Those were some excellent questions! ![]()

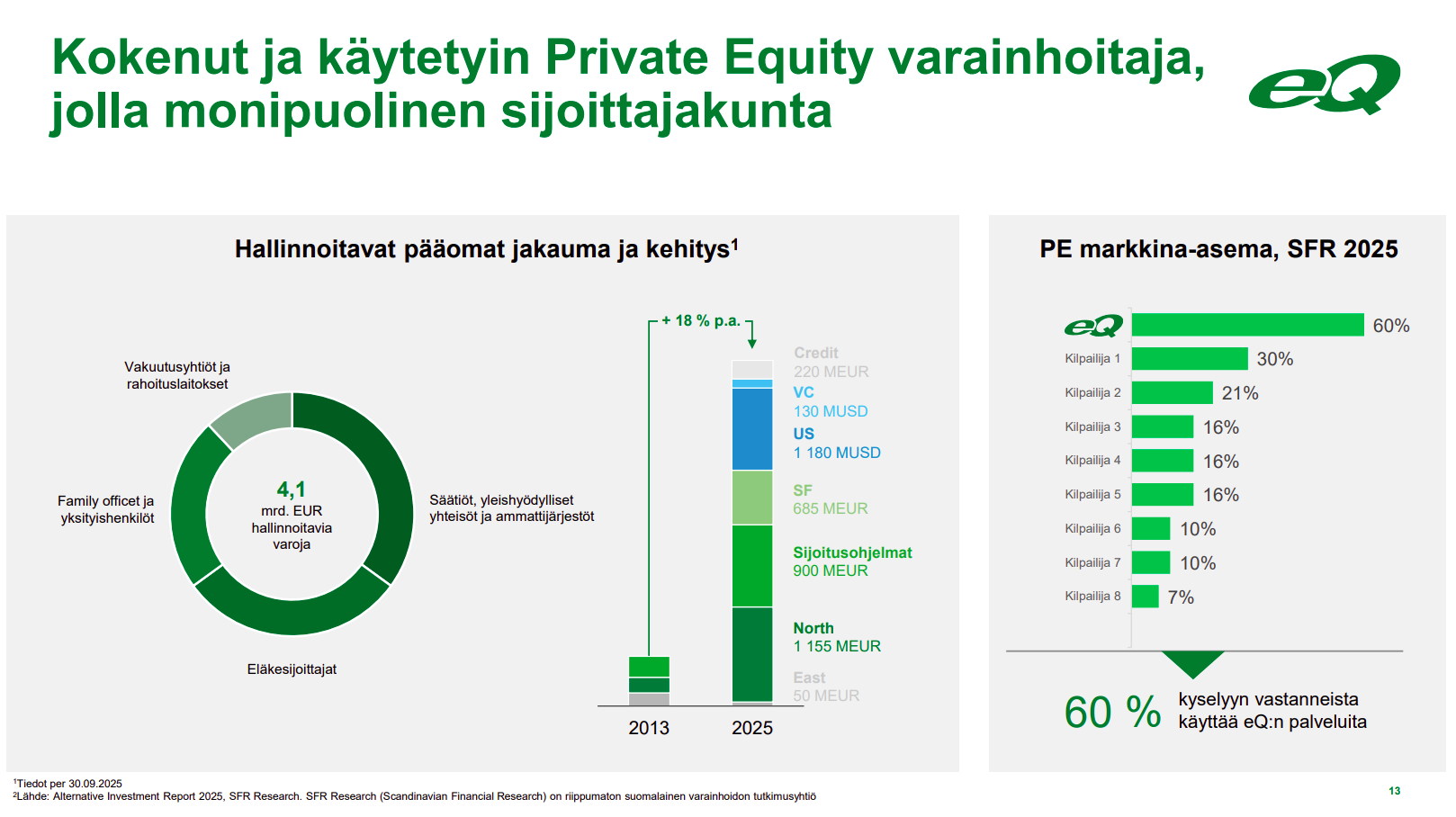

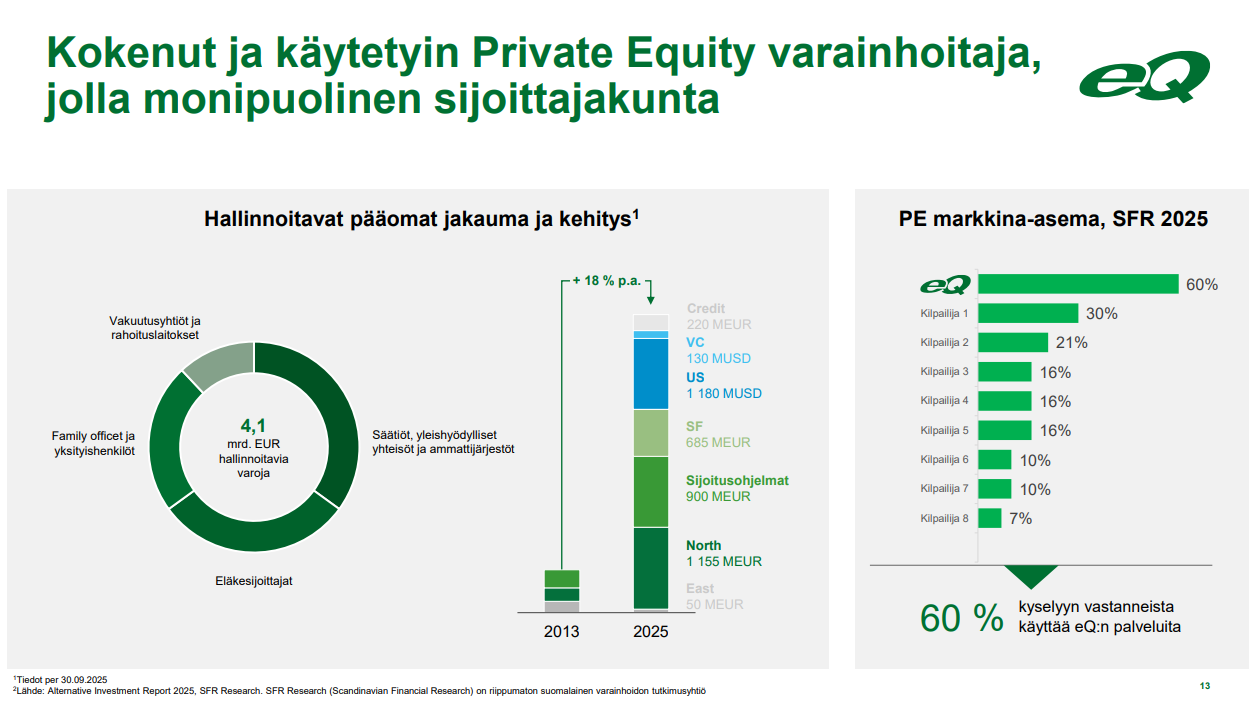

eQ’s real estate funds (as well as all of eQ’s assets under management) come mostly from institutions (instikot). In my understanding, the share of private clients is less than 10%, and in PE (Private Equity) or asset management, there are practically no private clients at all (the few that exist are comparable to institutions). There are, of course, a reasonable number of owners in terms of headcount in the real estate funds (2k and 4k), but I believe these are largely “small fragments,” and they mostly date back to the time when SPL and Investium were selling these funds widely in Finland. So, when for example 20% of a fund’s assets leave, many institutions are also involved. Attached is a screenshot from the comprehensive report regarding eQ’s client base:

Why is Titanium Hoiva (Care) a retail investor-driven fund and eQ YKK institution-driven? There are certainly several reasons for this, but one of the key ones is, of course, the focus of the organizations. eQ has always been an institutional house, while Titanium has always sold Hoiva to private investors (previously through SPL and Investium, and later directly). Another reason is the fee structure. Hoiva’s fee structure is clearly higher, and especially that cumulative performance-based calculation and the 2% transaction fee are components that are hard for institutions to swallow.

To whom are the properties sold? Herein lies the core of our market’s problem. During the previous red-hot bull market, we had two major buyer groups: international (KV) investors and domestic special investment funds (erkkarit). Now, for the coming years, special investment funds will be strictly on the sell side, and domestic pension companies are reducing their real estate weightings, so the buyer practically has to come from international investors. Until there is greater interest from international investors, there aren’t really enough buyers in the market. Furthermore, from this perspective, one cannot expect a return to the “wild years,” as special investment funds will not be the same kind of net buyers in the coming years. Larma also mentioned this in his farewell interview: eQ Q2'25: Kiinteistömarkkinan vaisu kehitys painaa - Inderes

You are absolutely right that untangling this web will take time. This will also inevitably leave its mark on the entire sector, as the reputation of special investment funds has taken a serious hit. eQ has arguably been one of the most active players in the market, and the company has genuinely tried to sell assets to get redemptions paid. This has meant that the values of eQ’s funds have come down significantly in a front-loaded manner, which in turn has been reflected in customer dissatisfaction (SFR 24 and 25). Could eQ gain a competitive advantage from this? Well, at least in the sense that from April onwards, you can no longer accept subscriptions if redemptions have been postponed. This could lead to a situation where the one who has handled their redemptions is one of the few funds that people can even invest in. But ultimately, the final verdict from investors depends on how the fund’s value has developed and how the manager was finally able to pay out redemptions once the whole situation is resolved. ![]()

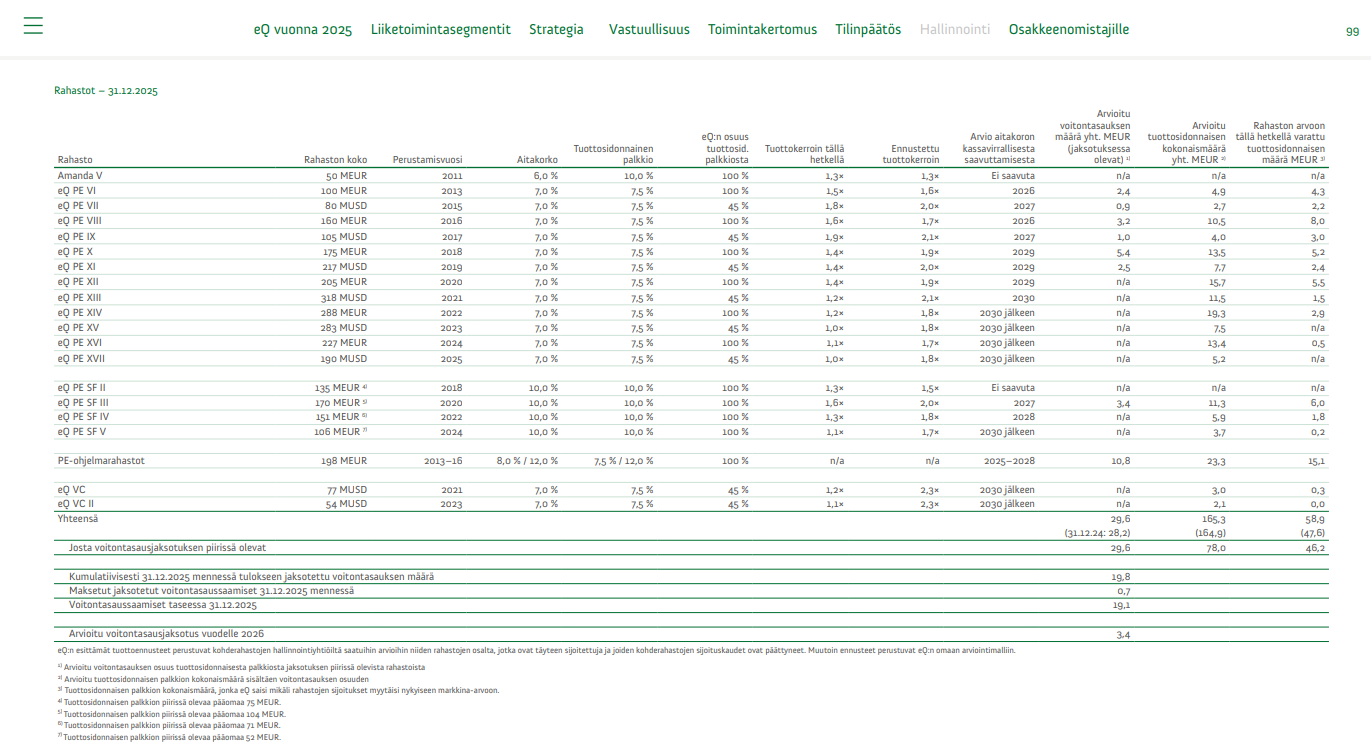

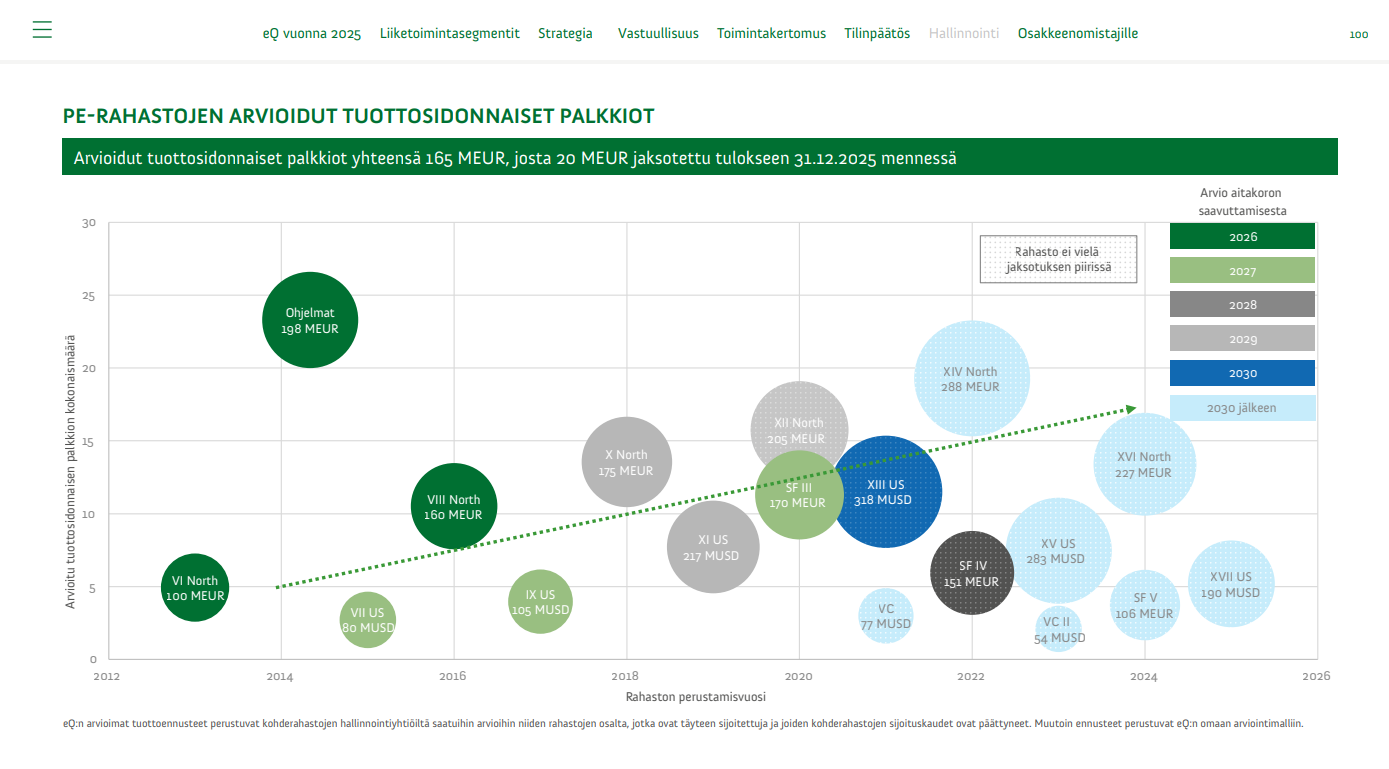

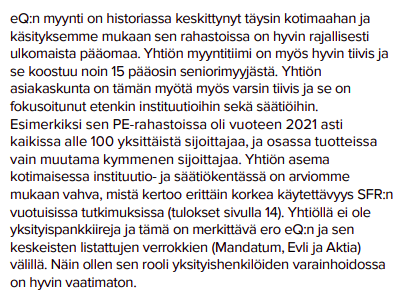

Regarding the sensibility of the FoF (Fund of Funds) structure. @Kermit already explained this logic well, and I largely agree with it. A smaller institution that doesn’t have its own large organization doesn’t have the resources (or even the capital) to access the necessary funds, let alone build a diversified portfolio from them. eQ’s core client base consists precisely of these various foundations/institutions for whom these products are very relevant. Regarding costs, you are right; a FoF is basically one extra layer, but of course, a good manager knows how to negotiate a deal so that the total cost for the end investor doesn’t rise completely out of proportion. In open PE funds, this is a very big risk because there are at worst three layers, and full fees are paid on all of them (performance fees might even be in two layers). ![]()

Advium has been part of eQ since its inception. In 2011, eQ was assembled from Advium, eQ Asset Management, and Amanda Capital. Advium is a company founded by Larma, and he was, of course, the lead architect in the whole arrangement. It’s worth remembering that the majority of asset managers have an investment bank included. It is generally seen as part of a full-service financial house. I think it’s important that the share of the investment bank is small enough so that it doesn’t swing the entire group’s results. In that case, the investment bank “inherits” the asset management multiples, and not the other way around. ![]()

Tomorrow is going to be a very interesting day! ![]()