This thread has been quiet for over three months. ![]()

@Tommi_Saarinen and @Antti_Viljakainen have provided preview comments ahead of the company’s H1 business review. ![]()

This thread has been quiet for over three months. ![]()

@Tommi_Saarinen and @Antti_Viljakainen have provided preview comments ahead of the company’s H1 business review. ![]()

This can probably be considered positive news. In Inderes’ forecasts, EBITDA is assumed to be 2.1 million this year, so there is potential for a positive surprise; additionally, uncertainty decreased through the guidance.

Tommi Saarinen interviewed Ecoup CEO Matti Kaski.

Topics:

00:00 Introduction

00:11 H1’24

01:37 Single-family house renovation

03:40 Technology business

05:52 Guidance and outlook

06:59 Impact of the new Vantaa production facility

07:49 Export outlook

Tommi and Antti have published a new company report on EcoUp. ![]()

EcoUp yesterday released its seasonally quiet H1 report, with the headline figures exceeding our forecasts. Additionally, the guidance issued by the company on Friday for the 2024 financial year reinforced our confidence in EcoUp’s ability to manage reasonably well in the current difficult market environment. Forecast changes following the report were limited to minor adjustments. Reflecting the stabilization of risks for the current year and the approaching earnings turnaround we forecast, we are raising our target price for EcoUp to EUR 2.00 (prev. EUR 1.80). However, as the overall valuation has slightly tightened due to the share price rise and the expected return remains neutral, we reiterate our Reduce rating.

Quote from the report:

Due to the back-loaded expected return (i.e., a significant earnings jump is likely required in 2026) and the high required rate of return, relying on this is not yet attractive. However, these calculations illustrate the share’s substantial upside in a scenario where the company reaches a trajectory towards its targets, or even our forecasts, in 2026.

I wrote about RT’s review in the LapWall thread. For EcoUp, the most relevant market is specifically small house construction, for which RT predicts a clear bottoming out for the year 2024.

EcoUp announced during the past week that it has made a conditional takeover bid for an insulation installation and sales company operating in Sweden. The target has encountered financial difficulties, which has apparently helped open the possibility for a moderately priced acquisition. The target’s 2022 revenue was approximately EUR 4 million (about 12% of our 2025 revenue forecast for EcoUp), so if completed, the acquisition would impact our forecasts for the coming years. The acquisition would have a clearly smaller impact on profitability forecasts, as the acquired company is less profitable compared to EcoUp.

From a strategic perspective, I believe EcoUp has fairly clear plans to implement a profitability turnaround for the target, as EcoUp has known the target through a customer relationship for many years. Furthermore, with the acquisition, EcoUp will have its own installation resources outside of Finland for the first time, which should support its position in export markets.

We commented on the takeover bid earlier here.

Tommi’s and Antti’s preview comments as EcoUp releases its Q3 report on Tuesday. ![]()

We expect the main line items to have settled broadly near the levels of the comparison period in a continued slow market environment. In our forecast, the decent development of the detached house renovation business and internal cost structure adjustment measures act as an antidote to the weak market situation. We do not expect the technology business to have generated revenue in Q3. We expect EcoUp to reach its guidance for the current year, although this requires a good performance during the seasonally busier end of the year.

Tommi’s and Antti’s quick comments on the Q3 results. ![]()

EcoUp published its Q3 business review this morning. Q3 revenue exceeded our forecasts as the company achieved growth driven by single-family house renovations in a shrinking market. Higher-than-expected revenue also helped the company beat forecasts in terms of profitability. EcoUp reiterated its full-year guidance as expected. In the insulation business, the short-term market situation remains very difficult, although the report showed that the company has performed commendably in a challenging market. Regarding the progress of commercializing the technology business, additional information remained scarce.

EDIT:

Here are also ROBO’s comments, what do you think of ROBO’s comments? ![]()

Here is a new company report from Tommi and Antti right after Q3. ![]()

The overall picture of EcoUp’s Q3 report was positive, as both revenue and profitability exceeded our forecasts. Our earnings forecasts rose slightly, even though we lowered our expectations regarding the progress of the Technology business’s commercialization. The expected return as the earnings turnaround progresses is attractive, but the uncertainty related to the turnaround in the residential construction market and the commercialization of the Technology business keeps the stock’s risk/reward ratio neutral.

Quoted from the report:

On an earnings and EBIT basis, EcoUp is priced very high for both 2024–2025. Consequently, it is only the 2026 forecasts that start to look attractive. When relying on 2026, forecast risks are high, but in our view, achieving clear earnings growth is very likely as the current historically poor market situation subsides.

Here’s a new company report on EcoUp from Antti and Tommi. ![]()

EcoUp announced yesterday that its conditional acquisition offer for an insulation sales and installation company operating in Sweden is proceeding according to the original terms. With this acquisition, EcoUp expands into Sweden with a small investment and a moderate risk level. The deal had only a small impact on earnings forecasts for the coming years due to the target’s recent weak profitability. With EcoUp’s share price decline and the approaching turnaround in small-house construction, we estimate that the risk/reward ratio is becoming attractive. Thus, we reiterate our target price of 2 euros and raise our recommendation to Add (previously Reduce).

Quoted from the report:

Despite its small size, the acquisition is strategically significant for EcoUp, as the acquired companies will create the first proprietary sales and installation unit outside Finland. With the debts forgiven in the debt restructuring, we also consider the purchase price reasonable relative to Isoleringslandslaget’s earnings potential (EV/EBITDA approximately 4.5x based on 2022 EBITDA).

Alongside market capitalization comparisons, it’s worth checking what EV, or the component added to enterprise value, i.e., net debt, is.

In Ecoupin’s case:

Sometimes that net debt can be quite significant, or non-existent, or very different from other companies in the industry.

During the COVID era, Outokumpu had net debt over 2 EUR/share and the share price was just over 2 EUR/share, meaning the enterprise value was double the market capitalization. Subsequently, the entire net debt disappeared completely, and the market capitalization matched the enterprise value.

In Ecoupin’s case, the enterprise value is about 20% on top of the market capitalization, i.e., about 0.55 EUR/share. So, probably not bad if the company’s financing is sound, or if cash flow is generated from operations.

Yep, in my opinion, there’s no problem with the balance sheet (yet), even though free cash flow has been negative every year due to large investments and a poor market.

At the end of H1’24, net debt was exactly that approx. €5M.

EcoUp only reports exact figures semi-annually; however, cash flow was positive in Q3. Seasonally, June-December are the strongest months, as construction sites are completed and homes are insulated. In Inderes’ forecast, net debt is €3.4M at the end of 2024.

EcoUp’s Q32024 Business Review, Market Outlook:

The company’s own estimate continues to be that the market for small-house construction will turn for the better in the first half of 2025, and in 2026, small-house starts will return to the long-term average of approximately 10,000 units. The company’s financial targets for the Insulation Business by the end of 2026 are also based on this estimate.

In my opinion, it is entirely justified to ask whether the assumptions underlying the setting of these targets are realistic. When examining housing starts by type of house (rolling annual sum), one has to look quite far back in history to find these volumes. Considering detached houses and terraced houses, these levels were last sustained in early 2014 and before. After that, we lived in a zero-interest rate environment for a long time, and these figures were briefly reached around 2017/2018.

https://rt.fi/tietoa-alasta/tilastot-ja-suhdanteet/kuviopankki/asuntomarkkinat-kuvaajat/

Currently, there are very few drivers that would quickly turn the small-house market into strong growth, even though pent-up demand certainly exists beneath the surface. The consumer confidence indicator for 12/2024 was -8.6.

https://stat.fi/tilasto/kbar

https://stat.fi/julkaisu/cllxls7104csr0aw55xdhuqdo

Only 11 percent of consumers considered the time opportune for expensive purchases. Fewer people than before intended to buy a home or a car.

It is just as easy to draw a negative scenario alongside the positive one. I prefer to calmly observe how the market develops rather than flipping a coin. In addition to the number of housing starts, the peace in Ukraine and its effects on the availability and prices of labor and building materials have been written down as a major risk in my notes. In a bad scenario, construction costs could once again jump upwards, causing a prolonged ice age in the market if consumer purchasing power and confidence in their own finances do not keep pace. In a good scenario, rising building material prices could improve margins, and positive developments in consumer purchasing power and confidence could stimulate the markets. Who knows how this will turn out.

Edit. clarification to the text.

Here are Tomppa’s comments as EcoUp publishes its financial statement release on Thursday. ![]()

As EcoUp has shown good performance in recent quarters, we expect both revenue and EBITDA to have grown from the comparison period, even though the market situation has, in our assessment, remained very subdued. The company has excellent starting points for improving growth and profitability in 2025, which is why we expect guidance that indicates an improvement in both revenue and profitability.

The revenue forecast beat was slightly offset by a higher cost structure than we expected, and the bottom line was ultimately in line with expectations. Over the last three quarters, EcoUp’s development has been upward-trending, even though the market still appears to have been dormant.

Tommi interviewed CEO Matti Kaski right after H2. ![]()

Topics:

00:00 Start

00:16 H2 updates

02:50 Exports

03:28 Products

06:49 Acquisition

09:30 Market outlook

12:00 Improving operating margin

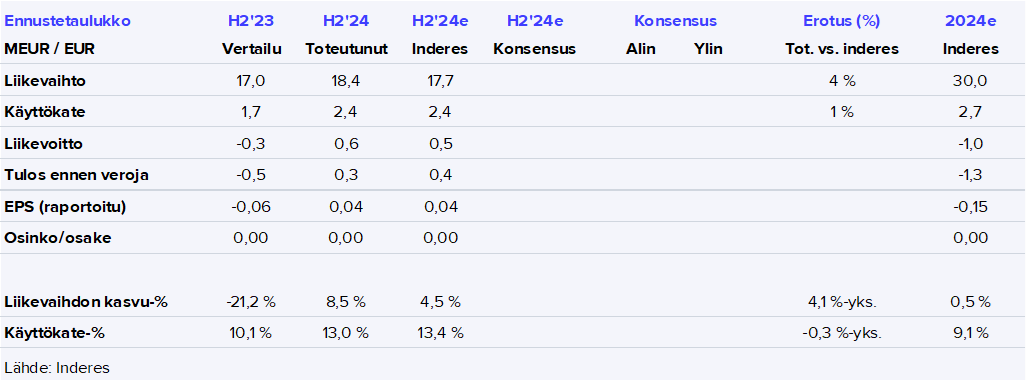

Tommi and Antti have prepared a new company report after H2. ![]()

EcoUp’s financial statement release confirmed our confidence in earnings growth and the Insulation Business’s competitiveness, as the company continued to grow in a challenging market. The main lines of the report and the guidance were in line with our expectations, so forecast changes remained minor. The earnings growth we forecast for the Insulation Business, despite the share price increase, still makes the return/risk ratio attractive according to our assessment, so we reiterate our Add recommendation for EcoUp and raise our target price to 2.60 euros (previously 2.00 euros).

Quoted from the report:

In the Technology Business, which is in the development phase, EcoUp made its first commercial product deliveries during the past financial year, but the revenue from these deliveries remained small according to our estimate. EcoUp’s target state in the Technology Business is to transition to deliveries of the company’s developed grinding line (Waste-X) by 2026, whereas the deliveries made during the past financial year were Cubeco elements produced on the line.

Tomppa and Antti are in a celebratory mood because the company will publish its Q1 business report next Tuesday. ![]()

We forecast revenue to have grown seasonally during a quiet period, which, combined with slight efficiency improvements, has also slightly strengthened profitability. Single-family housing construction shows clear signs of recovery as interest rates fall, although the likely slowdown in economic growth raises uncertainty. We expect the company to reiterate its guidance for strengthening revenue and EBITDA. On the results day, in addition to comments on the outlook, our attention will focus on the first steps of the Swedish business, which has been integrated into the EcoUp Group since the beginning of the year.

Antti and Tommi have published a new company report after the release of EcoUp’s Q1 report. ![]()

EcoUp’s Q1 report was mixed, with revenue growing stronger than our expectations, but profitability falling short of our forecast. Our earnings forecasts decreased, but we still expect clear earnings growth from EcoUp in the coming years, supported by the market. The earnings growth-driven return expectation, according to our estimate, barely reaches above our required rate of return. Due to negative forecast changes, we revise our target price to 2.5 euros and reiterate our Add recommendation.

Tommi and Antti have prepared a comprehensive report on EcoUp, which, like other comprehensive reports, is available for everyone to read. ![]()

We reiterate our ‘add’ recommendation for EcoUp and our target price of 2.5 euros. EcoUp consists of Insulation and Technology business segments, which operate in the construction value chain. In the short term, the market turnaround in small-house construction will accelerate the growth of the Insulation business, and in the long term, both business segments are supported by circular economy and sustainable construction trends. The profitability improvement in the coming years makes the return-risk ratio attractive for a year out, even though the stock is neutrally valued in the short term.

Quoted from the report:

We forecast EcoUp’s revenue to grow by approximately 3–8% p.a. in 2028–2032, with an emphasis on the Technology business. Our terminal growth forecast is at the long-term growth assumption level of Finland’s and Europe’s GDP, at 2.0%. Due to the very weak predictability of the Technology business, the uncertainty associated with long-term forecasts is high, as the share of the Technology business in the group’s revenue increases over time in our forecasts. Thus, even significant forecast changes are possible in the longer term, as visibility into the commercialization of technology and the expected growth rate begins to clarify during the strategy period ending in 2026.