Pitänyt tämä avata aiemmin ja @jaska1 on painostanut niin paljon että pistetään tulille ![]()

Eli Carvana (Tickeri CVNA) on Yhdysvaltalainen yritys, joka myy 100% verkkokaupan kautta käytettyjä autoja. Itse olen ollut Carvanan kyydissä osakkeenomistajana jo pidemmän aikaa ja sitä kautta seurannut yrityksen kehitystä.

Mikä tekee minun mielestäni Carvanasta mielenkiintoisen sijoituskohteen?

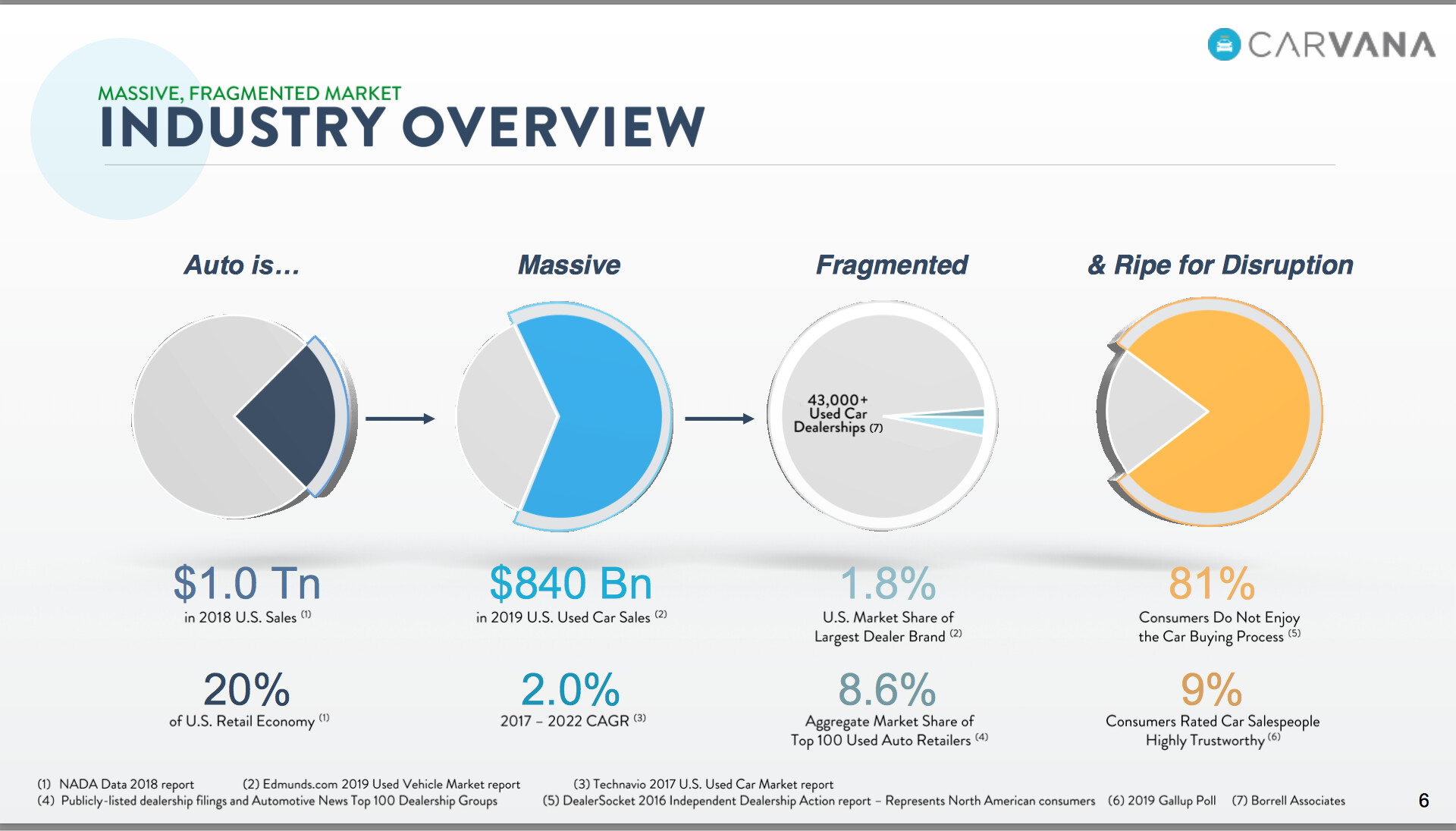

-Distruptoivat valtavaa käytettyjen autojen markkinaa joka on äärimmäisen fragmentoitunut

-Käytettyjä autoja myydään melkein 900 miljardilla vuodessa Yhdysvalloissa ja suurimman myyjän markkinaosuus (Lokakuu 2020 tieto) oli muutaman prosentin luokkaa !

-Valtaosa autokaupasta tehdään perinteiseen tapaan fyysisissä autokaupoissa mutta verkko-ostaminen kasvaa huomattavaa vauhtia

-Carvanan visio on mullistaa tämä jähmettynyt rakenne ja tulla digitaalisen aikakauden johtavaksi autokauppiaaksi joka rakennetaan puhtaasti digitaalisen maailman ehdoilla

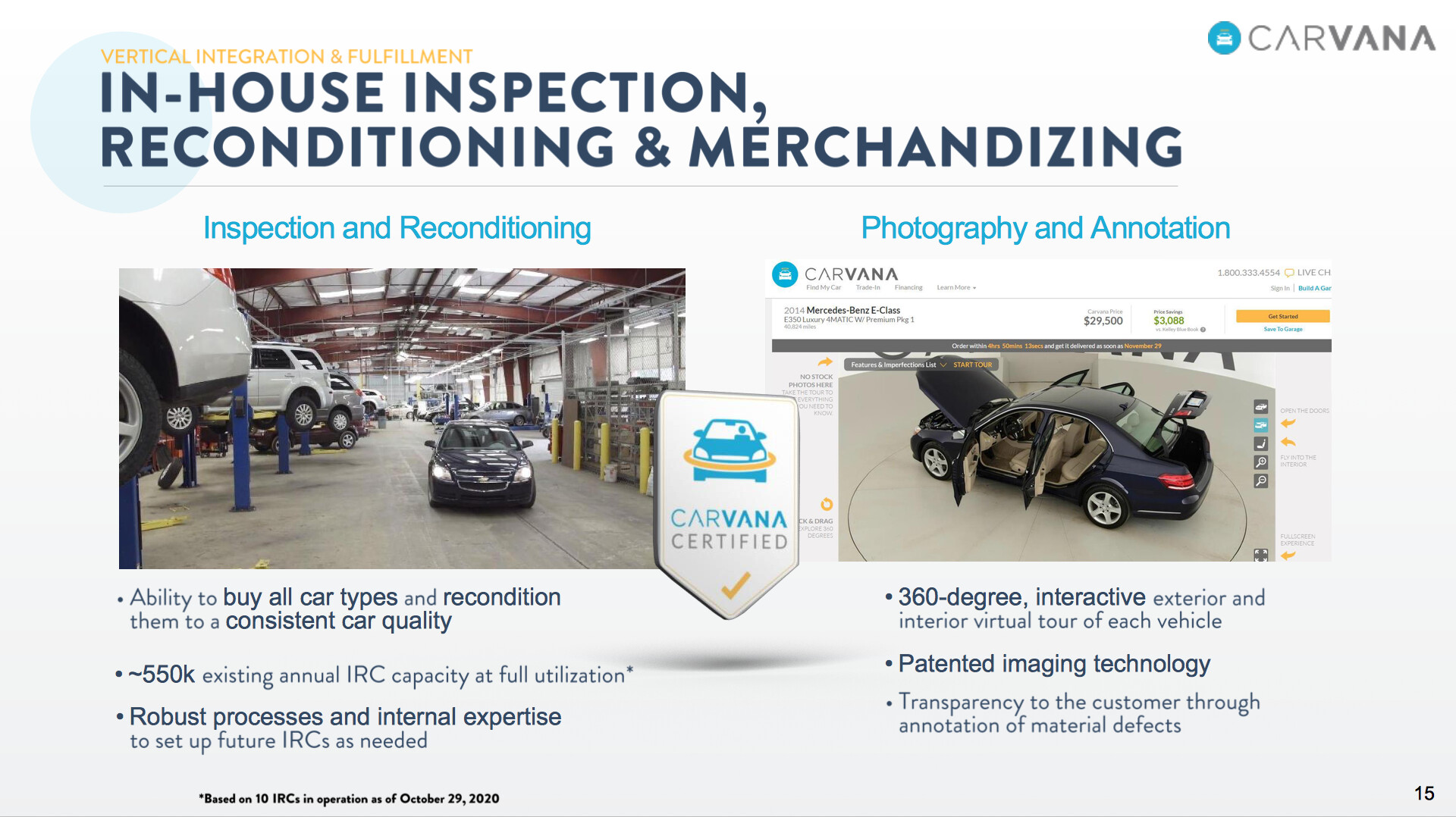

-Carvana tarjoaa ainutlaatuisen ostokokemuksen jossa ostat verkkokaupasta ja Carvana toimittaa autosi sinulle kotiovellesi viikon sisällä viimeistään. Tässä välissä auto on käynyt ja tutkittu Carvanan omassa autojen tarkistuskeskuksessa. Ostajalla on ilmainen palautusoikeus ostokselle.

-Yhdysvalloissa autokauppialla ei ole järinkään hyvä maine. Moni vihaa kauppoihin menevistä ja pelkää tulevansa huijatuksi. Se että voi ostaa netistä, tietää että auto on tarkistettu ja voit palauttaa poistaa todella monia kitkoja ostajalta.

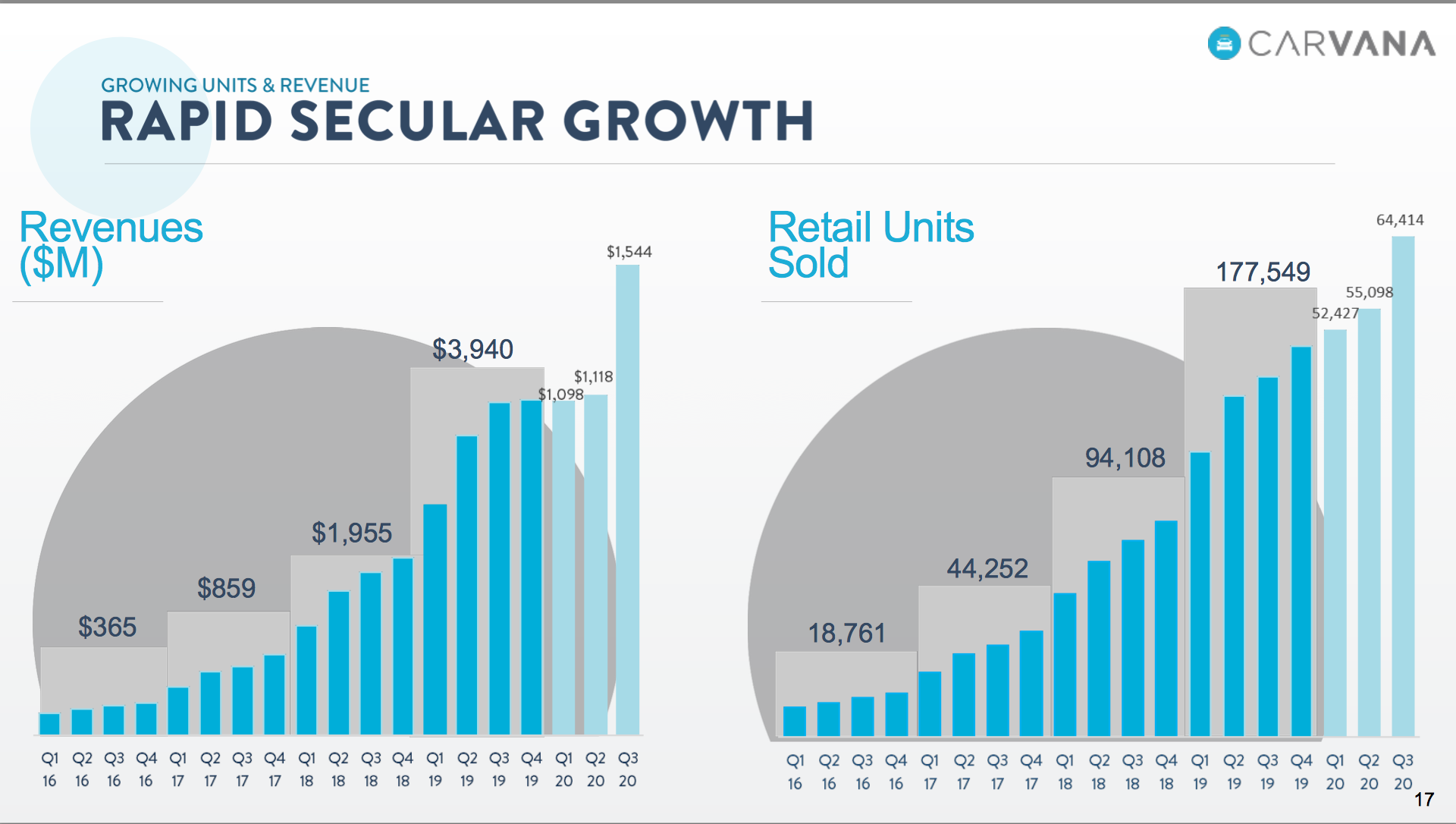

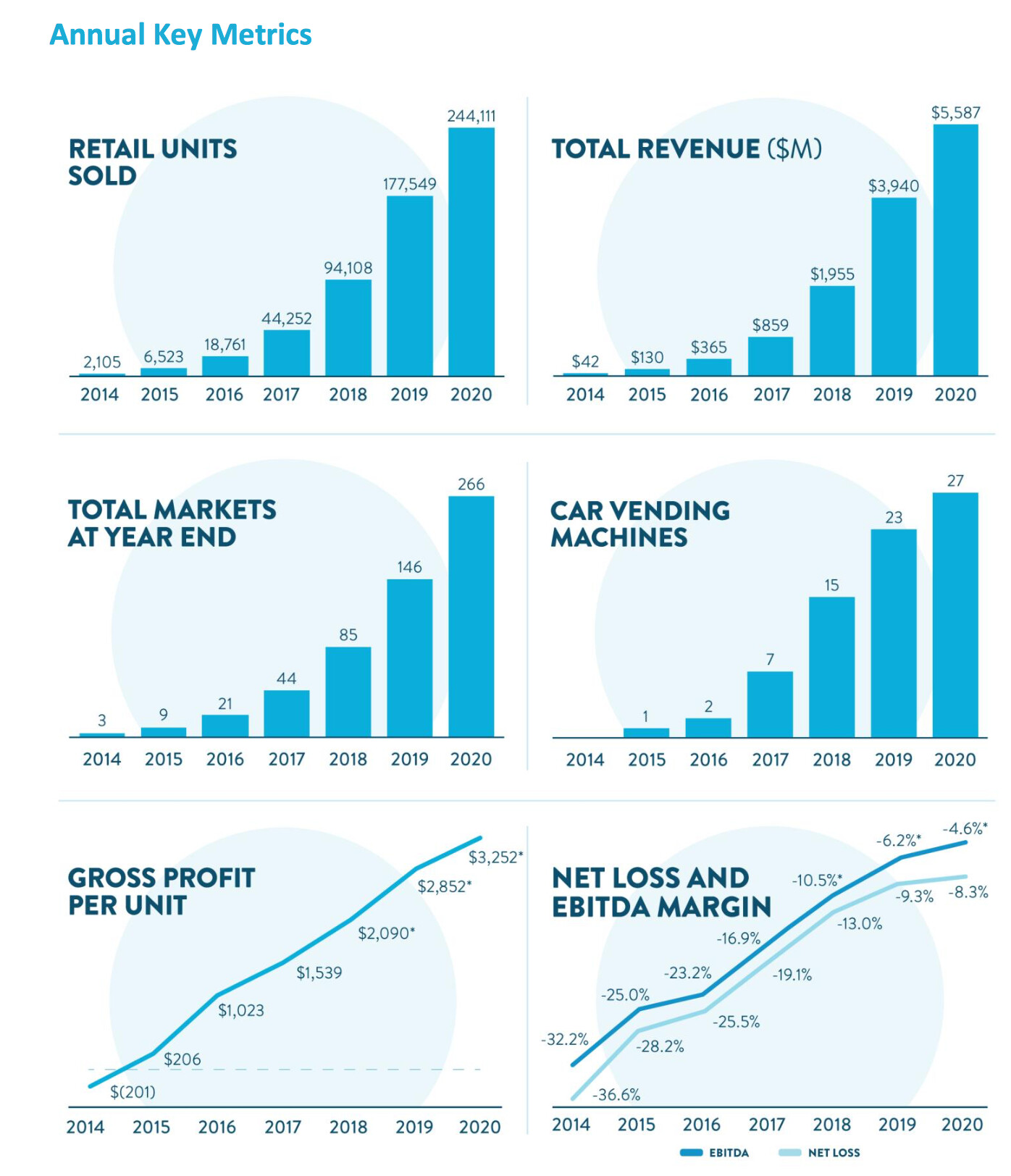

-Carvana on kasvanut erittäin nopeasti jo useamman vuoden, yli 100% kasvuvauhtia, tosin 2020 ei tulla pääsemään ihan siihen tahtiin, liittyen erityisesti koronan vaikutuksiin 2Q:lla. Mutta Q4 voi hyvinkin olla että palataan tuohon triple digit kasvuvauhtiin tai lähelle.

-Uskon että vuosi 2020 tulee olemaan tietyllä tapaa lopullinen läpimurtovuosi Carvanalle. Koronapandemia on tehnyt myös autojen ostamisesta onlinesta valtavirtaa ja ei ole näköpiirissä paluuta vanhaan.

-Carvana etenee oikeastaan kaikissa metriikoissa hyvää vauhtia. Toki yrityksen toiminta ei ole vielä voitollista mutta tälle on ollut syynsä; on haluttu investoida tulevaan kasvuun sen sijaan että optimoitaisiin tulosta tässä hetkessä.

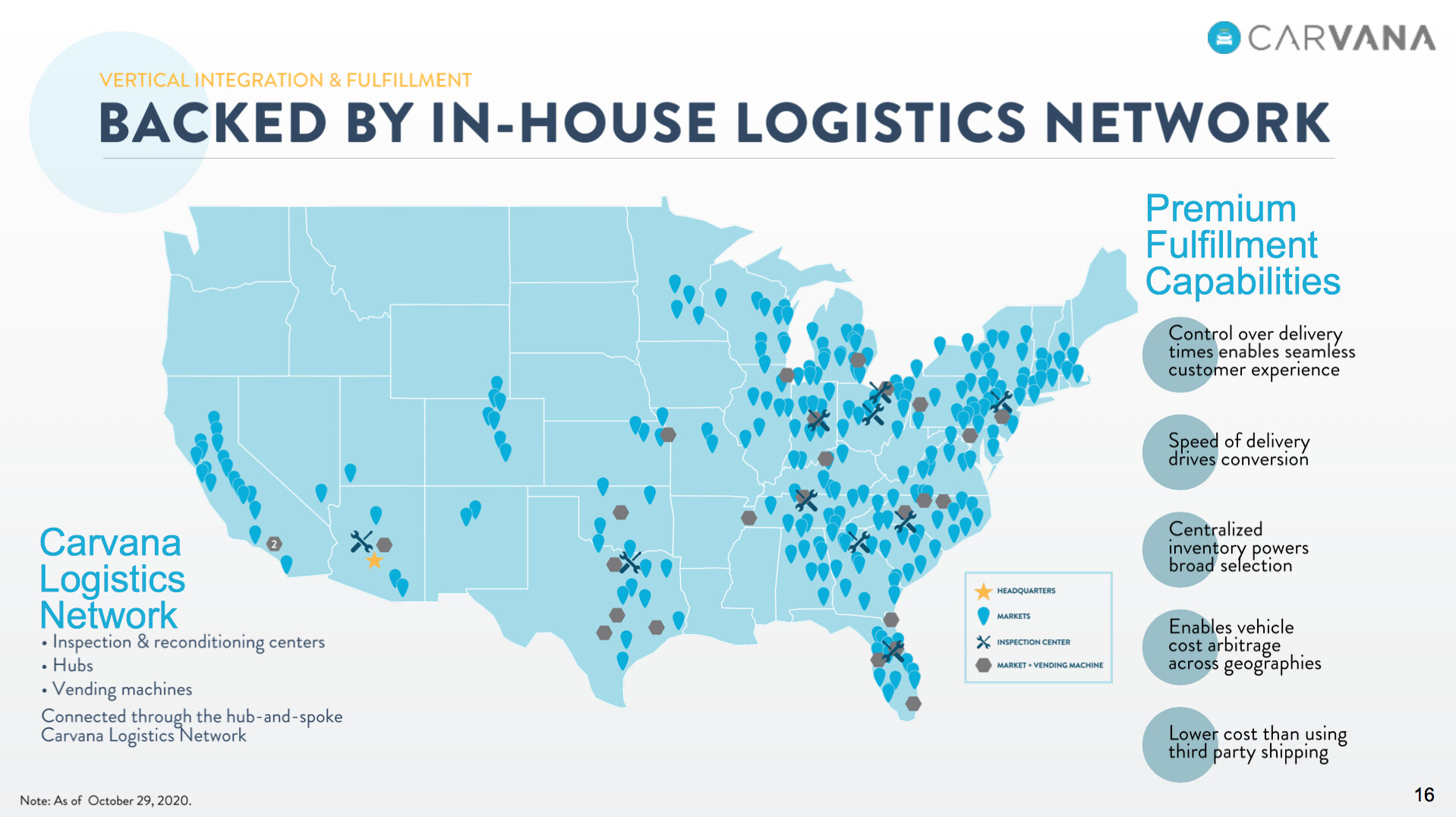

-Carvanan malli on edetä markkina-alue kerrallaan ja kasvattaa jatkuvasti tarjolla olevien autojen määrää lokaalisti. Tärkeä osa tätä on rakentaa tarkistuskeskuksia (Inspection Center) alueittain jota kautta pystytään palvelemaan paremmin asiakkaita.

-Lisäksi nämä investoinnit luovat vallihautaa muita kilpailjoita kohtaan jotka eivät pysty takaamaan ostajille autojen laatuja ja sitä tärkeää luottamusta että auto jonka ostavat on tarkistettu ja kunnostettu. Tämä poistaa yhden merkittävän kitkan ostokokemuksesta.

-Seuraavien 1-2 vuoden aikana uskon että Carvana tulee jatkamaan laajentumista uusille alueille, avaa lisää tarkistuspisteitä ja panostaa lisää koko ostokokemukseen ja luo tunnettavuutta brändilleen maanlaajuisesti

-Yrityksen perustaja ja toimitusjohtaja Ernest Garcia III on intohimoinen asiakaskeskeisyyden vaalija. Tämä näkyy jokaisessa asiassa mitä yritys tekee ja toimii.

-Garcialla on itsellään erittäin paljon ns “skin in the game”, hän omistaa 600 miljoonaa Carvanan osakketta (Eilinen closing price 261 taalaa eli melkoinen potti on pelissä…)

-Carvanan arvostustaso ei ole missään alelaarissa alkuunkaan. Markkina-arvo eilen 44 miljardia ja esim P/S on luokkaa reilu 20. Mutta itse lähestyn tätä sijoituscasea käyttäen Brian Feroldin ja Mats Christiansenin ajattelumallia eli onko yritys markkinoilla jossa on valtava TAM ja voiko yritys kasvaa vuosia jopa vuosikymmeniä ja olla johtava peluri sillä markkinalla.

Näen tämän erittäin mahdollisena Carvanalle, lisäksi tämä vain Yhdysvalloissa, sitten on tietysti mahdollista laajentua jatkossa esim Eurooppaan tai vaikka alkuun Kanadaan. Mutta yritys on johdonmukaisesti sanonut että fokus on nyt täysin Yhdysvalloissa mikä on järkevää koska tosiaan markkina on valtava ja erittäin fragmentoitunut. Sinne mahtuu hyvin kovimmat kilpailijat esim VRoom. Lisäksi kasvuoptioina on laajentaa myyntivalikoimaan esim tuoda mukaan vakuutukset, tästä yritys ei ole itse mitään sanonut tosin, tämä on vain omaa ajattelua.

Tähän perään läjä erilaisia materiaaleja tutustumista varten jos Carvana kiinnostaa. Suosittelen erityisesti kuuntelemaan Mads Christiansenin Carvana Q3 tuloksen läpikäynnin. Mads avaa erittäin hyvin pitkän aikavälin potentiaalia ja minkälaisia vallihautoja nyt rakennellaan.

Viikon vanha haastattelu, Ernie puhuu tavoitteesta myydä 2 miljoonaa autoa, pieniä vihjailua triple digit kasvusta rivien välistä Q4:lla

Ernien haastattelu CNBC:llä Q3 tuloksen jälkeen

Carvanan viimeisin investorpresis

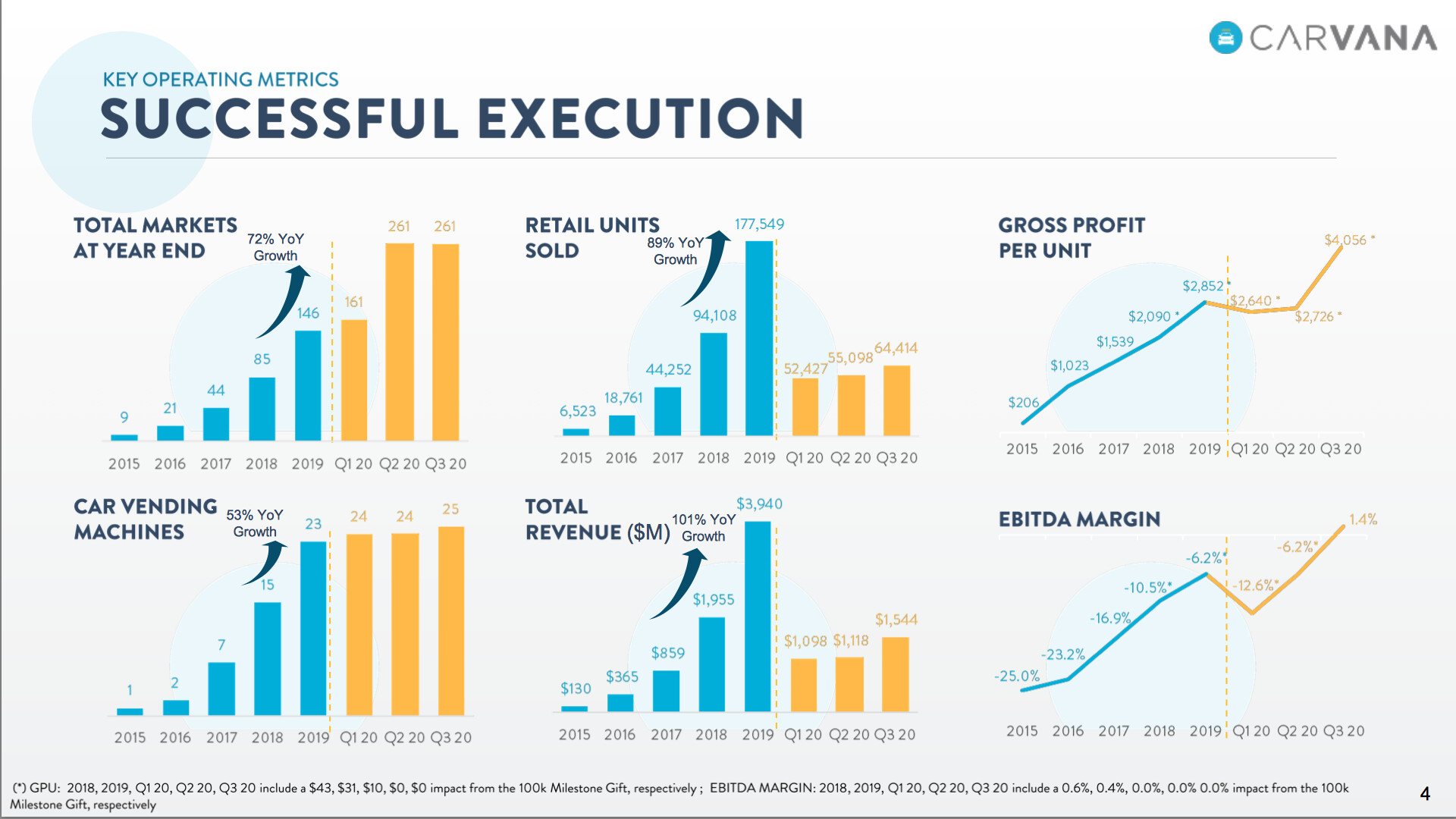

Carvanan Q3 tulostiedot:

Carvana mukana tässä podcastissa jossa puhutaan Internet-liiketoimintamalleista ja skaalan rakentamisesta. Todella hyvä podi kaiken kaikkiaan, Parameswaranilla on kova tracki, oli yksi Bytedancen (TikTok) ensimmäisiä sijoittajia mm.

https://www.joincolossus.com/episodes/22392883/parameswaran-internet-scale-businesses

Muutama poiminta investorpresiksestä loppuun: