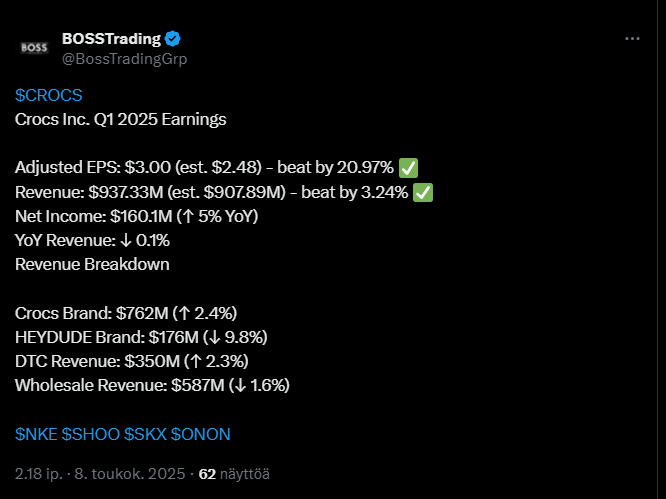

Crocsilta tänään lukuja. Löytyi jopa hyviä merkkejä HeyDuden osalta, viimeisellä neljänneksellä HD liikevaihto ei enää laskenut ja DTC myynti kasvoi 7.2%. Näkymissä kaavaillaan HD liikevaihdon edelleen laskevan.

Omienosto-ohjelmassa valtuutus 1.3mrd$, yhtiön markkina-arvon ollessa noin 6mrd$.

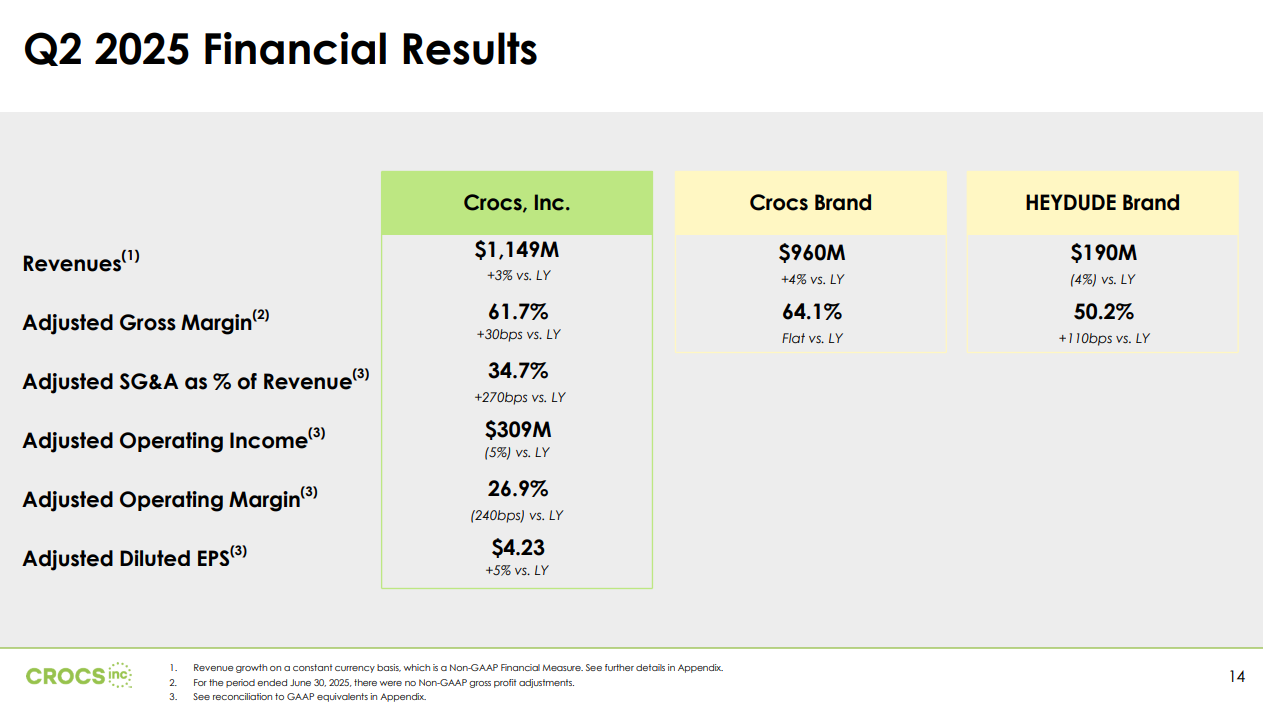

Crocsin liikevaihto kasvoi hieman ja erityisesti suoramyynti kehittyi vahvasti, mutta tukkumyynti pysyi lähes ennallaan. Liikevoitto parani ja yhtiö jatkoi osakkeiden takaisinostoja sekä velkojen lyhentämistä.

Itse Crocs-brändin myynti kasvo odotettua enemmän erityisestiPohjois-Amerikassa ja Kiinassa, kun taas tuo jo mainittu HEYDUDE pysyi edellisvuoden tasolla.

Tänä vuonna eli 2025 Crocs odottaa kasvun jatkuvan ja panostaa em. HEYDUDE-brändin elvyttämiseen. Yhtiö tähtää vahvaan kannattavuuteen ja pitkän aikavälin arvonluontiin.

Crocsin lippulaiva kenkä näyttää dominoivan Amazon.comissa ja on ollut Toukokuun alusta #1 Best Seller “Clothing, Shoes & Jewelry” -Kategoriassa. All time volyymitrendit näyttää myös hyvältä. Tiedä sitten kuinka hyvin Amazon indikoi myös muiden kanavien performanssia, mutta otin anyway position kiinni.

“Crocs, maailman johtava innovatiivisten vapaa-ajan jalkineiden valmistaja kaikille, tuo monsuunitunnelman etualalle kaikkien aikojen alueellisesti syvällisimmällä kampanjallaan, kattaen seitsemän keskeistä Kaakkois-Aasian markkina-aluetta, mukaan lukien Intia, Kiina, Japani, Korea, Thaimaa, Indonesia ja Filippiinit.”

Tunnuslukuja sekä kassavirtaa katselemalla vaikuttaa todella hyvältä, varsinkin jos tänään uutisoitu aasian kampanjointi alkaa puremaan kovemmin.

Liikevaihto 4.1mrd, ebit 1mrd markkina arvo 5.5mrd… Mietimpähän vaan, painaako markkina-arvoa tällähetkellä muu kuin kasvun näkymät sekä 1.8mrd lainat?

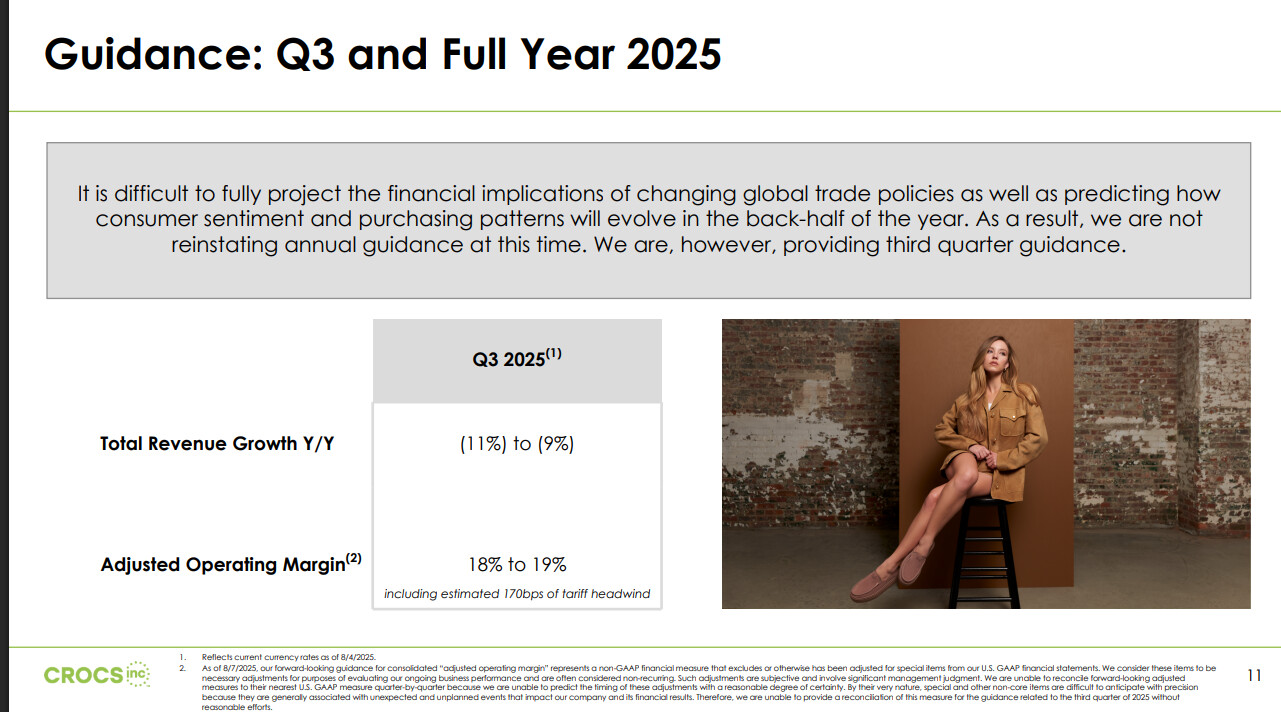

Toki tariffiuhkat on kääntänyt käyrän tänävuonna monesti.

Kasvun näkymillä itse lähinnä tarkoitan että onko talo kuitenkin vähän liikaa “parin tempun sirkus”, mihin asti näillä eväillä mennään?

Jenkki-bullerot redditissä sekä muutamilla muilla palstoilla hehkuttaa kovasti, ja kieltämättä houkuttaa nykyarvostuksella.

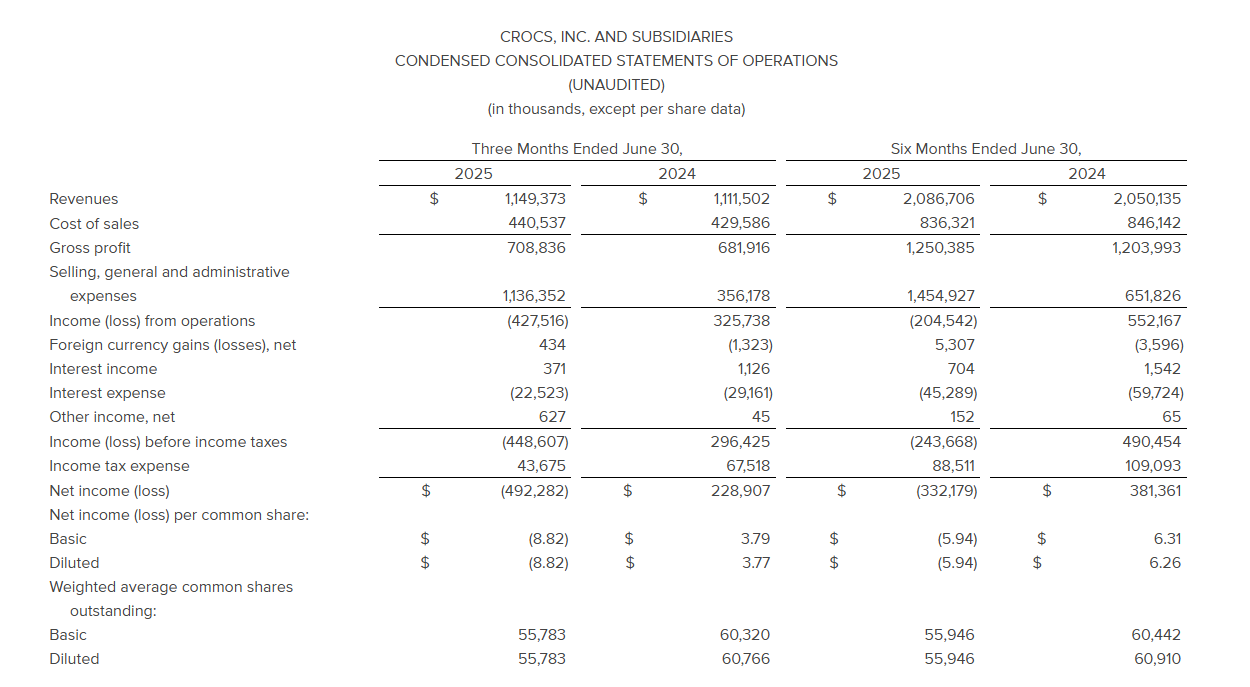

Crocs raportoi maltillista kasvua tällä kvartaalilla ja yhtiön bruttokate oli kuulemma ennätyksellisen korkea. Myynti kasvoi niin suorassa kuluttajakaupassa kuin myös tukkumyynnissäkin, mutta HEYDUDE-brändin liikevaihto hieman laski. EPS-tappiot johtuivat kertaluonteisista alaskirjauksista, mutta oikaistu tulos nousi.

Toimitusjohtaja Andrew Reesin mukaan toimintaympäristö on epävarma, joten yhtiö panostaa kustannussäästöihin, varastojen hallintaan ja hillitympään kampanjointiin. Yhtiö ainakin itse odottaa näiden toimien tukevan pitkän aikavälin kannattavuutta ja kassavirtaa, vaikka ainakin ne voivat hetkellisesti painavat liikevaihtoa.

Tähän on hyvä palata: HeyDuden kääntäminen menestystarinaksi olikin huomattavasti vaikeampaa kuin johto antoi ymmärtää ja näin on juuri käynyt. Nyt Q2/25-raportissa myönnettiin käytännössä rivien välissä: “The impairment was justified by a longer-than-expected time line to stabilize the HEYDUDE Brand”.

Mutta nyt kun impairment on vihdoin siivottu alta pois, tilanne näyttää selkeämmältä. Crocsin johto on varovainen Pohjois-Amerikassa, mutta luottavaisempi etenkin Aasian suhteen, ja siinä voi olla tuleva kasvutarina. Alan itsekin olla kiinnostunut osakkeesta, jos saisi ostettua 70usd paikkeilla.

Crocsilta ihan mukiin menevä tulos tuli tänään ja ihan mukiin menevä ohjeistus. Ei mikään huippu, mutta ihan ok kun ottaa huomioon osakkeen hinnan. Minä ja vaimo osteltiin tuolta $78-75 kieppeiltä. Markkinat on odottanut aivan surkeutta ainakin kun katsoo Crocsin osakkeen kehitystä. Ihan kohtalainen voi kuitenkin riittää, sillä ainakin on nyt pre-marketissa noin 15% nousussa. Kyllä kun tuota miten tahansa pyörittää niin kaikki alle $100 näyttää omaan silmään melko naurettavalta.

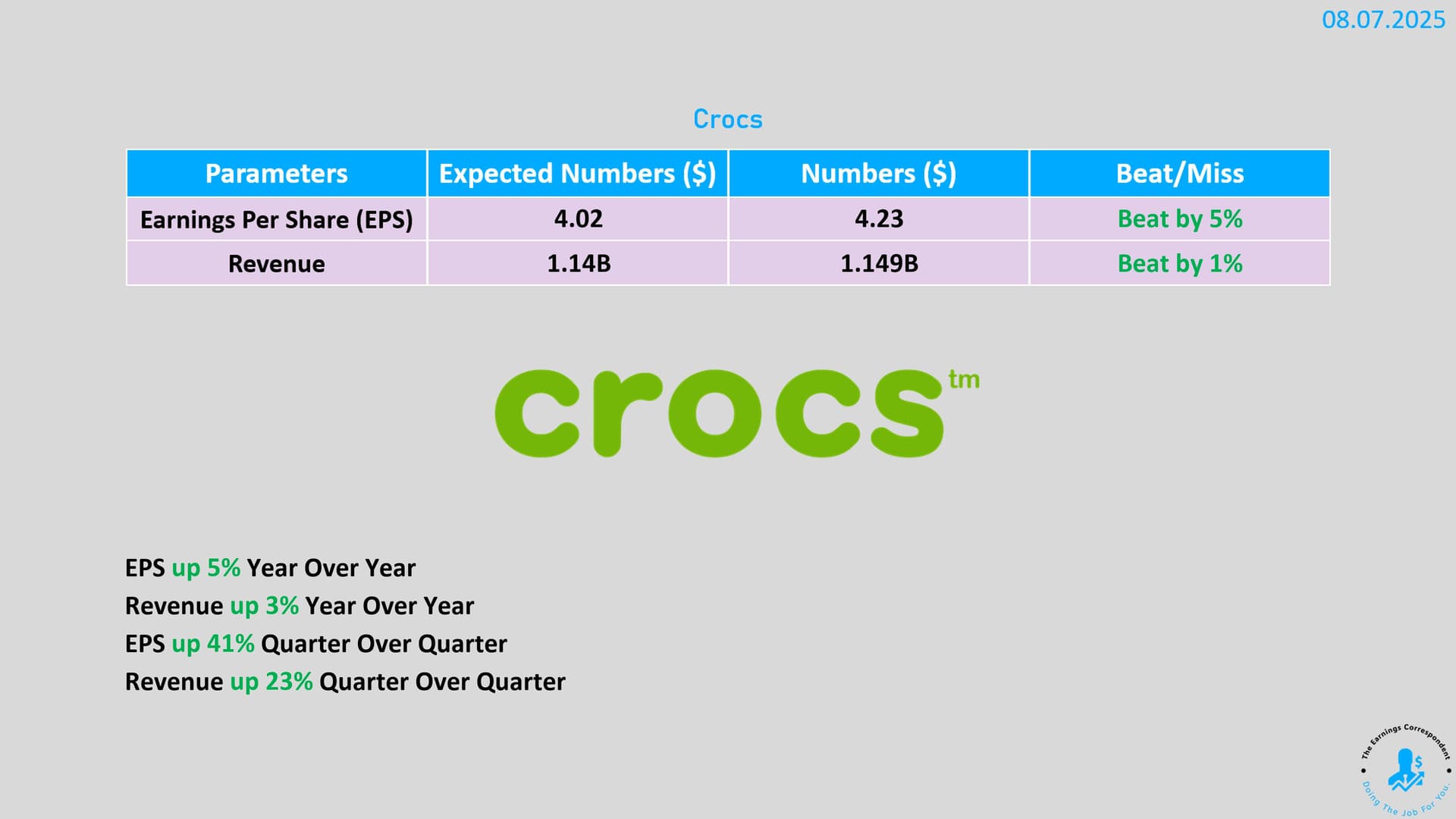

Tekivät oikaistua EPS:ä vuonna 2025 $12.51 (laskua 5% vuotta aiemmasta). Osake on noin 82dollaria, josta saadaan P/E 6,6 kun käytetään oikaistua lukua. Ensi vuonna odotetaan että päästään haarukkaan $12.88 - $13.35. Jos nyt lasketaan karkeasti $13 niin saadaan nykyhinnalla P/E 6,3. Aika halpaa vaikka samalla Hey Dude oli ihan vika ostos ja se sulaa koko ajan pienemmäksi ja pienemmäksi. Enää sillä ei sijoitustarinan kannalta ole paljoa väliä.

Fourth Quarter 2025 Operating Results (Compared to the Same Period Last Year)

Consolidated revenues were $958 million, a decrease of 3.2%, or 4.2% on a constant currency basis. Direct-to-consumer (“DTC”) revenues grew 4.7%, or 3.6% on a constant currency basis. Wholesale revenues decreased 14.5%, or 15.5% on a constant currency basis.

Gross margin was 54.7% compared to 57.9%. Adjusted gross margin decreased 320 basis points to 54.7% compared to 57.9%.

Selling, general, and administrative expenses (“SG&A”) of $377 million increased 1.1% from $373 million, and represented 39.4% of revenues compared to 37.7%. Adjusted SG&A of $363 million decreased 2.7% from $373 million, and represented 37.9% of revenues compared to 37.7%.

Income from operations of $146 million decreased 26.8% from $200 million, resulting in operating margin of 15.3% compared to 20.2%. Adjusted income from operations of $161 million decreased 19.7% from $200 million, resulting in adjusted operating margin of 16.8% compared to 20.2%.

Diluted earnings per share of $2.03 decreased 68.1% from diluted earnings per share of $6.36. Adjusted diluted earnings per share of $2.29 decreased 9.1% from $2.52.

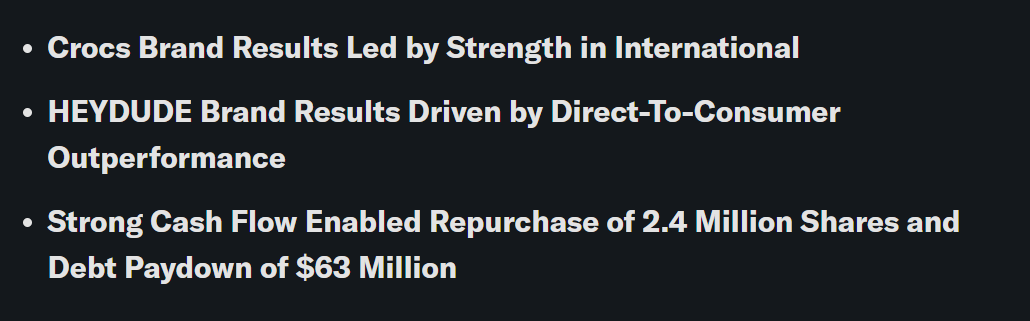

During the quarter, we repurchased approximately 2.2 million shares for $180 million at an average share price of $83.63. We repaid $90 million of debt.

2025 Operating Results (Compared to Last Year)

Consolidated revenues were $4,041 million, a decrease of 1.5%, or 1.7% on a constant currency basis. DTC revenues grew 3.3%, or 2.9% on a constant currency basis. Wholesale revenues decreased 6.2%, or 6.2% on a constant currency basis.

Gross margin was 58.3% compared to 58.8%. Adjusted gross margin decreased 50 basis points to 58.3% compared to 58.8%.

SG&A of $2,208 million increased 59.0% from $1,388 million, and represented 54.6% of revenues compared to 33.8%. The increase in SG&A is largely driven by non-cash impairment charges related to the indefinite-lived HEYDUDE trademark and HEYDUDE Brand reporting unit goodwill of $430 million and $307 million, respectively, during the three months ended June 30, 2025. Adjusted SG&A of $1,456 million increased 6.8% from $1,363 million, and represented 36.0% of revenues compared to 33.2%.

Income from operations of $150 million decreased 85.4% from $1,022 million, resulting in operating margin of 3.7% compared to 24.9%. The decline is driven by asset impairments, as described above. Adjusted income from operations of $901 million decreased 14.2% from $1,050 million, resulting in adjusted operating margin of 22.3% compared to 25.6%.

Diluted loss per share of $1.50 decreased 109.4% from diluted earnings per share of $15.88. The loss per share is driven by asset impairments, as described above. Adjusted diluted earnings per share of $12.51 decreased 5.0% from $13.17, which excludes non-GAAP adjustments.

During the year, we repaid $128 million of debt. We repurchased approximately 6.5 million shares for $577 million at an average share price of $88.68, and at year-end, $747 million of share repurchase authorization remained available for future repurchases.

Fourth Quarter 2025 Brand Summary (Compared to the Same Period Last Year)

Crocs Brand: Revenues increased 0.8% to $768 million, or decreased 0.4% on a constant currency basis.

Channel

DTC revenues increased 6.1% to $475 million, or 4.8% on a constant currency basis.

Wholesale revenues decreased 6.7% to $294 million, or 7.7% on a constant currency basis.

Geography

North America revenues decreased 7.4% to $436 million.

International revenues increased 14.1% to $332 million, or 11.0% on a constant currency basis.

HEYDUDE Brand: Revenues decreased 16.9% to $189 million, or 17.5% on a constant currency basis.

Channel

DTC revenues were flat at $133 million.

Wholesale revenues decreased 40.5% to $56 million, or 41.7% on a constant currency basis.

2025 Brand Summary (Compared to the Last Year)

Crocs Brand: Revenues increased 1.5% to $3,326 million, or 1.3% on a constant currency basis.

Channel

DTC revenues increased 3.4% to $1,726 million, or 2.9% on a constant currency basis.

Wholesale revenues decreased 0.5% to $1,599 million, or 0.5% on a constant currency basis.

Geography

North America revenues decreased 6.8% to $1,710 million, or 6.7% on a constant currency basis.

International revenues increased 11.9% to $1,616 million, or 11.2% on a constant currency basis.

HEYDUDE Brand: Revenues decreased 13.3% to $715 million, or 13.5% on a constant currency basis.

Channel

DTC revenues increased 2.9% to $379 million, or 2.8% on a constant currency basis.

Wholesale revenues decreased 26.3% to $336 million, or 26.5% on a constant currency basis.

Balance Sheet and Cash Flow (December 31, 2025 as compared to December 31, 2024)

Cash and cash equivalents were $130 million compared to $180 million.

Inventories were $369 million compared to $356 million.

Total borrowings were $1,231 million compared to $1,349 million.

Capital expenditures were $51 million compared to $69 million.

Financial Outlook

First Quarter 2026

For the first quarter of 2026, we expect:

Revenues to be down approximately 5.5% to 3.5% to the first quarter of 2025, at currency rates as of February 9, 2026.

Crocs Brand to be down approximately low-single-digits to the first quarter of 2025.

HEYDUDE Brand to be down approximately 18% to 15% to the first quarter of 2025.

Adjusted operating margin to be approximately 21.5%.

Adjusted diluted earnings per share to be in the range of $2.67 to $2.77.

Full-Year 2026

For 2026, we expect:

Revenues to be down approximately 1% to up slightly compared to full-year 2025, at currency rates as of February 9, 2026.

Crocs Brand to be approximately flat to up 2% compared to full-year 2025.

HEYDUDE Brand to be down approximately 9% to 7% compared to full-year 2025.

Non-GAAP adjustments to be approximately $25 million primarily associated with supply chain optimization and other cost savings efficiencies.

Adjusted operating margin to expand modestly from 22.3%.

GAAP effective tax rate to be approximately 23% and adjusted effective tax rate to be approximately 18%.

Adjusted diluted earnings per share to be in the range of $12.88 to $13.35. Adjusted diluted earnings per share guidance does not assume any impact from potential future share repurchases.

Capital expenditures of $70 million to $80 million.