Well, since my opinion was asked… Am I wrong in thinking that ETC (Ethereum Classic) is speculation on prices, and it doesn’t directly expose one to value appreciation created by work? I have been very interested in it, though.

That’s probably how it is. Or perhaps the “physical” versions of the products are based on the actual price of the product and not on futures trading.

Edit: From what I’ve compared, the prices of minerals versus the ETC prices seem to follow each other quite accurately.

For comparison, here are the prospectuses for physical gold and (synthetic) copper ETC:

“Assets Physically backed with allocated metal subject to LBMA rules for Good Delivery”

“Replication Method Synthetic - fully funded collateralised swap”

Copper price development over the years:

https://www.macrotrends.net/1476/copper-prices-historical-chart-data

vs. Copper ETC:

3 Likes

This year, I have been following this “junior mining” company, which is the first foreign company to operate in Mongolia’s lithium fields.

1 Like

https://twitter.com/baldingsworld/status/1502031532021760004?s=21

This shouldn’t be possible in free markets, right? The Chinese nickel giant has hedged itself by buying a huge amount of nickel short, which has now created this short squeeze. HKEX owns LME and CCP owns HKEX, so to avoid the Chinese giant firm’s bankruptcy, CCP has closed LME. Can this be true? Is there any discussion about this somewhere?

5 Likes

Looks like Biden is investing in domestic production of critical minerals. Good for the portfolio ![]()

6 Likes

Well, that Monday morning dip didn’t require much timing ![]() . This has always been in my portfolio, either held or under monitoring. Monitoring is really difficult because you have to be aware of so many different things… Price development in raw material markets… possible future deals… competitors’ deals, etc., etc. For me, monitoring is made a bit easier when my portfolio contains coupons that are linked to Umicore through connections… e.g., Glencore, Daimler, etc. From that, a technical analysis (TA) then forms a picture of when to buy and when to sell.

. This has always been in my portfolio, either held or under monitoring. Monitoring is really difficult because you have to be aware of so many different things… Price development in raw material markets… possible future deals… competitors’ deals, etc., etc. For me, monitoring is made a bit easier when my portfolio contains coupons that are linked to Umicore through connections… e.g., Glencore, Daimler, etc. From that, a technical analysis (TA) then forms a picture of when to buy and when to sell.

Good and foreseeable… By following these old news stories, you can get pretty far ![]()

https://www.deraktionaer.de/artikel/mobilitaet-oel-energie/general-motors-und-volkswagen-setzen-auf-eigene-batterie-produktion-20243527.html

Sorry, I don’t have time to elaborate on this any further right now… a bit busy on the crypto side ![]()

![]()

1 Like

Umicore’s eventual daily gain of more than 10 percent is likely due to rumors that South Korean LG Chem is interested in acquisitions. Umicore was mentioned by name in the rumors.

3 Likes

Stories about lithium…

https://finance.yahoo.com/news/trouble-lithium-210044324.html

Goldman Sachs forecasts a collapse in lithium prices

1 Like

That “forecast” part fits perfectly if, according to them, the price of lithium rises in 2024. Production should then begin at the Keliber and Rhyolite Ridge mines ![]() . However, what is GS’s interest behind such a price forecast? I recall the massive short squeeze seen in the market price of nickel in early spring…

. However, what is GS’s interest behind such a price forecast? I recall the massive short squeeze seen in the market price of nickel in early spring…

They don’t mention anything about PGM (Platinum Group Metals) prices: 2E PGM, 4E PGM, and 6E PGM, which are also quite central to the industry in question. I might ask why this is the case?

It wouldn’t be the first time an analyst’s (anaalikon) forecast, for some reason, doesn’t match actual prices ![]()

![]()

![]()

1 Like

Keliber’s operations are progressing gradually

2 Likes

Ownership grows as expected ![]()

Sibanye / Keliber

Edit. Keliber’s press release on the matter is also a bit late.

3 Likes

Europe has also woken up to the fact that money needs to be invested in this theme to guarantee availability.

Article from two weeks ago:

The European Raw Materials Fund is due to start with around 2 billion euros ($2.1 billion), but eventually the region will need more than 100 billion euros in investment to produce enough critical minerals, Bernd Schaefer, chief executive of EU-funded EIT Raw Materials, told Reuters.

2 Likes

Brand new report:

BATTERY METALS MARKET UPDATE

5 Likes

Sweden’s LKAB finds Europe’s biggest deposit of rare earth metals

“Swedish state-owned mining company LKAB on Thursday said it had identified more than 1 million tonnes of rare earth oxides in the Kiruna area in the far north of the country, the largest known such deposit in Europe.”

5 Likes

Chile’s leftist president Gabriel Boric has presented his plan to nationalize the country’s lithium reserves.

Chile has the world’s largest lithium reserves and is currently the world’s second-largest lithium producer. Lithium is used, for example, in the manufacturing of batteries.

According to Boric, a 100% state-owned lithium company should be established in the country, through which production contracts would be signed.

There are currently two lithium companies operating in Chile. Boric is not proposing the termination of their contracts, but hopes that they will eventually join the state company voluntarily when their contracts expire.

According to Boric, nationalizing lithium is the country’s best way to continue economic growth in the short term.

Boric’s plan requires the approval of the country’s congress. Congress has not previously approved all of the president’s ambitious plans.

Edit: News from Yle, I removed the link myself completely as I couldn’t get it to work correctly.

3 Likes

Below are a couple of links where you can easily find more information. For now, the situation is confusing, and no one can yet say how that partial nationalization would be handled in practice.

These two large lithium mining companies are Albemarle and SQM. Albemarle’s situation is better in the sense that their land lease agreement doesn’t end until 2044, and Boric has promised to respect existing contracts. SQM’s lease agreement ends as early as 2030, but even before then, a couple of presidents will have time to change. And indeed, the parliament still needs to approve the plan once its details are presented.

In any case, this plan is another example of why political risk keeps the valuation multiples of South American mining companies (and certainly many other companies) in check. Boric’s leftist actions are baffling also because these companies have already been returning a significant portion of their profits to the state:

Albemarle also noted it pays a lithium royalty rate that can be as high as 40%, the highest lithium royalty in the world

Does Boric really believe that a better outcome will be achieved as a state-owned company? Investments might suffer a bit before this matter is resolved…

https://www.mining.com/chile-to-nationalize-its-lithium-industry/

https://www.mining.com/web/sqm-sees-pathway-to-continue-mining-lithium-in-chiles-new-model/

https://seekingalpha.com/article/4595845-chilean-lithium-nationalization-albemarle-sqm

Itseäni asia koskee myös kun on pikkusiivu Lithium Power Internationalia salkussa. Tässä heidän kannanottonsa uutiseen:

THE NEW CHILEAN NATIONAL LITHIUM POLICY

Lithium Power International Limited (ASX: LPI) (“LPI” or the “Company”) is pleased to provide updated

comments on the recent announcement of the new National Lithium Policy in Chile, and the potential

impact it will have on the company’s Maricunga lithium brine project.

On the evening of 20 April 2023, Chilean President Gabriel Boric announced the long awaited National

Lithium Policy (“NLP” or the “Policy”). The NLP outlines the plans for the future implementation of

lithium exploration and exploitation policies that are intended to bring Chile back to the forefront of

global lithium production.

The NLP is different from the position of previous administrations, with this new policy being the result

of a consultation process with a wide variety of stakeholders nationally and internationally. It has also

taken into consideration the objectives of the Chilean State, including its role to participate in the

efficient and rapid development of the lithium industry. This is of strategic concern both to Chile and

the world as society moves towards “electrification.” LPI and its subsidiary Minera Salar Blanco have

been in constant dialogue with the Chilean government and private institutions that have participated

in the development of the NLP.

Lithium Power International’s Director and MSB’s Chairman, Russell Barwick, commented:

“We are pleased that the National Lithium Policy, as presented last week in Santiago, is very much

along the lines of what was discussed and expected in our various discussions with Chilean authorities. While a central part of the strategy focuses on current operations and future exploitation of the Atacama Salar, there is also an outline on the future development of projects in other Chilean Salars. This is the case with our flagship Maricunga Project, which is the largest, most advanced and fully

permitted pre-construction lithium project in Chile.”

Even though the Policy has primarily concentrated its focus on the huge lithium resource within the

Atacama salar, LPI wishes to clarify some core elements of the new Policy as it relates to the

Company’s Maricunga Project and assets:

• The Maricunga Stage One project is fully permitted for construction. Its Environmental Permit

(“EIA”) was approved in 2020 by the “Servicio de Evaluación Ambiental” (“SEA”), which was

explicitly mentioned by President Boric as the government agency in charge of environmental

aspects of any future project in Chile. LPI’s EIA permit was ratified by the Committee of

Ministers of the Chilean Government in 2022, rejecting all the objections submitted by third

parties. It also obtained the necessary Chilean Nuclear Energy Commission (“CCHEN”) permit

in 2018 that allows LPI to export lithium products from Chile.

• With regards to the inclusion of communities and the environmental and technical aspects

mentioned on the new Policy, LPI’s Maricunga Stage One project development serves as an

example by incorporating all social and community agreements as an integral part of its

environmental permit. This includes Maricunga being one of the few projects in Chile with a

comprehensive indigenous consultation process executed by the Government under the ILO

Convention 169, defining a new standard of social relationships. The Company is proud of

these achievements in promoting community participation over the long-term.

• The Maricunga project has established broad ranging the sustainable development initiatives,

which sets a unique and complete ESG profile standard for the future of the project. LPI’s

corporate vision aims to make the Maricunga Project one of the first lithium operations

globally to achieve carbon neutrality.

• The Company confirms that its wholly owned subsidiary Minera Salar Blanco (“MSB”), is the

sole owner of the property and concessions of both Stage One and Stage Two of the

Maricunga Project. There are no current legal processes challenging this aspect of the project.

This is a fundamental difference from the current operations in the Atacama Salar, where

state-owned company CORFO is the owner of the properties and concessions. CORFO then

leases these concessions to the current operators in Atacama for a set period of time. It is also

important to note that the mining concessions that serve as the base for the Maricunga Stage

One project, were given by the Chilean Government, before 1979 when only then did lithium

become defined as a strategic material.

• The Maricunga Stage One concessions, because of their pre-1979 “Old Code” status, do not

require a CEOL (Special Lithium Operation Contract) for exploitation. The Stage One project is

shovel ready, and currently awaiting the closing of its financing process to begin construction.

• It is important also to clarify that a CEOL does not provide any claim to ownership over the

area included under the CEOL contract. CEOL’s explicitly establish, that holders of the CEOL

have no rights to enter the area, or execute any activity, (exploration or exploitation ), without

a previous negotiation with the owners of the mining concessions.

• LPI embraces the possibilities for future public-private alliances as declared by the NLP, for

the development of Stage Two for the Maricunga project, which involve its post-1979 or “New

Code” concessions. The Company will continue to work closely with the Chilean Government

to transform the Maricunga Stage Two project into the first example of a public-private

alliance under the new parameters established by the new Policy.

• The Company acknowledges the existence of the Australia–Chile Free Trade Agreement

(“FTA”), which came into force in 2009, being the first FTA between Australia and a Latin

American country, as well as the Trans-Pacific Partnership (“TPP”) recently ratified by

Australia and Chile. Both international arrangements will positively support these publicprivate alliances and also incorporate clear mechanisms for investment protection under

international law.

• The new Policy does not constitute a nationalisation of the lithium industry in Chile. Its

objective, as clarified by the Mining Minister, is to set the conditions and parameters for the

country to have a more active involvement and higher financial returns in a strategic industry,

particularly where those lithium resources are located on concessions already owned by the

Chilean State on the Atacama Salar. The NLP also seeks to accelerate the development of new

projects in the country.

• LPI is currently evaluating a number of financing options for the Maricunga Stage One project,

ranging from strategic equity investment from potential offtake partners to debt/equity

financing alternatives. The announcement and future implementation of the NLP is timely to

provide the clarity and certainty required by financiers/investors on the parameters under

which the Maricunga project will be developed.

Lithium Power International’s Chief Executive Officer, Cristobal Garcia-Huidobro, commented:

“We are very pleased to see that our hard work over the last seven years of advancing Maricunga

Stage One project have been reflected in a development that closely mirrors the objectives of the newly

announced National Lithium Policy. Technical advancement and innovation, environmental and social

responsibility of the highest standard, and landmark community agreements that provide the

community the opportunity to share in the exciting future of the growing lithium industry, are all in

line with the objectives of the Strategy. We embrace the objective of Chile’s current administration to

promote public-private associations as the path forward for the development of the Maricunga Stage

Two project.

Since the announcement of the Strategy, there have been a number of differing opinions as to the

effectiveness, practicality, and legality of the National Lithium Strategy and its objectives. LPI wants

to clarify, that it believes the Policy is not a “one size-fits all” proposed legislation, and there are several

specific elements that differentiate LPI’s Maricunga Project from the rest of the existing operations or

future lithium projects in Chile. Rather than focus on what the legislation means for the future of the

Chilean lithium industry, our focus is on what it means for our Maricunga lithium project and how it

will transform the Chilean lithium industry through its development. At LPI, we welcome President

Boric’s National Lithium Strategy and its objective to positively transform the Chilean lithium industry.

Moreover, we are pleased to say we believe this strategy not only benefits LPI’s Maricunga Project but

has the potential to accelerate the development of our Stage Two project. As such, we look forward

to continuing our work with the Chilean Government to advance Maricunga.”

3 Likes

"Good news for fertilizer, solar panel, and electric vehicle battery companies: a massive underground deposit of high-grade phosphate rock has been discovered in Norway, containing enough minerals to meet global demand for those products for the next 50 years.

Norwegian mining company Norge Mining said the 70 billion tonnes of phosphate rock was uncovered in the southwest of Norway, where it sits alongside other minerals such as titanium and vanadium that are used in the aerospace and defense industries. Update (July 7): Norge Mining in an email let us know they have revised their estimate for how long the deposit allows for a supply of phosphate rock from 100 years to 50 years."

6 Likes

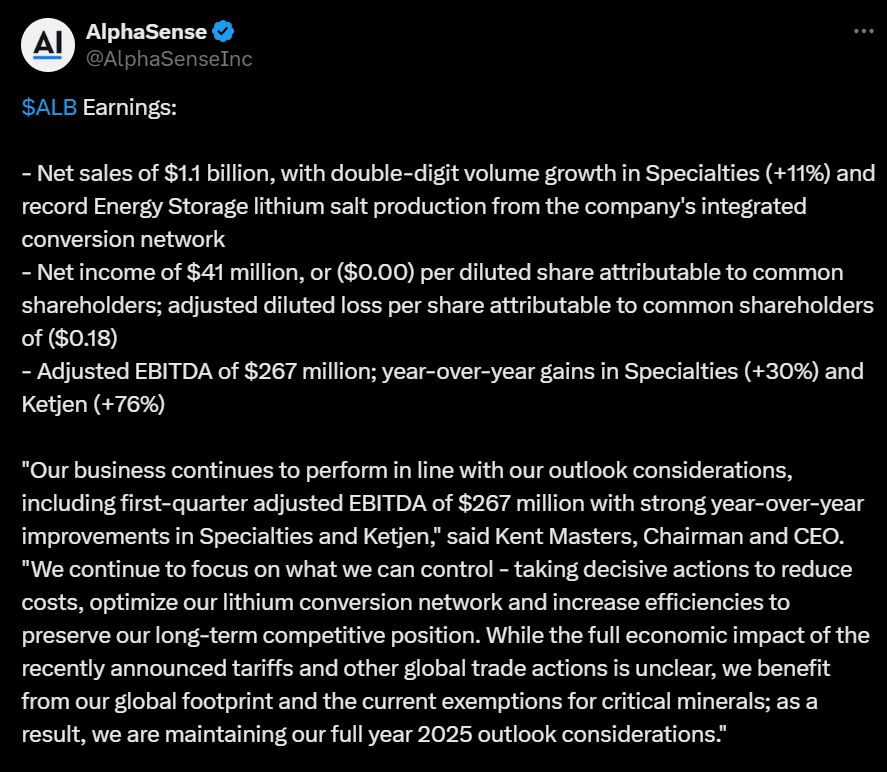

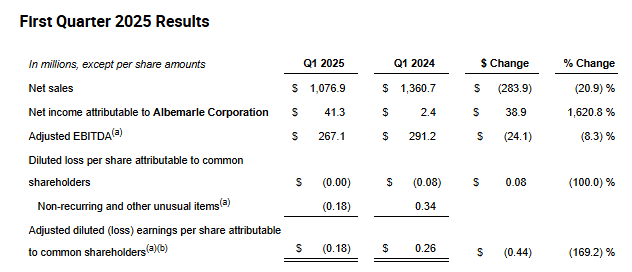

Good old 𝗔𝗹𝗯𝗲𝗺𝗮𝗿𝗹𝗲 ![]()

I posted this in case anyone is interested. I’m not really up to speed on this myself.

Albemarle increased production of specialty products and lithium, but the result remained in the red.

Management emphasizes cost cutting and improving efficiency to maintain competitiveness.

2 Likes