Avataas ketju tästäkin. Monet jenkkien retailerit ovat ottaneet kovasti osumaa samalla kun teknot ovat rallatelleet kohti uusia huippuja. Designer Brands (tikkeri DBI) ei ole poikkeus ja kurssi alkaa olla lähellä finanssikriisin aikaisia pohjia. 2020 maaliskuun pohjiin on vielä reilut 50% matkaa alemmas, mutta sinnekin saatetaan päästä taantuman avustuksella.

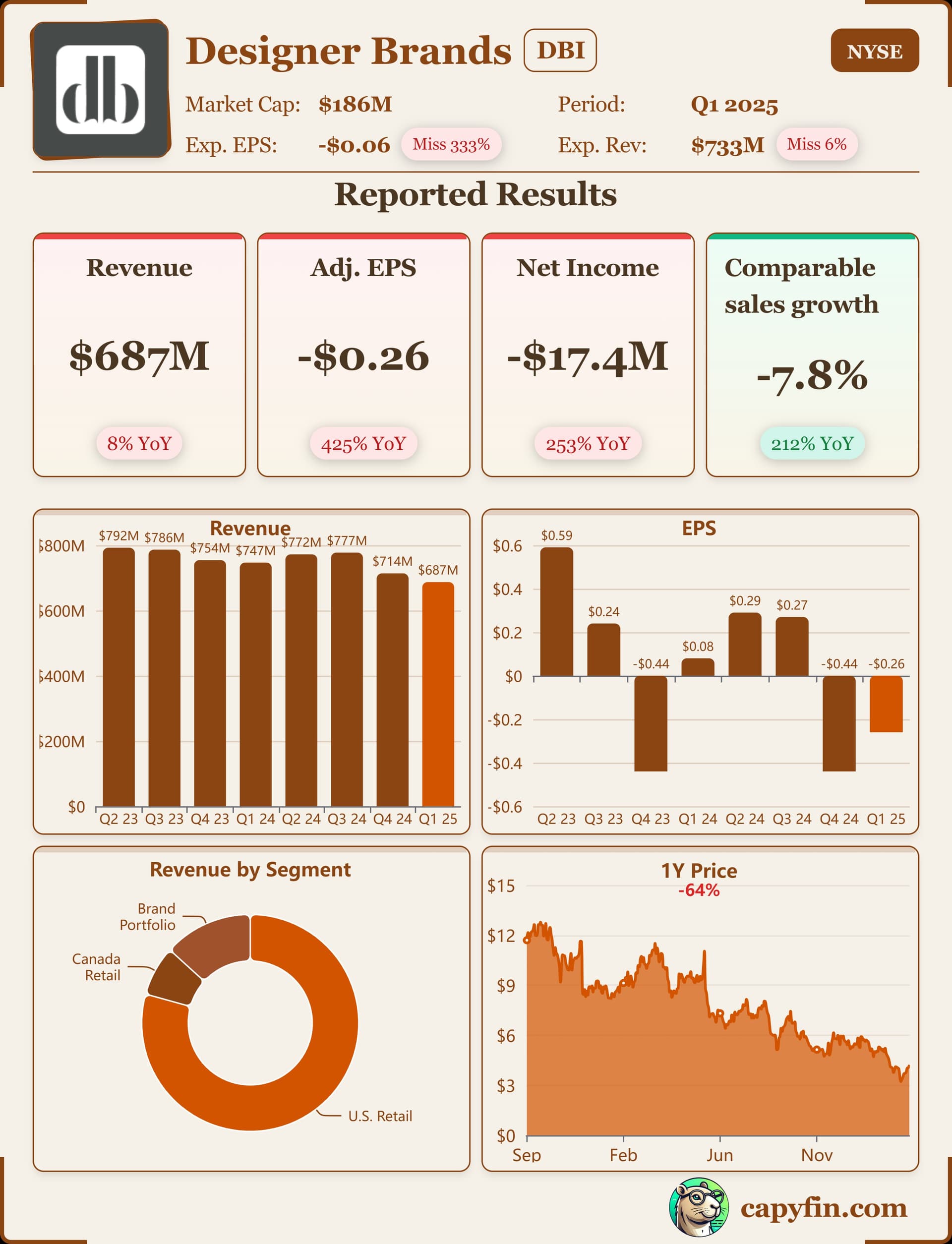

Markkina-arvo noin 430 miljoonaa $ ja P/E noin 3.

Yhtiön kuvaus itsestään:

“Designer Brands is one of the world’s largest designers, producers and retailers of the most recognizable footwear brands and accessories, transforming and defining the footwear industry by inspiring self-expression across every facet of its enterprise. Through its portfolio of world-class owned brands, led by the industry-setting Vince Camuto brand, Designer Brands delivers on-trend footwear and accessories through its robust direct-to-consumer omni-channel infrastructure, featuring a billion-dollar digital commerce business and nearly 650 stores across the U.S. and Canada. Its retailing operations under the DSW Designer Shoe Warehouse and The Shoe Company banners deliver current, in-line footwear and accessories from most of the largest national brands in the industry and hold leading market share positions in key product categories across Women’s, Men’s and Kid’s in the U.S. and Canada. Designer Brands also distributes its owned brands through select wholesale relationships while leveraging its design and sourcing expertise to build private label product for national retailers. Designer Brands is also committed to being a difference maker in the world, taking steps forward to advance diversity, equity, and inclusion in the footwear industry and supporting our global community and the health of our planet through donating more than six million pairs of shoes to the global non-profit Soles4Souls.”

FY 2022 olennaisimmat:

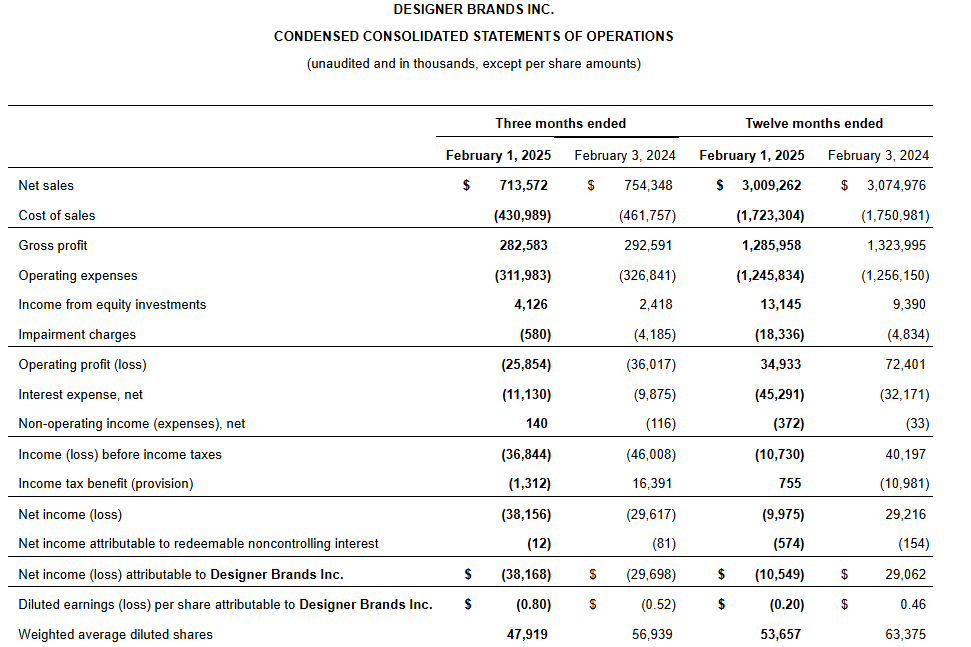

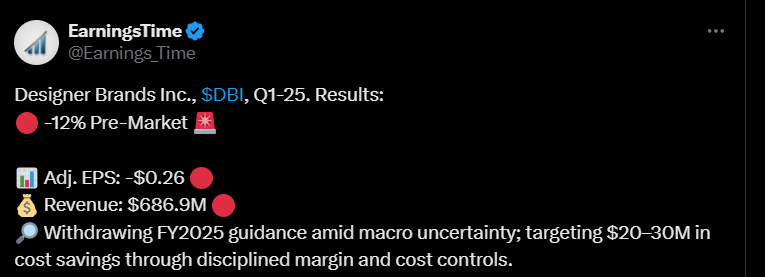

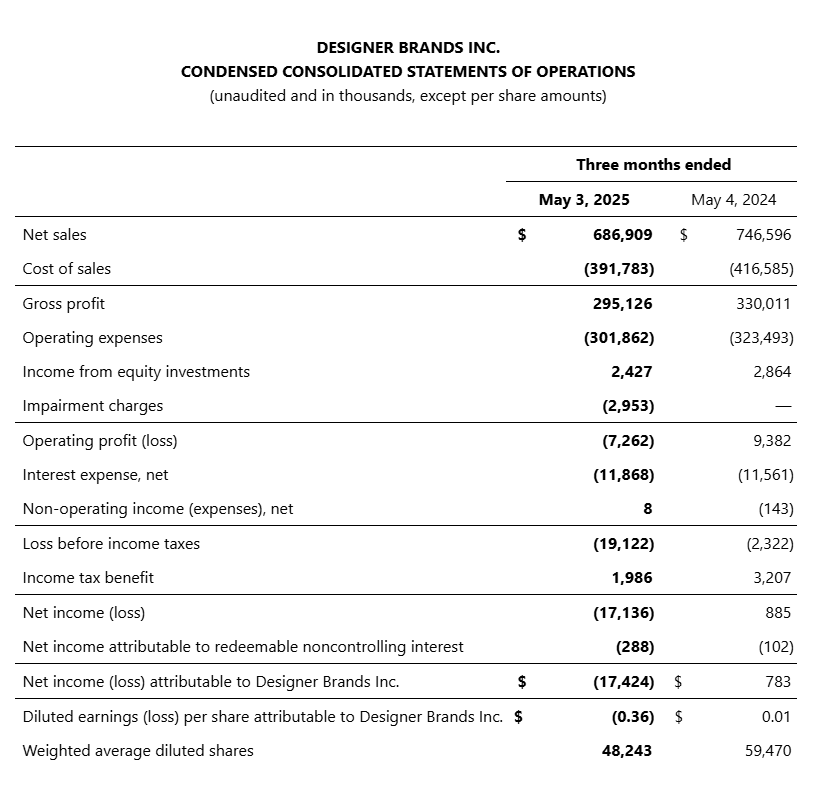

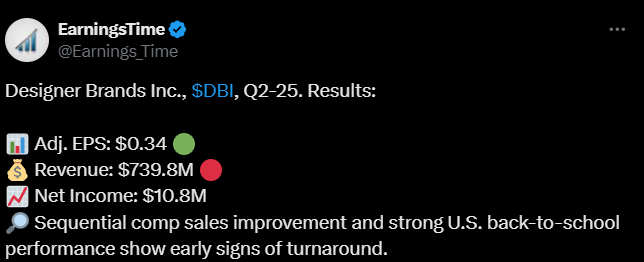

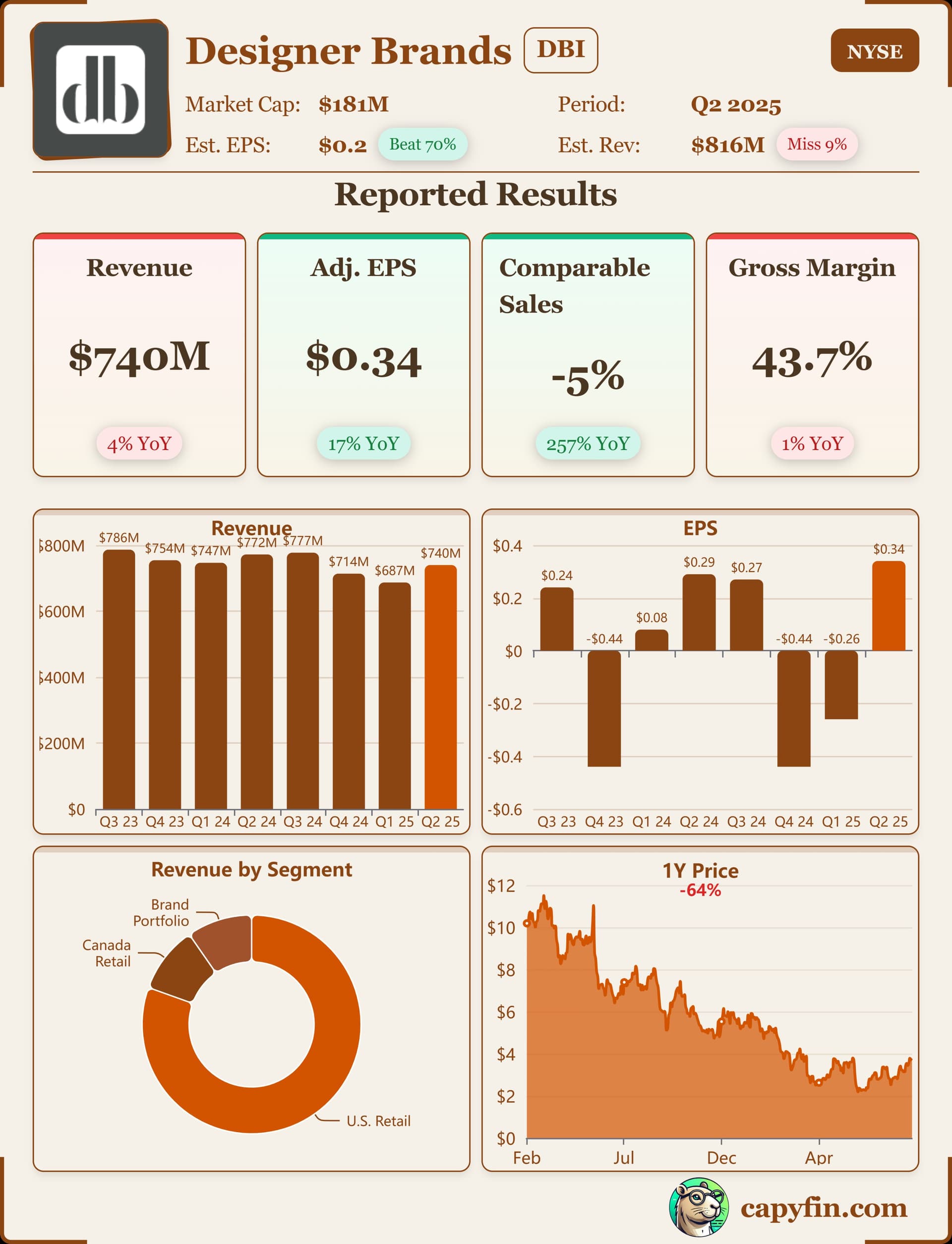

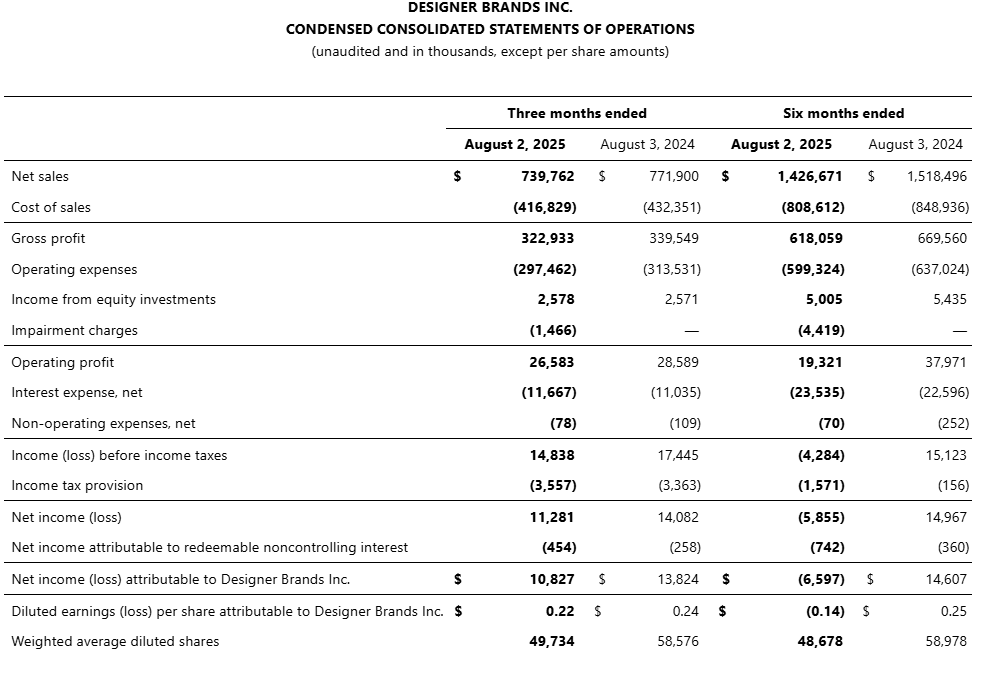

- Net sales increased 3.7% to $3.3 billion.

- Comparable sales increased by 4.4%.

- Gross profit was flat to last year at $1.1 billion, and gross margin was 32.6% as compared to 33.4% last year.

- Reported net income attributable to Designer Brands Inc. was $162.7 million, or diluted EPS of $2.26, including net benefits of $0.41 per diluted share from adjusted items, primarily related to the change in valuation allowance on deferred tax assets, partially offset by the loss on extinguishment of debt and write-off of debt issuance costs, restructuring and termination costs, CEO transition costs, and impairment charges.

- Adjusted net income was $133.7 million, or adjusted diluted EPS of $1.85.

Likviditeettikin siedettävällä tasolla:

- Cash and cash equivalents totaled $58.8 million at the end of 2022, compared to $72.7 million at the end of 2021, with $243.9 million available for borrowings under our senior secured asset-based revolving credit facility (“ABL Revolver”). Debt totaled $281.0 million at the end of 2022 compared to $225.5 million at the end of 2021.

- The Company ended the year with inventories of $605.7 million compared to $586.4 million at the end of 2021.

Omien osakkeiden ostot käynnissä ja lisäksi pientä osinkoakin irtoaa, ainakin toistaiseksi.

For the year ended January 28, 2023, we repurchased 10.7 million Class A common shares (14.6% of Class A and Class B common shares at the beginning of the fiscal year) at an aggregate cost of $147.5 million, with $187.4 million of Class A common shares that remain authorized under the program as of January 28, 2023.

• A dividend of $0.05 per share of Class A and Class B common shares will be paid on April 14, 2023 to shareholders of record at the close of business on March 31, 2023.

Ohjeistus herättää toivoa:

The Company has announced the following guidance for the full year 2023:

Net Sales:

Designer Brands net sales growth, excluding Keds: Down mid-single digits

Incremental net sales from Keds acquisition: $75.0 million to $85.0 million

Diluted EPS: Designer Brands, excluding Keds: $1.65 - $1.75

Contribution from Keds acquisition ~$0.00.

Yhtiön brändeihin kuuluu mm. monille tuttu Reebok:

En ole vielä ostanut positiota tähän lafkaan, kun on niin tappavassa laskutrendissä, mutta jossain vaiheessa uskon markkinan kääntyvän taas suotuisammaksi DBI:n osalta. Tällöin odotan, että yhtiön markkina-arvo saattaisi vähintään kolminkertaistua nykyisestä. Myös yhtiön verrokit voivat tarjota mielenkiintoisia tilaisuuksia.