The market’s disappointment with the latest interim report has still been on my mind. The reaction was really harsh, and the trend has been heading southeast even after that. I don’t dare to be quite as pessimistic about the company’s direction as the market is. Personally, I expect growth from a growth company, and there was plenty of that in the last report, even though profitability took a hit. Whether the decline in profitability remains temporary remains to be seen.

Admittedly, the biggest threat is tightening competition, as there is no real moat. Growing, drying, and bagging mangoes is, in itself, a relatively low-barrier business with no massive entry barrier. It’s unlikely that any great trade secrets can be hidden in the business that competitors couldn’t replicate.

Now during the summer, in particular, I’ve been traveling around different parts of the country and observing store layouts. I’ve seen Dellia products prominently displayed in the produce section aisles at least in Halpa-Halli and Citymarket stores, where the bags are surely easy to grab. I haven’t seen similar displays in S-markets; there, Dellia products were among other dried fruits. In terms of growth, this store placement is a good thing because I would argue that people don’t necessarily think to look for dried fruits for snacking or treats from the specific shelf designated for them. We’ll have to wait for information on how much this fun costs and eats into profitability. To my delight—or disappointment—it has happened at least twice that Dellia mangoes were sold out in the store, and I couldn’t get them for my car trip. Otherwise, the goods seem to move quite well even from the dried fruit shelf in a “rural village” like this that titles itself a city.

In my opinion, the product is very good, and I have replaced other treats with Dellia products myself. I can’t buy these as a snack, because I’m forced to eat the whole bag at once, which results in quite a lot of sugar. People are so conscious nowadays that many probably don’t consider this a health product by any means. But many could well replace unhealthier treats with, for example, dried fruit, which can shift demand to the product category, in addition to store visibility creating a completely new market.

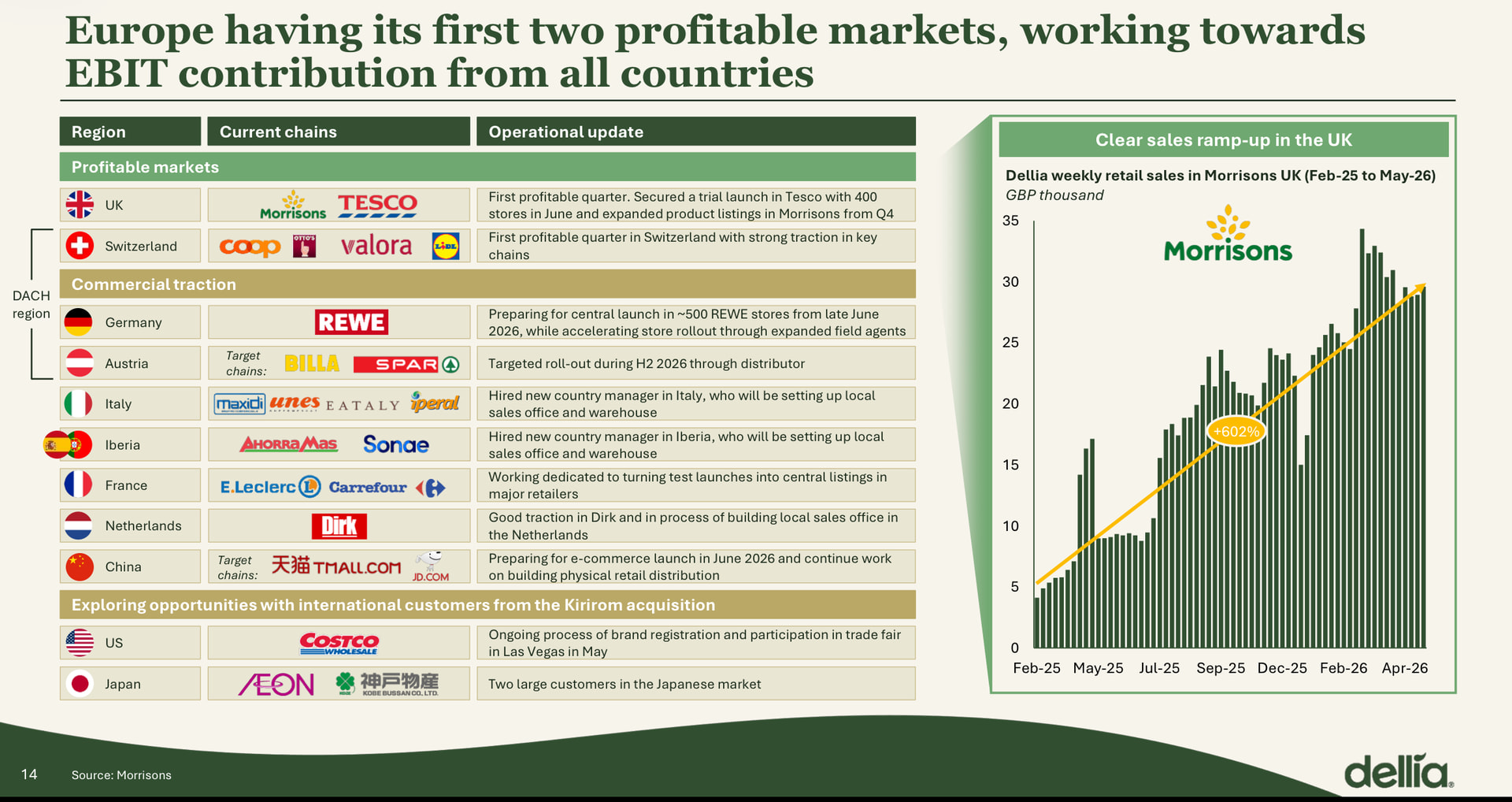

Because the product is genuinely good and there is still market to conquer, I believe there will be more growth, but tightening competition is the most worrying factor. However, the last report had good announcements regarding, among other things, the Tesco collaboration and expansion into the UK through that. The path is also being cleared in other populous European countries. There are many opportunities, and that’s why aggressive shelf wars in a few Nordic countries don’t worry me that much yet. However, the position was opened lamentably early with a small weight and perhaps a bit of FOMO, but every dip is an opportunity. In my opinion, it is still too early to declare the game lost for a growth company like this based on a single quarter.