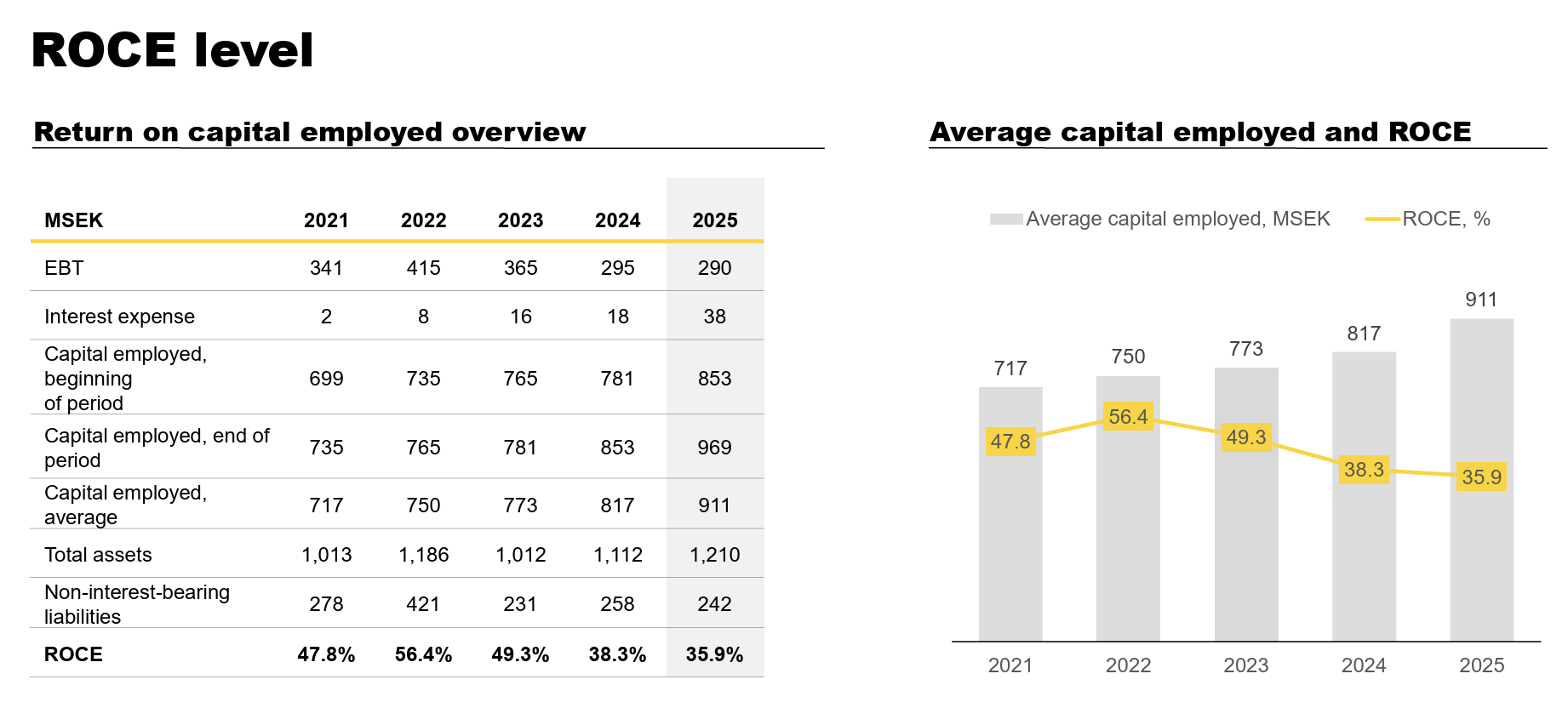

I’ve been eagerly following Engcon’s stock performance, but the company is still expensive. Especially since profitability (gross margins, ROCE) has been trending in the wrong direction in recent years. One can ponder these things for a while through “product mixes” and what not, but I wonder if there’s some structural pressure here. Even though the market is competed by a certain group, there is still competition.

The company’s NOPAT is roughly ~260 MSEK. Enterprise value is 8.8 billion. EV/NOPAT 34x.

Forward P/E with analyst estimates is 27x.

As written in the thread, there is considerable potential here, but it’s still a bit too expensive for my taste.