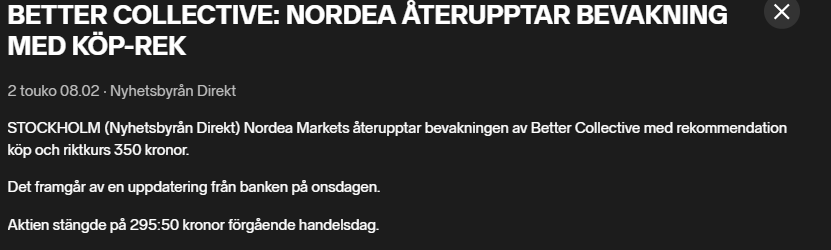

I don’t know if these volumes are already considered block trades, and if they have any information value. Regardless, I noticed that 36,146 shares were transferred through Nordea today at a price of 296 SEK each.

To avoid this being a completely empty post, the Q1 report will be released in just over two weeks, on May 21st after the market close.

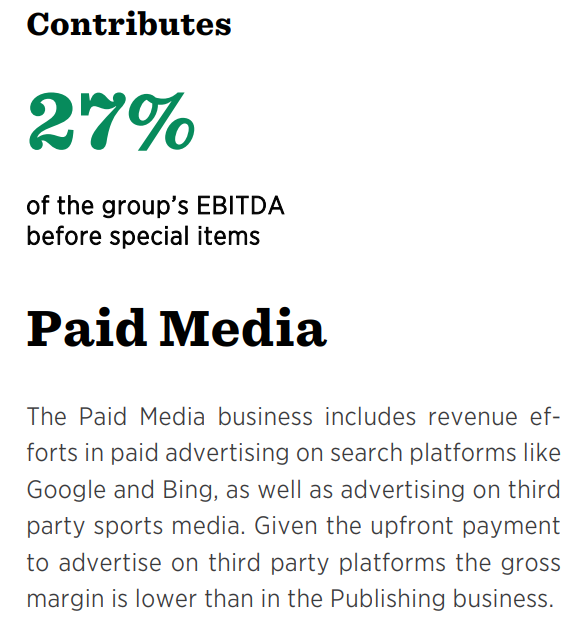

I’m not exactly an expert on this matter, but Google removed at least some of these media partnership sites from search results, which has a significant impact on site traffic and, conversely, improves the position of their own publishing sites in the results. For instance, when you search Google for “best sportsbook New York,” the New York Post’s betting section, which Betco may have managed, could have previously been at the top, and now that site has been removed from the results. Additionally, the paid segment includes direct advertising campaigns on external platforms like FB in addition to those search engine ads, so assessing the overall impact is difficult—reportedly for Betco themselves, and especially for outsiders, as nothing could be squeezed out of management in the webcast regarding the matter. This update wasn’t just about iGaming; all sorts of coupon/discount code sites on the subdomains of these major media brands were targeted by the update.

The share price took a nice dip just as share buybacks are underway (even though the amount is small, it will go toward the payment for an acquisition; though I don’t know exactly how the purchase price was agreed upon—whether the total price is now slightly cheaper, or if the cash portion increases when the share price is lower)

On 21 May 2024 Better Collective A/S (“the Company”) initiated a share buyback program for up to 2.4 mEUR, to be executed during the period from 22 May 2024 to 3 July 2024.

EBITDA flat at 29 mEUR with a 29% margin, mirroring exceptional performance last year and as expected limited near-term margin contribution from recent acquisitions

Net debt to EBITDA of 2.0

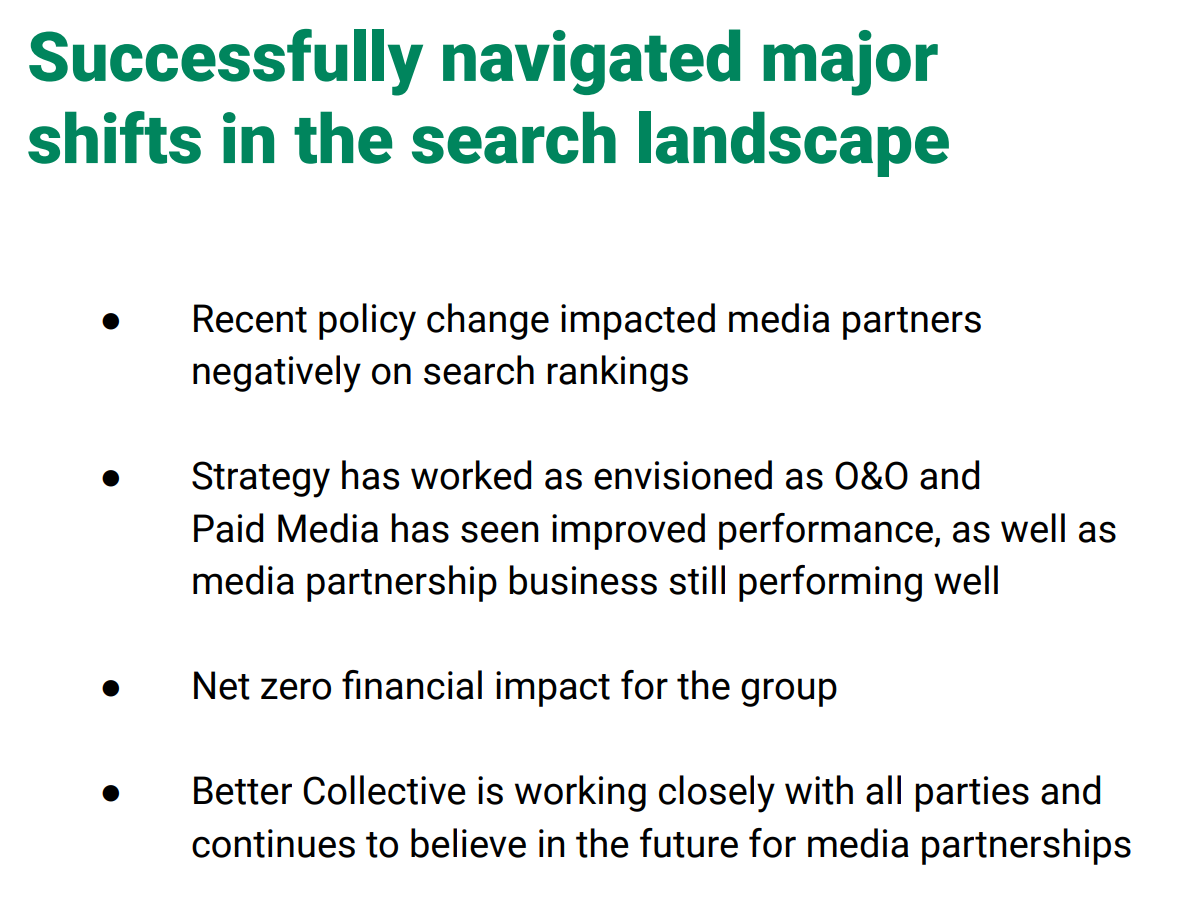

Media partnership changes have been fully mitigated and had a net zero impact for the group

Secured proof of concept and first operational success for AdVantage

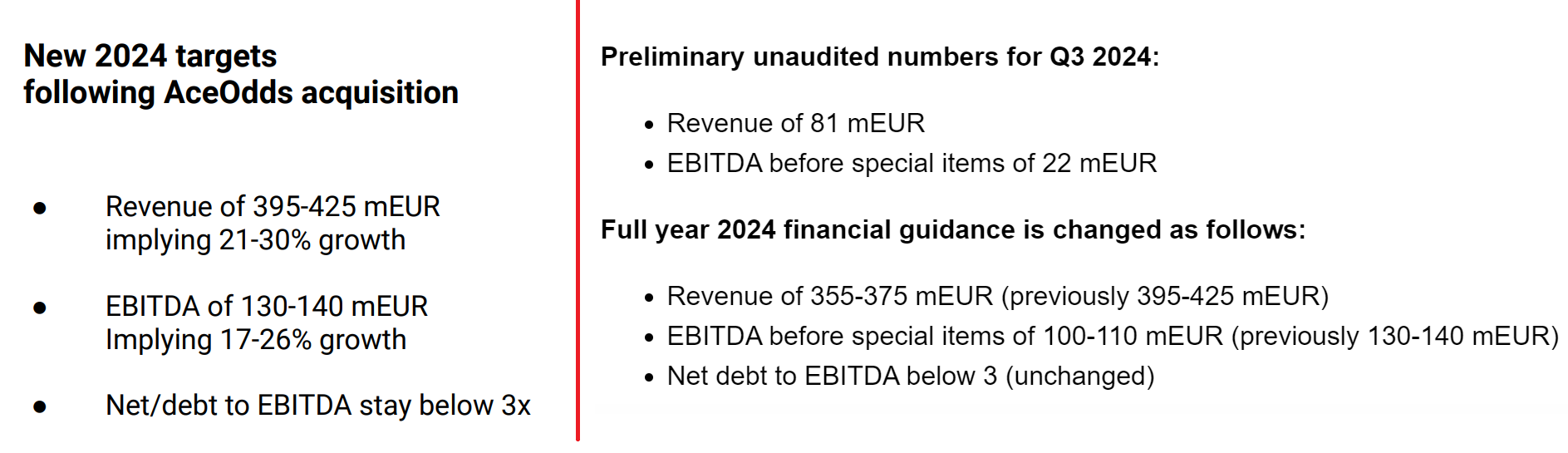

Full year financial targets were upgraded following the acquisition of AceOdds – and remain unchanged

Osari oli omasta mielestä ihan kohtuullinen, etenkin kun Googlen pelättyjä muutoksia kommentoitiin näin: Since the changes were announced, Better Collective has delivered group revenues, EBITDA and NDCs as expected prior to these changes, and the impact has been fully mitigated on a Group basis resulting in a net zero financial impact.

Red Eye’s forecasts were met quite well, but naturally, just hitting the forecasts is never enough for the market. Or maybe some are panic selling because, by operating region, Europe was stronger but the USA was weaker than predicted

Following an assessment of preliminary Q3 performance, including the first six weeks of high season in the US market, Better Collective is providing a trading update and adjusting its financial guidance. After recent large acquisitions and the market outlook, the Group is implementing a streamlining process to optimize the organization accordingly.

Regulatory release 53/2024

Preliminary unaudited numbers for Q3 2024:

Revenue of 81 mEUR

EBITDA before special items of 22 mEUR

Full year 2024 financial guidance is changed as follows:

Revenue of 355-375 mEUR (previously 395-425 mEUR)

EBITDA before special items of 100-110 mEUR (previously 130-140 mEUR)

Net debt to EBITDA below 3 (unchanged)

The financial downgrade primarily stems from a lower activity than expected from US partners. Furthermore Better Collective has, as seen in previous quarters, experienced a continued slowdown in activity in the Brazilian market heading into the expected regulation beginning of 2025. Better Collective remains confident in the long-term growth potential of these markets.

A severe profit warning and a downward revision in the full-year forecasts. I spent half a day digesting the report and eventually ended up doubling my position.

Here are also the justifications I posted in the buy/sell thread:

If they reach the guidance provided today (and I believe they will, as the range is quite wide and the 11th month is about to start), and implement those €50m annual savings by the beginning of next year, then this is a really cheap stock considering the opening of betting markets and the essential role affiliate sites play in them. After all, they are a clear market leader in their field.

I see today’s -40% crash as something of an overreaction (approx. 20-25% would have been justified), and I believe the market will correct itself sooner or later. The company is still on a clear YoY growth trajectory, and it is unlikely to taper off anytime soon.

I hope the quality of the produced content doesn’t deteriorate as staff are reduced. The question is, did they have too many employees for too long?

Better Collective CEO Jesper Søgaard took to LinkedIn on Tuesday to announce cutbacks that came after the company downgraded its “financial targets for the year.”

“Unfortunately, this plan also includes the difficult decision to part ways with some of our colleagues,” Søgaard wrote. “Each of them has played a role in shaping Better Collective into what it is today, and for that I owe them all a big thank you!”

I follow the site https://sportshandle.com myself and noticed that there hasn’t been any content for a couple of months. I usually follow the developments in the states from there.

Has anyone started digging into what caused that lowering of targets?

I waded through the Q1 and Q2 presentations:

Q1 guidance was adjusted upwards

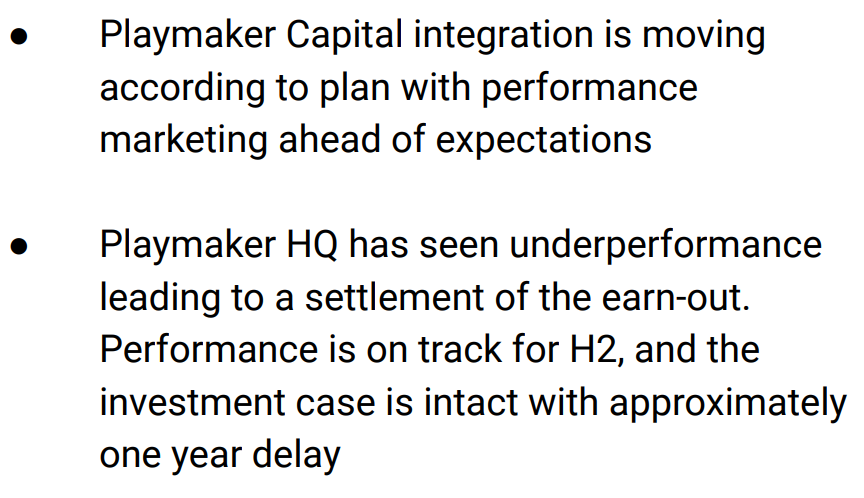

Q2 guidance was maintained. “Net zero impact” from SEO changes, but they complained about underperformance in PlayMaker’s results.

The biggest risk is that paid media would suffer from those SEO changes and that the profit warning was related to them. We’ll be wiser on Wednesday after the Q3 report, of course.

Could it be that US partners have started terminating contracts? Everything seemed to be going well right up until this quarter.

Could FanDuel have ended the partnership? It is the largest and also the most profitable sportsbook in the US.

If you go to Action Network’s FanDuel page, you get this popup:

This is what it looked like on July 2nd:

This is what it looks like now. Caesars, ESPN Bet, and FanDuel have been removed from the list, but they are clearly still partners. A promo code and link can be found on the main page for each of them.

Unfortunately for this company, the US market is heading towards a duopoly, or at most 5-7 major players.

300 people were laid off as the company restructures its operations. This represents 15% of the workforce.

Following recent large acquisitions as well as a changing market outlook, Better Collective has announced a cost reduction program of more than 50 mEUR. At the end of October, Better Collective made the difficult decision to lay off more than 300 employees, representing more than 15% of the workforce, and certain other operating costs will be reduced to lower levels. With most measures already having been executed, Better Collective is well on track for the cost reductions and tactical adjustments to have full effect from the beginning of 2025.

The CEO is very confident and the long-term targets remain unchanged:

Long term 2023-2027 targets remain unchanged as per below:

Revenue CAGR of +20%

EBITDA before special items margin of 35-40%

Net debt to EBITDA below 3x

The reason for the weakness in Brazil was explained quite clearly there. Before regulation, operators do not market actively, and because of that, BetCO cannot sell its products either. In 2025 everything changes, meaning this year is just a small speed bump.

Better Collective notes that several international sportsbooks have reduced activity in anticipation of the official regulation early 2025. This dynamic has affected Better Collective in two ways; Firstly, revenue share income has declined and secondly, there has been a decrease in new depositing customers as partners have limited marketing activity in the period leading up to the regulation.

Regarding Google changes:

On May 5, Google activated a new policy focusing on third-party content across a variety of commercial categories. This impacted the rankings and thereby audience to some of Better Collective’s media partnerships. The owned and operated sports media portfolio has made up for the decreased performance. Since Q2, Better Collective has not experienced more changes.

After reading the report, I didn’t find any drama, and I don’t see why this company would be a good long-term short target. Revenue share is growing over time, as are the US and LatAm betting markets.

There were some bumps in the road this year, but they were addressed promptly. If the efficiency measures work, we’ll be back on a growth trajectory.

And as a side note: I read the Q2 report while waiting for tonight’s earnings. It was the best CEO’s review I’ve ever read

Usually, they are just generic and cover everything at a high level. BetCO had a very detailed review that was also written from an investor’s perspective. You can tell the CEO has a large stake (17% of shares) in the company.

Let’s hope for a positive market reaction tomorrow. BetCO doesn’t seem like a company that lies. A -40% correction for a -22% cut in EBITDA was a big move. Of course, EPS was poor now (0.01 vs 0.06 in 2023), which might have an impact.

I also didn’t mention that the company carried out a share offering at the stock’s peak earlier this year. Because of that, their financial position is excellent.