New thread about Dovre Group, I couldn’t find an existing one.

Due to the oil collapse, Dovre was already quite deep in the mud, as its businesses were too reliant on oil companies. Revenue and profit fell catastrophically, and the merger with Norwegian NPC didn’t go smoothly either.

The stock was long burdened by the long-term share sales of the Norwegian major owners who came with NPC.

Now, later, the Norwegians have sold their ownership as a block trade to numerous domestic investors, including Kari Kakkonen, Erkki Etola, and Ilari Koskelo, who has long served on Dovre’s board.

Businesses have been “diversified”

Revenue has started to rise again, and operating profit is also growing now for the fourth or even fifth consecutive quarter.

The latest acquisition is Tech4Hire As, and a lot seems to be happening behind the scenes. Time will tell if this bears fruit and if more acquisitions are coming. Dovre is a debt-free company.

A one-cent dividend will be distributed in the spring.

OUTLOOK FOR 2020:

In 2020, revenue and operating profit are estimated to improve from 2019, excluding non-recurring items.

Great that you opened a thread for this company! In my opinion, the company is headed in the right direction and the risk/reward ratio is relatively attractive. I myself jumped in at around €0.29. What has been weighing down the share price in recent days? Could it be the latest share issue?

I hope you sold your shares with a good profit, because now it’s already below your purchase price.

Undeniably, this decline has gone overboard, it seems to be one of the biggest losers in these corona panics.

Originally, the stock likely fell due to disappointment over the dividend amount.

In itself, this decline is not justified because Dovre’s main markets are in Norway, and at least not yet, Corona is not humbling the Nordic countries.

Good buying opportunities are likely to be served today.

So Kakkonen didn’t dare touch Dovre anymore.

Well, I, for my part, have been buying this almost every day from panic sales. Will it turn out well for me in the end, badly, or very badly?

I guess tomorrow’s result will be OK, just like in the last quarters.

Those looking for quick profits are probably already eager to sell their shares tomorrow, as there has been such a steady rise with low trading volume.

Perhaps tomorrow we’ll also hear something nice about the dividend.

Edit: I had somehow confused the days, Q3 will apparently be published next week, not today.

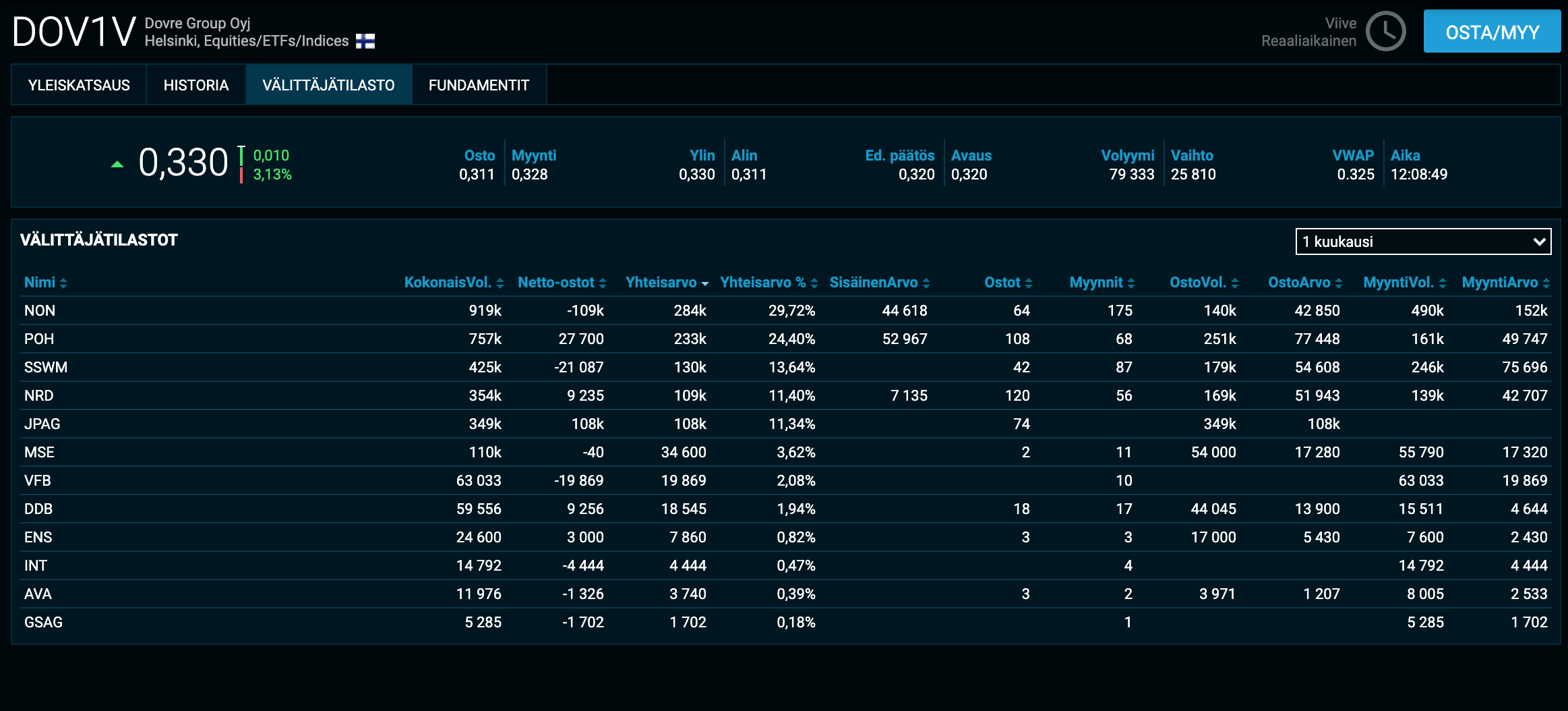

JPAG has been buying for some time now. Below are the monthly statistics.

I also have some Dovre, even though I’ve lightened my position. I originally went into this with the thought that when the stock cooled down from the K2 pump and buying continued, there was a little upside available. If the media picks up how Kyösti is buying again, there could be a small surge of interest in Dovre. Otherwise, Dovre has done quite well this year, and it will be interesting to see what the earnings report looks like.

Today, after the stock exchange had already closed, positive news was released.

The Board of Directors of Dovre Group Plc has today decided, based on the authorization given to it by the Annual General Meeting 2020, to distribute a dividend of 0.01 euros per share. The dividend will be paid to shareholders who are registered in the company’s shareholder register maintained by Euroclear Finland Oy on the dividend record date of November 2, 2020. The dividend will be paid on November 10, 2020.

Based on Dovre’s dividend decision, I believe the board now has some confidence in the future development of the business. Dividends would hardly be distributed if the short-term outlook were very weak. Of course, the project-based nature always brings its own uncertainty to the predictability of operations.

From Dovre’s perspective, the Norwegian government’s decision on tax changes concerning oil companies may have provided some support. Companies have been encouraged to make investments after the oil price collapse.

After the tax decisions in August, Statistics Norway (SSB) estimated that oil and gas investments in Norway will decrease less in 2021 than previously predicted.

Fitch estimated at the beginning of September that the decision benefits, among others, Aker BP, and the tax reliefs support the financial stability of service companies operating in oil fields.

On the other hand, tax reliefs only alleviate the situation, and competition remains fierce in Norway. Intense competition was already highlighted in the CEO’s review in the 2019 annual report, which stated: “Competition is extremely tight in our main market area, Norway.”

A rather expected “boring” result, meaning nothing revolutionary.

Revenue decreased, which was apparently anticipated.

Profit was 0.6 million (1.5 million), but in the comparison period, the sale of an office property increased sales profit by 0.8 million, so without this, the profit ended up being roughly the same.

Outlook remains largely unchanged.

I would perhaps start exploring the development and growth of Dovre’s business through acquisitions.

Speaking of websites, theirs could use a bit of an update, so if any web designer happens to be reading this, wink wink Nothing else to do but sell your skills there

Edit: Is something really going on there? The job openings and last week’s announcement about management transactions (Acquisition; Koskelo Ilari, Volume: 50,000 Average price: 0.27 EUR) might raise some suspicions.

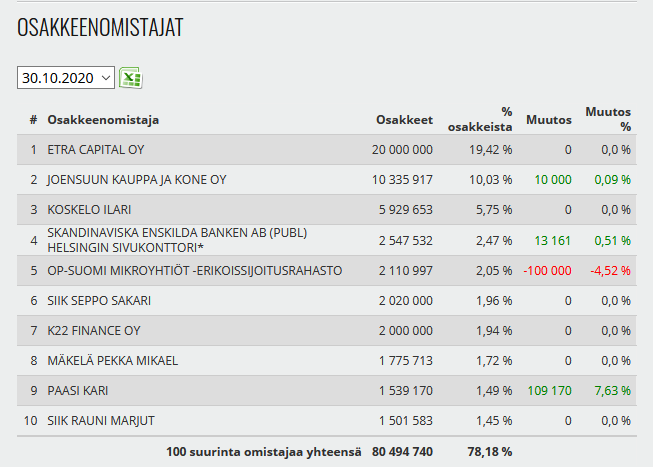

I’ve been wondering why Etola (Etra Group) owns nearly 20% of the company’s shares. An industrial investor, a software company investor, but a consulting company? Does anyone who has studied the company more closely know what the company’s most profitable part is?

Last year’s Tech4Hire acquisition. The company employs a large number of technology, IT, and project management consultants, mainly in oil and gas industry projects.

Thanks @Cadel, good point. I sold my Dovre shares around the Q3 report, which was a bit soft for my taste. Now I’ve mainly been following from the sidelines, but with this information, I decided to become an owner again, albeit with a small weighting. I did notice Ilari’s purchases but not the job openings.

There’s still a bit too much selling pressure for my taste, but then again, this and Ilari’s purchases give me confidence. Hopefully, K2 will free up some Revenio money for Dovre as well.

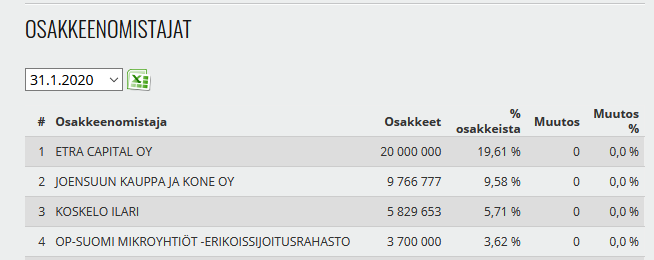

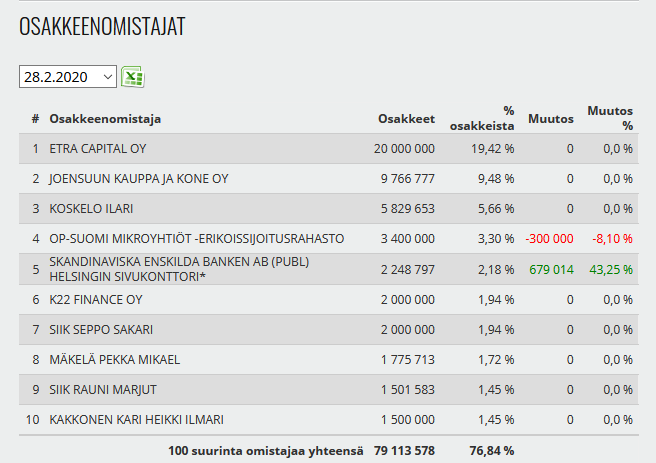

OP’s special investment fund has been heavily on the selling side. In January, it still had 3.7M shares, after which it has sold 90,000 - 415,000 shares per month. Mainly it has been -100,000 shares/month.

Since June, Joensuun kauppa ja kone oy has been buying more shares every month, 10,000 - 214,000 shares/month. Ilari’s purchases have been more sporadic throughout the year.

Skandinaviska Enskilda Banken has been buying and selling shares throughout the year. The biggest purchase was in February. After that, there have been small sales and purchases…