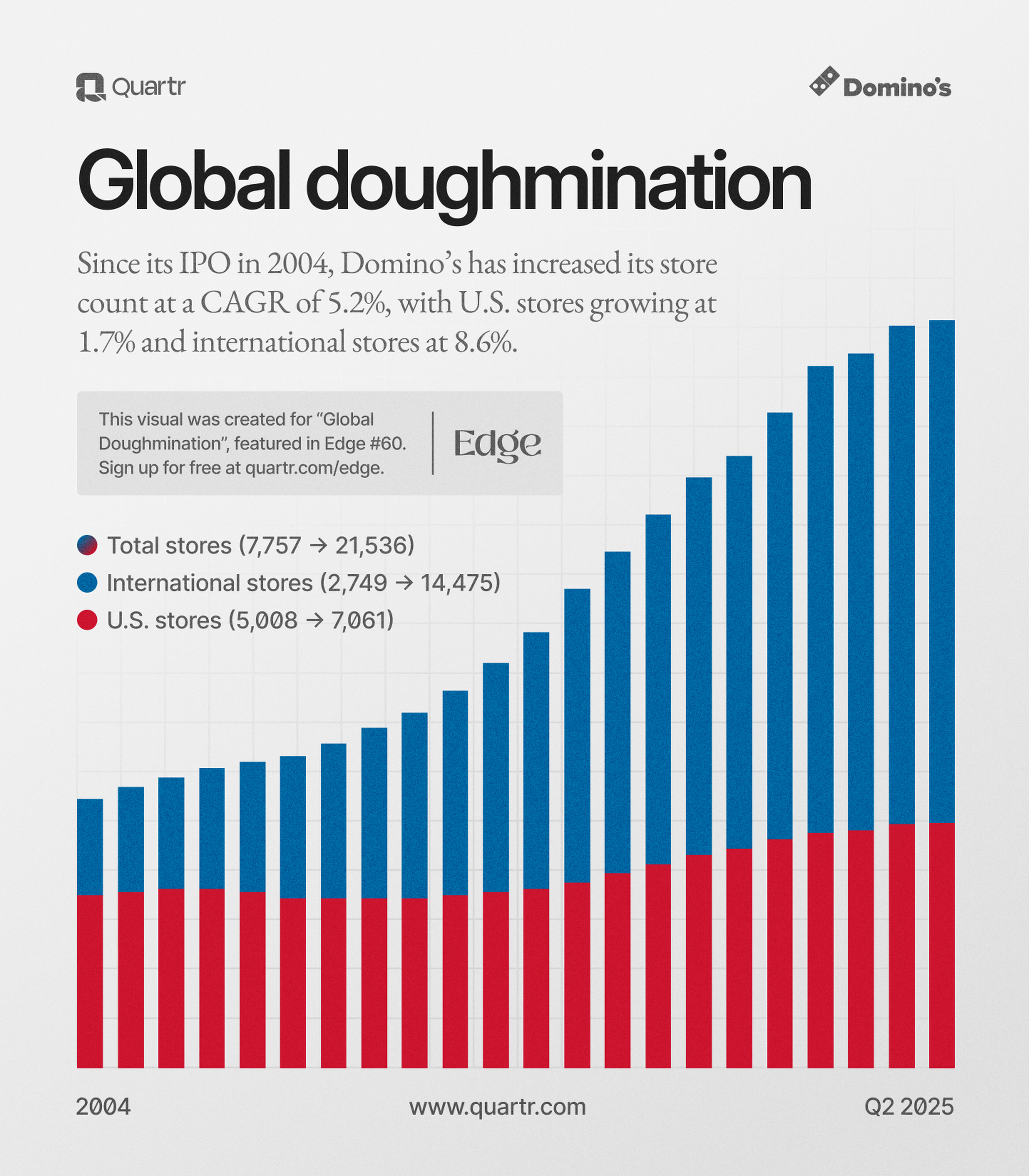

Domino’s Pizza on vuonna 1960 perustettu yhdysvaltalainen ravintolaketju, joka tunnetaan erityisesti pizzan kotiinkuljetuksesta. Yritys on kasvanut pienestä Michiganissa sijaitsevasta pizzeriasta globaaliksi toimijaksi, jolla on yli 20 000 toimipistettä ympäri maailmaa. Domino’s toimii yli 90 maassa ja on yksi maailman suurimmista pizzaketjuista.

Viime vuosina yhtiö on panostanut vahvasti digitaalisiin palveluihin ja nykyään valtaosa tilauksista tehdään verkkosivujen tai mobiilisovellusten kautta. Tämä teknologinen etumatka on ollut yksi tärkeimmistä tekijöistä yhtiön kasvussa, lisäksi Domino’s on tunnettu innovaatioistaan myös logistiikan ja tuotannon saralla, mikä on tehnyt siitä yhden alansa tehokkaimmista toimijoista.

Domino’s Pizzan osake on koettu hieman yliarvostetuksi nykyisellä hinnalla, vaikka yritys on kasvanut ja sen “Hungry for More” -strategia tuo uutuustuotteita ja avaa uusia liikkeitä… niin sijoittajat saattavat olla jo hinnoitelleet yrityksen täyden potentiaalin. Koetaan, että osakkeen arvo voisi siis olla nykyistä paljon alhaisempi…

Vaikka Domino’s on vahvasti mukana pikaravintolabisneksessä ja kuluttajien odotetaan lisäävän kulutustaan, yhtiön tuloskehitys on ollut kaikesta huolimatta vain keskinkertaista verrattuna kilpailijoihin. Tulosennusteet viittaavat kuitenkin 20 prosentin kasvuun tulevina vuosina, mikä voisi nostaa osakkeen arvoa (toivotaan, toivotaan?". Silti, monista nykyinen hinta ei tarjoa houkuttelevaa ostopaikkaa… ja jotkut saattavat hakea sitä myyntipaikkaa.

Domino’s Pizza oli haasteita kannattavuudessa, vaikka sillä menee vahvasti verkkotilausten ja oman logistiikan saralla. Yhtiö laajentaa aggressiivisesti kehittyville markkinoille, mutta kilpailu kiristyy vastaavasti ja toimitusketjuongelmat sekä nousevat kustannukset painavat tulosta. Toisaalta samaan aikaan Warren Buffett on kasvattanut omistustaan yhtiössä.

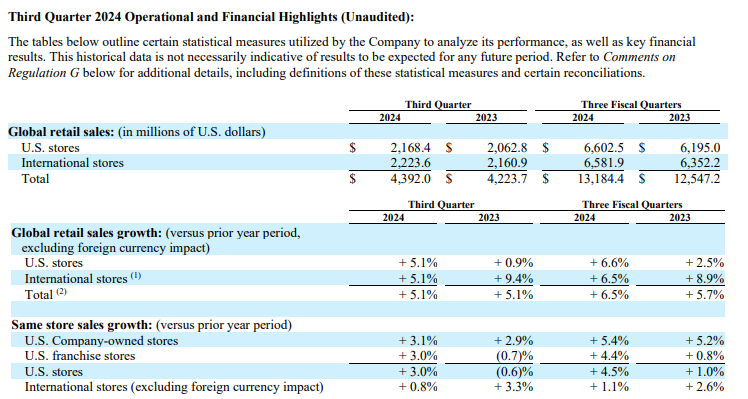

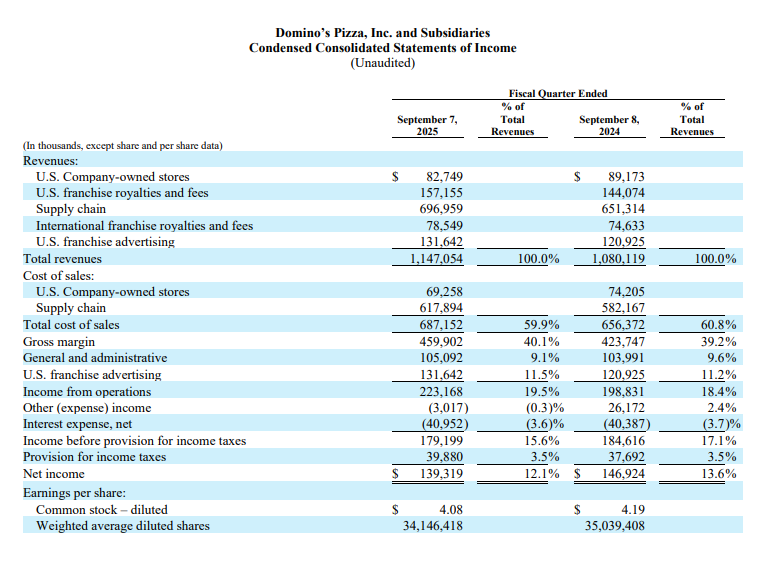

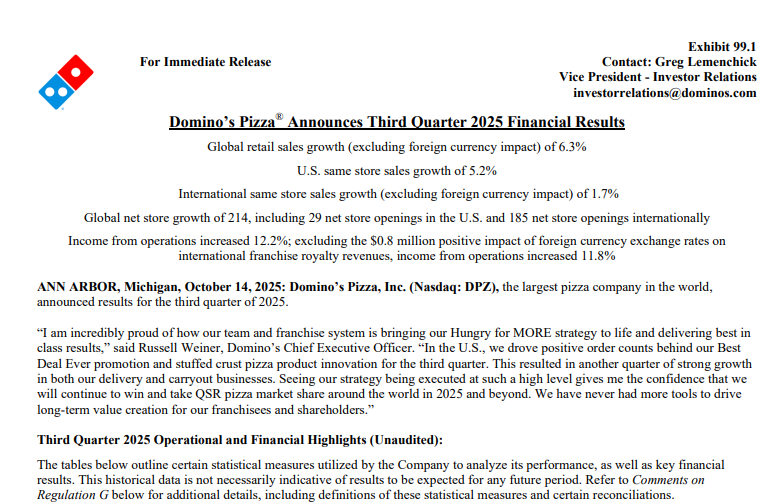

Domino’s Pizza ylitti tulosennusteet EPSis, mutta jäi hieman liikevaihtoennusteista ensimmäisel kvartaalil.

Yhtiön kansainvälinen myynti kasvoi odotettua paremmin, kun taas Yhdysvaltojen vertailukelpoinen myynti laski hieman. Globaali myynnin kasvu ilman valuuttakurssimuutoksia oli positiivista, erityisesti kansainvälisillä markkinoilla. Yhtiön tulos ja vapaa kassavirta paranivat merkittävästi edellisvuodesta.

Domino’s jatkaa strategista panostustaan kasvamiseen, vaikka taloudelliset haasteet ja epävarmuus Yhdysvalloissa vaikuttavatkin kuluttajien käyttäytymiseen. Yhtiö ilmoitti myös osingosta ja osakkeiden takaisinostoista.

Domino’s Pizzan tulos jäi hieman viime vuodesta, mutta liikevaihto ja myynnin kasvu olivat vahvoja.

Yhtiön kotimaaassa, eli Yhdysvalloissa sekä kotiinkuljetus että nouto vetivät hyvin, tämän lisäksi kansainvälistä kasvua nähtiin haasteista huolimatta.

Yhtiö luottaa vahvaan asemaansa ja näkee paljon mahdollisuuksia jatkossa, mutta ei nyt mitään erityisen vahvoja perusteluja tälle antanut.

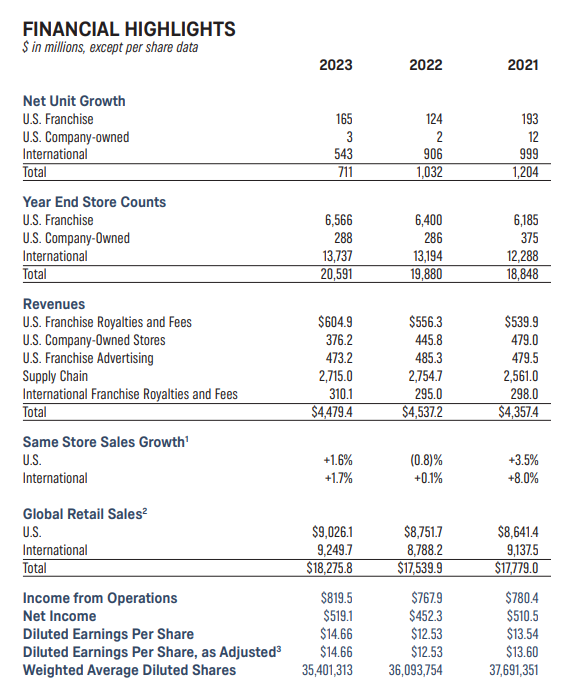

Tviitissä ollaan sitä mieltä, että Domino’s näyttää pärjäävän hienosti vaikeassa markkinassa sekä liikevaihto että käyttökatteet ovat kasvaneet tasaisesti, erityisesti Yhdysvalloissa, kuten edellisessäkin viestissä on todettu.

Aika hyvin kulkee pizzabisnes, vaikka kuluttajilla on tiukkaa tai osin ehkä siksi, kun on ehkä halvempi vaihtoehto perusravintolaruoalle - tosin ei se kaikilla roskaruokatoimijoilla ole näin mennyt. En tiedä.

Dominosista enemmän kiinnostuneille suosittelen lämpimästi tätä massiivista Quartrin blogia yhtiöstä.

Kuten monelle pitkäikäiselle firmalle on tupannut käymään, Dominos on uusiutunut monta kertaa matkan varrella. Yhtiö meinasi liian kovalla kasvulla ajaa itsensä ojaan 1970-luvulla. 2000-luvun alkuun mennessä taas pizza alkoi maistumaan pahville. Siitä alkoi ryhtiliike, mistä Dominos nykyään tunnetaan: tasalaatuinen, ei halvin mutta edullinen, tehokas ja nopea pizzatoimittaja.

Yhtiö on laadukas, enemmän mietityttää pitkän aikavälin kasvuvara joskin esim. Intiassa luulisi latua riittävän. Ja pieniä Dominos-putkia mahtuu pienillekin paikkakunnille.

Dominosin Master franchise-yrittäjiä löytyy myös muutamia listattuna. Enterprises näyttää jonkinlaiselta liikalaajentumisen fiaskolta Aasiassa, mutta Dominos Pizza Group Iso-Britannissa näyttää hyvin johdetulta. Se treidaa nyt joku P/E 10x ja olen ostellut vähän osakkeita viime aikoina. Täytyy katsoa jos siitäkin ehtisi avata oman ketjun.

Alla on juttu, miten Domino’s uudistaa brändinsä ensimmäistä kertaa 13 vuoteen. Uusi ilme tuo kirkkaammat värit, uuden oman “Domino’s Sans” -fontin ja rohkeamman logon, jotka näkyvät esimerkiksi pizzalaatikoissa ja myöhemmin myös henkilökunnan asuissa sekä sovelluksissa.

Mukana tulee myös uusi tunnussävel “Dommmino’s”, jonka esittää Shaboozey. Uudistuksella haetaan kuulemma raikkaampaa fiilistä ja lisää asiakkaita kilpailulla ravintola-alalla.

Tämä ei ole @Verneri_Pulkkinen:n pirkkapitseria ky, vaan tämä on se kunnon Domino´s Pizzan ketju.

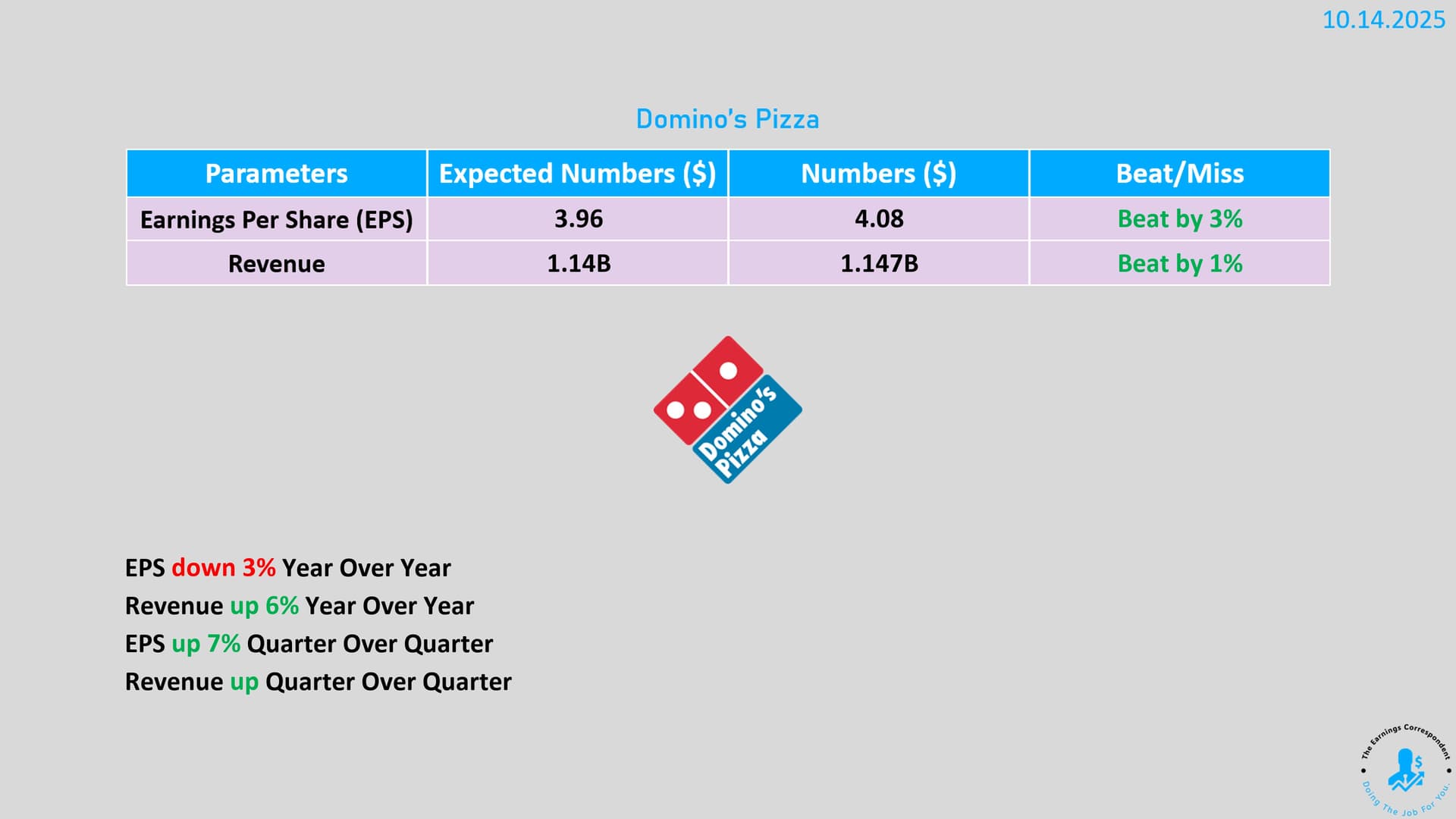

Domino’s veti kovan kvartaalin esim. jenkkimyynti lähti kunnolla lentoon ja “Hungry for More” -strategia näyttää purevan. Täytetty reunapizza ja halpakampanjat toivat uusia asiakkaita ja markkinaosuutta napattiin kilpailijoilta reippaasti.

Tulos jäi otsikoissa laimeammaksi

kertarerän

Net income decreased $7.6 million, or 5.2%, in the third quarter of 2025 as compared to the third quarter of 2024, primarily due to an unfavorable change of $29.2 million in the pre-tax unrealized losses and gains associated with the Company’s investment in DPC Dash Ltd. To a lesser extent, an increase in the provision for income taxes also contributed to the decrease in net income. The effective tax rate increased to 22.3% in the third quarter of 2025 as compared to 20.4% in the third quarter of 2024 resulting in an increase in the provision for income taxes of $2.2 million. These decreases were partially offset by higher income from operations as discussed above

takia, mutta perusbisnes kulkee hienosti. Sekä nouto että kotiinkuljetus vetivät hyvin, vaikka ulkomailla kasvu oli vielä vaisua. Porukka odottaa nyt, päivittääkö firma pian näkymänsä ylöspäin.

Domino’s Pizza Enterprises kiisti väitteet, että Bain Capital suunnittelisi yhtiön ostoa, vaikka näin on huhuiltu eikä mitään ehdotusta ole ainakaan saatu.

Suurin omistaja Jack Cowin yrittää viedä läpi “projektia”, jonka tavoitteena on selkeyttää hinnoittelua ja vähentää kuponkiriippuvuutta tarjoamalla edullisempia ja läpinäkyvämpiä hintoja.

Jonnet ei muista mutta parikyt vuotta sijoteltiin UNIQUE PIZZAAN, sen ajan kuumin meemilappu.

Näyttää vaihtaneen nimeä ja tickeriä puolentusinaa kertaa, nimihistoria tällainen:

GBH Liberia, Inc. → Coastal Services Group, Inc. → Unique Pizza & Subs Corp → Unique Foods Corp → Gourmet Provisions International Corp → Unique Global Innovative Solutions Corp.

Nykyisessä tyttäret Jose Madrid Salsa, PopsyCakes, Unique Tap House ja Pizza Fusion.

Uniquen lappu OTC:lla ja nykyään $0.0001 taalaa, mutta kävi miljardeissa.

Oi oisitpa Alokas tuolloin vinkannut Dominosta ois onni käynyt toisin!