I am no expert in mango cultivation, but I happened to be brainstorming with an AI yesterday about the risks associated with farming in Cambodia. El Niño events stood out in Kirirom’s history as occurrences that, every 3–4 years, have significantly destroyed harvests and complicated local life.

Can someone who has followed the company longer comment on how significant this risk is, and has the company mentioned how effectively they can mitigate it?

This risk was explained well in the IPO papers, although the situation has changed somewhat since the company acquired its own mango factory with plantations (own + contract farms), which at least makes the risks easier to manage.

Previously, the company had to scramble to secure a sufficient quantity of mangoes from the season’s harvest to last the entire year until the next crop. Additionally, they had to hope that the Kirirom factory had enough spare capacity. If the harvest turned out to be poor, mango prices spiked, and they might not even get enough supply → empty shelves.

If, on the other hand, the harvest was good and mangoes flooded the market driving prices down, they couldn’t necessarily take full advantage of the situation because manufacturing capacity wasn’t fully in their own hands.

The fierce growth rate certainly added its own flavor, making demand forecasting far from easy.

The mango harvest will continue to vary wildly between seasons, but in my opinion, the company is now better positioned to exploit this volatility thanks to its own factory and its own/contract plantations.

The “best before” date of the finished product is likely over a year away, so during good harvest seasons, they can better capitalize on low raw material prices by hoarding as many mangoes as possible.

Correspondingly, during poor seasons, they can better protect the production of their own brand and, if necessary, cut back on contract manufacturing.

In some years, of course, a drought or floods will surely ruin the harvest catastrophically despite this, but that hardly shows up in a DCF model when considering the long-term case

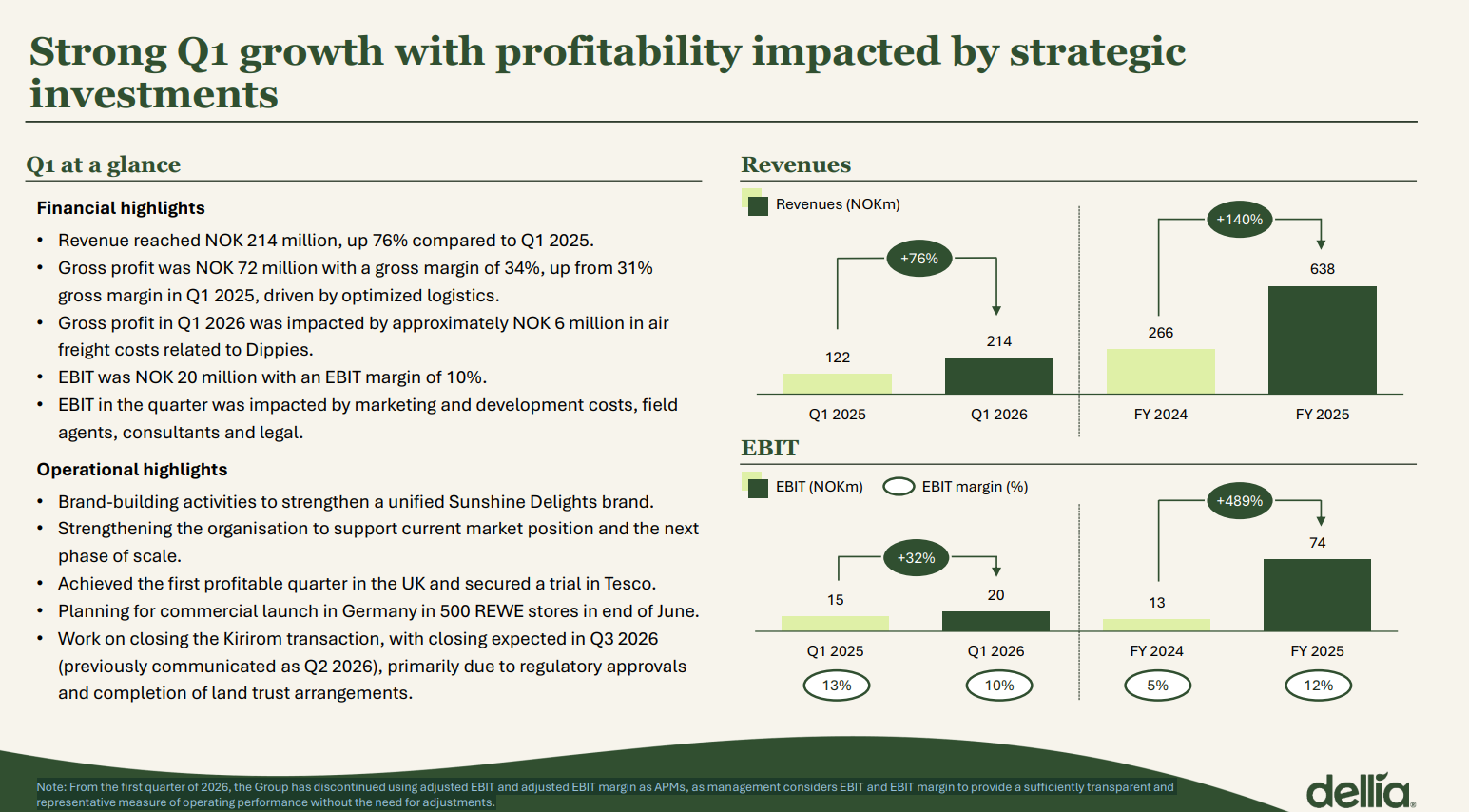

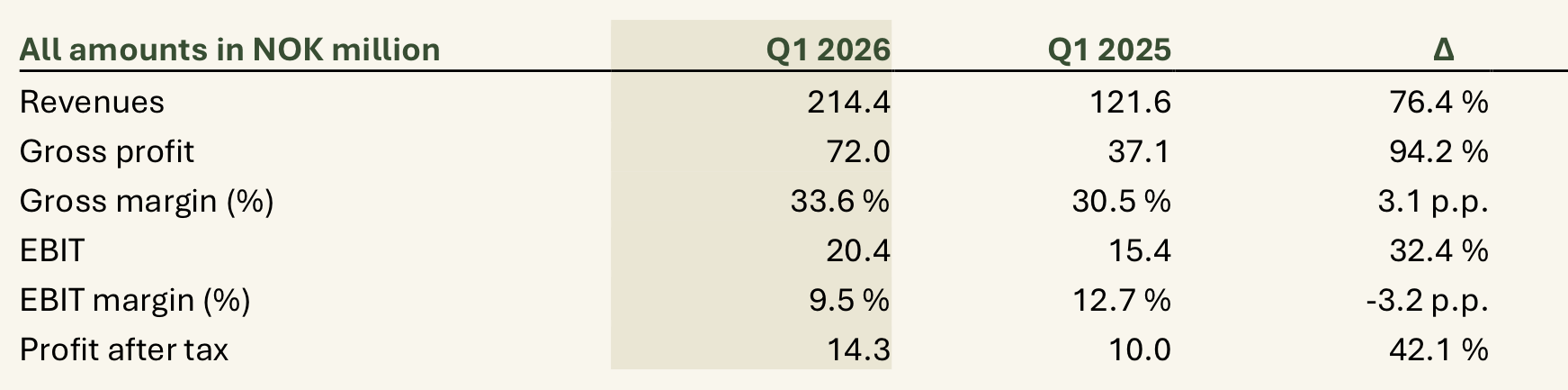

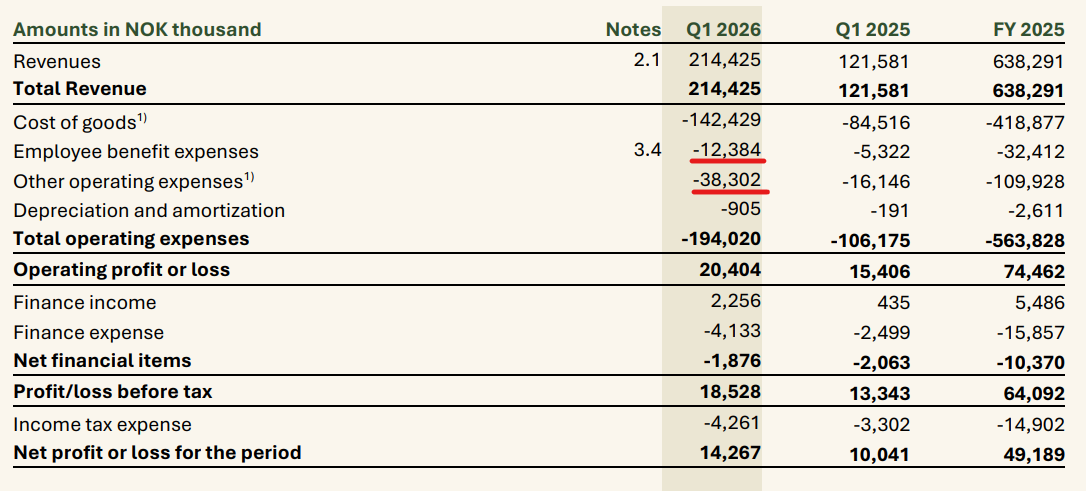

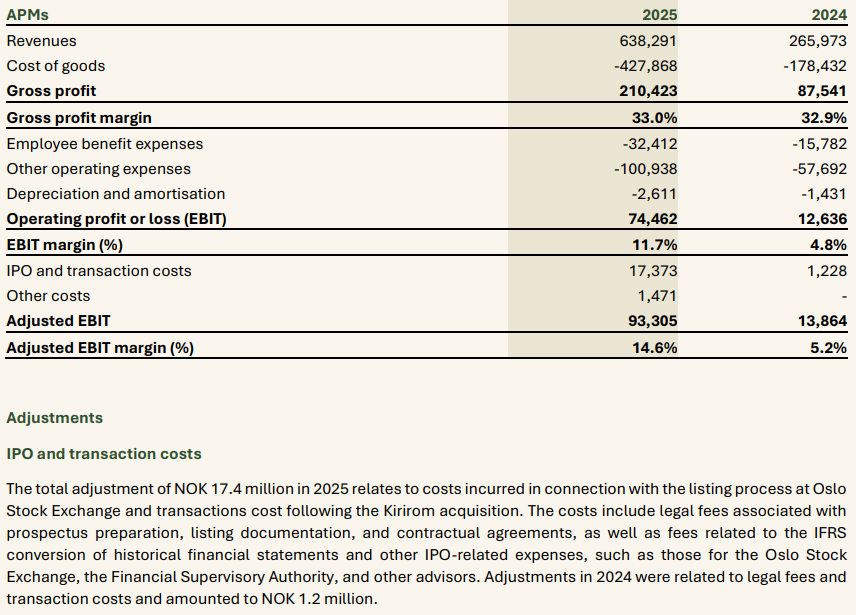

Q1 is out, strong revenue momentum continues, +76% YoY. Gross margin also developed favorably. On the other hand, there was downward pressure on the EBIT margin, partly due to marketing investments. The company apparently threw adjusted EBIT into the trash, which is always a positive Expenses likely include a fair amount of consultant and legal fees related to the Kirirom acquisition. Need to dive deeper into this when I have more time.

Note: From the first quarter of 2026, the Group has discontinued using adjusted EBIT and adjusted EBIT margin as APMs, as management considers EBIT and EBIT margin to provide a sufficiently transparent and representative measure of operating performance without the need for adjustments.

EDIT: and the closing of the Kirirom deal is pushed back a bit:

Work on closing the Kirirom transaction, with closing expected in Q3 2026 (previously communicated as Q2 2026), primarily due to regulatory approvals and completion of land trust arrangements.

The results seem to have fallen significantly short of expectations, at least at the operating profit level. It might be a good spot to add to the position if it dips significantly.

It’s not stuck; the Oslo Stock Exchange just halts trading if the price moves too much (for some reason).

To my eyes, I didn’t see anything majorly wrong with the quarter, so I guess I’ll have to buy more while it’s cheap. Growth is strong, after all; the profit will surely follow.

If I had only looked at the quarterly report, I would have thought the share price would rise +30% instead.

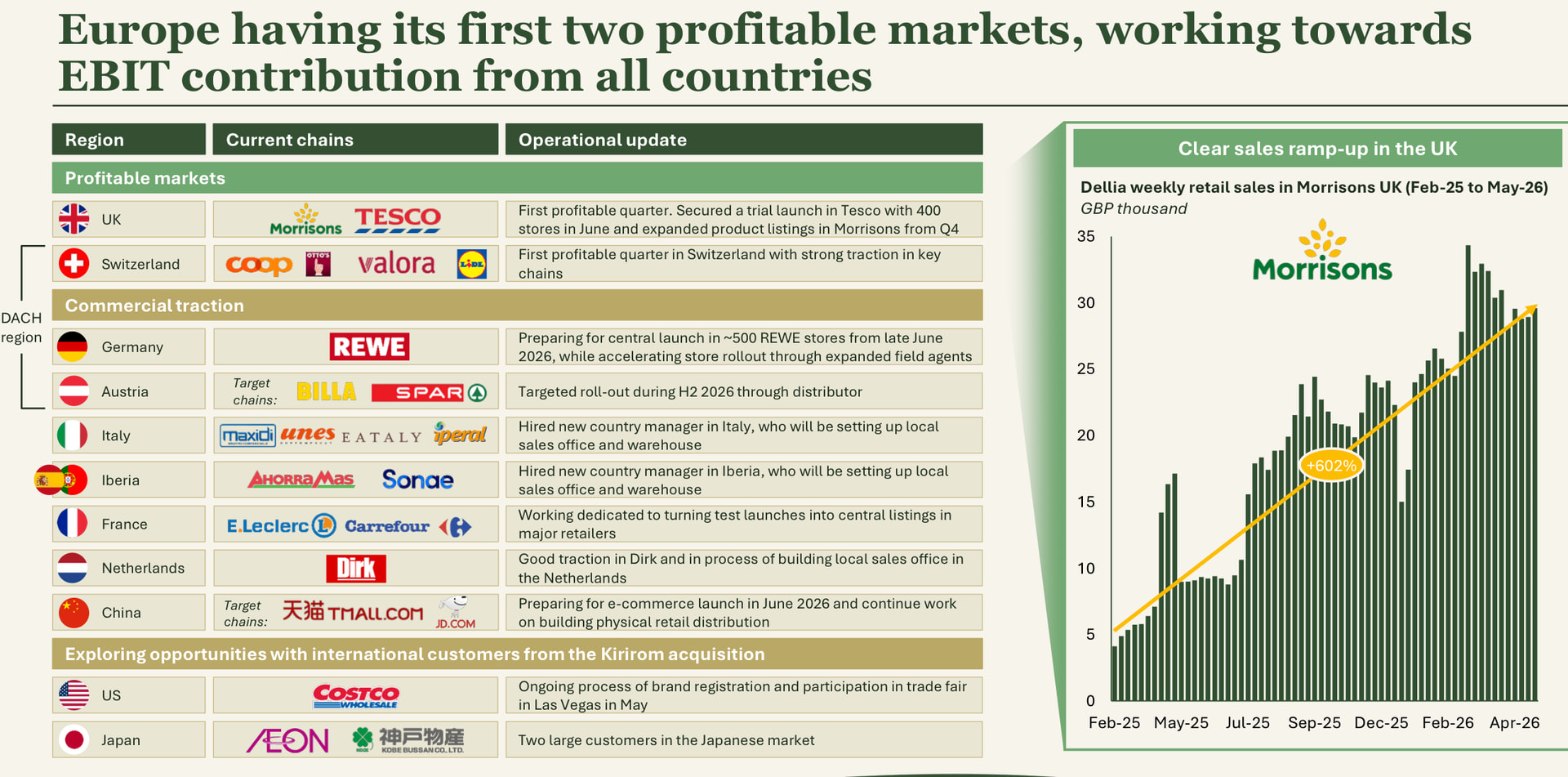

The German and Chinese markets will kick off in June, and as I understand it, the possibility of expanding into Japan has now been flagged for the first time.

No one should care about a risky acquisition being delayed by a single quarter, and I’ve heard some quite good arguments from investors as to why its cancellation might even be a positive development—so that this fruit company with an excellent brand doesn’t get mixed up in primary agricultural production, but instead focuses on higher-margin branding and sales operations. Growth is strong and the gross margin is only improving:

I don’t understand the share price reaction, and my first thought was whether it’s time to retire from this game altogether when the company in my portfolio that delivered the best earnings report drops the most

I haven’t looked into or even noticed this company before, but now that such a share price reaction caught my eye, I checked through the quarterly report’s business figures. Given those growth rates and the fact that the company is already profitable, I assumed the stock would be trading at P/E 30+ multiples, in which case a drop in the share price wouldn’t be surprising. Apparently not; it’s another one of these strange low P/E Nordic companies that experience suggests are probably best to stay away from, but I might have to consider a monitoring position .

Reading quickly, this must be what’s currently grating. Any kind of uncertainty is apparently absolute poison to today’s markets. It has never been liked, but to be punished like this is something else.

I’ve been wrestling with an uncertainty factor in another stock. ZIM is priced at 24 USD while HL’s binding offer is 35 USD, which the general meeting has approved. Granted, the State of Israel and its decisions are still in between, but since a second offer has been made at 37.5 USD, you would think some kind of deal will happen. The arbitrage is already significant enough that you can’t help but question the rationality of your own investment.

This somehow reinforces the idea that in this sentiment, uncertainty is penalized with a heavy hand.

Perhaps Mr. Market was spooked by this (from the earnings call):

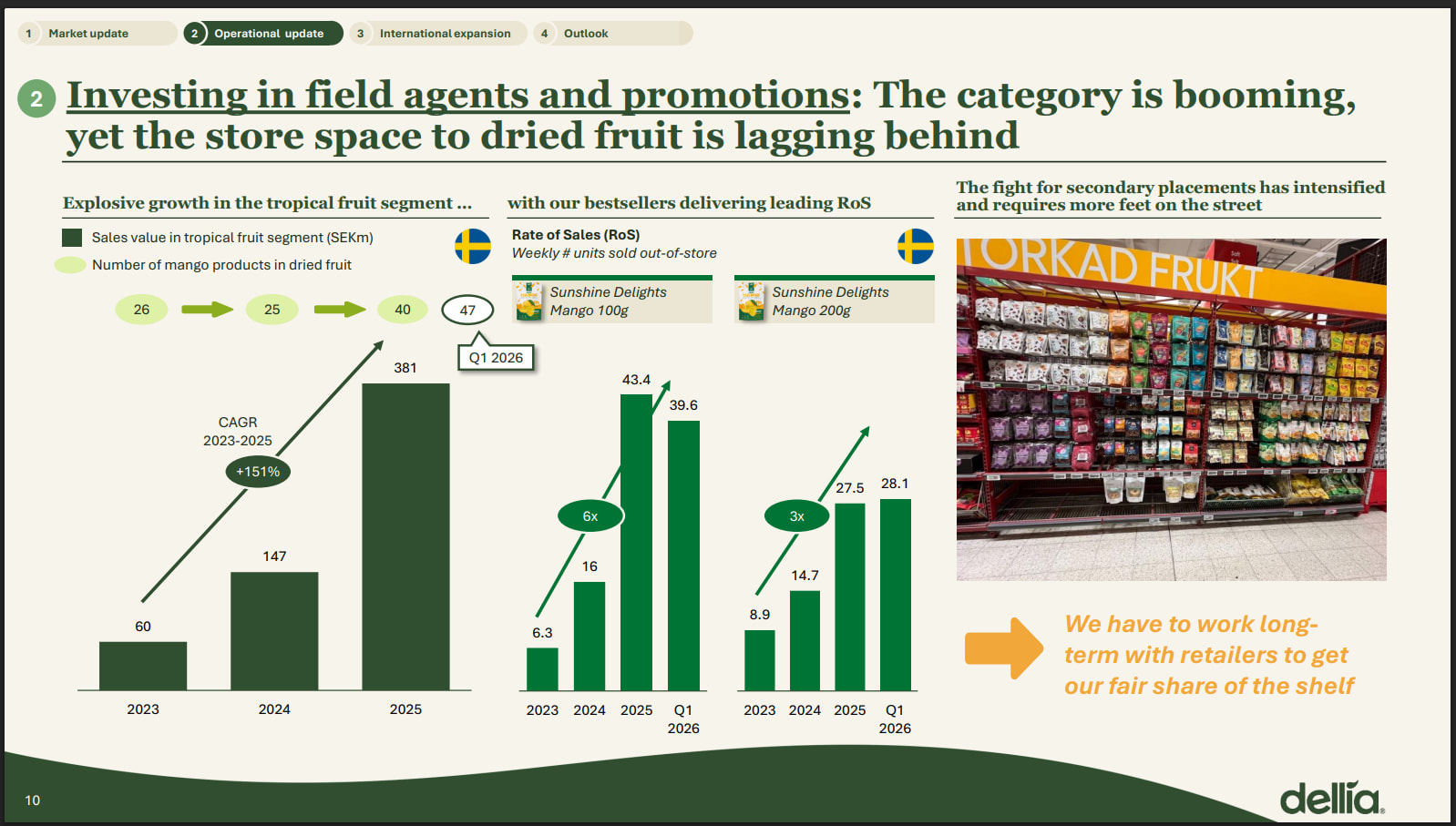

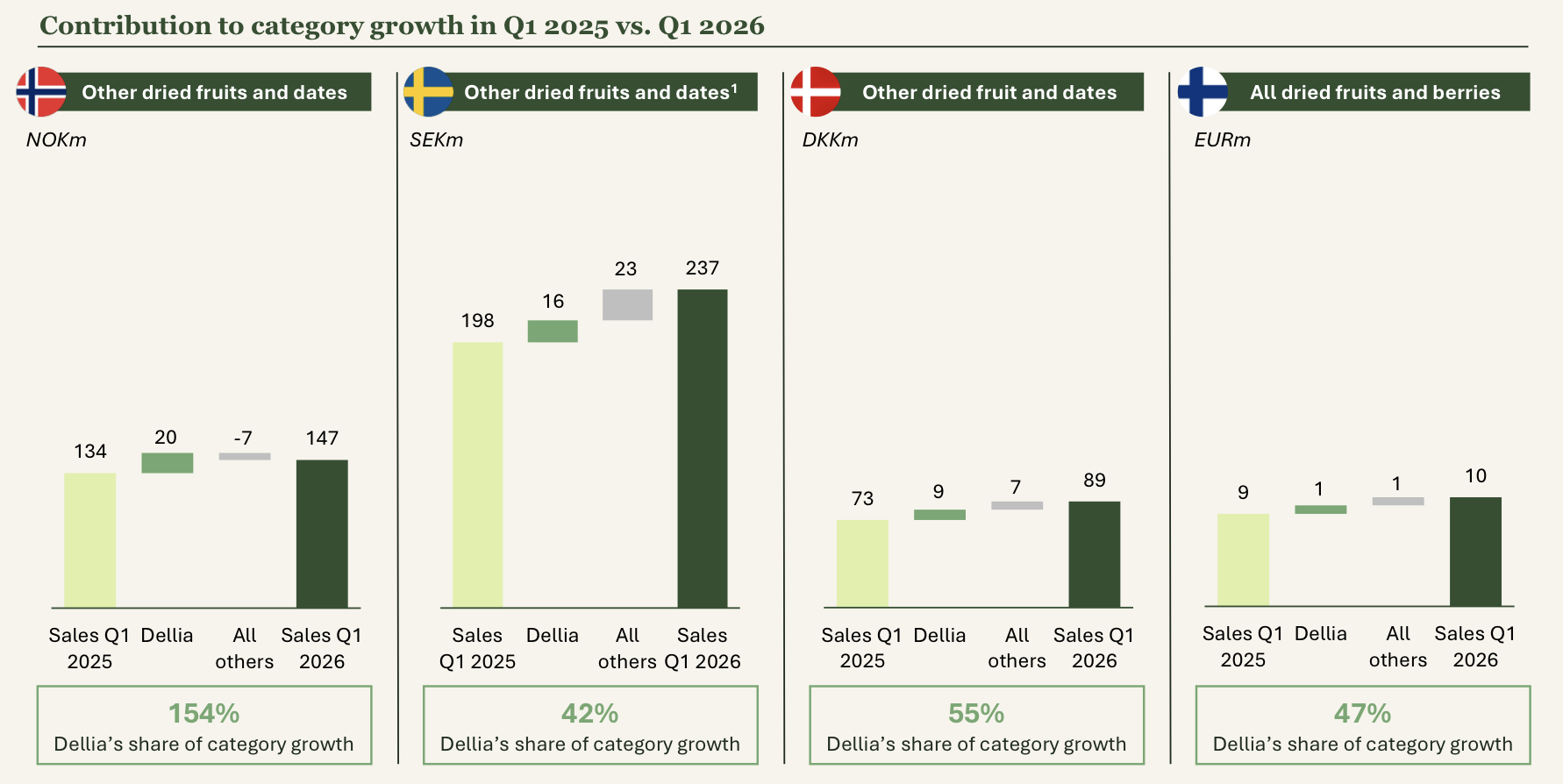

I want to look at Sweden as an example here. If you look on the left side, you can see the category, tropical fruit in Sweden. That’s a subcategory of dried fruit in Sweden.

It has grown from NOK 60 million in retail sales value in 2023 to in 2025, almost approach NOK 400 million in retail sales value. At the same period of time, the number of mango SKUs in Sweden has normally been laying flat around 26, 25, but during end of 2025 and in the first quarter of this year, the number of mango SKUs have almost doubled from 25, standing now at the first quarter 2026, at 47 units listed in Nielsen database. How did that impact our sales in this quarter? To understand that, we want to look on rate of sales, ROS. That is number of units sold out of the store per store, per week. From 2023, when we started launch mango 100 gram and mango 200 gram, it used to be around 6.3 units sold per week and 8.9 of the mango 200 gram.

That has grown up to the peak in 2025 in Sweden at 43.4 units. That came down now to 39.6 units in the first quarter. We have a slight impact on the ROS of the mango 100 gram. However, the 200 gram grew still from 27.5 up to 28.1. The impact on our rate of sales has not been that large, but you’ll start seeing some impact on it. What we have here now is a category that is growing. More and more mango SKUs going into the market during the first quarter of this year and end of last year. The space in the category, dried fruit, is the same as before. The space in the category haven’t changed. There’s a lot of more companies now fighting for the same space.

The fight for secondary placements or impulse location in the store has intensified during the quarter. That require much more feet on the street. The conclusion here is the category is booming, yet the store space of dried fruit is lagging behind, meaning we have to work long-term with retailers to get our fair share of the shelf. We are working on all fronts to give the category its fair share of store space.

In other words, the number of product SKUs in this category (in Sweden) has doubled over the last six months, and consequently, competition for shelf space has intensified. During the same period, the company’s sales per point of sale have decreased by 10% in this category. The company sees this as something they now need to focus on heavily, meaning they anticipate competition tightening even further.

That -10% dip in weekly sales per store seemed to only affect the 100g bags, whereas the 200g bags were still chugging upwards. Admittedly, a lot of competing products have entered the Swedish market; Peter Lynch would already be heading for a trip to a Swedish supermarket Many of these have appeared on shelves in Finland too, but so far they haven’t been challengers in terms of taste or price.

The market also seemed to be spooked by the fact that operating leverage was no longer visible in the margins; instead, operating expenses came in quite front-loaded, and they weren’t even softened with adjusted figures, which I personally definitely like.

This is quite normal in such an explosive growth phase when the organization is struggling to keep up with the growth and occasionally needs to recruit more heavily or make other growth investments, such as in marketing. Scaling rarely happens as if drawn with a ruler at this stage, especially when pushing forward in multiple markets simultaneously and a lot is happening The situation of a single quarter doesn’t really tell you anything about this. However, the gross margin scaled nicely.

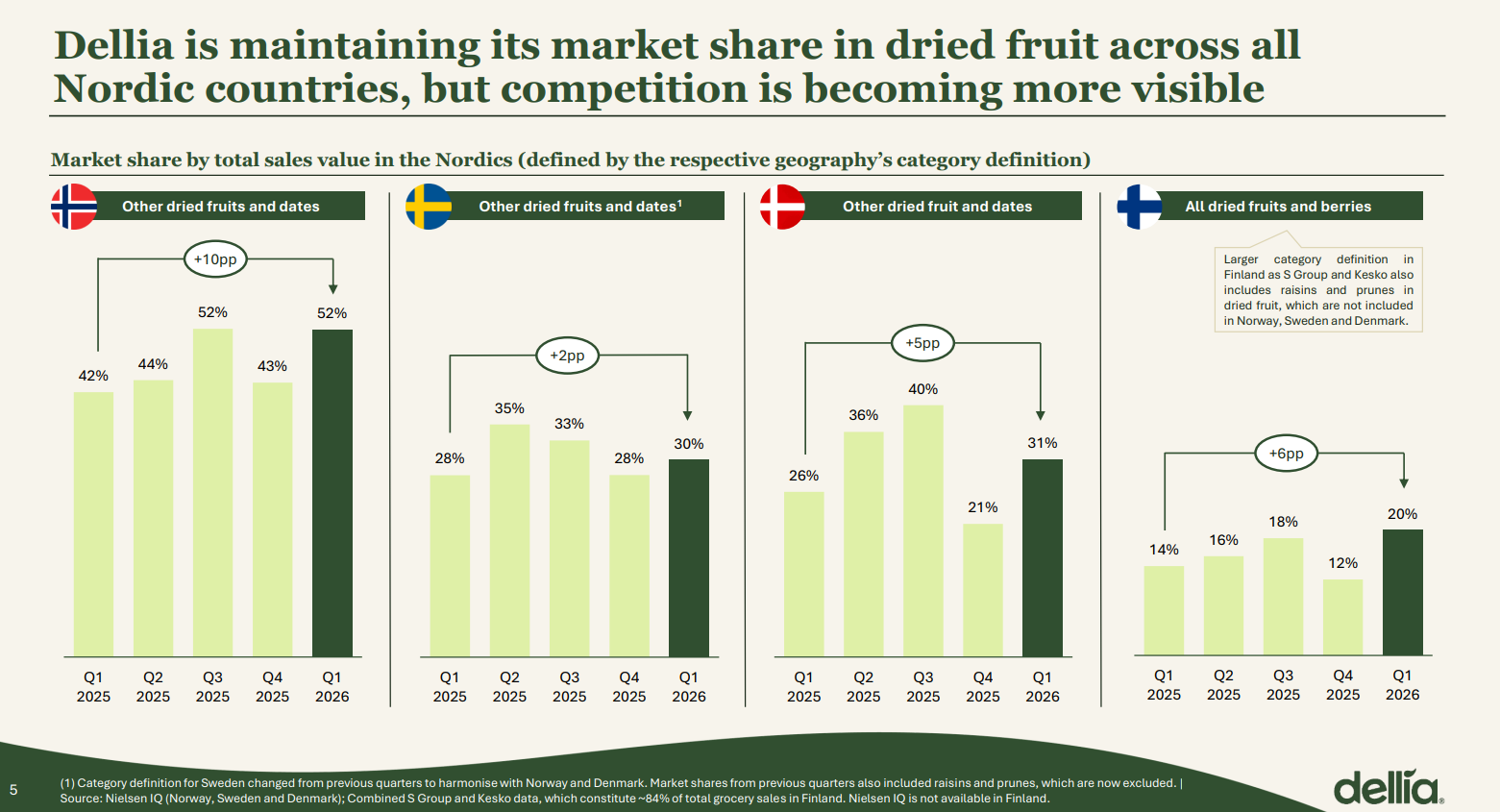

Personally, I’m not too worried about the competition at this stage either, as things are progressing in Europe and in the Nordics the entire product category is still growing rapidly, driven by Dellia, requiring more shelf space. Market shares, however, remain stable. Concern would definitely arise if the product started losing market share more clearly in the Nordics, even if things were happening in Europe meanwhile. This will certainly be closely monitored with Mr. Market in the coming quarters. A single quarter is too short a time to draw any conclusions, but Mr. Market already made his

I personally see it this way: even a loss of market share isn’t necessarily a bad thing, as long as comparable sales grow at the same time and EBITA remains under control. In this industry, it’s quite normal for a so-called first mover to lose market share while still growing profitably at the same time. 20% of a million-dollar market is significantly better than 50% of a hundred-thousand-dollar market, and so on.

The example from Sweden is concerning in the sense that absolute sales in that category decreased even though money was poured into the war for shelf space. But that is just one data point; the big picture is what matters. However, these are the two things that will determine Dellia’s success: like-for-like sales growth (selling the same products in the same stores) and the cost of “marketing expenses,” i.e., the shelf war. I believe the gross margin will be easy to maintain at a good level. Opening new countries is, of course, important for long-term growth, but the development of more mature markets provides an indication of the entire company’s business potential.

Now if this Iranian oil crisis would just push transport costs to the max and cause a temporary drop in the share price and a buying opportunity, I’d be more than happy to jump in

I don’t understand the price reaction, and my first thought was whether it’s time to retire from this game altogether, when the company in my portfolio that posted the best quarterly report is also the one dropping the most

Better to start off with small stakes

In other words, the number of product SKUs (in Sweden) in this category has doubled over the last six months, and consequently, competition for shelf space has intensified. During the same period, the company’s sales per point of sale have decreased by 10% in this category. The company sees this as something they need to focus on heavily now, meaning they expect competition to tighten even further.

I’m not (that) worried about competitors at the moment; we’ve discussed the difference in quality in this thread before. But competitors will surely catch on to this. Could Dellia be an interesting acquisition target?

I generally try to look at the bigger picture in investing, and my biggest long-term concern is the trend sensitivity of this particular (premium dried fruit) market. A niche market in a “lifestyle” segment like this is always a bit tricky. After all, Peloton has amazing state-of-the-art exercise bikes too (maybe not the best example because of Covid, but it works).

Good point, thank you! Can you say where these shelf war costs mainly show up in the income statement for players in this industry, or in Dellia’s case as the competition gets tougher? In the report, it was commented that it partly weakened the gross margin, as they had to, among other things, give lower prices to retailers and run joint campaigns.

With nearly -40% on the board, one can once again say that valuation levels have normalized

EV approx. 1.3 billion NOK

LTM reported EBIT 80 million NOK

EV/EBIT approx. 16x

The reported EBIT includes, for example, IPO costs of over 17 million NOK, which one can consider whether it is a recurring expense Additionally, there is likely less need for consultant and legal fees once the Kirirom acquisition is completed. Everyone can adjust these according to their own taste using the information from the annual report.

On that basis, one could build a reverse DCF and consider the expectations, but roughly the market expects some of these or all of them:

Growth stalls, market entry in Europe is only achieved to a very limited extent, if at all? Not to mention the US, Asia, or anywhere else.

The Kirirom acquisition does not materialize at all or it fails, resulting in years of integration hell with heavy costs?

Growth in the Nordics will only be very modest in the future and competition starts eating into margins → operational leverage is no longer seen, and instead, the company will struggle at the current level combined with anemic growth?

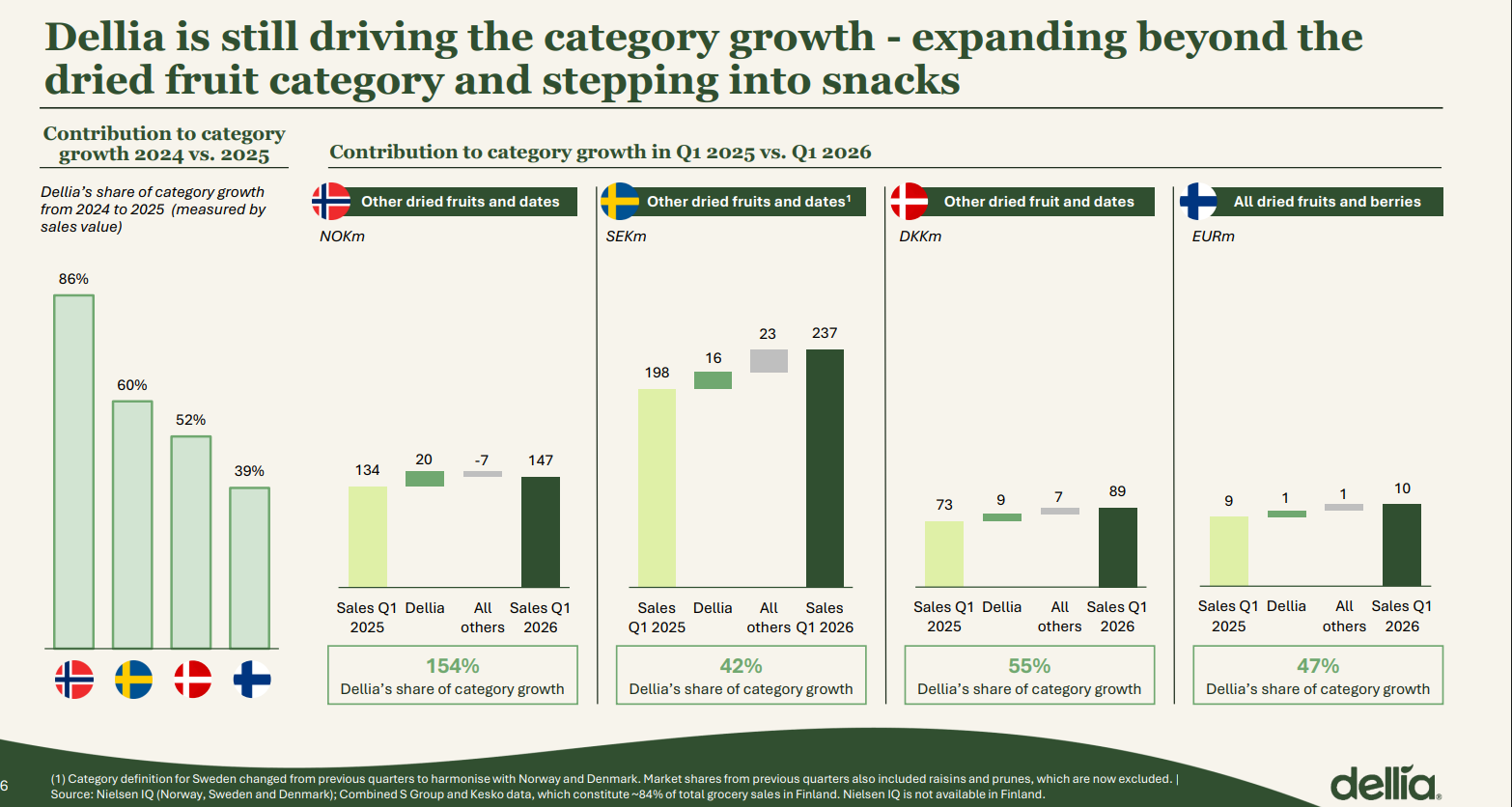

I wouldn’t find it very surprising that such a rapidly multiplying blue ocean market also attracts all kinds of experimenters, and the rising tide helps all market players. So far, Dellia has captured a large portion of the category’s growth for itself:

In Q1, there were even delivery difficulties, and in some stores, both sales and shelf space were lost to competitors because there was nothing to deliver and they had to resort to expensive air freight. It is quite clear that in such a situation, you have to put the brakes on sales growth a bit. Also, unit sales per store decrease even if revenue grows, as the product is introduced to less attractive retail locations. They likely entered the best locations first. Sales of basic mangoes are also being cannibalized by the company’s own other new mango products, such as strawberry mangoes:

I would consider it certain, however, that the Nordic countries will shift to a red ocean market in the coming years when the category no longer grows at the same pace and market shares must be competed for from other products. At that point, economies of scale and the brand must be in order to compete smaller players out of the market. I find the company’s brand name, Sunshine Delights, a bit clunky and the bag design is amateurish, as every bag is opened by throwing the company logo into the trash, and then after tasting, it is no longer easy to find out whose tasty products you are actually eating. Fortunately, more investment will be put into this now, but the Norwegians, as a dividend-oriented people, will surely penalize the stock when money is invested in the business instead of being distributed as dividends.

Sweden is currently clearly the most competitive of all Dellia’s markets, and for now, the situation cannot be generalized to other markets. They were able to grow for a long time without significant challengers, so of course, it cannot come as a surprise that at some point other companies wake up to the lucrative opportunity. However, the company management guides that similar competitive pressure is not visible in Europe, and those are several times larger markets. Even if growth in the Nordics were to be only in the double-digit percentages in the future, the revenue will easily multiply driven by other sales.

Regarding China, it was mentioned that tourists in Europe have been asking when these products will be available in their home markets, and regarding the United States, it was guided in the quarterly call that trademark registration is in the final stages, after which they can attempt to launch sales. Such strong growth is being sought from abroad that such a massive share price reaction to potentially slower growth in a single country during a single quarter seems like an absurd overreaction.

Let’s put a shelf tour in Sweden on the to-do list for June

Admittedly, their products taste great, and it’s no wonder consumers are picking them up from store shelves.

I came across this company for the first time earlier this week, and my initial thought was: what is a company like this doing on the stock exchange? Usually, these small firms pursuing rapid international growth are creating value for PE (Private Equity) investors.

Now, the risk of being listed seems to be materializing, where stock market investors are scrutinizing the bottom line with a magnifying glass, which spoils inorganic growth opportunities fueled by using one’s own shares.

Greetings to the thread. Dellia’s mangoes are a hit here too!

I found this Dellia thread and have been following along. What bothers me about the investment case is the basic issue that it’s difficult to imagine a competitive advantage. Could someone help me visualize their moat?

The product, while in my opinion tasting good and being the best, is still generic and contains nothing that a competitor couldn’t bring to the table. Do you see anything exceptional regarding the product?

The market situation undeniably suggests that dried fruits as a category are currently on a strong upward trend. In your opinion, is this enough to support the investment case?

Regarding market position, it seems Dellia was the first to capture market share with a good product. Are there enough grounds here? Is it enough to capture the market leader position now and just hang on to it?

Is Dellia simply at such an early stage in its story that growth will show in the numbers for that reason alone?

Does Dellia have anything else that could be considered a competitive advantage?

I know it’s very old-fashioned to ponder a company’s future this way, but it would be very interesting to hear your thoughts. So far, I’ve stayed away from the stock, but I’ve been monitoring the situation since the beginning of this year. Of course, the drop in share price at the end of the week makes me wonder once again.

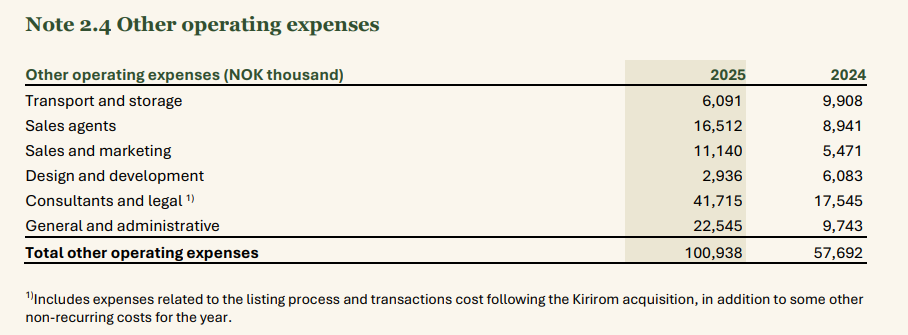

Of course, the gross margin can also take a hit when campaigning together with retailers, but at least so far, this hasn’t shown up significantly in the numbers. Otherwise, the costs of the shelf war go under “Other operating expenses,” which is reflected in the EBIT but not in the gross margin. Dellia doesn’t break down expenses more specifically than that in their quarterly reporting, but the annual report provides more detail:

From these, the items “Sales agents” and “Sales and marketing” are directly where the shelf war costs flow. “Transport and storage” can also increase if, to please the retailer, deliveries are made in smaller batches more frequently—this is a form of subsidy as well. On an annual level, it is therefore worth monitoring the ratio of these items to revenue in addition to the gross margin development. On a quarterly level, one has to settle for the entire “other expenses” pie, which contains a lot of other things as well.

These same questions apply to all food industry products, from Vaasan Ruispalat to Coca-Cola. It is completely impossible to create an edible product that someone else couldn’t copy, as food products don’t have the same patent protection as, for example, pharmaceuticals. Nevertheless, some companies will always win the shelf war and their packaging ends up in the shopping basket decade after decade, while others disappear from store shelves entirely.

Competitive advantages stem from the brand, product range, supply reliability, scale, and potentially later from vertical integration. Currently, they are mostly operating only in the small Nordic markets, and sales in the less competitive German-speaking countries, the UK, and China are only just beginning. Even after those, France, Japan, and the United States are on the list, so the targets for revenue growth aren’t going to run out anytime soon. The most important thing now is to capture markets faster than competitors and achieve a market leader position in all key markets so that it cannot be easily challenged later.