I’ve been looking at BioDelivery Sciences International (BDSI) after reading VIC’s excellent article on the subject.

Link: Value Investors Club / BIODELIVERY SCIENCES INTL (BDSI)

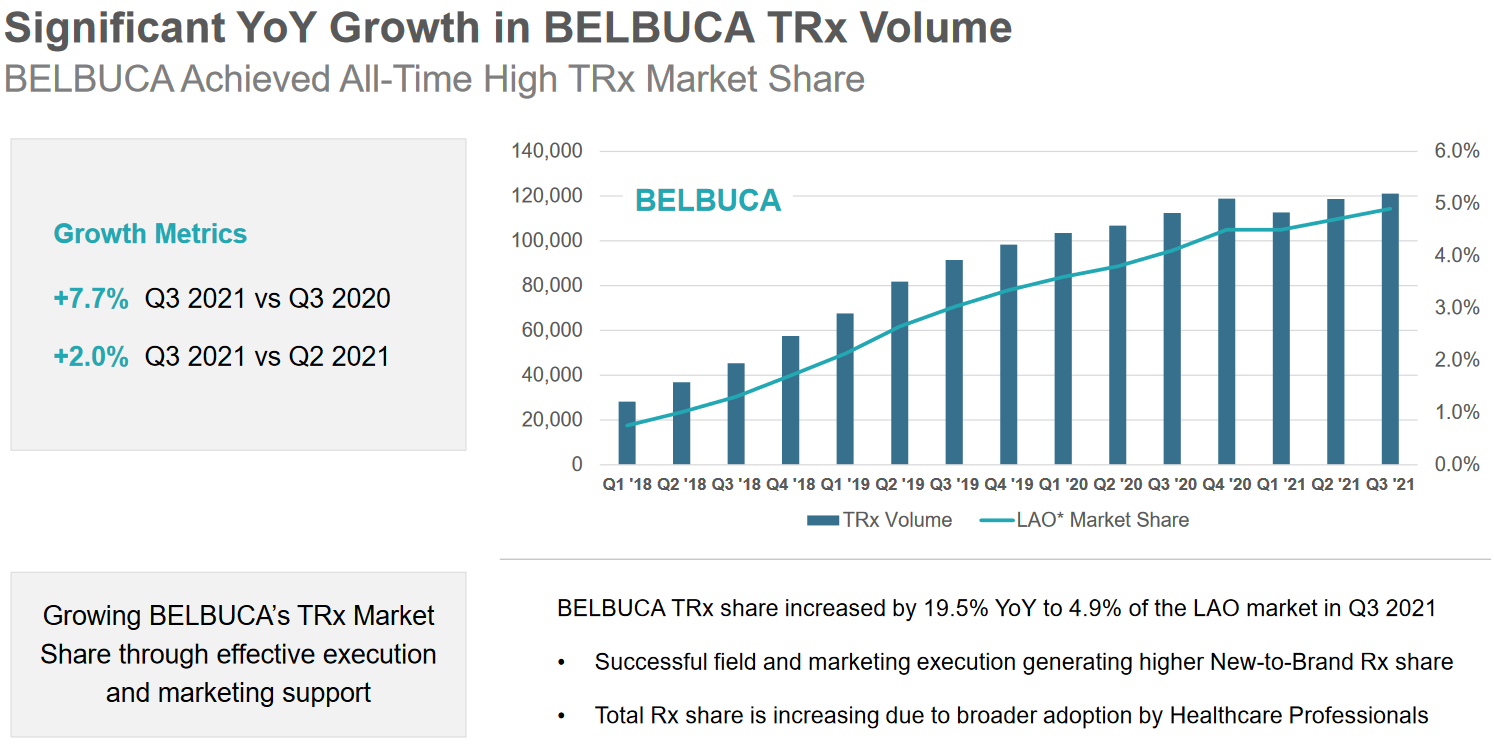

It is a US pharmaceutical company whose patented main product, Belbuca, accounted for 90% of revenue in the latest quarter. Belbuca is an opioid-based pain medication that, due to its delivery method and properties, is more difficult to abuse than its counterparts and has fewer side effects.

Belbuca is administered as a strip placed in the cheek, which dissolves into the mucous membrane. The growth in revenue and market share gained speaks to the drug’s competitiveness, which slowed during the pandemic.

During H1 2021, Belbuca revenue grew by approximately 10%, approaching pre-pandemic trends. More on Q3 events later.

Currently, the company is valued at approximately EV/EBITDA 7 and P/E 10-12 based on 2021 multipliers. DCF, with various scenarios, gives a share price of $6-8, with the current price being $3.3. A low price for an excellent company.

The reason for this is a patent lawsuit that began when Alvogen attempted to bring a similar product to market. Alvogen’s argument is that BDSI’s patent was preceded by a patent providing the same drug effect (Tapolsky patent), and indeed, that patent came into force a few years before BDSI’s patent. I cannot interpret court reports or the actual differences between patents, but my interest concerns BDSI’s performance in past disputes and management’s recent behavior.

BDSI has been in legal battles with Teva Pharmaceutical and Aquestive before Alvogen.

The Teva case ended in a settlement between BDSI and Teva, and in the Aquestive case, the court “sided” with BDSI. From this, we can conclude that BDSI is capable of defending its patents.

Another interesting turn has occurred in insider trading. Before the spring lawsuits, insiders continuously sold their holdings until they abruptly stopped in February. Since then, insiders have aggressively exercised options and, in one case, also bought from the open market. I would describe their actions as cautiously optimistic.

The company’s operational activities have also taken a more active turn. In January 2020, the company changed its CEO and initiated share buybacks of $25 million. The company also made an acquisition of ELYXYB during Q3 for $15 million, adding a migraine drug to its portfolio starting in 2022. Does this sound like a company whose revenue and margins are about to contract?

During the third quarter, other interesting events also occurred. Alvogen began selling its version of Belbuca, contrary to agreements. This was quickly brought under control. Still, even this lowered revenue guidance by approximately 5-10%. This is a taste of the possible loss of exclusivity for Belbuca sales. However, I believe the reason for this sale is the most interesting aspect.

What could be the fair value in the event of Belbuca’s loss of exclusivity? Here is an incomplete calculation with the following assumptions: BDSI grows at 2% forever after 2021, EBITDA margin drops from 24% to 15% after 2021. WACC is 8.

Let’s add a 20% margin of safety for potential litigation costs and the calculator’s incompetence. The price becomes 2.55, with yesterday’s closing price at 3.3 USD.

Optimistic scenarios give a share price of 6-8 USD.

The risk-reward ratio appears excellent in light of this. Of course, this does not guarantee that the price will not halve in the face of bad news.

The author bought this conveniently before Q3, only to experience a 20% price drop and a stop loss activating at 3.5 USD within a few days. I might jump back in with a small stake.

Sources:

Q3 presentation:

https://ir.bdsi.com/static-files/174f60b6-d1d7-4b3e-96d8-d2f060c58e52

Insider trades:

https://www.nasdaq.com/market-activity/stocks/bdsi/insider-activity

Litigation reports: