Constellation Software Inc. ![]()

Constellation Software (abbreviated as CSI, ticker CSU) has been one of the most successful serial acquirers of software companies in recent decades. The company’s ability to disciplinedly reinvest growing cash flows with excellent returns has also shone through in shareholder returns: at the time of writing, the company’s stock has returned approximately +16,000% since its 2006 IPO.

Some figures:

Market Cap: ~46B USD

Revenue: 11.6B USD

FCF2S: 1.7B USD

Stock Price: 2936 CAD

Shares Outstanding: 21.2 million

EV/FCF2S (the company’s reported free cash flow relative to enterprise value, adjusted for accounting headaches): 22x

CSI was founded by venture capitalist Mark Leonard in 1995. Mark avoids the spotlight, so this “Gandalf picture” is mostly what circulates about him online.

CSI’s business model is simple on paper but difficult to execute in practice.

CSI’s strategy is to buy vertical market software (VMS) niche companies for permanent ownership, i.e., companies whose software product solves a specific problem for the customer. For example, an ERP system.

Common features in the acquired companies include their business-criticality to the customer, a small target market (TAM might be as little as five million dollars), and limited competition. Frequently mentioned customers in investor blogs include hospitals, district courts, the public sector in general, funeral homes, media, retail, etc.

This legendary image circulates online as an example of CSU’s software for the Seattle court system. ![]()

Software companies generate abundant cash flow and do not have large investment needs. This feature is essential, as it allows their cash flows to be maximally reinvested into new acquisitions.

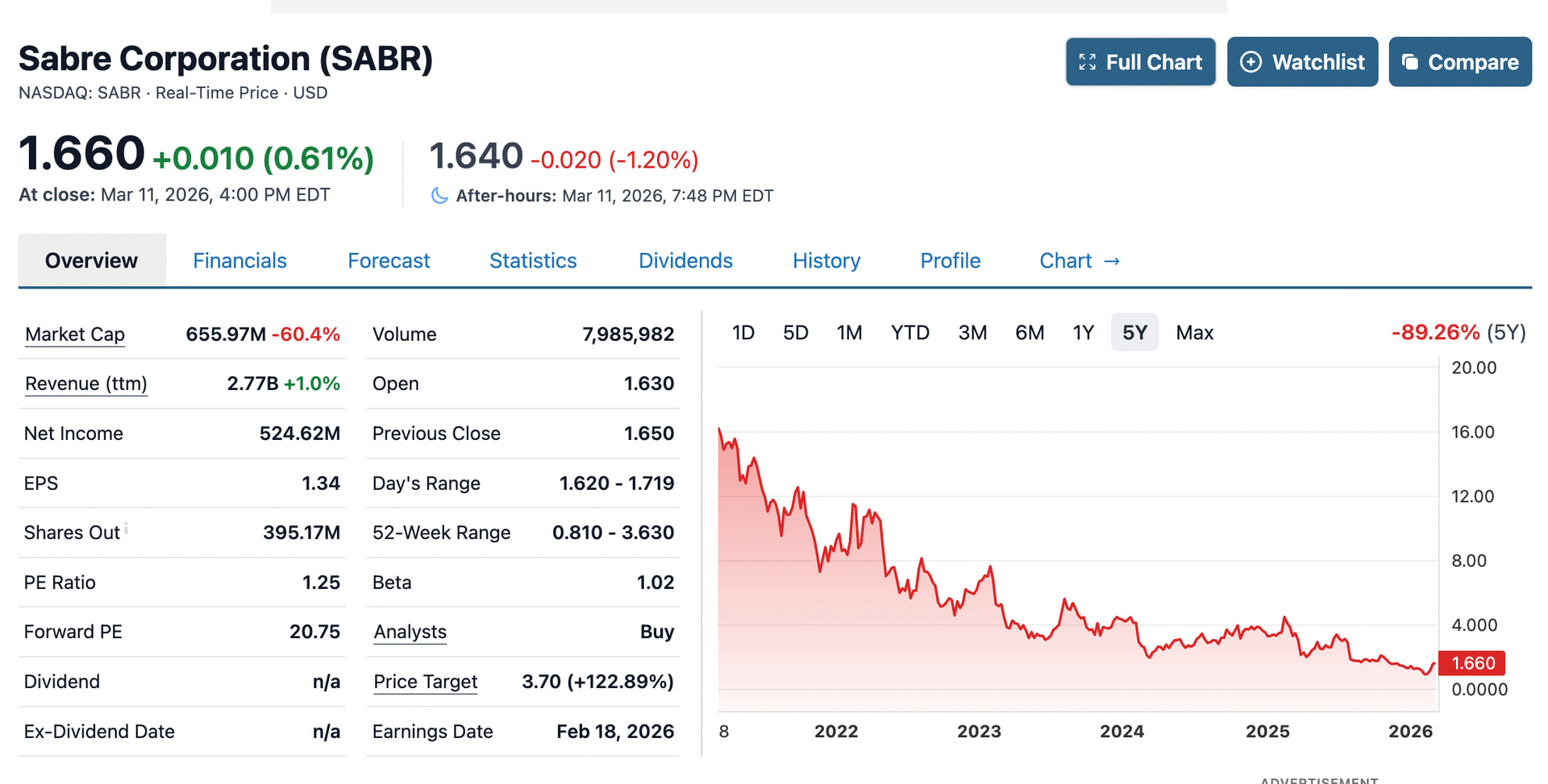

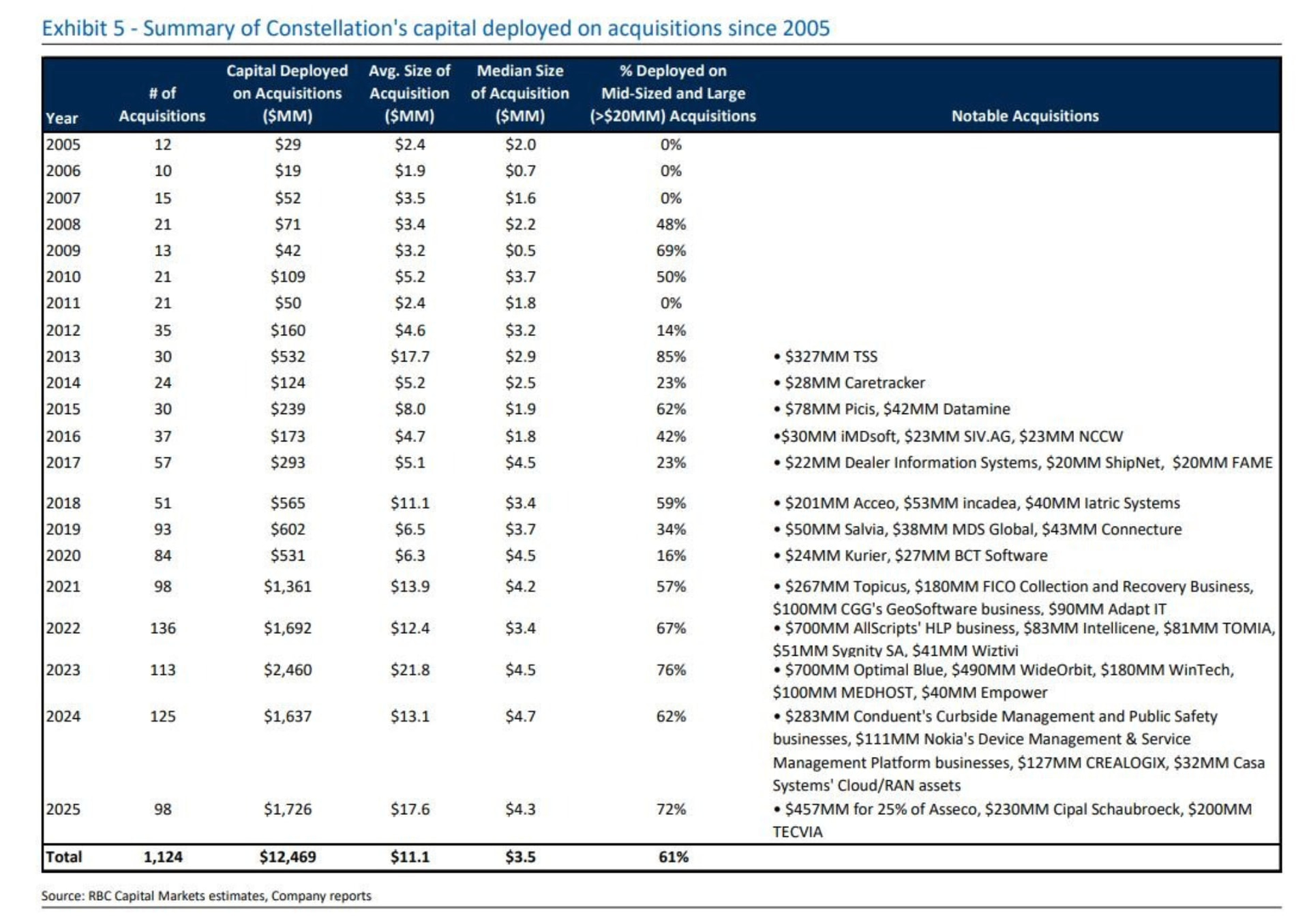

CSI is a disciplined buyer: according to various estimates, its annual hurdle rate is 30% for small targets and 15% even for larger acquisitions. Historically, the company has grown by buying huge numbers of small companies, but in recent years, due to its increased scale, the company has also started making deals worth hundreds of millions of dollars. For example, CSI recently invested in the listed company Sabre. CSI talks about a PEMS strategy, or “Permanent engaged shareholder strategy,” where the company aims to favorably influence the company’s development as an owner.

During its listing history from 2006–2025, the company’s revenue per share has grown from ten to 550 dollars, or just under 24% per annum. The share count was nailed to the current level of 21.2 million after the IPO, and the company has not used significant debt. Growth has therefore been achieved solely by reinvesting abundant cash flow while disciplinedly sticking to a high hurdle rate!

The second pillar of the company’s strategy is a deeply implemented model of decentralized decision-making. Even in the early years, Mark Leonard realized he couldn’t make all capital allocation decisions. Thus, this power has been gradually decentralized down the organization. In addition, Constellation’s hierarchy has been kept flat.

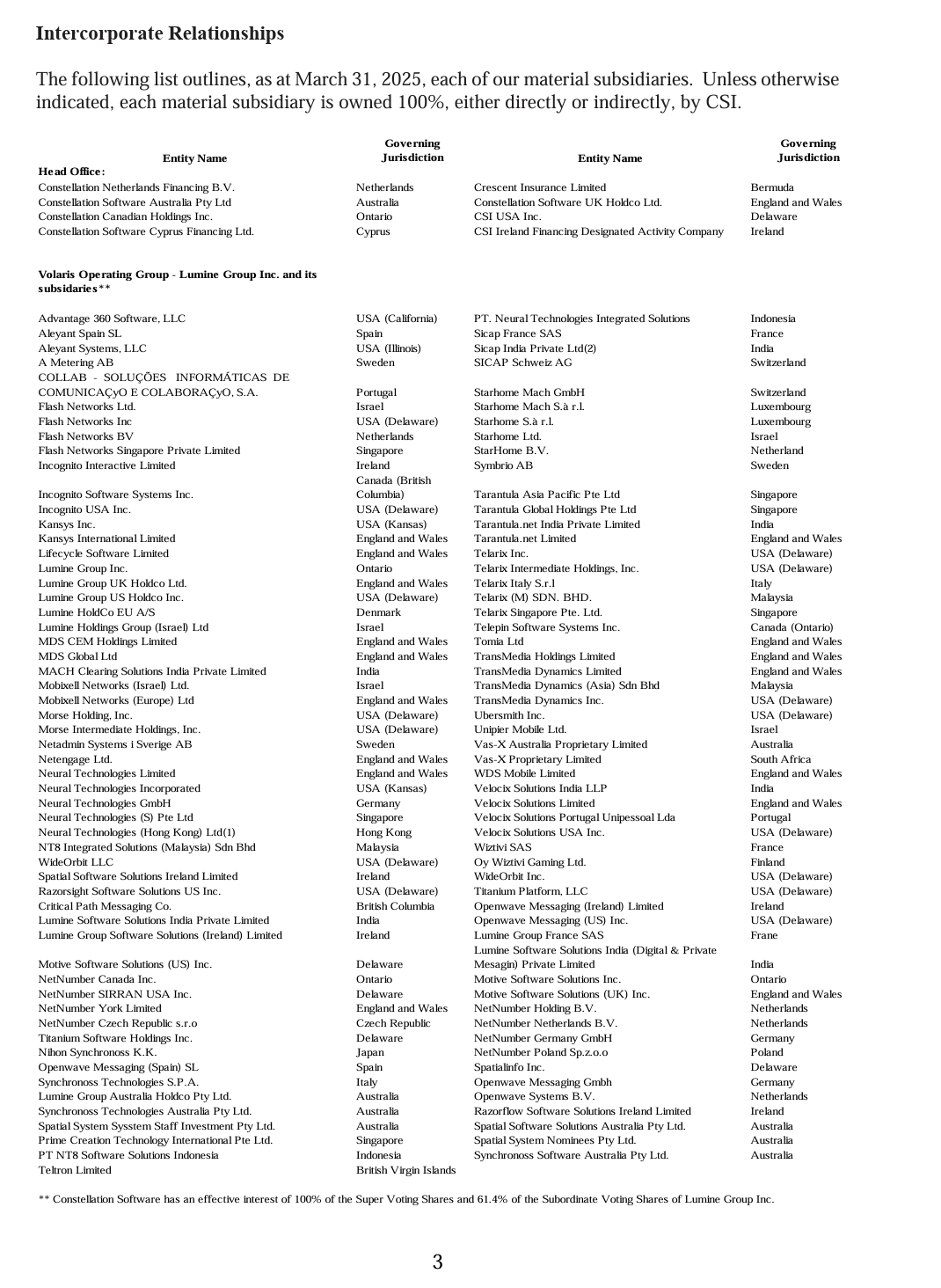

The company is divided into six operating groups. One is even separately listed on the stock exchange: Topicus. Then there is the even more independent Lumine, which was spun out from the Volaris group, also to the stock exchange. For instance, Volaris itself is further divided into several operating groups. Breaking business units into agile, smaller units is clearly a core concept within CSI!

Incentives for managers are clear: achieve an excellent return on the massive cash flows. I.e., maintain high return on invested capital while simultaneously growing. Growth must be achieved without compromising returns. Cash bonuses must largely be reinvested into CSI shares on the open market.

In my opinion, several factors support CSI’s longevity and competitive advantages. First, a disciplined culture and incentive model honed over decades. Entrepreneurs seeking quick wins are unlikely to even apply to such a firm. Second, CSI acknowledges that technological change is rapid and unpredictable. That’s why it buys niche businesses with high switching costs. Third, the company can operate in fields that don’t attract too much competition due to their small size, because it has decentralized capital allocation decisions. The best proof of these is the company’s historical track record. Since the company owns over 1,000 companies and makes even over a hundred acquisitions a year, following individual companies is madness. Instead, an investor can track the development of the company’s organic growth and conservatively reported free cash flow. Free cash flow must grow over time. If, on the other hand, organic growth turned into a decline at the total business level, the wheel would be spinning in the wrong direction. Note: in individual cases, Constellation may buy declining businesses if they can be had cheaply enough.

The company’s numbers can be confusing for an investor getting to know the company: reported earnings look small because they are weighed down by amortization of intangibles related to acquisitions. Earnings are reported in US dollars, but the stock is in Canadian dollars. The company is tight-lipped in its reports, and regular CEO letters ended in 2017 because the company’s competitors were copying CSI’s every move. Additionally, an odd “IRGA / TSS membership liability revaluation charge” appears in the papers, which is essentially a call option to buy Topicus entirely under CSI. For some reason, this theoretical cost is deducted from the company’s reported FCF2S cash flow, even though it is only an accounting matter. Therefore, I adjust it out of the free cash flow myself.

The biggest risks for CSI include its increased size: the core question for an investor is, how long can CSI reinvest its cash flows at excellent returns exceeding the hurdle rate? Copycats abound from Private Equity to “discount Constellations” like Sweden’s Vitec. Personally, I believe there is still enough runway, as the company has first-mover advantage and a good reputation as a permanent home for companies. But the law of large numbers is starting to weigh in. For example, at a 15% growth rate, the company’s revenue would double to 24 billion dollars in 2031. Currently, the global size of the VMS market is estimated to be somewhere in the ballpark of 150 billion dollars. Everyone can consider how large CSI can grow in this VMS land of thousands of small ponds.

Some investors have also been stressed by the legendary Mark Leonard stepping down from the CEO position last fall for health reasons. However, his successor, Mark Miller, has been with the firm for 30 years: he joined with CSI’s first acquisition, the transit software firm Trapeze in 1995, and he led the Volaris group successfully for years. Additionally, Mark Leonard was involved in, for example, the latest Sabre investment. Due to the company’s decentralized operating model, I do not consider key person risks to be excessive.

The share price has also been hammered by investors’ AI fears. The company itself commented last fall that it is still early to assess the impact of AI on VMS businesses. They have already survived several technological disruptions over the decades, such as the internet and SaaS. Coding becomes faster, but that could also benefit CSI’s programmers. I don’t believe that district courts, hospitals, and funeral homes will start “vibe-coding” their own software. Time will tell.

The valuation is modest for my taste, with the stock trading at 22x free cash flow at the time of writing. Note: this is a realized figure, not a forecast. For a company that has historically created shareholder value, this feels like a modest level.