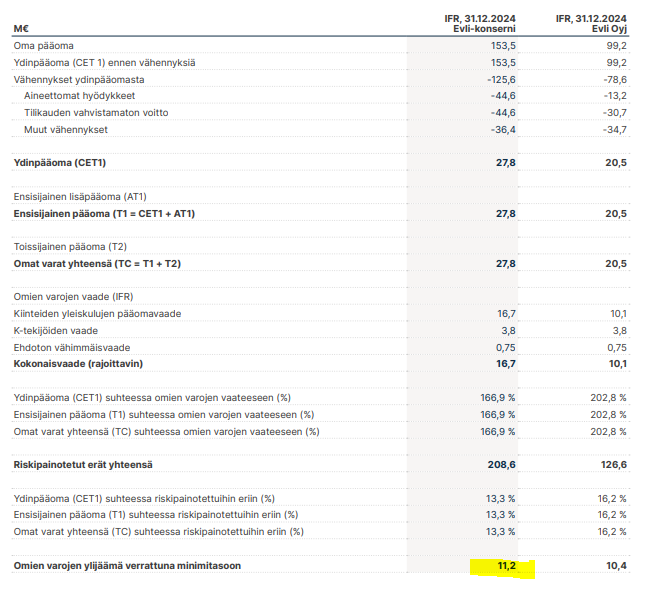

Solvency, on the other hand, is the item an investor should look at. The EAB transaction was very expensive in terms of solvency (a lot of goodwill), and the company doesn’t even have much excess capital within the framework of solvency. At the end of 2024, excess capital was EUR 11 million, or less than EUR 0.5/share.

By deleveraging its balance sheet, Evli could indeed increase its solvency and thereby free up a lot more capital. However, the scale is far from what you’ve drawn, and in reality, we would probably be talking about tens of millions. I would point out, however, that beyond a certain point, this would also affect business operations, for example, by having to limit the activities of its own desk.

Historically, Evli has been a very conservative house and has wanted to keep its balance sheet somewhat overcapitalized. The company’s main owners clearly have the will that Evli can withstand all possible storms on its own. Therefore, no major balance sheet deleveraging efforts should be expected. Against this background, distributing almost the entire profit as a dividend is, in my opinion, a good starting point. Whether the payout ratio is ultimately 90% or 100% doesn’t change the overall picture much ![]()