Suomalainen pörssiyhtiö Elecster Oyj keskittyy UHT-maidon (Ultra High Temperature eli iskukuumennettu maito) käsittely- ja aseptisten pakkauslinjojen suunnitteluun, valmistukseen ja markkinointiin sekä näihin liittyvien pakkausmateriaalien maailmanlaajuiseen myyntiin. Yrityksen pääasiassa vientiin suuntautuvista tuotteista 80–90 % toimitetaan noin 60 eri maahan.

Aavistuksen mutuilemalla keksityt plussat ja miinukset:

Plussat:

operatiivinen kannattavuus on parantunut ensimmäiseen vuosipuoliskon suhteen

meijerikoneiden kysyntä nousussa

yhtiö toimii monilla eri markkinoilla, kuten Aasiassa, Balttiassa ja Pohjoismaissa

ilmeisesti jatkuvaa tulovirtaa tuo tekninen tuki ja huoltopalvelut

Miinukset:

negari, sijoittajat eivät arvosta

yhtiö ei ole Inderesin seurannassa, joten siksi tämä on paljon paljon tuntemattomapi, ihan vieras mulle

pakkausmateriaalien toimitusten väheneminen

markkinaympäristö ei ole suotuisa tällekään yhtiölle

**SISÄPIIRITIETO, TULOSVAROITUS: ELECSTER ALENTAA LIIKEVAIHTO- JA TULOSARVIOTAAN **

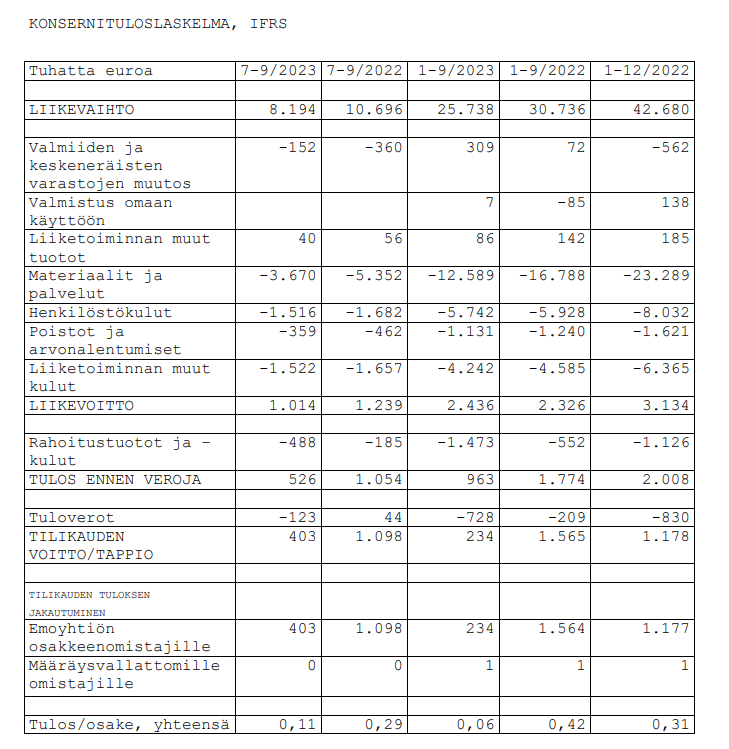

Elecster-konserni alentaa vuoden 2023 liikevaihtoa ja osakekohtaista tulosta koskevaa ohjeistusta.

Uusi ohjeistus Koko vuoden osalta arvioimme konsernin liikevaihdon pienenevän ja osakekohtaisen tuloksen painuvan tappiolliseksi.

Aiemmin Elecster on arvioinut koko vuoden liikevaihdon säilyvän samalla tasolla tai pienenevän ja osakekohtaisen tuloksen säilyvän samalla tasolla tai paranevan edelliseen vuoteen verrattuna.

Korkojen nousu, sekä Elecsterin kannalta keskeisten valuuttojen arvon tuntuva alentuminen euroon nähden ovat merkittävästi nostaneet rahoituskustannuksia ja hidastaneet asiakkaiden investointihankkeiden toteutumista ennakoitua enemmän. Osittain samasta syystä pakkausmateriaalien toimitusvolyymi jäi viimeisellä vuosineljänneksellä selkeästi vertailuvuoden tasoa alemmaksi. Tulosta heikentävät myös saataviin kohdistuvat kertaluonteiset alaskirjaukset, joilla ei ole vaikutusta kassaan. Täten operatiivisen kannattavuuden suhteellinen parantuminen ei täysimääräisesti heijastunut osakekohtaiseen tulokseen.

Elecster on Helsingin pörssin tupakantumppi. Yhtiö ei tunnu kykenevän kannattavaan kasvuun bisneksen junnatessa paikallaan vuosi toisensa perään. Lisäksi yhtiöllä on K-osakesarja, jolla äänivalta rohmuttu pienille piireille. Nuo saisi jo lopullisesti kuopata listattujen firmojen osalta

Osta, mutta hyvin hyvin halvalla ja muista myydä ajoissa. Keskinkertaisiin bisneksiin ei kannata rakastua ja jäädä odottamaan kuinka yhtiö alkaisi jollain ilveellä tuottamaan lisäarvoa omistajilleen

Lisäisin miinuslistaan Elecsterin läsnäolon Venäjällä. Asialla on moraalinen puolensa, mutta myös maariski liiketoiminnan jatkuvuudelle. Pakotteet eivät ole koskeneet Elecsterin kalvotehdasta Permissä toistaiseksi eikä hallinto ole sosialisoinut toimintaa, toistaiseksi.

Vielä 2021 vuosikertoimuksessa kuvattiin Venäjän toimintoja, mutta 2022 vuosikertomuksessa ei liene haluttu enää korostaa bisneksiä siellä ja toimintokuvaus on jätetty pois.

2021 vuosikertomuksesta:

“Elecster toimii Venäjällä tuotemerkillä Finnpack, koska nimellä on vahva imago ja vuosikymmenten perinteet paikallisessa meijeriteollisuudessa. Finnpackilla on Venäjällä kaksi toimipistettä, Pietarissa toimisto ja Permissä kalvotehdas.

Permin kalvotehdas pitää huolen siitä, että IVY-maiden alueen asiakkaille saadaan nopeasti toimitettua hyvälaatuista pakkausmateriaalia Elecsterin toimittamiin pakkauskoneisiin. Permin kalvotehtaan tiloihin on tullut noin 40 % lisää tuotannon toimitilaa, joka mahdollistaa entistäkin laadukkaamman kalvonvalmistamisen tason. Uuden toimitilan rakentaminen sisäpuolelta on vielä kesken, mutta käyttöönoton tulisi tapahtua vuoden 2022 aikana.”

Tähän sellainen heitto, että Elecsterin UHT-maidon linjastoja ei taida olla Pohjoismaissa juurikaan. Maidon kulutus kasvaa edelleen kehittyvissä maissa ja UHT-maidon prosessi- ja pakkauslinjastoja meneekin lähinnä niihin maihin, joissa ei ole edelleenkään luotettavaa kylmäkuljetusketjua. UHT-maito muovipakkauksessa säilyy lämpimässä pitkään. Maidon kulutustilastoja kannattaakin seurata Etelä-Amerikka, Afrikka, kehittyvät Aasian maat -suunnilla. En nyt alkanut kaivamaan faktaa, mutta ymmärtääkseni kulutus kasvaa ko. alueilla edelleen.

Voi kasvaa, mutta tarkasteltaessa myyntiä Suomeen, Eurooppaan ja muihin maihin ei voi todeta minkäänlaista trendinomaista kasvua näissä ns. kasvusegmenteissä. Yhtiö voisi periaatteessa olla mielenkiintoinen mikäli sillä olisi kasvumarkkina, jonka päämarkkinoiden taantuminen peittäisi, mutta mitään tällaista ei numerot anna olettaa

Elecster ei kait ole tarkemmin avannut Venäjän osuutta myynnistä? Niin tai näin niin tuolle ei varmaan kannata antaa paljon arvoa. Vaikka bisneksiä jatkettaisiin niin talous luultavammin kyykkään pahemmin jossain vaiheessa ja liiketoiminta maassa ajautuu ongelmiin

SV. Sisältää proosaa (‘I suffered for my art, now it’s your turn’ - Marshall Crenshaw)

Kun ketju aloitettiin, surffailin aika paljon yrittäen löytää infoa näiden linjastojen markkinasta, lähinnä kilpailijoista. En oikein saanut kiinni teknisistä kuvauksista oliko kilpailijoilla mahdollisuutta samankaltaiseen modulaariseen lähestymistapaan mikä kyllä Elecsterillä näyttää hyvältä.

Näiden linjastojen tarjoajilla tuntuu olevan informointitapana ‘jos haluat tietää enemmän, myyntiosastomme on enemmän kuin halukas keskustelemaan kanssasi’ Joten pintaraapaisuksi jää.

Näin ollen päätin että oikea lähestymistapa olisi tavata firman vuosikertomukset läpi 20v ajalta ja kirjata ylös kehityskaari (luvuilla höystettynä) tähän päivään. Vuosikertomuksessa kuitenkin on pohdintaa markkinoista ja teknologiasta tasolla, johon ei googlettelemalla yllä. Tähän ei nyt kuitenkaan aika&into riitä, mutta suosittelen sitä @Sijoittaja-alokas jos et ole jo tehnyt.

Silmäilin itse muutaman (päällipuolisesti) 2002-2003, 2021-2022 ja eihän siinä mitään. Tasaista puksutusta ehkä tavanomaista suuremmalla riskillä. Porukka on sama, ainakin samaan sukuun kuuluva toimari alkuajoista on vain valunut hallitukseen ja uusi valittu tilalle. Kassavirtaluvut on samalla pallokentällä 20v molemmin puolin eli en nyt oikein mitään vettä kielelle nostattavaa näe tässä. (tase tietty vahvistunut, ainakin omaan harjaantumattomaan silmääni)

Koko firman historian ajan on ollut kova tarve maailmalla tietyissä paikoissa hyvin säilyvälle maidolle mutta ei kummempaa raketointia kai ole tapahtunut tällä alalla. Minkään valtiollisten tahi YK- yms projektien/puheiden varaan en alkaisi projisoimaan mitään. Pikatuomiona pitäisin tällä hetkellä OMXH25-indeksiä suorastaan ylivertaisena sijoituskohteena tähän verrattuna kun puntaroidaan riskejä, jotka tässä ovat huomattavat. Eri asia jos poraa syvemmälle ja huomaa jotain mikä on minulta piilossa.

@Iikka on tehnyt erinomaisen tviittiketjun yhtiöstä.

Kiitos Iikka, tästä yhtiöstä puhutaan liian vähän. En ole yhtön fani, mutta kiva, kun näistä tulee lisää tietoa ja ajatuksia, mistä yleisesti puhutaan vähän.

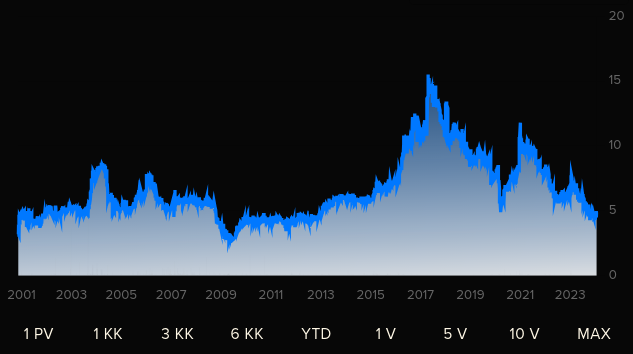

Elecsterin osakekurssi kyntää.

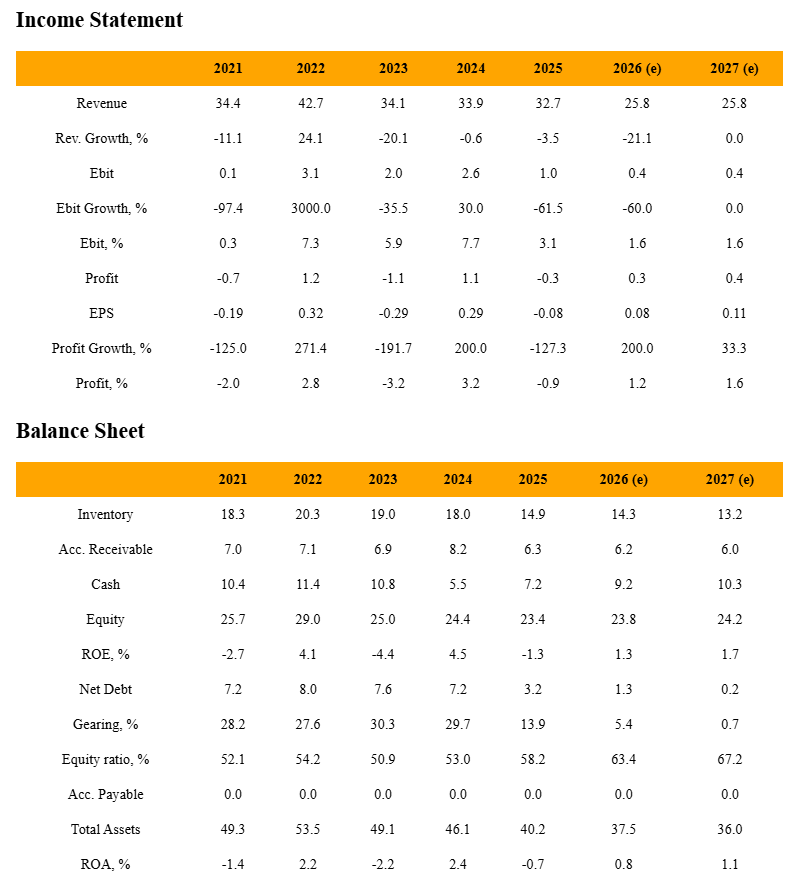

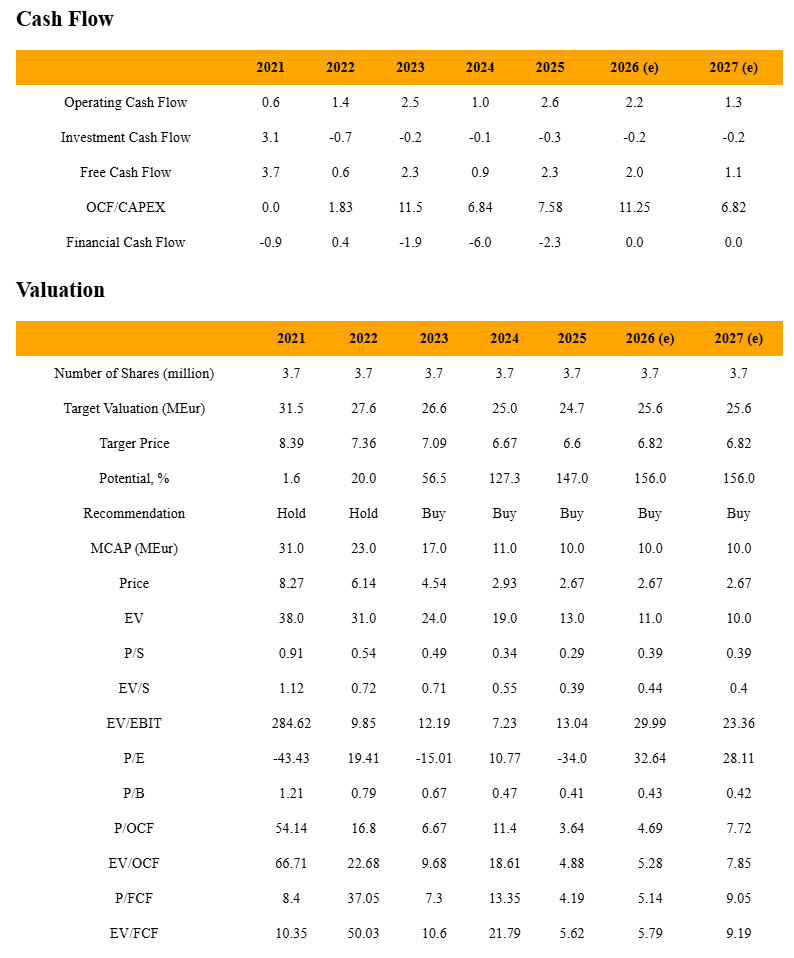

Elecster on onnistunut tekemään hyvinä vuosina n. 2,5M€ tilikauden tulosta.

P/E-luku olisi tällöin 5,5x, joka ei ole paljon, mutta yhtiössä on riskejä…

Kiitos @Iikka ketjusta! Joskus vuosi-kaks takaperin tuli itsekin firma käytyä läpi. Firma on mielestäni juurikin näennäisen halpa, sillä jos katsoo yhtiön vapaan rahavirran suurutta suhteessa yritysarvoin, niin ei tämä ole enää edes halpa. Kasvu on tiukassa ja tulos voi olla jopa paineessa. Liikaa toimintaa on riskissä autoritäärisissä maissa ja kasvu otettava kehitysmaissa. Syystä halpa, mielestäni.

Erittäin hyvin tiivistetty! Olen samaa mieltä, että arvostuskertoimia painaa liiketoiminnan fokus kehittyvissä tai autoritäärisissä maissa. Tässä on vähän samaa kuin Tecnotreessä, jonka toiminnan ydin on kehittyvissä maissa, joissa paikallinen valuutta ei ole aina välttämättä kovin stabiili.

Kehittävissä maissa pitäisi ensin olla alkutuotantoa mitä iskukuumentaa ja pakata. Esim. Aasiassa käytetään paljon ulkomailta tuotuja UHT-maitoja, “tuoretta” maitoa alkanut saamaan vasta viime vuosina.

Alkutuotannon kasvaminen on hankalaa ja aikaa vievää. Näin ollen en usko tämän yrityksen lähitulevaisuuteen

Elecster julkaisi tuloksensa ja tuolla alla olisi linkki sitten koko tiedotteeseen. Nostin vain muutamat asiat tähän alle.

Elecsterin Venäjän liiketoiminta on pääasiallisesti paikallisen tytäryhtiömme valmistamien pakkausmateriaalien myyntiä paikallisille meijerialan yrityksille. Pakotteita on laajennettu moneen kertaan ja sillä on ollut vaikutus myös Elecsterin vientiin Venäjälle.

Vetäytyminen Venäjän toiminnoista olisi myös Elecsterin osalta aikaavievä ja vaikea prosessi. Aiemmin ilmoitetun mukaisesti Elecster-konserni toistaiseksi jatkaa Venäjän toimintojaan ja seuraa tilanteen kehittymistä.

Hyvän tilauskannan ansiosta näkymä vuodelle 2025 on positiivinen. Meijerikoneiden osalta odotamme positiivistä kehitystä heti vuoden alusta lähtien ja pakkausmateriaalien osalta odotamme, että toimitusvolyymit ovat ensimmäisellä vuosipuolikkaalla samalla tasolla kuin vertailuvuonna ja toisella vuosipuolikkaalla panostuksemme pakkausmateriaalien myynnin kasvattamiseksi alkavat näkyä toimitusvolyymin kasvuna.

No niin, tällainenkin Tomi Lahden tviitti tuli vastaan:

On kumma selitys kvartaalista toiseen, että kalvopakkaustehtaasta venäjällä on niin kovin vaikeaa luopua. Onnistuihan esimerkiksi Huhtamäki poistumaan Venäjältä ryhdikkään nopeasti. Ihmettelen tätä yhtiön motiivia pysyä tiukasti terroria harjoittavassa maassa. Ehkäpä, kun on riittävän pieni yhtiö, niin pystyy tutkan alla siellä vielä operoimaan. Isompana yhtiönä tästä jäisi eri tavalla kiinni.

Luulen, että moni piensijoittaja ei periaatteesta halua tähän Akaan ihmeeseen enää sijoittaa tämän Venäjä-kytköksen vuoksi.

Alla oleva Kauppalehden juttu ei ole ainakaan vielä maksumuurin takana. Bongasin jutun Sijoituskästin Jani Järvisen X-tililtä.

Elecster tiedotti tilinpäätöstiedotteessaan maaliskuun alussa yhtiön Kiinan tytäryhtiössä mahdollisesti tapahtuneesta kavalluksesta, jota Kiinan poliisi tutkii. Yhtiö kirjasi kavallusepäilystä noin 1 miljoonan euron kertaluontoisen arvonalentumiskirjauksen viime vuoden viimeisen vuosineljänneksen tulokseen.

Vastaavasti Elecster kertoo, että sen Venäjän liiketoiminta on pääasiallisesti paikallisen tytäryhtiön valmistamien pakkausmateriaalien myyntiä paikallisille meijerialan yrityksille. Pakotteita on laajennettu moneen kertaan, ja sillä on yhtiön mukaan ollut vaikutus myös Elecsterin vientiin Venäjälle.

Oman projektini puitteissa tuli tutustuttua Elecsteriin. Yhtiö ei juurikaan keskustelua synnytä, eikä numeroidenkaan puolesta yhtiöstä on vaikea kiinnostavia asioita. Tulospohjaisesti arvostustasot kallistuvat turhan kalliin puolelle.

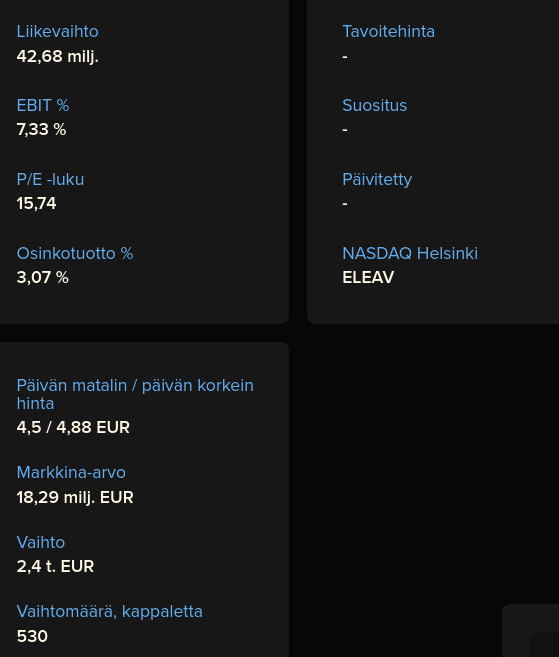

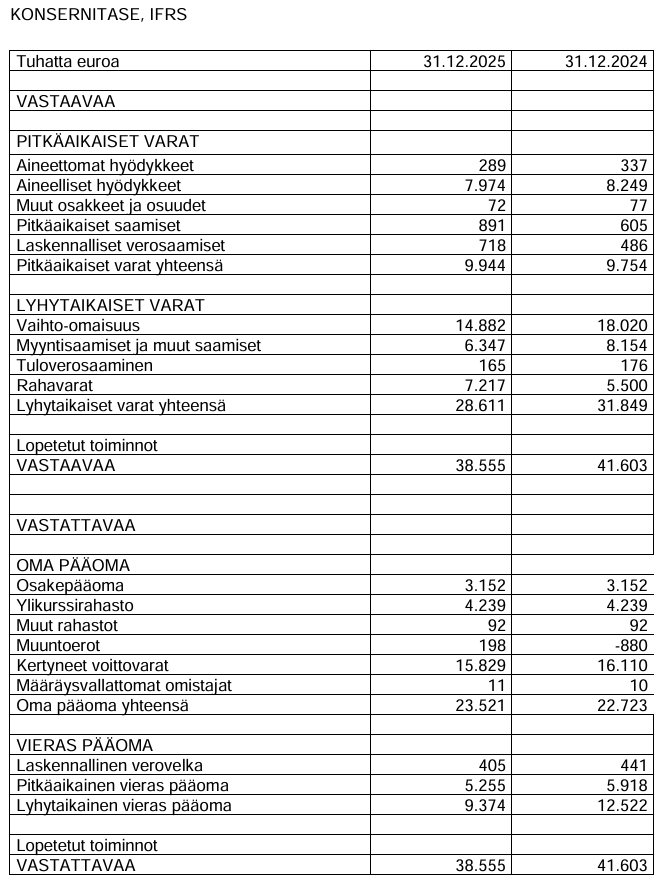

Arvostustaso on kuitenkin laskenut alhaiselle P/B 0,4x tasolle, mikä lisää mielenkiinto tutustua paremmin taseen sisältöön. Markkina-arvo on vain 10 miljoonaa.

Arvonmääritys algoritmi määrittää tavoitehinnan suunnilleen P/B 1,0 tasolle ja antaa Osta-suosituksen. Potentiaalia nousulle ainakin löytyisi nykytasoon verrattuna.

Suurin osa tuoreen tilinpäätöksen taseen varoista on lyhytaikaisia varoja 28,6 miljoonaa, jotka on luultavasti lähellä käypiä arvojaan. Rahavaroja löytyy 7,2 miljoonaa, mikä on aika merkittävä määrä markkina-arvoon suhteutettuna. Reiluhkolla osingolla voisi saada vauhdikasta liikettä yhtiön arvonmääritykseen.

Pitkäaikaiset varat ovat enimmäkseen aineellisia varoja, joten suurempaa alaskirjauksen riskiä ei näihin liittyen pitäisi olla.

Omaan makuun ei ihan tarpeeksi ole aineksia sijoituspäätöstä varten. Mikäli tähän yhdistyisi kannattavuuden paraneminen niin Elecster voisi olla hyvinkin mielenkiintoinen sijoitus.