I came across Elecster as part of my own project. The company generates very little discussion, and even in terms of the numbers, it’s hard to find anything particularly interesting about it. On an earnings basis, valuation levels lean towards being a bit too expensive.

However, the valuation level has dropped to a low P/B of 0.4x, which increases the interest in taking a closer look at the balance sheet contents. The market cap is only 10 million.

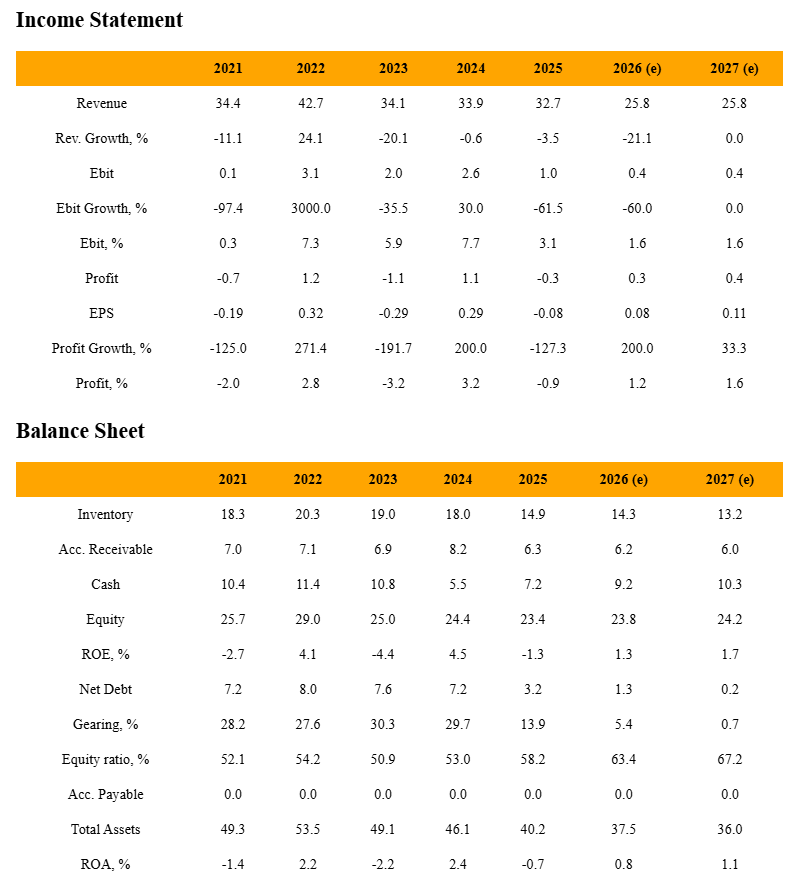

The valuation algorithm sets the target price at approximately the P/B 1.0 level and gives a Buy recommendation. There would at least be potential for upside compared to the current level.

More detailed information and forecasts: https://www.quantfactory.eu/HelsinkiOMXH/ELEAV.he

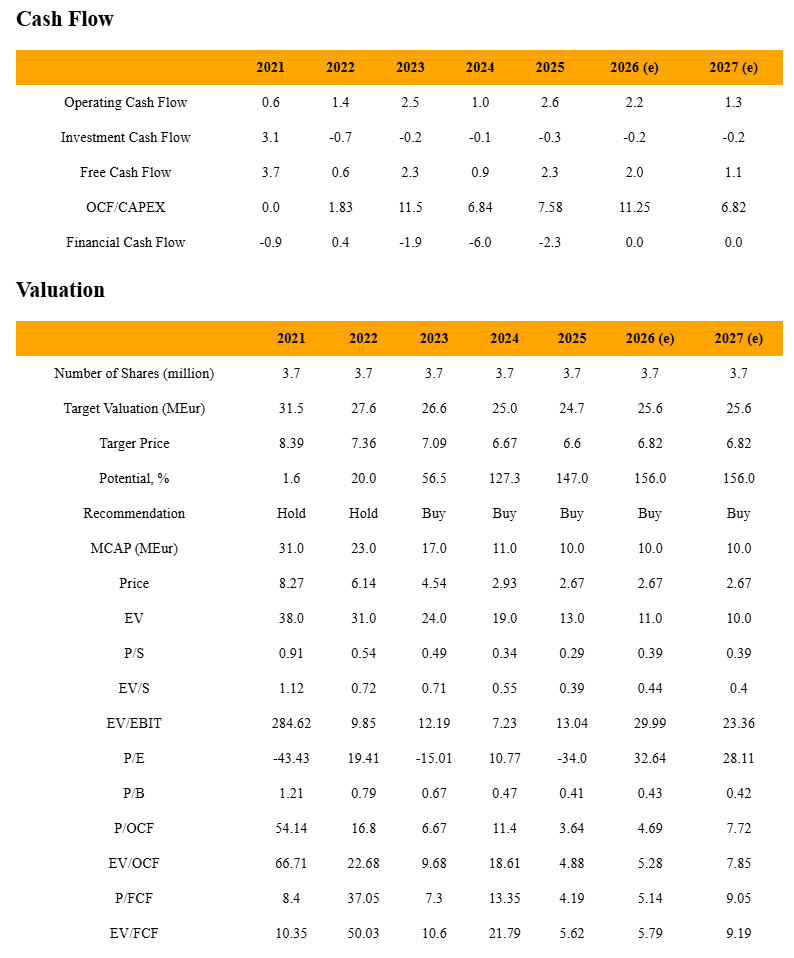

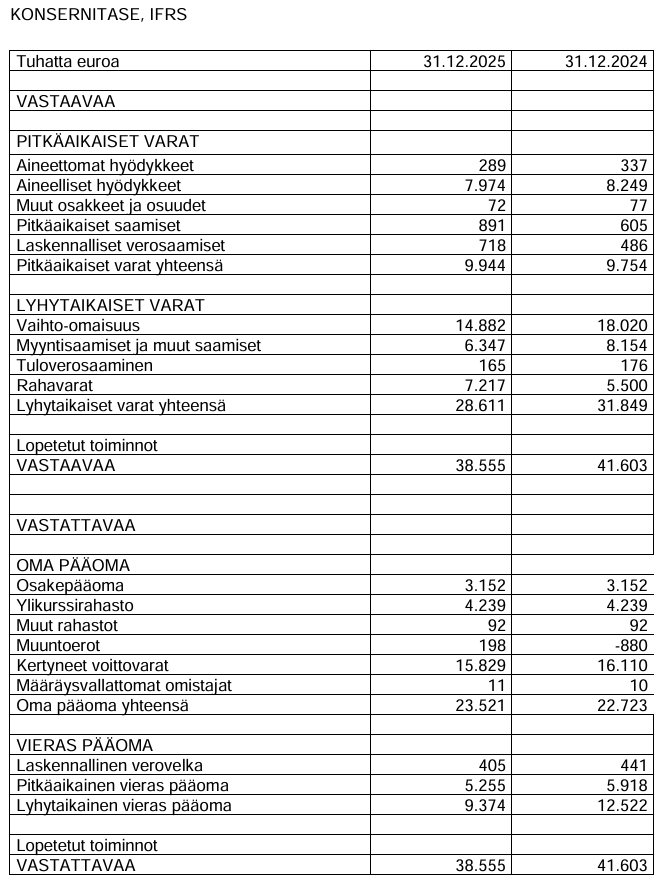

Most of the assets on the balance sheet from the recent financial statement are current assets, totaling 28.6 million, which are likely close to their fair values. There are 7.2 million in cash and equivalents, which is a fairly significant amount relative to the market cap. A generous dividend could bring some momentum to the company’s valuation.

Non-current assets are mostly tangible assets, so there shouldn’t be any major risk of write-downs associated with them.

For my taste, there aren’t quite enough ingredients for an investment decision. If this were combined with an improvement in profitability, Elecster could be a very interesting investment.