Borg on entinen ruotsalainen tennispelaaja, jota pidetään yhtenä lajin historian merkittävimmistä pelaajista. Vuosina 1974–1981 hän voitti 11 Grand Slam -turnausta ja edusti Ruotsia voittamalla kerran Davis Cupin. Borg saavutti ITF:n maailmanmestaruuden vuosina 1978–1980 ja hänet valittiin vuoden pelaajaksi 1976–1980.

Björn Borg on myös brändi, joka tunnetaan erityisesti kalsareista, mutta valikoimista löytyy urheiluvaatteita, kenkiä, laukkua ja vähän kaikenlaista muutakin. Kyseessä on siis eräänlainen urheilumuotimerkki. ![]()

Björn Borg toimii noin 20 eri markkina-alueella, joista suurimmat ovat Ruotsi, Alankomaat, Suomi ja Saksa. Vuonna 2023 yli 80 % yhtiön liikevaihdosta tuli näiltä neljältä markkinalta ja tämä oli itselleni iso yllätys. Luulin, että merkki on paremmin hajautunut ympäri maailman. Yhtiön vahva asema kotimaassaan perustuu sen laajaan jälleenmyyntiverkostoon ja omaan verkkokauppaan.

Yhtiö on kasvanut keskimäärin 6 % vuodessa vuosina 2013–2023, yhtiön liikevaihdon kasvu on ollut hitaampaa kuin kilpailijoilla, mutta yhtiö on viime aikoina keskittynyt laajentamaan urheiluvaatetarjontaansa, mikä on auttanut monipuolistamaan liiketoimintaa. Mielestäni hienoja vaatteita ja varmaan laadukkaita, mutta salitreenaajana en ole nähnyt syytä ostaa yhtiön tuotteita, koska ihan hyviä ja ehkä toimivampia vaatteita saa halvemmalla (äärimmäisen kiinnostava tieto sijoittajille ![]() )

)

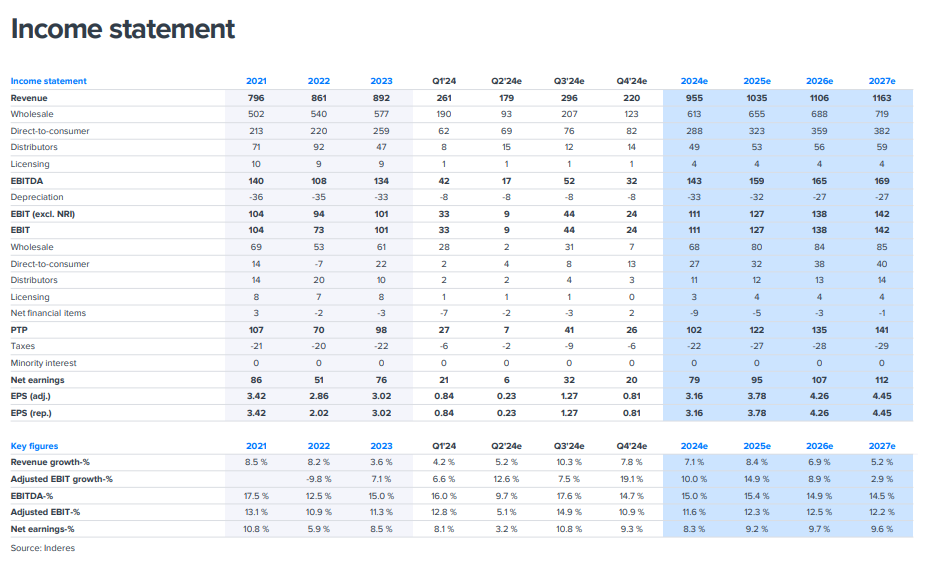

Vuonna 2023 Björn Borgin liikevaihto oli 892 miljoonaa Ruotsin kruunua (luulin paljon isommaksi firmaksi), joka tarkoittaa 4 % kasvua edellisvuodesta. Yhtiön käyttökate (EBIT) oli 101 miljoonaa kruunua, mikä vastaa 12 % liikevaihdosta. Verkkomyynti kasvoi merkittävästi, ja vuonna 2023 se muodosti 41 % yhtiön kokonaismyynnistä, mutta en osaa sanoa, miten tämä vertautuu muihin kilpailijoihin.

Enemmän asiaa sijoittajille:

Björn Borgilla on vahva brändi, mutta se on myös altis muotitrendien vaihtelulle, mikä voi vaikuttaa myyntiin. Kilpailu muotialalla on kovaa, mutta yhtiön on kyennyt nostamaan hintoja, mikä kertonee brändinsä vahvuudesta.

Björn Borg tarjoaa kannattavaa kasvua, jolla on vahva brändi. Yhtiö on maksanut säännöllisesti osinkoja hyvän kannattavuutensa ja vakaan taseensa ansiosta, mikä tarjoaa sijoittajille jatkuvaa kassavirtaa.

Miksi lukea Alokkaan höpinöitä, KOSKA:

Tämä rapsa on sitten ihan kaikkien luettavissa. ![]()

Björn Borg has a strong track record of profitable growth, consistently generating value for its shareholders. We see solid growth opportunities in key markets for this strong Nordic brand. The valuation of P/E 15x and EV/EBIT 11x for 2025 looks moderate and a combination of dividends and earnings growth should give around 10-15% expected return.