Another defensive victory for BHG, at least a better report than my own expectations. Revenue is down -10% as expected, but inventories are being cleared and cash flow (766 million SEK) is at a high level. New share issues likely don’t need to be feared, at least with these figures.

15 Likes

What are others’ thoughts on BHG at the moment? With a market cap of 2.46 billion crowns and cash reserves of over 1.0 billion, it sounds quite reasonable. EV/S is around 0.3, assuming revenue is 12.0 billion for 2023 (H1 was 6.1 billion).

Have you seen any news that could be related to BHG? How are Swedish consumers holding up? How has consumer behavior evolved in Sweden? What about the Nordics in general?

2 Likes

Cost reduction and the journey towards a pure-play online model continue in the Value Home segment. I would say that it simultaneously creates a foundation for potential structural arrangements, for which there are vast opportunities in the Nordic region.

10 Likes

Vesa Koskinen, partner at EQT, has left his position on the Board of Directors of BHG Group with immediate effect, since EQT Public Value Fund has recently sold its entire remaining holding in BHG Group.

I’m keeping an eye on BHG from the sidelines. Let’s see how Q4 goes.

5 Likes

Interim report: 1 January-31 December 2023

Significantly strengthened balance sheet and reduced inventory levels during the year and improved profitability in the quarter

– During the year, we generated SEK 1.6 billion in cash flow from operating activities, reduced our total interest-bearing liabilities by SEK 1.6 billion and carried out several structural changes in order to simplify and streamline our operations in line with our strategy.

“Our focus has been on strengthening our balance sheet and cash flow by reducing inventory and implementing changes that simplify, lower the cost base and consolidate our structure. There has been significant progress in all of these areas in 2023 and we are now financially, structurally and commercially stronger. Our strategy is working and yielding results. We set a goal to reduce our inventory by SEK 600m in 2023 and I am pleased to conclude that we have exceeded the goal with a reduction of SEK 900 during the year. In a continued challenging market, we improved our profitability in the fourth quarter compared with the previous year for the first time since mid-2021.” says Gustaf Öhrn, President and CEO.

Highlights

1 October – 31 December

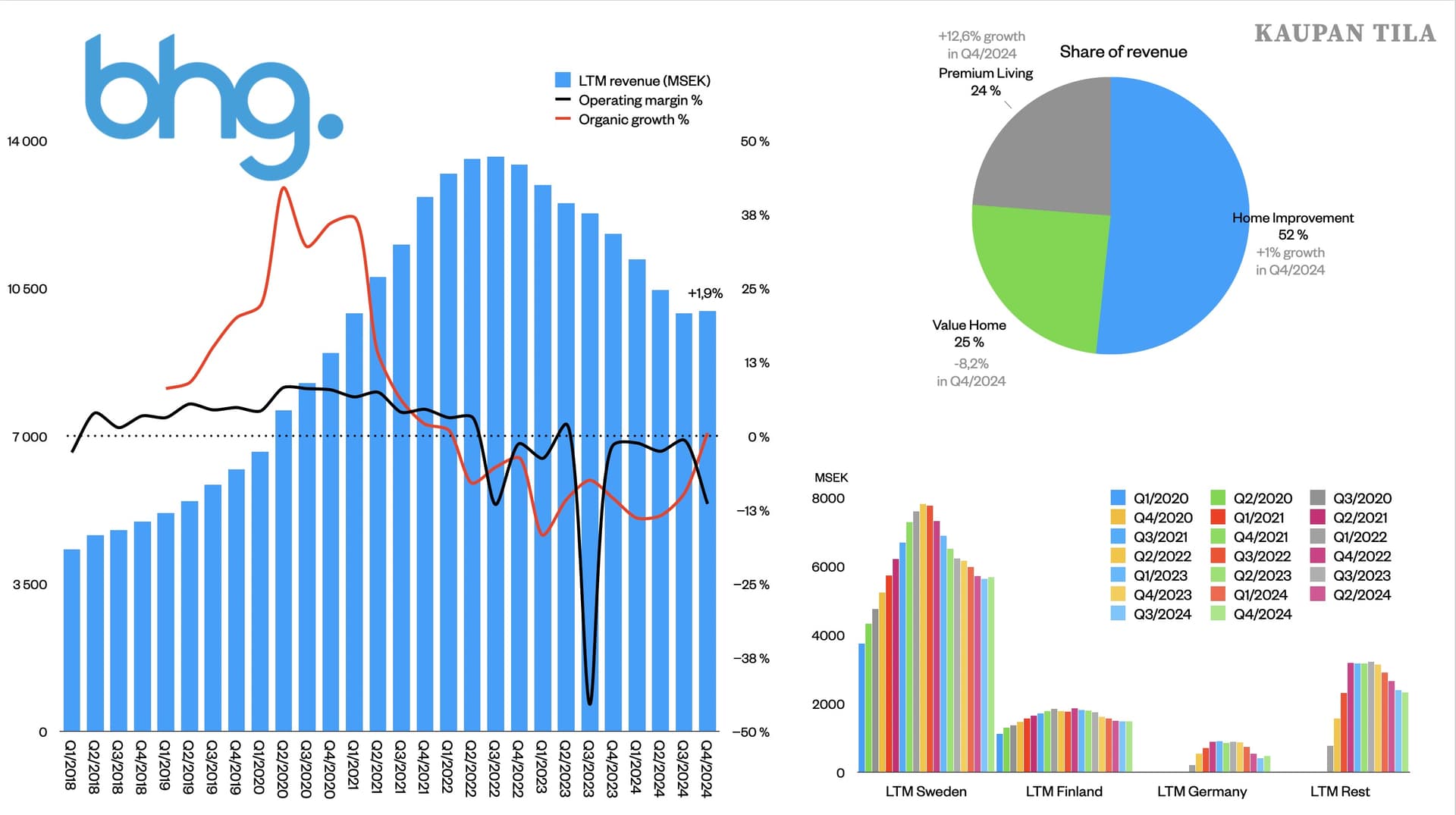

- Net sales declined -14.5% to SEK 2,828.8 million (3,307.9). Organic growth was -10.6% and pro-forma organic growth was -10.6%

- Adjusted gross profit amounted to SEK 718.1 million (804.9), corresponding to an adjusted gross margin of 25.4% (24.3)

- Adjusted EBIT amounted to SEK 54.8 million (30.7), corresponding to an adjusted EBIT margin of 1.9% (0.9)

- Cash flow from operating activities amounted to SEK 348.9 million (67.5)

- Earnings per share amounted to SEK -0.89 (-1.20) before dilution and SEK -0.89 (-1.20) after dilution

1 January – 31 December

- Net sales declined -12.2% to SEK 11,790.2 million (13,433.6). Organic growth was -11.2% and pro-forma organic growth was -11.1%

- Adjusted gross profit amounted to SEK 2,944.8 million (3,368.4), corresponding to an adjusted gross margin of 25.0% (25.1)

- Adjusted EBIT amounted to SEK 96.7 million (374.9), corresponding to an adjusted EBIT margin of 0.8% (2.8)

- Cash flow from operating activities amounted to SEK 1,550.2 million (-105.6)

- Earnings per share amounted to SEK -8.73 (0.25) before dilution and SEK -8.73 (0.25) after dilution

The Board of Directors proposes to the Annual General Meeting that no dividend be paid to the shareholders for 2023.

Key events during the fourth quarter and after the period

- On 13 December, it was announced that EQT Public Value Fund had sold its entire remaining holding in BHG Group and as a consequence Vesa Koskinen, partner at EQT, had left his position on the Board of Directors of BHG Group.

- On 21 December, a number of structural changes were announced: the consolidation of our Danish operation Frishop into HYMA Skog & Trädgård, the integration of the Lindström & Sondén warehouse structure with Hafa Brand Group, and the consolidation of inventory in Arc E-commerce AB from two warehouses into one.

- On 11 January 2024, BHG announced it was strengthening its market-leading position in the Premium segment through Nordic Nest’s acquisition of the KitchenTime brand in an asset purchase transfer and consolidation of LampGallerian.

6 Likes

Up nearly 50% in YTD figures. Are there any smarter people on the forum who have been following this and could tell if the rise is based on fundamentals?

2 Likes

The numbers were certainly a cold shower. The thesis I had when entering this has definitely evaporated. The top lines are eroding so badly that this year’s revenue will likely remain very modest. Despite platform solutions, synergies between these businesses haven’t materialized. Valuation is starting to look very stretched if the trend in the sales segment doesn’t change drastically. The only positive thing in the report was the positive development of gross margins, but otherwise, there’s no joy in watching a sinking ship. Are other forum members on the same page, or do you hold a different view of BHG Group’s future?

2 Likes

Yet another pitch-black report from BHG Group. It’s hard to see even the current share price as justified, even though we are at a “bottom” from a historical perspective.

Structural changes are good and needed, but things still seem to be in very bad shape in almost all segments. Home improvement was the only segment where some kind of defensive victory was seen.

Has everything been going from bad to worse ever since EQT exited the company?

Am I missing something in the big picture, or does anyone else see any light for this company?

2 Likes

Here is the Q2 2024 report itself

3 Likes

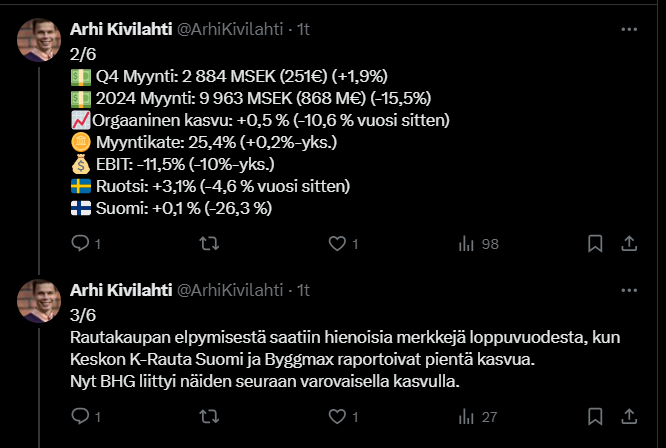

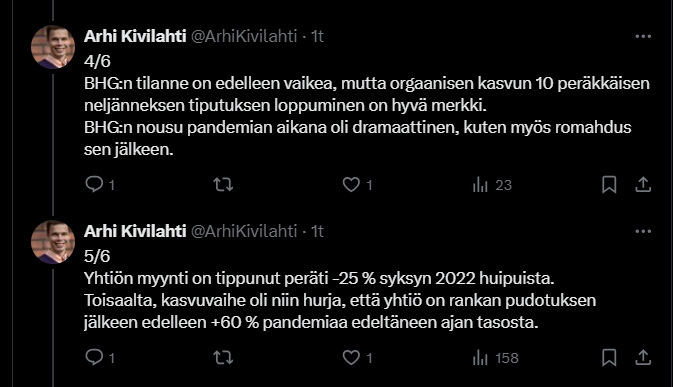

@Arhi_Kivilahti has created a tweet thread about BHG, the thread also discusses a bit about “hardware stores”.

https://x.com/ArhiKivilahti/status/1885213766402408573

7 Likes