Vaivaa toki

Täytyy todeta, etten ole pahemmin miettinyt retailin kannattavuutta kuin siltä kannalta, että:

i) kannattavuudesta voidaan tinkiä, kunhan kassakone kilisee ja

ii) se kilisee ajan myötä enemmän, koska tinkimällä kannattavuudesta saadaan pidettyä/kasvatettua markkinaosuutta.

Toisin sanoen, Amazon voisi mun nähdäkseni tehdä retailia jopa nollakatteisena, koska tällä bisneksellä on tarkoitus tuoda yhtiölle likviditeettiä ja kasvattaa absoluuttisia käyttäjämääriä Amazonin ekosysteemissä (ostajat/myyjät, käyttäjät/IT-ratkaisijat jne) sekä maksimoida näiden väliset verkostovaikutukset.

Tärkein ajuri on retailissa eCommercen kasvu globaalisti. Amazonin arvo riippuu siitä, miten juuri tuo kasvu jatkuu ja miten kassa saadaan hyödynnettyä verkostovaikutusten luonnissa.

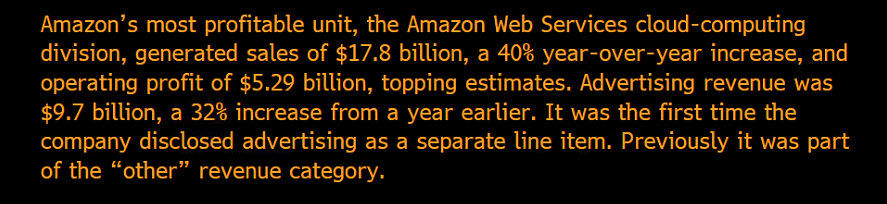

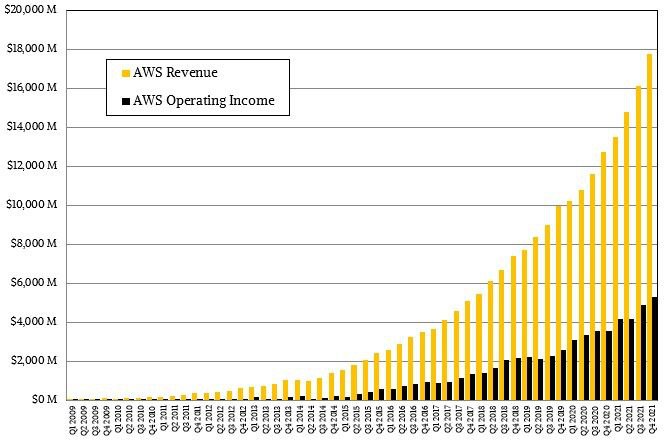

AWS on yhtiön rahastuskyvystä hemmetin hyvä esimerkki: AWS oli alkuun verkkokaupan konehuone, josta tuli “platta platassa”, joka lähti sittemmin elämään omaakin elämäänsä. Amazonin tuskin tarvitsee koskaan pohtia minkään bisneksen osalta, kuinka isoja panostuksia joutuvat tekemään IT-infraan, koska nämä investoinnit ovat todennäköisesti jatkossakin AWS:n käyttäjien toimesta takaisinmaksettuja.

Ad-bisnes on samaisesta kyvystä toinen hyvä esimerkki. Kannattavaahan tuo tietysti on, kun oli jo valmis infra (verkkokauppa + AWS), samoin osapuolet (ostajat ja myyjät, AWS:n puolella myyjien IT-osastot ja näiden IT-toimittajat)  Tämä bisnes linkittyy toki vahvimmin tuonne retailiin tällä hetkellä.

Tämä bisnes linkittyy toki vahvimmin tuonne retailiin tällä hetkellä.

Riviania en ihan vielä hahmota, miten se tuonne kokonaisuuteen uppoaa, mutta tod. näk. kyseessä sekä AWS:n että Ad-bisneksen jatke - mikseipä myös verkkokaupankin, jos sitä kautta pystyy hoitamaan Rivianin aftersalesin huolloista tuunaukseen?

Mitä enemmän keksivät tapoja luoda uusia verkostovaikutuksia, sitä arvokkaampi tästä tulee - ja samalla hankalampi arvottaa pelkästään retailin tuomalla kassavirralla, jos ja kun AWS kasvaa retailia suuremmaksi. Edit: samaa mieltä siitä, ettei pelkkä retail oikeuttaisi tällaisia kertoimia