EAB is the last of the investment service companies that doesn’t yet have its own thread, and I thought it was high time to open one for it where material related to the company can be collected.

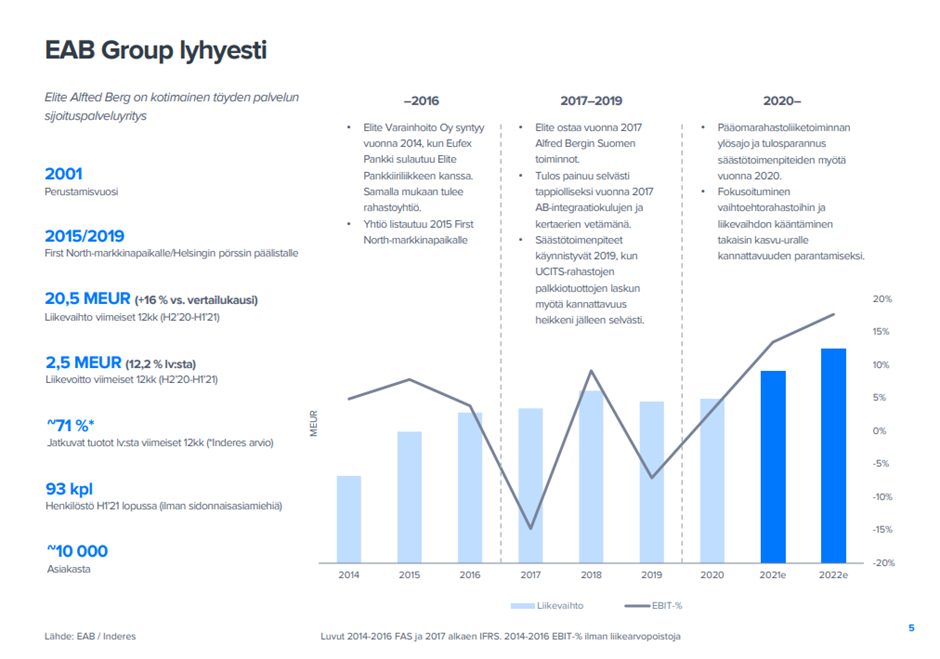

In terms of investor profile, EAB is a fairly classic turnaround company. The company’s financial development since its listing in 2015 has been very modest, and the company has had problems tapping into the industry’s very favorable trends. The key reasons, in my view, have been a lack of strategic focus, poor competitiveness of the product offering, and strategy implementation. When viewed through numbers, the company’s size relative to its wide range of services has simply been too small to conduct truly profitable business.

In 2020-2021, the company achieved a significant turnaround in its results. The key factors behind this turnaround are a more focused strategy than before and improved competitiveness of the product offering (prices have decreased and returns have improved). In addition, the very strong market has significantly facilitated this turnaround. With the turnaround in results, the company’s solvency has strengthened, and its room for maneuver in this regard has clearly improved.

In the short term, the most interesting thing about EAB, in my opinion, is this possible merger with Alexandria. I have already said before that Alexandria’s acquisition of a 9% stake has nothing to do with a financial investment, even though Alexandria strongly claims otherwise. My more detailed comments in this video: Alexandria: EAB ei ole finanssisijoitus - Inderes

I also find it interesting that EAB’s CEO said surprisingly directly that EAB would be an interesting target for someone else. In my opinion, this is an unusually direct reference to the fact that EAB is for sale/willing to be a party in arrangements. EAB Group H2’21: Historiansa paras tulos - Inderes

This is easy to understand, as EAB’s potential does not come out at that size, but the company should reach the next size class in one way or another. A merger with Alexandria would be a smart solution for this, at least on paper. We have outlined this scenario in EAB’s extensive report:

If one wants to continue this M&A speculation a little further, one clear “smoking gun” is the recruitment of the company’s CEO. The company announced almost a year ago that it would start looking for a new CEO, with the current one moving to operational tasks within the group (EAB:n toimitusjohtaja vaihtuu - Inderes).

Even though the CEO recruitment started from scratch, it normally does not take a year. Typically, a search started from scratch lasts ~3-6 months. Six months is already a very long time, especially in a smaller firm. At least I don’t remember a CEO recruitment lasting this long in my stock market career. It is, of course, possible that the company has had very bad luck, e.g., that a candidate has withdrawn at the last minute and the process had to be started from scratch. However, it is at least equally likely that the acquisition of Alexandria’s stake plays a role in this. Could it be possible that the recruitment is put on hold/shelved if the companies are in negotiations or if EAB would like to negotiate? The current CEO would be a natural person to conduct these, not a new CEO likely coming from outside the company.

So the acquisition speculations were indeed accurate, although the buyer was a different party than expected. EAB’s owners will continue their journey with Evli once the merger is finalized in the autumn.

As noted in this morning’s report, the arrangement is very favorable for EAB’s owners. EAB’s owners will receive a good compensation for their companies, plus an option for the appreciation of Evli’s share price. Evli is undeniably one of the long-term winners in the industry, whereas the same cannot be said for EAB.

This might have been the shortest thread in Inderes Forum history

They haven’t yet disclosed the detailed specifics of the arrangement, as the intention to merge has just been announced. The more detailed specifications will be available when the official agreement is signed later this spring. The amount does fall within the range you calculated.

Thanks, Sauli, for the answer and a follow-up question.

How does this potential EUR 3 million cash consideration benefit EAB shareholders in this case, Sauli? Will it still be in shares or in what form for the owners?

Quote:

Evli will issue EAB’s owners new B-series shares equivalent to 10% of Evli’s current share count, plus a cash consideration of EUR 3 million. Additionally, EAB may distribute an extra dividend of EUR 2.35 million before the merger.

Indeed, more detailed information has not yet been released, but at least to my understanding, the 3 MEUR will be paid in cash, meaning a little over 0.20 euros in cash per share will go to EAB shareholders in connection with the transaction. In other words, part of the purchase price will be paid to you, the owners, in cash.

In addition, EAB will distribute a dividend of 2.35 MEUR from its cash reserves, which is approximately 0.17 euros. This is equally comparable to a cash consideration. There was a clause in the announcement about this dividend stating that it would be distributed if the company had the means to do so (which, according to our calculations, it should).

So, in total, investors will receive approximately 0.22e + 0.17e, plus the previously discussed number of shares.

I tried to pose questions in my earlier messages that might concern a less professional investor.

This time, Sauli, I won’t thank you, but I’ll give you 3/3 stars for the service.

Now we’ll just wait for the official agreement.

Below is a summary of the merger from EAB’s perspective and a description of EAB.

Of course, a client base of 10,000 wealthy individuals is interesting.

EAB’s share price is at a reasonable level

Upon the completion of the arrangement, the value of EAB’s share capital is tied to the new Evli shares received as consideration (approximately 2.4 million units), a cash consideration of EUR 3 million, and an additional dividend of EUR 2.35 million to be paid before the merger. Thus, EAB’s market value at Evli’s current share price is approximately EUR 50 million, and the share value is EUR 3.6 per share. However, this does not take into account the risk associated with the completion of the arrangement, which we consider small, but which in any case has a moderately negative effect on the fair value of the company’s share. Conversely, it can be calculated that, based on the closing prices of the companies on Friday, the market estimates the probability of the arrangement failing to be approximately 4%, which we consider a reasonable assumption in terms of magnitude.

EAB in brief:

Elite Alfred Berg (EAB) is an investment services company founded in 2004 that offers its clients savings, investment, and wealth management services. The company’s private bankers and experts serve clients personally in 13 locations in Finland. EAB focuses particularly on the wealth management of wealthy private individuals, and the company has approximately 10,000 clients. At the core of EAB’s business is the management of clients’ wealth, which the company implements according to its wealth management models.

Sauli, how do you see it when EAB has branches or services in 13 locations? Is Evli going to utilize them to keep “service points” and thus improve its local service network across Finland? Doesn’t Evli currently only have an office in Helsinki, though things are handled online these days, but it just came to mind. It seems those 13 branches are pretty well spread across Finland right now.

Apologies for the delayed response; I completely missed this. So, Evli also has an office in Turku, and in addition, sales are supplemented by a team of a few agents (I understand mostly outside the Helsinki metropolitan area). But EAB’s nationwide office network and large number of agents are completely new to Evli, and I’m not sure how Evli intends to proceed with this. I would assume that the network will be maintained because EAB’s sales power relies precisely on it. But this is a big change in Evli’s way of operating, and this is one reason why I’m still quite puzzled by this merger from Evli’s perspective. Namely, without this merger, it would not occur to Evli to establish offices all over Finland.

Thanks for the answer, Sauli. Evli’s report today still mentioned that progress will be made on the matter during May, so we shouldn’t have to wait long for more thoughts on the situation.

Of course, there’s a lot of good here, but also certainly a lot of harmonization needed in corporate cultures and operations.

Evli’s strategy/goals mention: leading Nordic asset manager

EAB’s strategy/goals mention: The most respected asset management expert in the Nordics.

Last week’s developments:

After several weeks of decline, stock prices on several major markets turned to a clear rise last week. The largest increase in euro terms was seen in the United States (+5%), but also in Europe (+3.13%) and Finland (+3.26%) the increase was significant. In Asia (-1.23%), emerging markets (-0.52%) and Japan (-0.12%), on the other hand, prices were on a downward trend, but despite this, global stock markets (MSCI World AC) rose by 3.55% at the end of the week.

Upon completion, EAB shareholders will receive 0.172725 new Evli Series B shares for each EAB share they own as merger consideration, and a total cash consideration of three (3) million euros, which will be distributed equally among the outstanding EAB shares on the trading day preceding the effective date of the Merger. Based on current share counts, the cash consideration would be 0.217196 euros per share (“Merger Consideration”). EAB shareholders would then own approximately 9 percent of the shares and one (1) percent of the votes of the Combined Company, and Evli shareholders approximately 91 percent of the shares and 99 percent of the votes. The merger consideration shares will be applied for listing on the official list of Nasdaq Helsinki Oy (“Helsinki Stock Exchange”) in connection with the Merger.

The completion of the merger (“Completion”) is expected to take place in the latter half of 2022, provided, among other things, that Evli has received approval from the Financial Supervisory Authority for the change of ownership. According to the merger plan, the Completion would occur approximately on October 1, 2022.

Evli and EAB announced on Tuesday, May 31, 2022, that they had signed a merger agreement, according to which EAB will merge into Evli. There is no longer much uncertainty regarding the completion of the arrangement, so with the merger, the return on EAB’s share will in the future be determined by Evli’s share.