The volumes are absolutely incredible. Trading has already reached SEK 160 million (EUR 16m) in the first hour. Take Kamux as an example. It has a larger market cap and has traded EUR 100k.

1 Like

Does anyone know if CDON is planning to make a mobile app? It seems somehow absurd that they have no visibility in app stores.

Currently, CDON is giving a “digital real estate” free pass to its competitors. It goes without saying that a customer would rather open, for example, the Etsy or Amazon app than specifically go looking for Cdon online.

1 Like

Tomorrow morning, the annual report will be released at 7:00 a.m., followed by the Q4 presentation a couple of hours later. The recent stock price increase has been so sharp that disappointment will be profound if any weakness appears in the report or comments. I’ll probably take some risk management measures in my own portfolio if it’s another +15% today. It fits my “Cut profits & Let losses run” strategy in an overheated market.

Are there any early reads available or are FVC’s figures the latest guesses?

Hey, I don’t think there’s any analyst coverage for this yet. In any case, I’d focus on these:

-

Marketplace. The company’s own retail business isn’t the long-term game; a strong transformation to the Marketplace business model started in 2018. So, focus on the Marketplace.

-

What numbers then from the Marketplace? By far the most important is GMV (Gross Merchandise Volume). It has grown about 100% YoY every quarter in 2020, and if it suddenly dropped from this, it would be a huge disappointment. In addition, it’s worth tracking:

-Number of third-party sellers

-Number of active users

-Number of web visits to the platform -

Cost structure. It’s probably best to completely forget COGS (Cost of Goods Sold) because the company’s own retail business is almost insignificant. Instead, SG&A (Selling, General & Administrative expenses) is important, and the business should show strong signs of scalability.

-

Management presentation. A video presentation available to everyone in English. Everyone surely knows how important management is (Efecte, Kamux, Qt, etc.).

14 Likes

Report out:

A bit of a disappointment for me. GMV growth “only” 60% in Q4. The positive is that the number of third-party sellers continues to grow. Just over 1000 in Q4 2019, 1385 in Q3 2020, and now over 1500. Also, many visits to the site, which is likely influenced by the IPO. What will the stock do then… hard to say. This case involves many foreign institutional investors, deep-value investors, and growth investors. As I said, I was left with a slightly lukewarm feeling, mainly due to GMV growth. Three quarters of > +100% before this…

11 Likes

I don’t know if anyone else listened to the presentation, but this big American investor, Adam Wyden, managed to turn the stock price around during the call. He really boosted the narrative as much as he could ![]() No wonder, since he owns 6% of the entire company

No wonder, since he owns 6% of the entire company ![]()

6 Likes

He’s probably selling his own shares with a sweat on his brow ![]()

This is way too expensive for me, and I don’t really see why that market value would be justified. The “moats” are probably quite small and their website is relatively poor. If he were to present that valuation on Shark Tank, someone might comment that a better platform could surely be built with a few million euros and, for example, a 100M€ marketing campaign could get quite a bit of visibility. Why pay a few hundred million extra? The company has an operating profit of just over 5M€ and a slightly negative result, with a market value of 350M€. There’s still a lot to do if it intends to be the Amazon of the Nordics… it might be that the real Amazon will still compete quite strongly with its logistics. Time will tell, I don’t really have enough faith, but the market clearly believes.

1 Like

Quite a day for CDON! The share price went down about -25% and is now in the green?

This morning I regretted not cashing out my shares in time, but something is creating quite a lot of upward pressure on the valuation.

Feel free to flag this, but I’ve been waiting too long for @Aston_Livingstone’s take, so I just had to ping them ![]()

25% was just a warm-up…haven’t we already risen nearly 50% from there? The rise today and yesterday was largely due to CSV. When you notice that broker entering the buy side, it’s probably worth taking a small swing. https://twitter.com/Hex_Hermoilija/status/1356661809810440196

Same guy in 2017: ![]()

8 Likes

SEB TP 850 SEK

https://twitter.com/finwiresmallcap/status/1360139173726986242?s=21

Aston sold too early at 460-470 SEK levels when he doubled up. Not good ![]()

![]()

1 Like

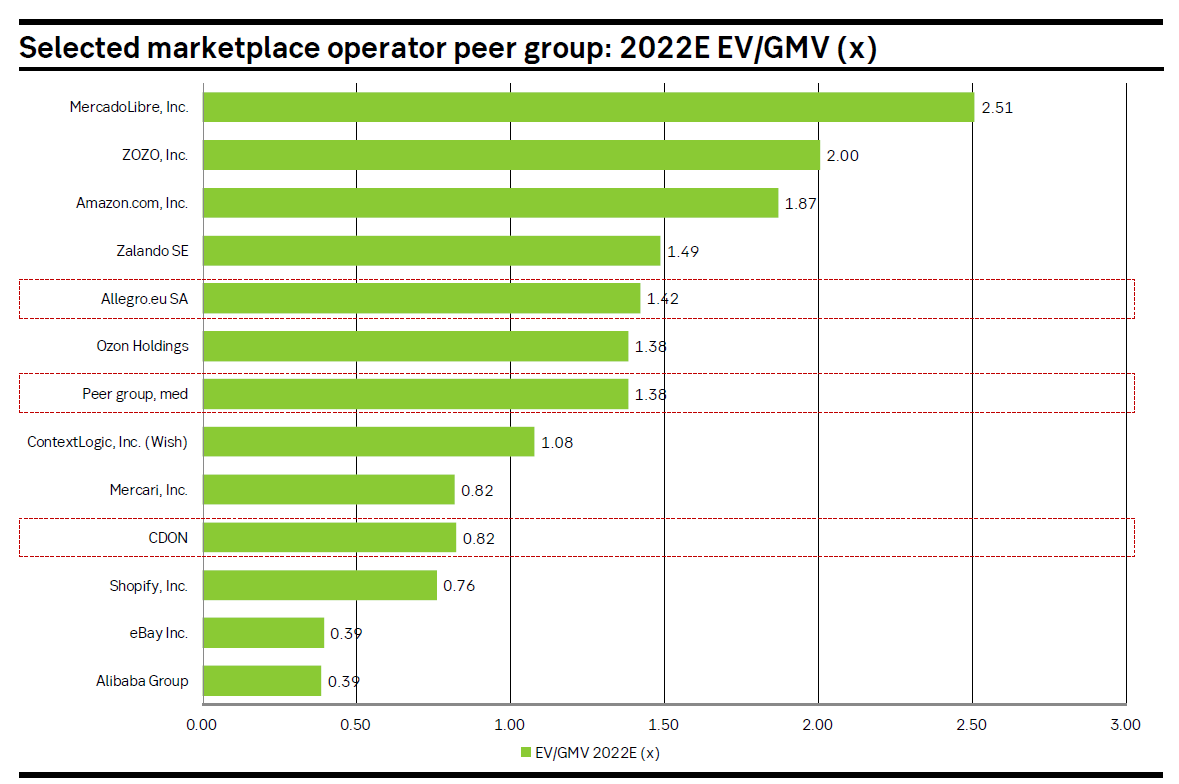

The valuation is based on the idea that the business should be valued at the EV/GMV 2022E level of its peers. So about 1.4x. I came across it somewhere ![]()

2 Likes

The company is trading today at approximately 10x 2023E EV/Marketplace sales. This is roughly the same as Qt 2023 EV/sales. In my opinion, Qt has better margin potential in the long term, and also very good visibility for the next 3 years. In summary, in my opinion, at the current price, CDON is no longer a “bargain” and expectations for the coming years are largely priced in.

20 Likes

Can it be concluded from this that Arimatti is no longer in the ride? One could infer from the forum’s silence that the odds have already scared off quite a few to just watch the rise from the sidelines. I don’t dare to be in with my whole pot anymore either, but I’m still hanging in for a laugh. Many investors must have immense faith for the stock to keep reaching new highs. Flag it if this is just unnecessary spam in the message flood ![]()

3 Likes

Let’s just say that if the company had a very heavy weighting in my wife’s portfolio on January 12th, it has been significantly lightened since then. Too early, even.

An American investor, who was very active during the Q4 call, has recently acquired over a 14% holding in CDON as a whole. It will be interesting to see what Adam Wyden achieves. There was an article about him in the Graham & Doddsville letter in spring 2016.

7 Likes

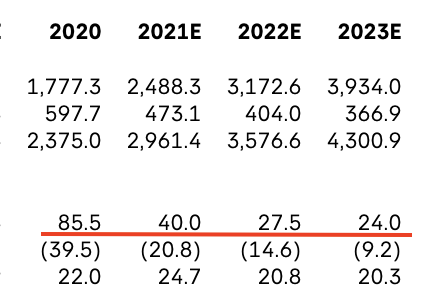

Here is a GMV growth forecast for the coming years (percentages) taken from SEB’s analysis.

Based on SEB’s target price, the stock is starting to be quite fully priced. However, the target price is based on the median GMV multiple of 2022E peers (1.4x).

It would be interesting to hear what the forum thinks of these growth forecasts. Do you think the analysis is conservative? Anyone can read it for free on CDON’s IR pages. ![]()

1 Like