I tried to find comments and posts about CTT Systems on the forum, but I couldn’t find any. This is definitely an interesting company that deserves its own thread.

CTT System AB in brief:

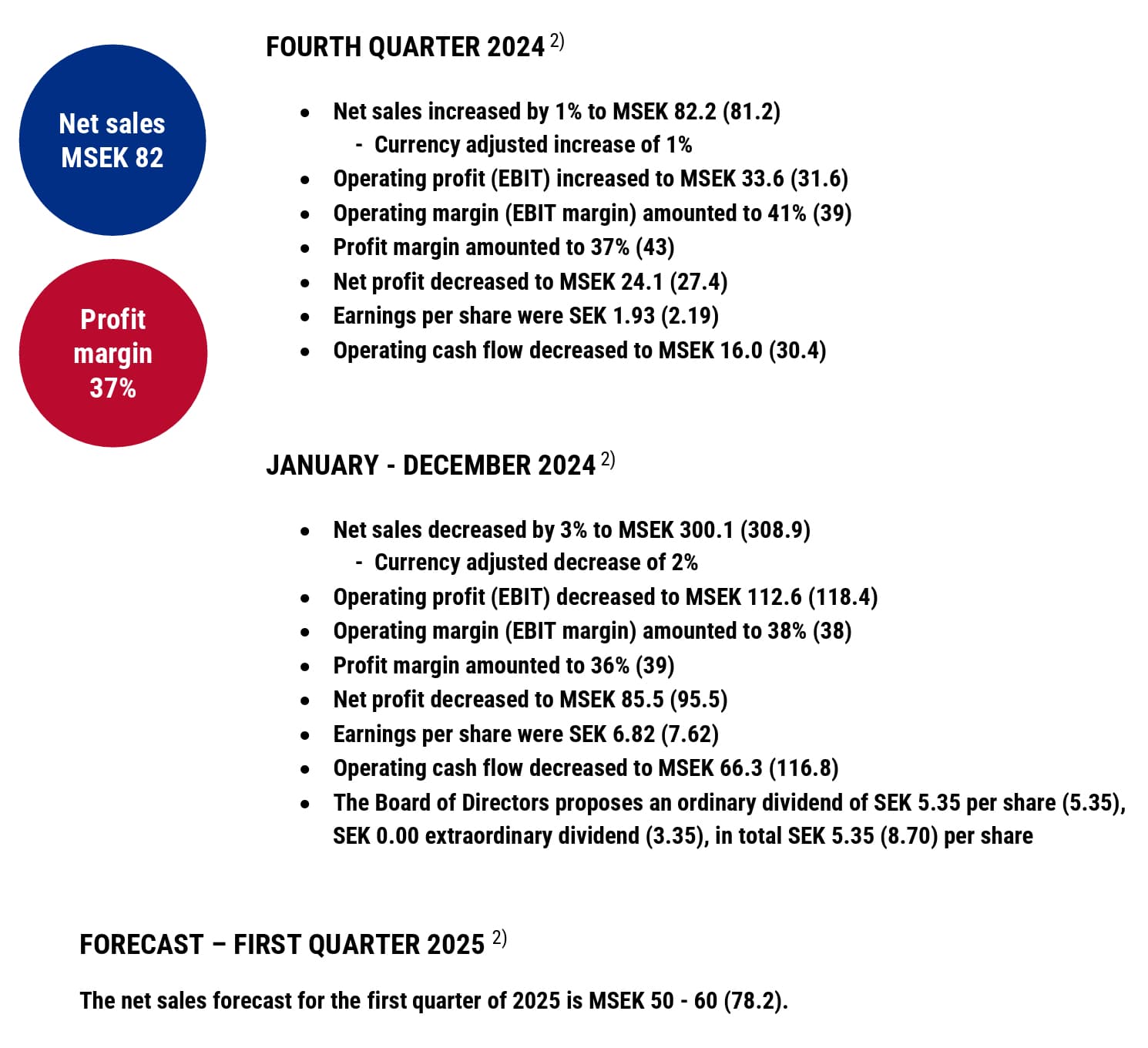

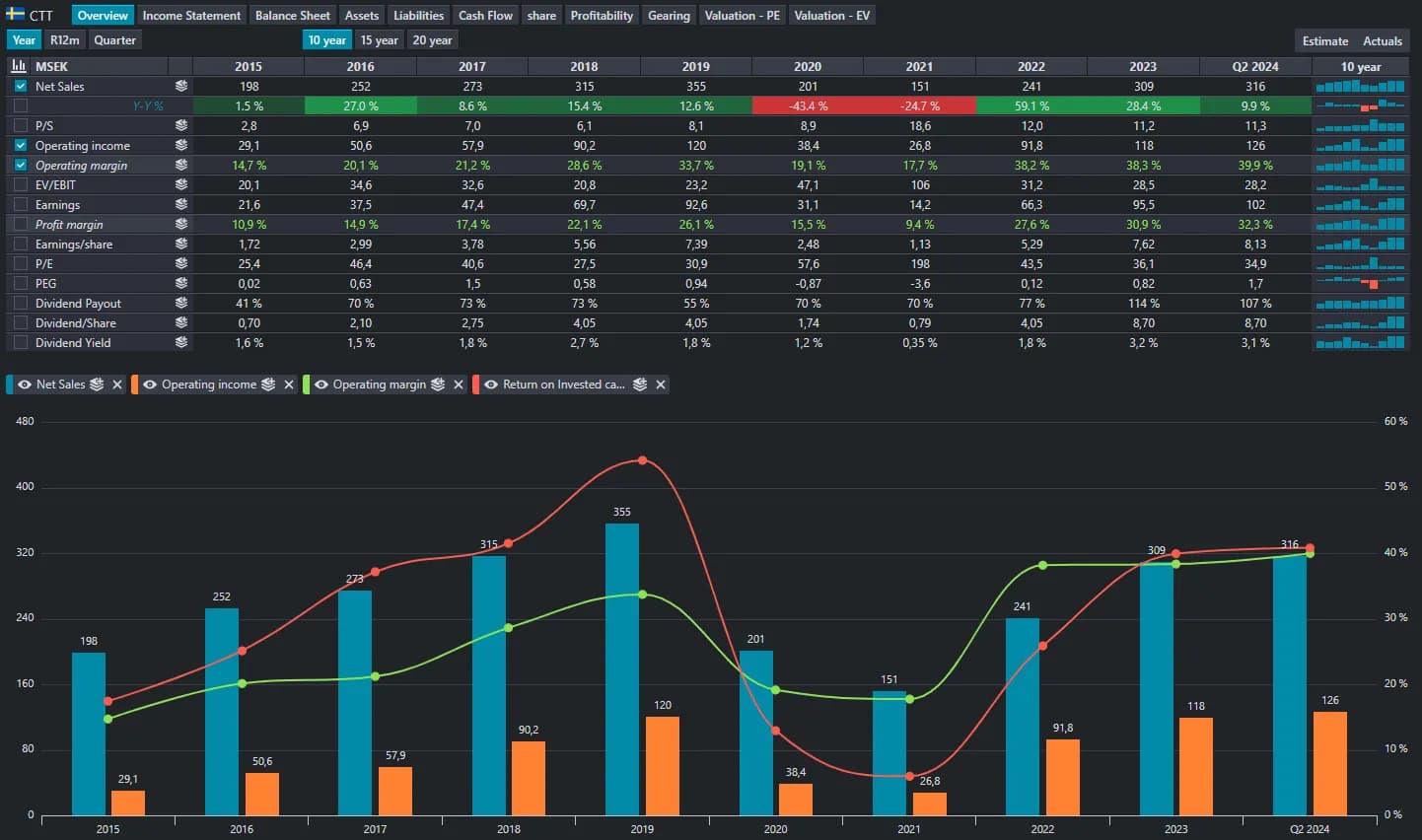

CTT Systems AB (CTT) is a global leader in the manufacture, design, and supply of active humidity control products for aircraft, aiming to solve the aircraft moisture paradox. CTT’s products are available for both line-fit and retrofits in commercial aircraft, as well as in private jet outfittings. The company is headquartered in Nyköping, Sweden, and had 80 employees at the end of 2023. CTT Systems’ market cap is currently 3,583 million SEK (316 million euros), and the company has a net cash position. In 2023, CTT’s revenue was 309 million SEK, and the company achieved an operating profit (EBIT) of 118 million SEK, representing a 38% EBIT margin.

Historical financial development:

CTT experienced strong financial growth between 2015 and 2019, but the COVID-19 pandemic interrupted this development. Revenue grew impressively, driven by system sales and rapidly expanding aftermarket sales. As the share of aftermarket sales grew, CTT’s profitability also improved. Now CTT is ready to return to the same growth path it was on before the pandemic.

Investment case in a nutshell:

CTT Systems offers an attractive investment opportunity as it is the sole supplier of humidifiers for major wide-body aircraft programs such as the Airbus A350, Boeing 787, and Boeing 777X. As production rates recover and 777X production begins in 2025, CTT is excellently positioned for a long growth trajectory. The company’s high-margin and recurring revenue aftermarket segment operates on a “razor-and-blade model,” ensuring profitability and stable cash flows as the installed base expands. The company operates with an asset-light business model and has a strong balance sheet, including a net cash position. CTT also provides downside protection, as it may attract interest as an acquisition target among aerospace industry players or private equity firms if its valuation drops significantly below its intrinsic value.

Interesting features:

- Monopolistic business nature

- Attractive growth prospects for years to come, supported by increasing production rates of key aircraft programs (B787, B777x, and A350), an increase in the number of systems per aircraft as penetration of different systems increases, a growing private jet business, and a strongly growing aftermarket.

- Very high profitability thanks to attractive aftermarket sales following the “razor-and-blade” model.

- Growing share of the aftermarket, which is recurring in nature, increasing business predictability in the long term.

- Asset-light business model – focuses on assembly and R&D.

- Operating in an industry with high barriers to entry.

- Strong balance sheet – net cash position.

- Downside protection – if CTT’s valuation drops significantly, it could become a very attractive acquisition target for either a strategic player in the aerospace industry or a private equity firm.

- Competent and committed management and staff – The Chairman of the Board owns 13.4% of the company, and the CEO owns approximately 0.5%. Additionally, CTT has a profit-sharing foundation that grants every full-time employee an equal share of the company’s financial success annually.

I also wrote a longer analysis of CTT. You can find it here: https://substack.com/home/post/p-148315513?source=queue&autoPlay=false