Itseäni kiinnostaa miksi ja miten ChatGPT tappaa haun ja rahavirrat? Ensiinäkin ChatGPT:hen pitää kirjautua. Käytän mieluumin palvelua johon ei tarvitse kirjautua. Toiseksi tuleeko vastaus nopeasti? Google voitti aikanaan hakukonekisan Yahoota ja Alta Vistaa vastaan, kun sillä blank hakusivu eikä mainoksia, jonka seurauksena se oli selvästi nopeampi. Uskon ihmisten edelleen haluavan googlata äkkiä. Toiseksi Googlatessa usein se ensimmmäinen ehdotus ei ole mitä haluaa. Helpompi selata vaihtoehdoista kuin odottaa minuutti tekstiä joka tuubaa ja antaa uusi kysymys.

4 tykkäystä

Tätä on varmasti tässäkin ketjussa sivuttu, mutta tuon oman näkökulman esiin. Nykyisin jos etsin jotain tietoa niin kysyn sen suoraan joltain tekoälyltä yleensä siis ChatGPT:ltä. Joten tässä tapauksessa tekoäly on korvannut aivan kokonaan Googlen käytön. Anekdoottisesti voisin vastata myös että minulle ei ole väliä joudunko kirjautumaan johonkin palveluun. Tekoälyille tai agenteille voi antaa käskyjä esimerkiksi että pidä vastaus lyhyenä jolloin se vastaus on yleensä lyhyt ![]()

Lähinnä siis yritän tuoda sitä pointtia että tekoälyn käyttäminen on huomattavasti vaivattomampaa kuin Googlen käyttö kun etsii tietoa.

Mutta käytän googlea edelleen, mutta nykyisin se on pelkästään puhelinluettelo jota käytän kun haluan mennä johonkin tietylle sivustolle, esimerkiksi johonkin verkkokauppaan.

7 tykkäystä

Mielenkiintoista keskustelua tästä jättiläisestä. Kirjoittelin joskus aiemmin aivopierun sijoituscastin Microsoft vs Google -videon jälkiliukkailla.

Koitan kirjoittaa päivitellyn aivopierun vol. 2, kieli poskessa ja lippa takana.

- Analysoidaan, missä oikein mennään Q3/2025-raportin ja Gemini 3.0 -julkistuksen valossa. Edessä on mahdoton tehtävä.

- Sijoittajan silmin tilanne on pikkuisen jännittävä: perusliiketoiminta jauhaa kassavirtaa mutta aina on pientä puristusta pakaroissa.

1.Gemini 3.0 – Pysyykö haku relevanttina?

Keskustelu on siirtynyt chatboteista “agentteihin”. Google on teknisesti kirinyt kilpailijat kiinni ja vähintään rinnoille, mahdollisesti painellut ohi, ainakin väliaikaisesti.

Agentit : Gemini kykenee jo suorittamaan toimintoja, joissa on arvoa (varaukset, ostokset). Tämä on kyllä todella tärkeä kehitysaskel, jossa Google alkaa päästä kunnolla hyödyntämään nykyistä ekosysteemiä ja käyttäjämassaa.

Kriittisenä kysymyksenä on kuitenkin, miten tämä kaikki oikeasti kaupallistetaan kannattavasti.

- Q3-data: “Google Search & Other” 56,56 miljardin dollarin liikevaihdon +14.5 % kasvulla. Haku ei sula, se kasvaa. Tämä on aika rajua touhua.

- Generatiivisen haun kustannusrakenne on varmasti raskaampi, mutta näyttää siltä, että vastauksiin upotetut mainokset toimivat.Yhtiö joutuu varmasti tasapainoilemaan käyttäjäkokemuksen ja katteiden välillä.

- Bloombergin uutisesta lainattuna latausmääriä:

”As of October, Gemini’s app had 73 million monthly downloads, well shy of ChatGPT’s 93 million monthly downloads, according to research firm Sensor Tower.”

Tärkeää pöhinä-tekoälykeskustelussa on huomioida missä käyttäjät oikeasti tekevät rahallista arvoa tuovia toimintoja.

Hassutteluna ja lippa vinossa:

Voin kirjoitella Fugen kuumimmalle matkaoppaalle runon ChatGPT:n avulla ja luoda samalla onnittelukortin.Kuitenkin, kun alan lyömään rahaa tiskiin ja vertailemaan hotelleja, lentoja tai Black Friday -tarjouksia, tiedän mihin suuntaan. Talvirenkaita tutkaillessa voin kysyä samalla Geminin mietteet.Tästä toiminnasta ehkä myös mainostajalle iloa. En väitä etteikö runo Fugen matkaoppaalle ole arvokas.

2.Infra: Omat sirut (TPU) vs. Nvidia

-

TPU: Valtaosa yhtiön omasta AI-kuormasta pyörii Googlen TPU-siruilla. Tämä “suojelee” katteita, kun kilpailijat maksavat Nvidian raudasta.

-

Kolikon kääntöpuoli: TPU on osaltaan suljettu ekosysteemi. Ainakin näin olen ymmärtänyt? Saa korjailla. Riskinä tässäkin on, miten kehitys kehittyy ja jääkö Google eristyneeksi, kun muu maailma kehittää sovelluksia Nvidian standardeilla.

-

Bloombergin uutinen Metan kiinnostuksesta (sama lähde kuin ylempänä):

”On Monday, tech publication the Information reported that Meta planned to use Google’s chips in its data centers in 2027. Google declined to address the specific plans, but said that its cloud business is “accelerating demand” for both its custom TPUs and Nvidia’s graphics processing units. “We are committed to supporting both, as we have for years,” a spokesperson wrote in a statement.” -

Tässäkin ehkäpä isossa kuvassa vaakakuppissa löytyy positiivinen tekijä. Kustannusetu on mahdollisesti Googlen puolella. Kovan kilpailun ja kannattavuuden tilanteessa tämä tuo etua taas Googlen laariin.

-

Tähän myös lyhyt lainaus:

”Google’s TPUs are mostly attractive to a handful of companies with big computing bills, like Meta and Anthropic, said Meryem Arik, CEO of the AI startup Doubleword.”Business insider uutinen: Nvidia, AMD Stocks Fall As AI Chip War With Google Heats up - Business Insider

3.YouTube on tällä hetkellä uskoakseni mainosmyynnin kivijalka.

-

Q3/2025 YouTube-mainonta 10,26 miljardia dollaria (+15 % kasvua). Tässä on erittäin vakuuttavaa kehitystä. Samaan aikaan tulee ottaa huomioom, että mobiililaitteissa käytetään entistä enemmän aikaa TikTok. Saa nähdä miten Shorts kehittyy ja pärjää tässä.

- TV vs. Mobiili: Nielsenin datan mukaan YouTube voittaa (Connected TV) Yhdysvalloissa. https://www.nielsen.com/news-center/2025/youtube-netflix-ride-the-wave-of-summer-streaming-highs-in-nielsens-media-distributor-gauge/

-

Data: YouTuben strateginen merkitys korostuu videomuotoisen opetusmateriaalin lähteenä tekoälylle.

- Tämä on varmasti taas positiivinen resurssi, kun kilpailu siirtyy multimodaaliseen tekoälyyn (video, ääni, kuva).

4. Uudet kasvuntekijät: Cloud, Pixel ja (Waymo)

Yhtiön riippuvuus mainonnasta on vähän vähentynyt, uudet alueet ottavat aikaa ja vaativat kuitenkin investointeja.

-

Google Cloud: Q3/2025 luvut (15,15 miljardia dollaria (+33,5 % kasvua) vahvistavat, että pilvi on kuitenkin se kovin kasvun alusta. Kilpailuasetelma on vakiintunut: AWS johtaa volyymissa, Microsoft yritysintegraatioissa, Google hakee kasvua AI-kärjellä.

-

”Google Cloud is one of the most important priorities for Alphabet as a whole and I expect it to play an even more central role as the company moves forward,” Alphabet CEO Sundar Pichai told Reuters in an interview earlier in October.”

-

-

Pixel: Nevahöörd? Q3/2025 Google Subscriptions, Platforms and Devices" toi 12,9 miljardia dollaria (+20,8%).

-

Pixel on myös tärkeä alusta, jossa Google voi hallinoida raudan, ohjelmiston ja tekoälyn kehitystä. Markkinaosuuden kasvu on positiivista, mutta tärkein taloudellinen vipu on kuitenkin omalla laitteella tehtävä haku vs iphonella tehty, josta joudutaan maksamaan Applelle “veroa”.

”Pixel phones do seem to be gaining steam. Sort of. Five years ago, only about 1 percent of American phone buyers picked a Pixel. Now it’s 4 percent.”* https://www.washingtonpost.com/technology/2025/08/19/best-android-phone-google-pixel-apple-samsung/

-

“Luxus” luokassa:

“Google’s share in the $600+ price band rose to 6.1% in September 2025 from 0.1% in September 2022, an impressive feat in the mature US market.”

Google Sees Record Single-Month Pixel Sales in US During September 2025

-

-

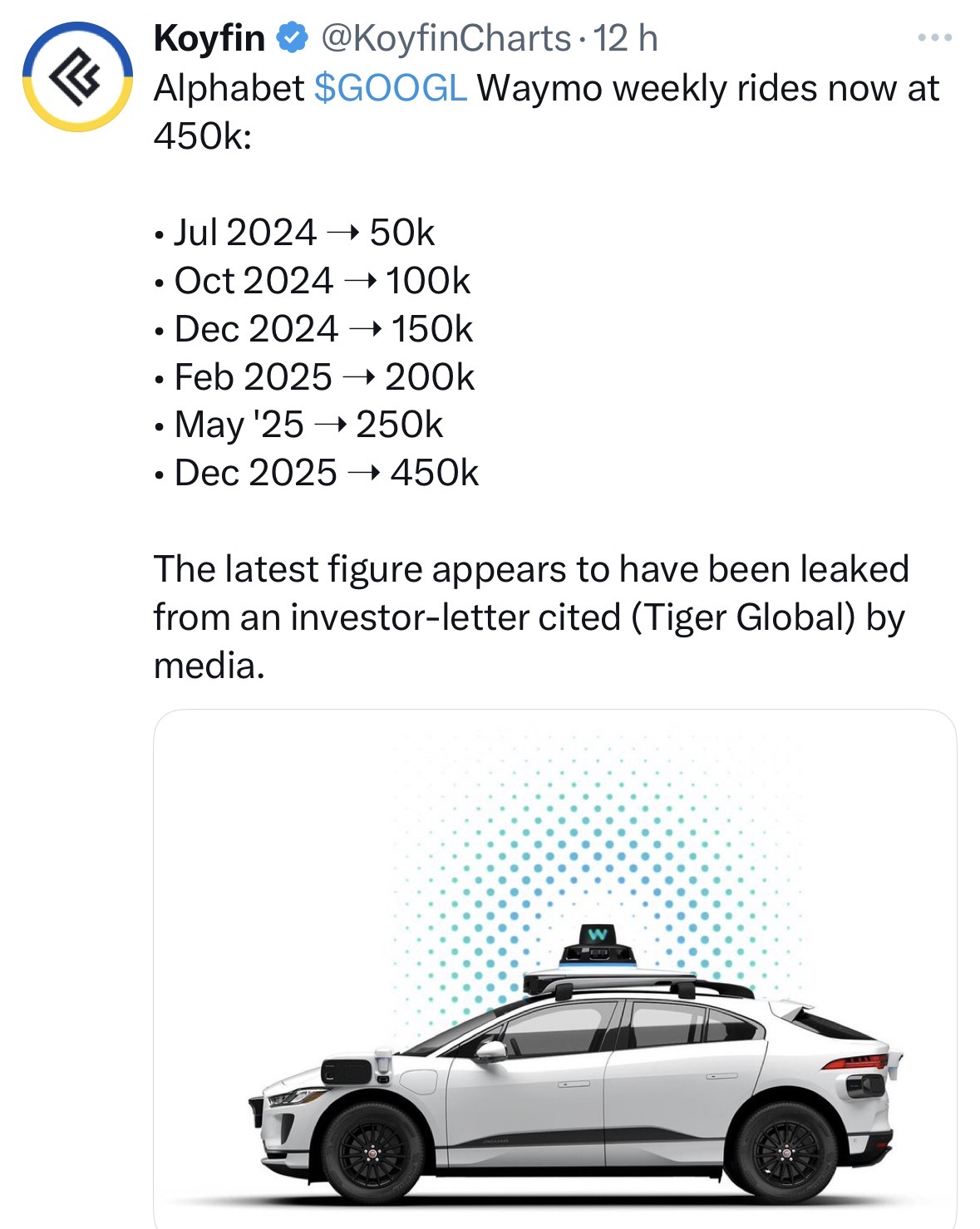

Waymo: Skaala kasvaa (lähes 250k viikkokyytiä), mutta globaali kannattavuus ja skaalautuvuus on yhä kysymysmerkki. Tämä on optio, jonka arvo voi olla oikeastaan mitä vaan 0 ja taivaan välillä. Tällä hetkellä tätä ei varmasti mitenkään noteerata jos mietitään arvostusta. Aivan mahdotonta tälle on suoraan mitään arvoa antaa. Kuitenkin mukava bonus.

Jos haluaa härkämäistä luettavaa niin tästä löytyy: Waymo Is A Trillion-Dollar Opportunity. Google Just Needs To Seize It.

Tehdään loppuun horoskooppeihin ja tähtitieteeseen pohjautuva arvio miten liikevaihto voisi kehittyä ja millainen rakenne on esim 3-vuoden kuluttua 2028:

-

Mainosbusiness (67.99% liikevaihdosta):

Kasvu n. 5 % tasolle. Haku olisi näin kypsynyt erittäin kypsäksi ja AI syö volyymia, mutta hinta kompensoi. Muistutuksena Q3 tämä oli aika hurjaa menoa +14.5 % kasvu. -

Cloud (20% liikevaihdosta):

Tämä on kasvumoottori ( noin 20 % kasvuvauhtia). Tämän hetken kasvuvauhti (+33,5 %). Nykyisellä vauhdilla 20 %:n osuus liikevaihdosta voitaisiin saavuttaa todennäköisesti vuonna 2027. -

Muut (12,01% liikevaihdosta) eli Waymo/Pixel/Subs

Mainonnan osuus liikevaihdosta tippuu varmasti pikkuhiljaa nykyisestä 75 %:sta alle 70 %:iin. Yhtiö muuttuu enemmän infrastruktuuripeluriksi.

Katteet voi mahdollisesti tippua lähitulevaisuudessa mutta tästäkään ei ota selvää kuin ajan kanssa. Toisaalta onko yhtiöllä potentiaalia tehostaa omia jo entisestään tehokkaita työtapoja ja kehitysmenetelmiä.

Mielenkiintoinen tilanne voi syntyä JOS TPU-kauppaa alkaa käymään kunnolla ulkopuolelle, Metan ja kumppaneiden suuntaan. Nappaan kuitenkin lääkkeet tähän väliin.

Monia positiivisia ajureita on piilotettuna tekstiin mutta tarkoitus ei ollut kirjoitella härkämäistä analyysiä. Erittäin vahvaa holdausta. Viisaammat miehet ovat myös mukana menossa.

(Kuva: Voronoiapp ja Author stockmen9)

Norsun syönti on nyt päättynyt. Sanotaanko nyt näin, että jos jotain opin, niin aivopieru vol 3:sta en lähde hetkeen kirjoittamaan.

16 tykkäystä

Waymo aloittaa robottitaksien “manuaaliset” testiajot Baltimoressa, Pittsburghissa ja St. Louisissa.

Waymo toimii, suunnittelee palvelua tai testaa ajoneuvojaan jo ainakin 26 kaupungissa.

Uudet alueet laajentavat palvelua, kun Waymo tähtää täysin autonomisiin kyyteihin - laajeneminen jatkuu kilpailun kiristyessä.

https://www.cnbc.com/2025/12/03/waymo-baltimore-pittsburgh-stlouis.html

7 tykkäystä

Google Cloud solmi monivuotisen yhteistyösopimuksen AI-koodausalusta Replitin kanssa vahvistaakseen asemaansa nopeasti kasvavassa jossain vibe-coding-markkinassa.

Replit ottaa entistä kattavammin käyttöön Googlen pilvipalveluja ja malleja, mikä voi tuoda Googlelle lisää uusia yritysasiakkaita. Tämä hurja startuppi kasvaa vauhdilla ja on jo miljardiluokan liikevaihtotasolla.

"

Points

- Google Cloud is locking in a multi-year partnership with AI coding startup Replit

- Google is betting on Replit as a breakout platform in the fast-growing vibe-coding phenomenon

- Replit will expand use of Google Cloud services, add Google models onto its platform, support AI coding use-cases"

https://www.cnbc.com/2025/12/04/google-replit-ai-vibe-coding-anthropic-cursor.html

5 tykkäystä

11 tykkäystä

Yhdysvaltalainen tuomari Amit Mehta viimeisteli Googlen hakumonopolia koskevat seuraamukset ja lisäsi perjantaina vielä uusia yksityiskohtia päätökseen.

Ankarimmat rangaistukset, kuten Chromen pakkomyynti, niin hylättiin, mikä helpotti sijoittajia. Google ei kuitenkaan saa tehdä pitkäkestoisia tai yksinoikeudella hakua suosivia sopimuksia, lisäksi sen on avattava enemmän hakudataa kilpailijoille. Päätös ei jutun mukaan varsinaisesti murskaa Googlea, mutta voi silti “kirpaista” kuiteski.

https://www.cnbc.com/2025/12/05/judge-finalize-remedies-in-google-antitrust-case.html

4 tykkäystä

Sanoisin, ettei ole mitään merkittävää vaikutusta Alphabettiin. Vahinko on jo käynyt eli Google on saanut suosituimman aseman hakukoneena ja päässyt laajimpaan dataan kouluttaakseen tekoälyä ennen muita. Se, että nyt ei saa enää tehdä kilpailua poissulkevia sopimuksia esim. Applen kanssa, ei ole mielestäni kovinkaan relevanttia. Tähänkin varmasti keksitään jokin juridinen porsaanreikä.

2 tykkäystä

Tässä on vielä SalkunRakentajan juttu Geminin menosta ja siitä, miten ChatGPT:n meno on rauhoittunut ollen kuitenkin samalla vielä selkeästi se “suurin”.

Samaan aikaan Googlen Gemini rakentaa kiihtyvällä tahdilla omaa käyttäjäkuntaansa. Alphabetin toimitusjohtaja Sundar Pichai kertoi syksyn tulosjulkistuksessa, että Geminin erillinen sovellus on noussut yli kuudensadanviidenkymmenen miljoonan kuukausittaisen käyttäjän tasolle, kun vielä keväällä luku liikkui vain runsaan kolmensadan miljoonan tuntumassa. Kasvu on ollut poikkeuksellisen ripeää, ja sen taustalla ovat paitsi aggressiivinen jakelu Googlen ekosysteemiin myös kuluttajia houkutelleet kuvageneraattoriominaisuudet, kuten Nano Banana -toiminto.

Alaotsikot:

- Käyttäjän kasvu hiipuu – sitoutuminen jakautuu

- Gemini hyödyntää jakeluetuaan

- Raskas kustannusrakenne painaa OpenAI:ta

- Google pelaa pitkää peliä tuloksella

- Kilpailu siirtyy kuluttajista infrastruktuuriin

7 tykkäystä

Alphabet’han nimenomaan saa tehdä yksinoikeussopimuksia kunhan niiden kesto on korkeintaan yhden vuoden. Aikaisemmin tätä sopimusten kestoa ei oltu rajattu. Tämä koko anti-trust oikeudenkäynti on kääntynyt Alphabet’in kannalta suotuisasti. Luonnehtisin näitä tarkempia ehtoja erittäin lieviksi, eikä aikasemmin Chrome-selaintakaan tarvinnut divestoida. Mielestäni nämä yksinoikeussopimukset hakuun nimenomaan ovat erittäin tärkeitä yhtiön asiakashankintaan ja varsinkin pienikuluista sellaista. Nyt ison 10 miljardin hintalappusen sijaan pulitetaan sitten vuosittain vaihtuva määrä rahaa yksinoikeudesta. Tämä mahdollistaa käytännössä samanlaisen toimintamallin aikasempiin vuosiin nähden, joskin yksinoikeuksien hintalappu saa osakseen inflatorista painetta vuosittain nousumarkkinan aikana.

Datan jakaminenkin jää nähtävästi pieneen osaan ja eiköhän rakas monopolimme työnnä tikkua rattaisiin jokaiselle, joka tähän raakadataan haluaa käsiksi päästä. Jos joku parempi skenaario oli olemassa tämän oikeudenkäynnin suhteen, en sitä itse ainakaan mielessäni kuvitellut. Käytännössähän tämä oli tuomarin hyväksyntä monopolille. Tästä on hyvä jatkaa liiketoimien suojelemista.

7 tykkäystä

Google tuo kehittäjille uuden Antigravity-ympäristön, joka rakentuu Gemini 3 Pro -mallin varaan ja jutussa kerrotaankin, että yhtiö nostaa tekoälyagentin koodauksen keskiöön.

Kova kysyntä pakotti rukkaamaan käyttörajoja esimerkiksi Pro- ja Ultra-tilaajat saavat mm. korkeimmat kiintiöt ja sitten taas ilmaiskäyttäjille Antigravitya jaetaan viikkokiintiöinä, jotka kuluvat tehtävän vaativuuden mukaan eivätkä niinkään pyyntöjen määrään.

The entire Gemini 3 suite is experiencing high user demand, with Google capping Gemini 3 Pro and Nano Banana Pro usage at the end of November. Now, Google is making similar adjustments for Antigravity. However, instead of slashing rate limits, the company is tweaking them to make Antigravity available as much as possible while keeping up with the demand.

5 tykkäystä

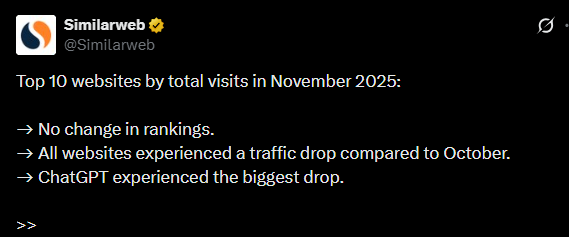

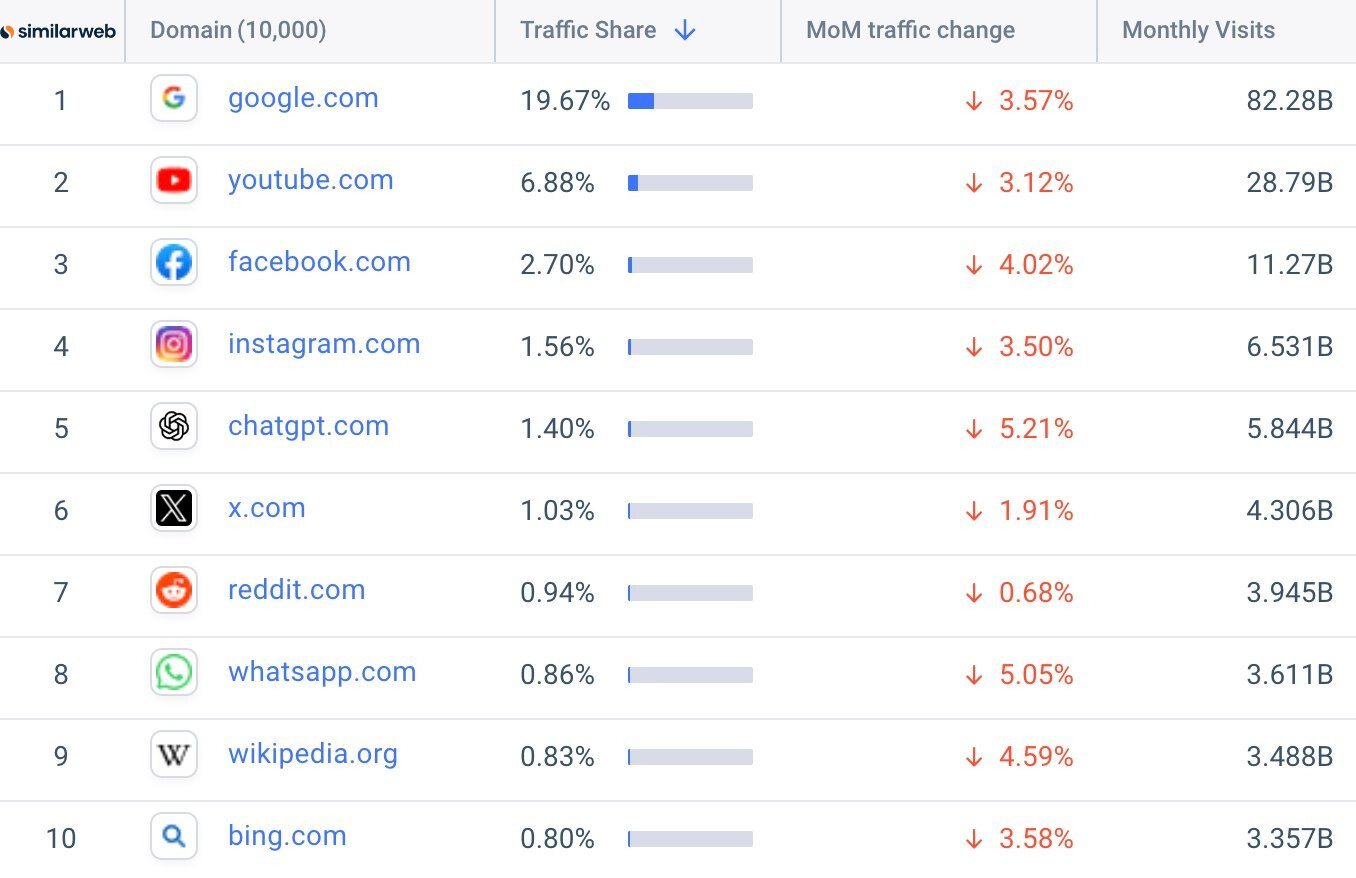

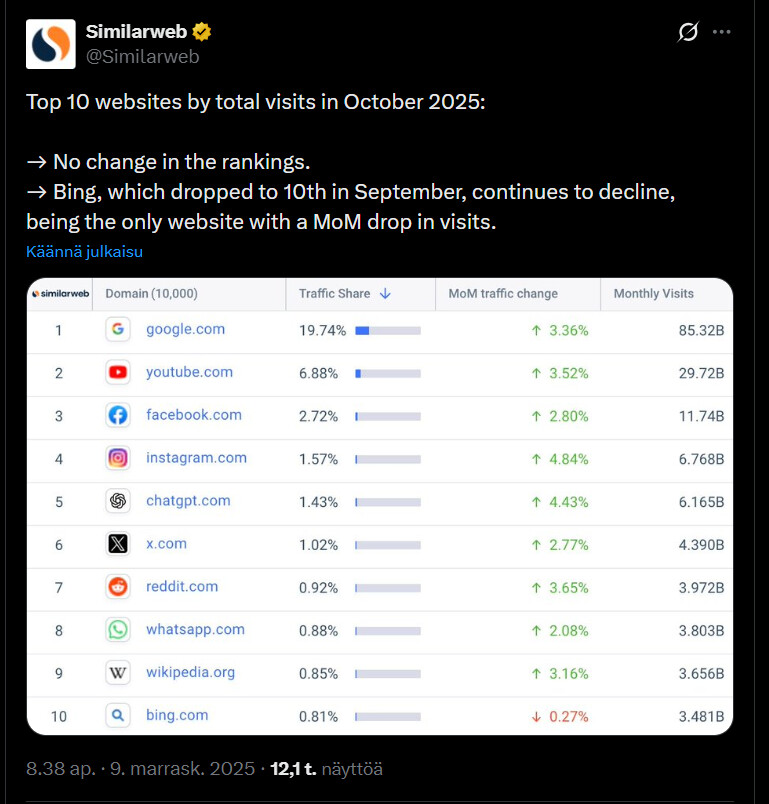

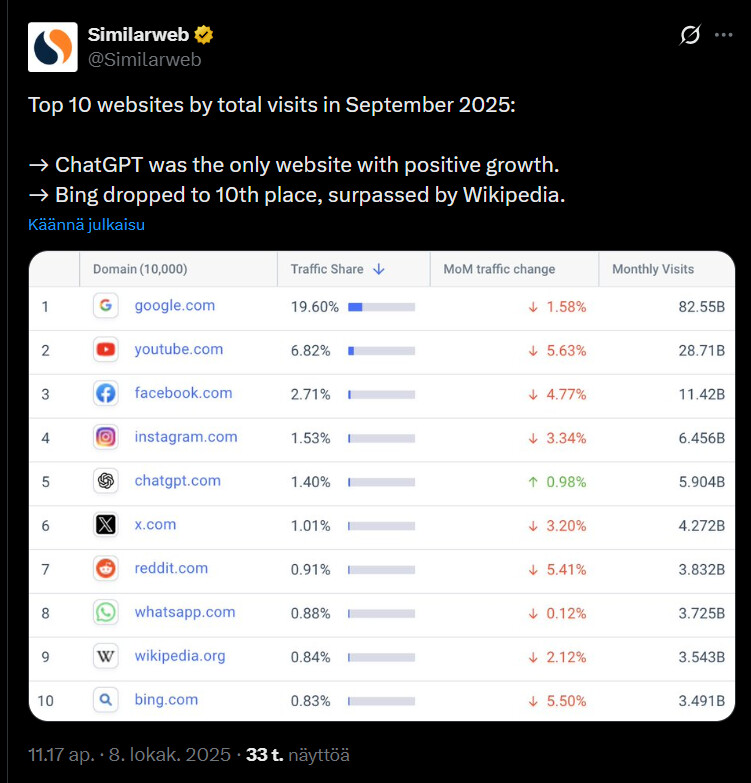

Tämä alla oleva tviitti kiinnostanee tässä ketjussa, vaikka pitkälle menemiä johtopäätelmiä ei voi toki tehdä tuon ChatGPT:n muita kovemman laskun perusteella. ![]()

https://x.com/Similarweb/status/1997963677065195902

Toisaalta syys- ja lokakuussa sillä meni lujaa

3 tykkäystä

Itsellä chatGPT:n verkkosivun käyttö pienentynyt huomattavasti, sillä puhelimella käytän appia ja tietokoneella Copilotin GPT5 mallia.

Ihan vain huomiona että nämä verkkosivujen käynnit ei ehkä tule olemaan yhtä relevantteja tulevaisuudessa.

Esim perplexityä käytän suhteellisen usein puhelimella googlen korvaajana, ja silläkin käytän heidän omaa sovellusta.

7 tykkäystä

Hyvä huomio, aluksi moni käytti vain tietokoneella, nyt sitten monet ottavat kännykän appeineen esille. ![]()

Alla on juttua siitä, miten Google aikoo tuoda ensimmäiset tekoälylasinsa markkinoille ensi vuonna kilpaillakseen Metan Ray-Ban Meta -lasien kanssa.

Tulossa on sekä ääniavusteisia Gemini-laseja että myös malleja, joissa on linssiin upotettu näyttö esimerkiksi kartta- ja käännöstiedoille. Laitteet perustuvat Android XR-malliin ja niitä kehitetään yhdessä mm. Warby Parkerin, Samsungin ja Gentle Monsterin kanssa.

https://www.cnbc.com/2025/12/08/google-ai-glasses-launch-2026.html

4 tykkäystä

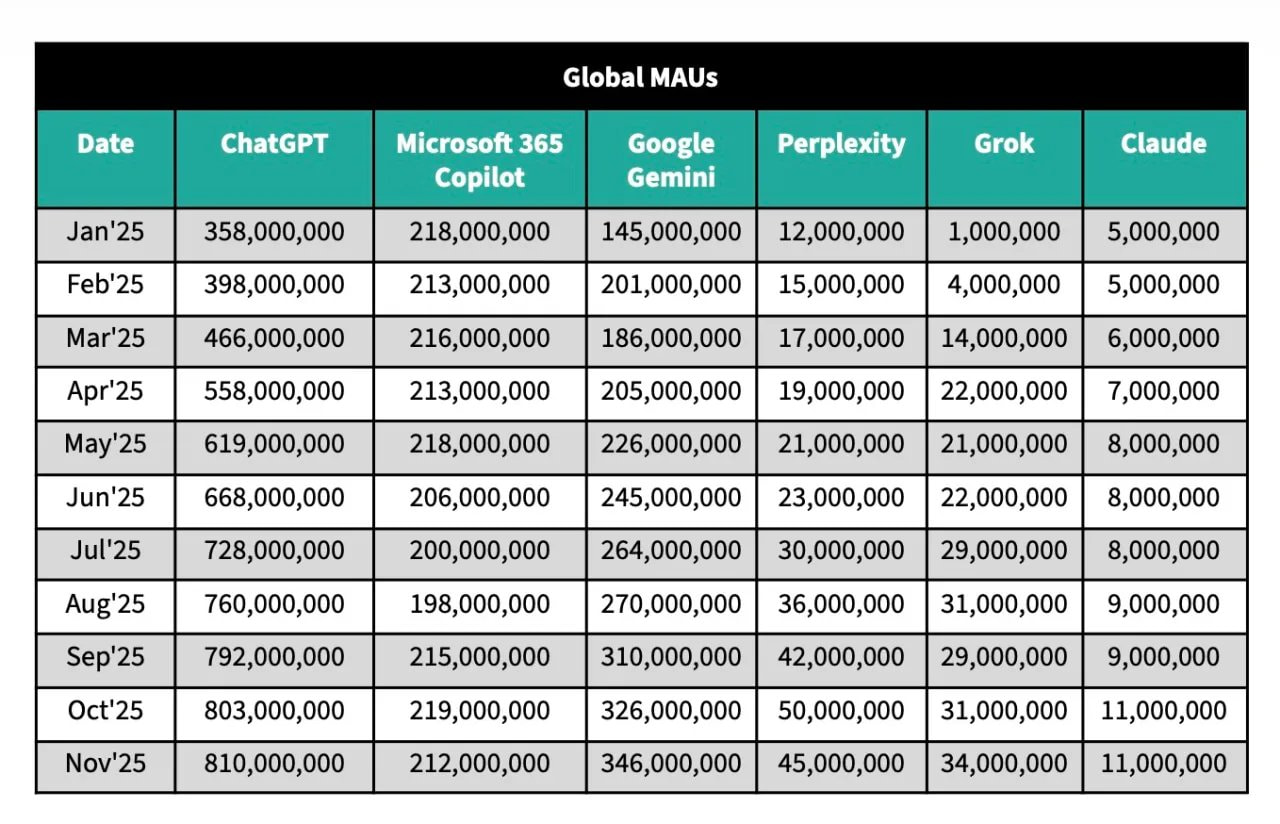

Alla olevassa jutussa on tuttu asiaa, jossa kerrotaan mm. miten Googlen Gemini kirii vauhdilla OpenAI:n ChatGPT:tä, tuplaten verkkokäynnit (elokuu–marraskuu 2025) ja kasvattaen kuukausiaktiivit 346 miljoonaan tuoreen datan mukaan.

ChatGPT pitää yhä etumatkan noin 810 miljoonalla käyttäjällä ja muutenkin pidemmillä käyttösessioilla. Kilpailu kiristyy siinä määrin, että OpenAI:n Sam Altman on jo julistanut taloon sisäisen ”code redin”.

Lisäksi Google aikoo vahvistaa asemaansa hakukoneen AI-toiminnoilla sekä nopeasti kasvavalla Gemini-sovelluksellaan, jota käytetään jo laajasti ympäri maailmaa jne.

10 tykkäystä

Tässä ei puhuta sinänsä kait dollarimääräisesti ainakaan vielä isoista summista, mutta on silti varmaan mielenkiintoinen uutinen.

Yhdysvaltain puolustusministeriö ottaa Googlen Gemini-tekoälymallin käyttöön ensimmäisenä Pentagonin uudella GenAI.mil-alustalla, joka on tarkoitettu kolmelle miljoonalle työntekijälle.

Mallia käytetään mm. taustatutkimukseen, dokumenttien muotoiluun ja myös kuva-analyysiin. No taustalla on jo kuitenkin Googlen aiempi 200 miljoonan dollarin AI-sopimus puolustusministeriön kanssa.

U.S. Defense Secretary Pete Hegseth said on Tuesday that the Department of Defense had chosen Alphabet Inc’s (NASDAQ:GOOGL) Gemini as the first model in an artificial intelligence platform for its three million employees.

11 tykkäystä

Sääntelyuhkasta uutiset varmasti väsyttävät täällä, mutta tässä on ihan hyvä kriittinen kirjoitus Alphabetin mahdollisuudesta Googlebotin avulla “ryövätä” koko internet AI-koulutukseen ilmaiseksi siinä missä muut maksavat siitä. Sen lisäksi kun AI-vastaus täytyy Googlen yläosan, jää käytännössä kaikki sivut pimentoon.

Ennen vanhaan vitsailtiin, että paras paikka piilottaa ruumis on laittaa se Google-hakujen toiselle sivulle. Nyt ei haittaa vaikka ruumis olisi ensimmäisen linkin paikalla, koska AI-vastaus peittää sen. ![]()

5 tykkäystä

Ennustan että ainakin yksi asia tapahtuu jollain aikavälillä:

Tapa sivustoille sallia Google-haun indeksointi mutta estää AI-treenausbotin nuuskiminen.

Tällä hetkellä nämä on bundlattu, ja sivustoilla ei ole mahdollisuuksia blokata vain AI-treenausta Googlelta. Ja hakuindeksoinnin blokkaus on käytännössä varmistus sille että kukaan ei koskaan tule sivullesi.

Muiden toimijoiden osalta AI-crawlerit voi blokata, ainakin teoriassa.

Toisaalta tässä on koko AI-palveluiden fundamentaalinen ongelma pähkinänkuoressa. Ne toimivat vain jos saavat treenata vapaasti kaikella mitä irti lähtee. Mutta sisältö tuottaville tahoille tämän salliminen tuhoaa heidän bisneksensä. Tähän pitää löytyä jollain aikavälillä joku ratkaisu koska muuten joko AI-botit blokataan kaikesta sisällöstä tai kaikki sisällöntuotanto loppuu koska se ei enää ole taloudellisesti kannattavaa, kun ainoa lukija on AI-treenausbotti ja ihmiset lukevat tavaran AI-palvelusta.

10 tykkäystä

Olen seurannut mielenkiinnolla robotaxien kehitystä ja Waymon skaalautumista. Waymoa on povattu robotaxeissa häviäjäksi, koska se ei voi skaalautua niin kuin Tesla. Tällä hetkellä kuitenkin näyttää siltä, että Waymoon laajentuminen onnistuu hyvin.

https://www.cnbc.com/amp/2025/12/08/waymo-paid-rides-robotaxi-tesla.html

Vuodessa viikottaiset kyydit ovat kasvaneet 150k kyydistä 450k kyytiin. Tässä varmasti myös kulut kasvavat, koska autot ovat kalliimpia kuin Teslan vastaavat, mutta uskon edelleen, että Waymo pystyy puskemaan kustannuksia merkittävästi alemmas toiminnan laajentuessa. Waymolla on myös ensimmäisen liikkujan etu eli saa markkinoita haltuun muilta ja brändin kuluttajien mieliin. Mielenkiintoista!

12 tykkäystä

Google DeepMind aikoo avata ensimmäisen ”automaattisen tutkimuslaboratorionsa” Britanniaan ensi vuonna.

Laboratoriossa yhdistetään tekoälyä ja robotiikkaa uusien suprajohteiden ja puolijohdemateriaalien kehittämiseen.

Brittiläiset tutkijat saavat etuoikeuden päästä DeepMindin edistyneisiin AI-työkaluihin, ja myöhemmin yhteistyö voi laajentua mahdollisesti esimerkiksi ydinfuusion tutkimukseen. Hanke on osa Iso-Britannian strategiaa vahvistaa maan tekoälyosaamista.

https://www.cnbc.com/2025/12/11/googles-ai-unit-deepmind-announces-uk-automated-research-lab.html

5 tykkäystä