Let’s open a dedicated thread for Cadeler A/S, which installs and maintains offshore wind turbines and is part of the larger Swire group. The company recently listed on the Oslo Stock Exchange, and DNB Markets has initiated coverage with a target price of 38 NOK and a buy recommendation.

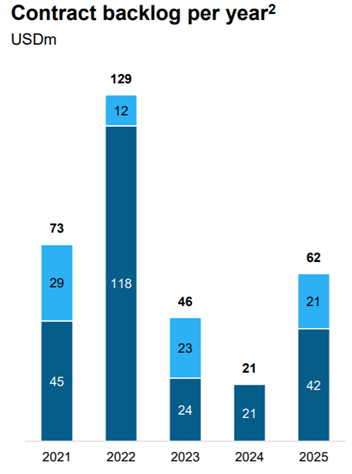

A bit of background: Cadeler installed its first wind turbine in 2010, and since 2012, the company claims to have completed over 20 wind turbine projects. The current backlog stands at USD 249 million in orders, with an additional USD 83 million in optional orders. The largest orders currently seem to be concentrated in 2022, but the situation may change considerably due to EU green investments. Below is a picture of the backlog in November 2020.

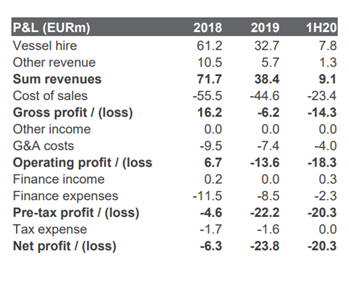

Looking at the financial figures, the company’s performance in the three previous reported years (2017-2019) was weaker than in the preceding three-year period (2014-2016), but from 2017 to 2018, the direction of EBITDA was upward. According to the company, the 2019 figures were negatively affected by one vessel being in dry dock (the vessel is simultaneously being fitted with a larger crane for future, larger wind turbines), apparently due to an accident, but I do not have more detailed information on this. Additionally, the weakening EBITDA is attributed to strengthening the organization with an eye on the future, as well as the working vessel being involved in a lower-margin project. Below is a picture of the financial figures.

The company currently has two vessels that are among the industry leaders in lifting height, vessel length, and depth installations (i.e., the vessels are capable of installing turbines in deeper waters than competitors). However, in terms of lifting capacity, there seem to be a couple of other vessels on the market with more lifting power than Cadeler’s vessels. According to the company, with crane upgrades, their ships will once again rank among the best. The company also plans to acquire a third vessel, which was apparently one of the reasons for its listing.

As we have all probably noticed, renewable energy is projected to have tremendous growth prospects. According to a European Commission study, offshore wind power is set to increase fivefold by 2030 and 25-fold by 2050. To achieve this goal, the study estimates that approximately 800 billion euros in investments in wind power will be required. According to the company itself, offshore wind power is expected to grow sevenfold from 2018 to 2030. Floating wind turbines will also play some part in this, but currently, they are still a relatively small component compared to offshore turbines. (Energy produced by floating turbines 40MW vs. offshore turbines 12GW). I cannot assess whether Cadeler has a role in floating turbines.

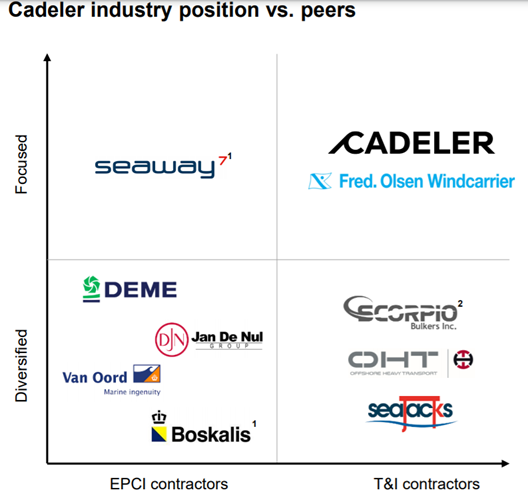

According to the company, its most direct competitor is Fred Olsen Windcarrier, but other companies have focused slightly differently. A picture of the competitive landscape according to the company’s view:

Additional material on the topic:

European Commission’s offshore wind strategy: Energy - European Commission)

Cadeler company presentation from November 2020: Chicken Road ▷ Casino Spil | Gratis Gambling & Rigtige Penge

What do you, esteemed forum members, think? Is this a potential company for the future, and what are its main challenges?

Adding the company’s website: https://www.cadeler.com/