Consti’s results are out, not exactly causing cheers, although revenue is indeed growing, the order book has decreased. It’s also worth noting that the dividend ex-date is today, meaning one had to own shares yesterday to be entitled to it: Consti Oyj osavuosikatsaus 1.1.-30.9.2025 - Inderes

REVENUE GREW, OPERATING PROFIT AT A REASONABLE LEVEL

Key events 7–9/2025 (comparable figures 7–9/2024 in parentheses):

Revenue 90.8 (86.0) million euros; growth 5.6 %

EBITDA 4.0 (4.4) million euros and EBITDA margin 4.4 % (5.1 %)

Operating profit 3.1 (3.4) million euros and operating profit margin 3.5 % (3.9 %)

Order book 239.9 (250.4) million euros; change -4.2 %

New orders 41.2 (64.8) million euros; change -36.4 %

Free cash flow 3.4 (1.7) million euros

Earnings per share 0.30 (0.31) euros

Key events 1–9/2025 (comparable figures 1–9/2024 in parentheses):

Revenue 241.2 (234.4) million euros; growth 2.9 %

EBITDA 8.1 (9.7) million euros and EBITDA margin 3.4 % (4.1 %)

Operating profit 5.5 (6.6) million euros and operating profit margin 2.3 % (2.8 %)

New orders 206.4 (191.9) million euros; growth 7.6 %

Free cash flow 5.9 (2.4) million euros

Earnings per share 0.49 (0.58) euros

Guidance for the Group’s business outlook for 2025 (unchanged):

Consti estimates that its full-year 2025 operating profit will be 9–12 million euros.

It should also be added that free cash flow was at a good level, so one can and dares to wait for an improvement in the economic cycle. Indebtedness is at a very low level. The dividend yield will remain strong.

Consti fell short of profitability expectations and it seems it might not improve in the coming quarters:

“Our third-quarter profitability was negatively impacted by the prolonged downturn in construction, the investments made in tendering and negotiation activities to secure our order book, and the continued low revenue and profitability level of our Service business.”

Here are some quick comments from Ate on the Q3 results.

Consti’s revenue moderately exceeded our forecast, while profitability was clearly weaker than we expected. The weakness in profitability was mainly due to the still challenging market situation. Consti’s order book decreased slightly compared to the reference period, but remained at a strong level. Despite this, the decreased order book combined with the persistently weak market situation puts pressure on our short-term forecasts.

The hardworking proletarian of the Ruoholahti cooperative, Atte, has made a new company report

Consti’s Q3 result fell short of our forecasts, as challenges in the company’s service business weakened the result even more strongly than anticipated. In addition, the competitive situation in the renovation and repair construction market has remained tight. We do not expect an improvement in the situation during the rest of the year, and following forecast revisions, our estimate for the current year’s operating profit is approaching the lower end of the guidance range. We also do not rule out the possibility of an earnings warning later in the year. In our view, a clearer improvement in results and the realization of the stock’s potential require a turnaround in market conditions. Nevertheless, we remain positive on the stock, considering its moderate valuation and strong dividend yield supporting return expectations. We reiterate our ‘add’ recommendation and lower the target price back to 11.0 euros (previously 11.75 euros).

Senate Properties has selected Consti as the service provider for the construction of the Government Palace building project

Senate Properties has selected Consti Korjausrakentaminen Oy, a subsidiary of Consti Oyj, as the service provider for the construction of the Government Palace building project.

The total cost estimate for the project, to be implemented with the spearhead project alliance model, is approximately 195 million euros.

Construction work is scheduled to begin in autumn 2026 according to the preliminary timetable and conclude during 2030.

The procurement decision is legally binding after the appeal period under the Procurement Act has ended.

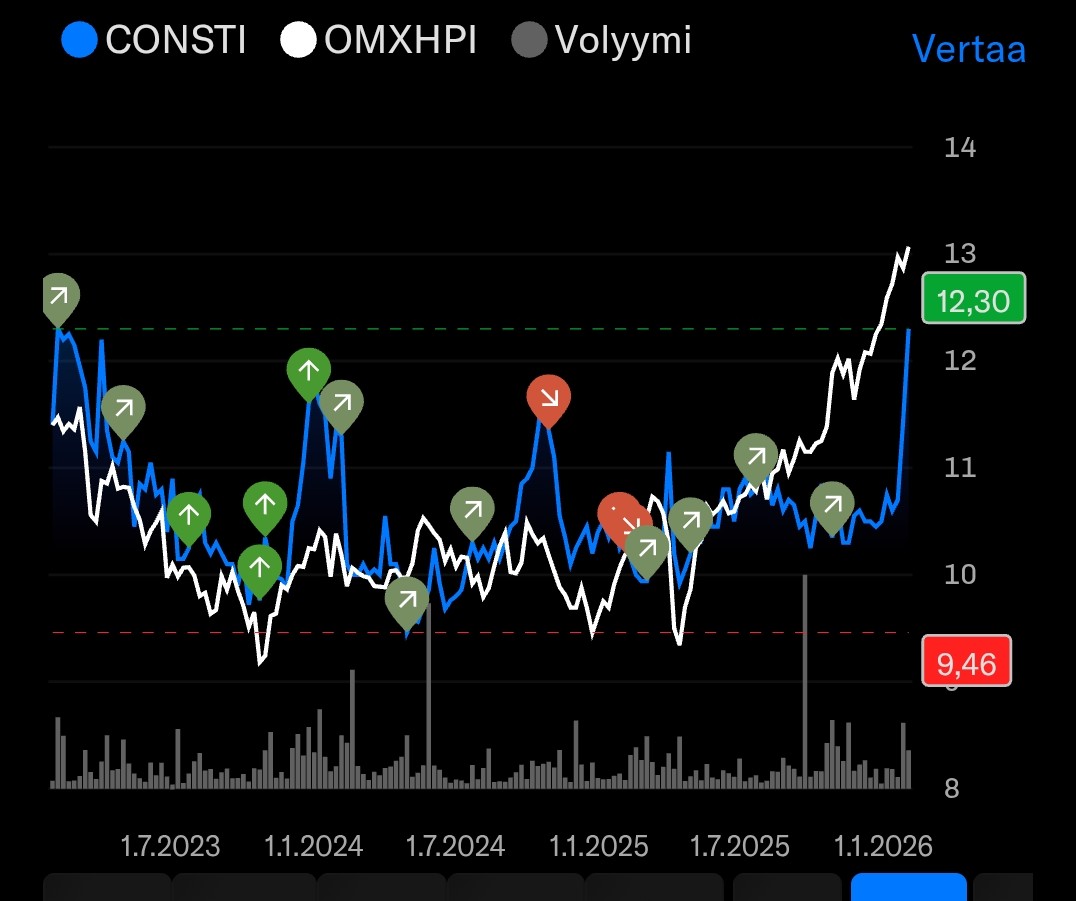

I own Consti and the stock has risen over 16% within a week without any news, or at least I haven’t found any. I wonder if some people know more than others

On Sunday, Arvopaperi hyped Consti, added it to its model portfolio, and highlighted a “7 percent dividend yield” in the headline. It likely got buyers moving.

I’m no technical analysis expert, but buying near ten and selling at 12 has been a good rule of thumb for a long time for a dividend payer that’s stable relative to its sector.

@Atte_Jortikka, you wrote this morning: “In our view, Consti’s valuation multiples of 9x EV/EBIT and 12x P/E, based on our estimates for the current year, represent a more neutral level.”

In the latest comprehensive report from March 3, 2025, @Olli_Koponen wrote: ”The valuation range we accept based on the grounds mentioned above is: EV/EBIT: 10–14x”.

According to the range in the comprehensive report, Consti should still be cheap. So, has the ”accepted range” changed this much in a year, or is there a difference of opinion between the analysts?

Hi, if I return to that comprehensive report: ”The valuation range we accept based on the aforementioned grounds is: EV/EBIT: 10–14x, P/E: 10–14x.”. I don’t particularly disagree with that acceptable valuation range. However, in my view, the upper end of the range (14x) would require a significantly stronger growth outlook for the company than the current one. Based on current forecasts for 2026, EV/EBIT indeed drops to around 9x and P/E to 12x levels. As I stated in the report, these levels are overall more neutral compared to, for example, the valuation based on fiscal year 2025 forecasts, and also in relation to that accepted range. With the updated target price, EV/EBIT and P/E will fall to approximately 9x and 11x levels in 2026–2027, which overall settles roughly at the lower end of the range. In my opinion, this is justified at this stage, considering the uncertainty related to the forecasts for the coming years.

Consti and Senate Properties have signed a spearhead project alliance agreement for the Government Palace block construction project

Consti PLC’s subsidiary Consti Korjausrakentaminen Oy (“Consti”) and Senate Properties have signed an agreement for the implementation of the renovation and expansion of the Government Palace. The total cost estimate for the project, to be carried out using the spearhead project alliance model, is approximately 195 million euros.

Well, now some news has come out (Senate deal). Maybe someone knew this in advance, but how on earth can you prove it when at the same time there’s been that hype from Arvopaperi.

Consti will publish its financial statement release for 2025 on Friday, February 6, 2026. We forecast that revenue and operating profit grew slightly in Q4 compared to the comparison period, and for the full year, the result remains at the lower end of the guidance range in our forecasts. We expect growth to remain slow for next year, but relative profitability to improve due to, among other things, efficiency measures. As the risk of a profit warning has dissipated, we rely more heavily on the future in setting the target price and raise our target price to EUR 12.5 (previously EUR 11.0). However, due to the recent share price rise, the valuation picture has turned neutral even in the slightly longer term, and thus we lower our recommendation to Reduce (previously Accumulate).

This will amount to ~half a year’s revenue. As long as this doesn’t turn into St. George the Second, this is absolutely fantastic news! Thanks to Inderes (?), the share price dropped significantly yesterday, so I just had to load up.

I’m wondering the exact same thing – the share price has practically gone nowhere for 30 months, and then a month ago it suddenly rose +20% in a month, without any news.