Alphabet

Kaliforniassa Yhdysvalloissa majaa pitävä Alphabet, joka tunnetaan paremmin Google-nimellä, perustettiin vuonna 1998 Larry Pagen ja Sergey Brinin toimesta. Alunperin se oli hakukoneprojekti yliopistolla, mutta kasvoi nopeasti maailman suurimmaksi hakukoneeksi ja verkkomainostajaksi.

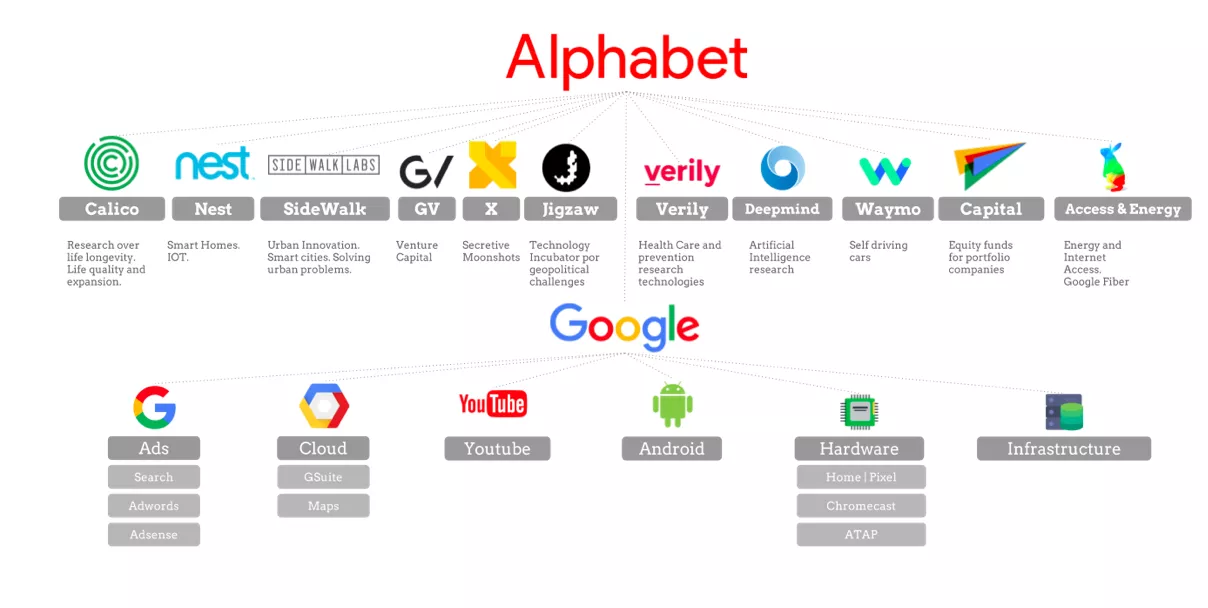

Vuonna 2004 yhtiö listautui pörssiin ja vuotta myöhemmin Google laajensi palveluitaan hankkimalla Androidin sekä lisäämällä tarjontaansa Gmailin, Google Mapsin ja YouTuben. Vuonna 2015 Google uudelleenorganisoi itsensä Alphabetiksi, joka toimii emoyhtiönä useille tytäryhtiöilleen. Lisäksi Alphabetin muut palvelut kuten Waymo (itsenäinen ajamisen teknologia), Verily (biolääketiede), ja Calico (ikääntymisen vastainen tutkimus) ovat myös kasvaneet vuosien saatossa. Merkittävää potentiaalia löytyy myös tekoälystä ja pilvipalveluista, joiden kehittämistä yhtiö jatkaa aktiivisesti.

Nykyään Alphabet hallitsee digitaalista maisemaa, johon ei voi olla törmäämättä lähes kaikkialla. Alphabet on maailman neljänneksi arvokkain yhtiö karvan alle 2 biljoonan dollarin markkina-arvollaan. Vuoden 2004 lopulla Alphabettiin sijoitettu euro olisi tämän päivän noteerauksella arvoltaan noin 7200 euroa. Vaikka maailmalta löytyy vielä hurjempiakin kurssiraketteja, on tämän yhtiön kyydissä kannattanut pysyä mukana.

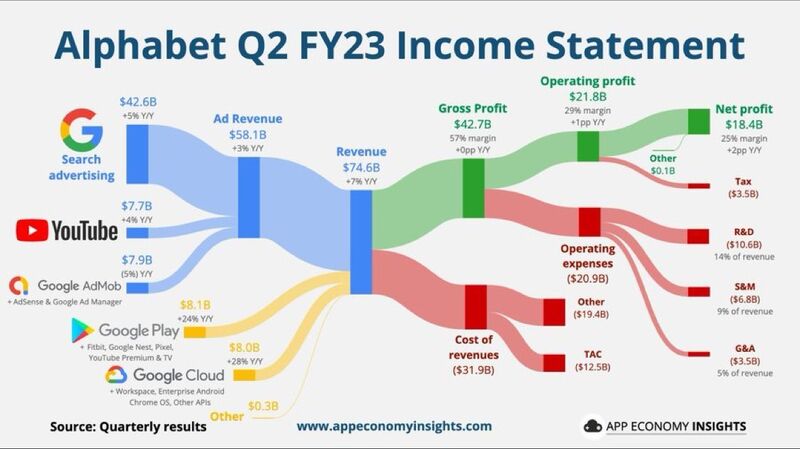

Alphabetin tärkein tulonlähde, kuten arvata saattaa, on Googlen mainostulot, joita yhtiölle tuli viime vuonna hieman vajaat 43 miljardia usd. Kasvu tässä segmentissä on kuitenkin hidastunut ja uusia kasvuaihioita odotetaankin nousevan mm. pilvipalveluista. Yhtiön kannattavuus on pysynyt hyvällä tasolla nettomarginaalin heiluessa viimeisten 15 vuoden aikana pääasiassa 20-30 %:n välimaastossa.

Tekoälyllä höystetyn Google haun ja YouTuben kasvu on ollut merkittävä tekijä yhtiön menestyksessä. Tekoäly ja koneoppiminen ovat mullistaneet haun ja sisällön suositukset, tehden niistä henkilökohtaisempia ja osuvampia käyttäjille. Tämä on lisännyt käyttäjien sitoutumista, klikkausmääriä ja mainostuloja. Myös Google Lensin ja YouTuben automaattisen tekstityksen kaltaiset ominaisuudet ovat parantaneet käyttäjäkokemuksia.

Vaikka kilpailu on kovaa, Alphabetin valtava käyttäjädatan määrä erottaa sen kilpailijoistaan. Yhtiö kerää dataa monista lähteistä, kuten Google hausta, YouTubesta, Gmailista ja Android-laitteista. Tämä data antaa arvokasta tietoa käyttäjien käyttäytymisestä ja trendeistä, mahdollistaen tuotteiden ja palveluiden räätälöinnin sekä kohdennetut mainokset. Voi siis sanoa, että Alphabetin 90 % markkinaosuus hakukoneissa antaa sille ainutlaatuisen kilpailuedun.

Tulevaisuuden potentiaalia löytyy myös Gemini LLM:stä, sillä seuraavan sukupolven kielimallin odotetaan olevan tehokkaampi ja monipuolisempi kuin kilpailijoilla, tarjoten multimodaalisia ominaisuuksia ja käsitellen laajoja asiakirjoja ja koodirivejä. Mallin odotetaan siis ottavan ominaisuuksiltaan kiinni ChatGPT:tä.

Miltä osakkeen arvostus sitten näyttää tällä hetkellä? Tulospohjainen arvostus vaikuttaa historialliseen keskiarvoon nähden kalliin puoleiselta vaikkakin kovempiakin kertoimia on Alphabetistä maksettu. Mikään vuosikymmenen ostopaikka ei kuitenkaan kertoimien valossa ole käsillä, mutta toisaalta tekoälyn luomia kasvumahdollisuuksia voi olla vielä vaikea hahmottaa, ja analyytikot ovatkin viimeisen vuoden aikana nostaneet lähivuosien ennusteitaan useampaan otteeseen. Sen sijaan loppuvuodesta 2022 osaketta pääsi jälkikäteen tarkasteltuna ostamaan varsin edulliseen hintaan. Tämän vuoden ennusteilla Alphabettiä arvostetaan P/E 23.4x ja ensi vuoden ennusteilla 20.6x, kun kannattavuuden odotetaan edelleen kohenevan samalla kun myös kasvun odotetaan olevan matalalla kaksinumeroilla tasolla, mikä tarkottaisi varsin kovaa tuloskasvua. Myös pääoman tuoton odotetaan säilyvän tulevina vuosina n. 23-30 % haarukassa.