Olen viime aikoina yrittänyt paneutua yhtiöön ja sitä kautta teknologiaan, joka on mielestäni liian tärkeä/tarpeellinen epäonnistumaan. Jo näin ajatteleminen on sen tason punainen lippu, että haluaisin mielelläni kuulla näkevätkö muut tilanteen samalla tavalla. On vielä asia erikseen kuuluuko kyseinen yhtiö tämän muutoksen voittajiin, mutta uskon teknologian käyttöönottoon keskipitkällä aikavälillä, koska kaikkea ei heti saa päästöttömäksi, ja Pariisin ilmastokokouksessa sovittu maali siirtyy yhä kauemmas.

Yhtiöllä on jo tämä ketju, joka on viime aikoina ehkä vähän väljähtänyt aktiivisten kirjoittajien, ja ehkä myös sijoittajien, puu(t)tuessa. Tätä selvittäessä myös tuntui, että uudella sijoittajalla on aika työ karsia kaikki tieto kasaan, joten aloituskynnys on luotaantyöntävä. Veikkaan hiljaisuuden liittyvän osaltaan myös siihen, ettei IPO:a seurannut lähtö ollut kovin vauhdikas ja alun innostus on muuttunut realismiksi, jossa odotellaan sekä lainsäädännön hyväksyntää tekniikalle että hinnan asettumista houkuttelevalle tasolle. Mielestäni tämän osalta on kuitenkin tapahtunut paljonkin.

Koska en voi tehdä yhtiölle uutta aloitusta, kokeilen tehdä uudelleenkäynnistyksen ja samalla jäsentää itsellenikin näkemystä yhtiön kokonaistilanteesta. Jos lafka tämän myötä osoittautuu uudeksi Theranosiksi, tulen pääsemään tästä vielä nollatuloksella ulos. Koska kuitenkin päädyin tekemään tämän, ei odotuksiani yhtiön potentiaalista tarvitse varmaan erikseen tuoda esiin. Siispä pidemmittä puheitta…

Tekstissä käytettyjä lyhenteitä lyhyesti avattuna:

CCS – Carbon capture and storage – Hiilensidonta (CO2) + varastointi

CCU – Carbon capture and utilization – Hiilensidonta (CO2) ja hyötykäyttö

CCUS – Kahden ylemmän yhdistelmä, joka sisältää koko mahdollisen arvoketjun

W2E - Waste to energy. Jätettä polttava voimalalaitos.

BECCS - Bioenergy with carbon capture and storage. Biomassan poltosta voimalaitoksessa syntyvän hiilidioksidin talteenotto. Keino vähentää kasvien sitoman CO2:n määrää kierrossa.

EU ETS - EU:n päästökauppajärjestelmä, jossa vuosittain kiristyvä kokonaispäästöraja sekä toimijakohtainen historiaan perustuva päästökiintiö. Päästökiintiön täytyttyä toimija joutuu ostamaan päästöoikeuksia päästökauppajärjestelmästä, jossa päästöoikeuden hinta määräytyy kysynnän ja tarjonnan mukaan.

FEED – Front-end Engineering Design -sopimus, joka sisältää alustavat suunnitelmat. Sopimuksen voittaja tuottaa tekniset määrittelyt ja vaatimukset projektille, arvioi projektin keston ja hinnan ja suunnitelmallaan pienentää projektin seuraaviin vaiheisiin liittyviä riskejä. Tämän saaminen ei vielä tarkoita koko projektin voittamista.

PDP – Process Design Package on FEED:n kanssa samaan vaiheeseen kuuluva sopimus, jossa tuotetaan prosessi- ja teknologiatietoa seuraavia vaiheita varten. Kohdistuu enemmän varsinaiseen prosessitekniikkaan, kun taas FEED sisältää myös maa- ja vesirakentamista sekä muuta projektin ympärille liittyvää. PDP onkin usein FEED:n osa.

EPC – Engineering, procurement and construction -sopimus on käytännössä projektin toteutusvaihe, johon pääseminen tarkoittaa samalla tarjouskilpailun voittamista.

FID - Final investment decision. Lopullinen investointipäätös, jonka jälkeen projektin toteutus saa vihreän valon.

ktpa = kilotonnia CO2 per annum. Vuodessa siepatun hiilidioksidin määrä tuhansissa tonneissa.

mtpa = miljoonaa tonnia per annum. Vuodessa siepatun hiilidioksidin määrä miljoonissa tonneissa.

IRA = Inflation Reduction Act. USA:ssa 2022 voimaan tullut liittovaltion laki, joka liittyy aiheeseen lähinnä uusiutuvan energian projekteihin liittyvien tukiensa kautta.

Yhtiö ja tuotteet

Kuten aloituksessakin mainittiin, Aker Carbon Capture ASA on hiilensidontaan ja varastointiin erikoistunut pure play -yhtiö, joka on saanut alkunsa Norjalaisesta Aker-konsernista irronneena spin-offina vuonna 2020. Yhtiön päätoimialueet ovat Pohjoismaat, Länsi-Eurooppa sekä USA. Työntekijöitä reilu 200.

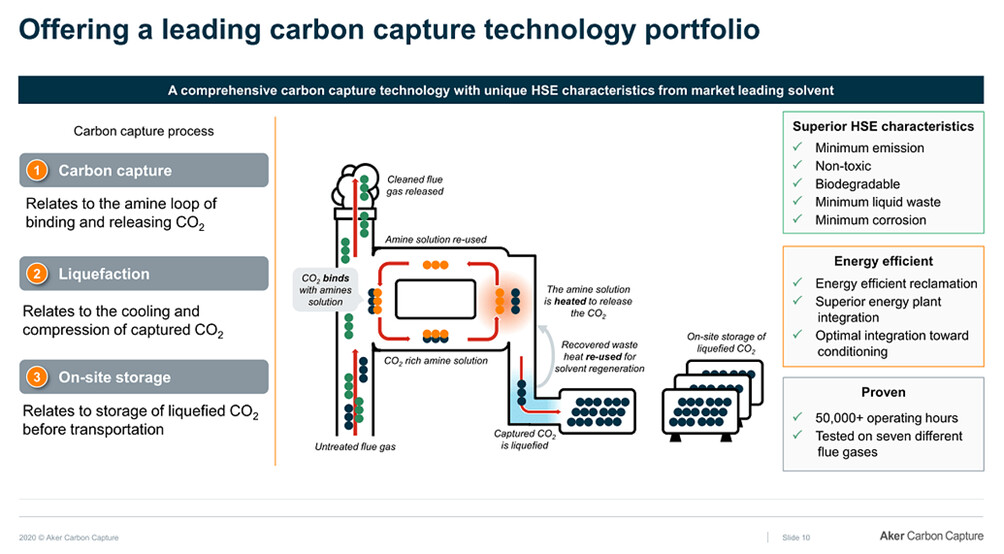

Yhtiön oma asiantuntemus tiivistyy palamisenjälkeiseen hiilensidontaan (Post-combustion carbon capture), jossa yhtiö käyttää patentoitua amiinipohjaista liuotinteknologiaa, joka sitoo hiilidioksidin ja vapauttaa sen kuumennettaessa. Yhtiö muistaa joka välissä mainita amiiniliuottimensa HSE-ominaisuudet: liuotin on pitkäikäinen ja hiottu savukaasujen epäpuhtauksia hyvin sietäväksi, mikä vähentää ei-toivottuja sivureaktioita. Hiilidioksidi kyetään poistamaan savukaasuista noin 90-95%:sti ja erotetun hiilidioksidin puhtaus on yli 99 %, joissain lähteissä jopa 99,9 %. Teknologiaa on 2023 Q4 lopulla testattu 11 eri savukaasutyypillä yhteensä yli 60 000 tunnin ajan.

Eristetty hiilidioksidi yleensä joko varastoidaan lopullisesti, jolloin terminä on CCS (Carbon capture and storage) tai käytetään hyödyksi muualla, jolloin kyseessä on CCU (Carbon capture and utilization). Uudelleenkäyttökohteita ovat esimerkiksi hiilidioksidin käyttö yhdessä vedyn kanssa e-metanolin, e-metaanin tai e-kerosiinin valmistuksessa tai esim. suora käyttö kasvihuoneteollisuudessa kasvuaineena. Hiilensidonnan kohteena ovat lähinnä vaikeasti vihreiksi muutettavat teollisuudenalat, kuten sementtiteollisuus (8% maailman hiilidioksidipäästöistä), jätteenpolttolaitokset, terästeollisuus ja sinisen vedyn valmistus.

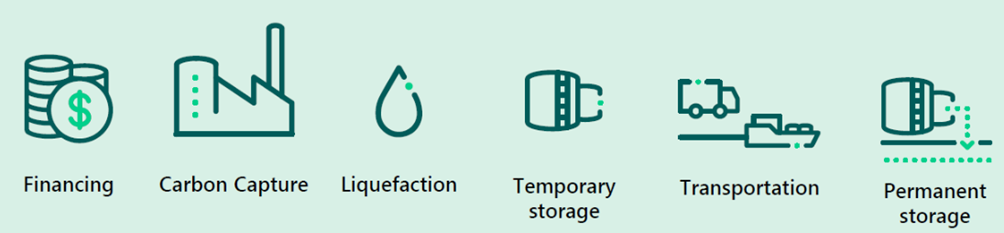

Yhtiö myy hiilensidontalaitoksiaan erilaisina avaimet käteen -paketteina sekä koko arvoketjun sisältävänä käyttöoikeuspalveluna (Carbon Capture as a Service), jossa asiakas maksaa kiinteän summan per sidottu tonni CO2:ta. Käyttöoikeuspalvelussa varsinainen hiilensidontalaitos ja sen ylläpito tulevat ACC:lta ja loput arvoketjusta yhteistyökumppaneilta. CCUS arvoketju sisältää hiilensidonnan, väliaikaisvarastoinnin, kuljetuksen sekä tilanteesta riippuen joko lopullisen varastoinnin tai hyötykäytön.

Yhtiö on päätynyt tarjoamaan myös käyttöoikeuspalvelumallia, koska CCUS on laaja kokonaisuus, eikä yhtiöllä tai useimmilla sen asiakkaista olisi yksin rahkeita koko ketjun kattamiseen. Suurimmalle osalle asiakkaista CCUS on lisäksi uusi konsepti, joka vaatii suunnittelua, suuria etukäteisinvestointeja, erillisiä sopimuksia arvoketjun eri askelmilla sekä erilaisia fyysisiä rajapintoja matkalla hiilensidonnasta lopulliseen varastointiin tai hyötykäyttöön. Tarjoamalla koko ketjun palveluna yhtiö pyrkii tekemään monivaiheisesta ketjusta helpommin lähestyttävän. Käyttöoikeuspalvelu on vaihtoehdoista kalliimpi, joten odotan tämän yleistyvän kunnolla vasta päästöoikeuksien hintojen myöhemmän nousun myötä. Myös kuljetus- ja varastointivaihtoehtojen vähäinen tarjonta rajoittaa palvelun tarjoamista. Tilanne helpottuu, kun ala kypsyy hieman lisää.

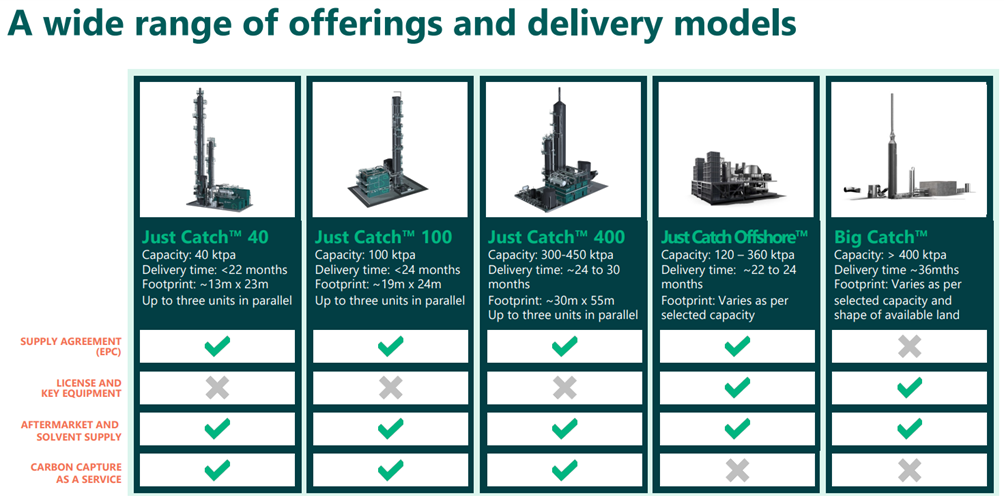

Tuoteportfolioon kuuluu yhteensä 5 eri hiilensieppauslaitosta, joista kolme ensimmäistä ovat modulaarisia ja yhdisteltävissä suuremmiksi kokonaisuuksiksi.

Yhtiöllä on myös testiyksikkö, mobile test unit (MTU), joka on siirreltävissä maasta toiseen, ja jonka mukana kulkee oma testitiimi. Sen avulla potentiaalinen asiakas pääsee testaamaan laitteistoa livenä omassa laitoksessaan ja operatiivinen riski pienenee. Yksikkö onkin ollut sen verran suosittu, että ACC on päättänyt rakentaa toisenkin MTU:n, joka on kohta valmis (tilanne Q4-2023). Esim. uusien savukaasutyyppien testaus onnistuu MTU:lla kätevästi.

Projektit ja tulevaisuudennäkymät

Yhtiön pörssitiedotteista piirtyy selvä ja suunnitelmalliselta vaikuttava kehityskaari. Koska yhtiö on hyvin spesifin alan toimija, se on pyrkinyt osaksi suurempia kokonaisuuksia. Ensimmäisinä vuosina yhtiö sopi paljon yhteistyökuvioita eri alojen toimittajien kanssa (ohjelmisto-, kaasuturbiini- ja voimalaitostoimittajat, sinisen vedyn valmistuslaitteistojen tuottajat, hiilen varastointiyritykset yms.), joiden tarkoituksena oli kehittää ja integroida tekniikkaa sekä mahdollistaa CCUS-pakettien tarjoaminen yhdessä muiden CCUS-arvoketjuun kuuluvien yritysten kanssa. Yhteistyökumppanihin kuuluvat esim. Microsoft, MAN Energy Solutions, Siemens Energy, Haldor Topsoe, Hitachi Zosen Inova, Carbonor, Carbfix sekä tietenkin Northern Lights JV, Norjan julkis-yksityinen hiilidioksidin varastointiprojekti.

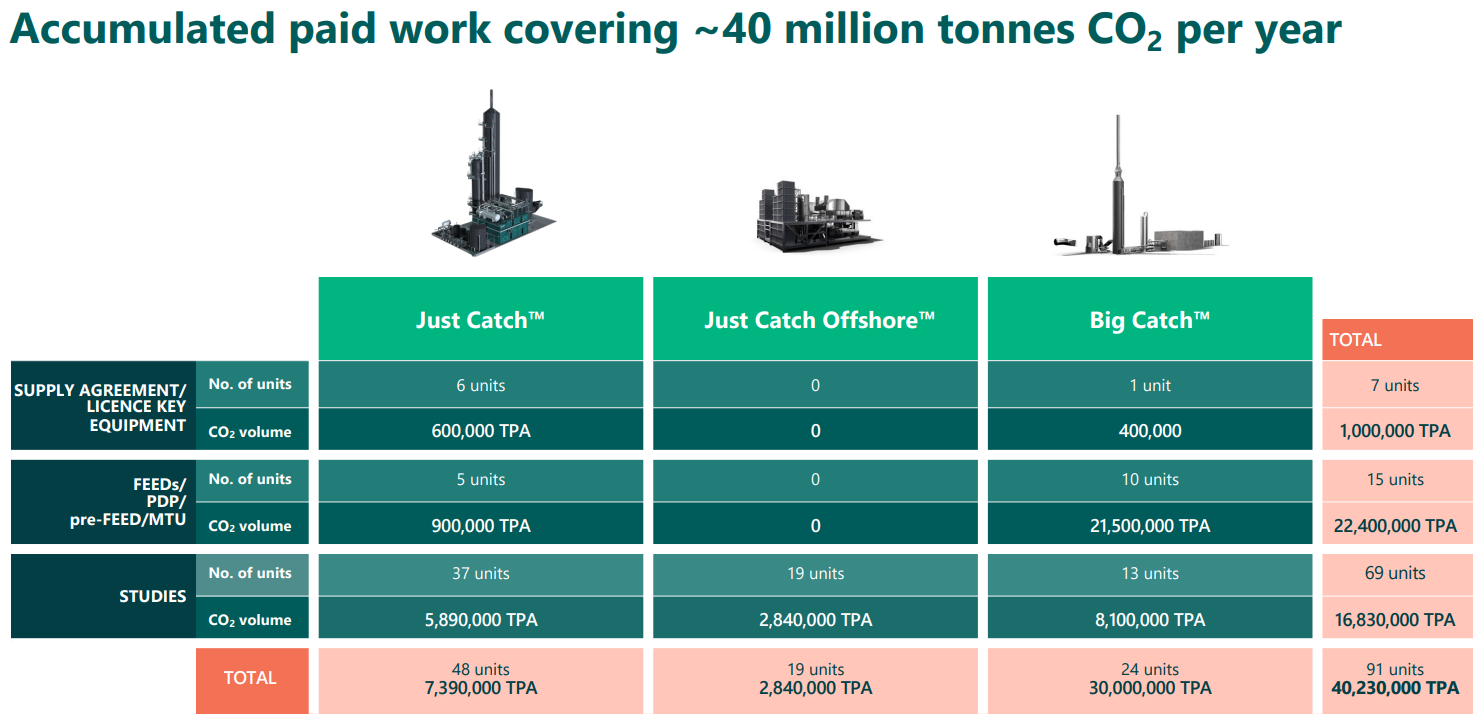

Noin viimeisen vuoden aikana eri suunnittelusopimukset ovat varastaneet uutistilan, minkä tulkitsen uuteen vaiheeseen siirtymisenä. Yhtiö on viimeisen 6 kk aikana saanut enemmän FEED- ja PDP-sopimuksia sekä feasibility studyjä kuin koko aiemman 2020 alkaneen historiansa aikana. En suostu laittamaan tätä kaikkea sattuman piikkiin, vaan uskon tämän johtuvan myös markkinan heräämisestä, mikä myös Q4 webcastissa tuotiin ilmi. Yhtiö on itsenäisenä yrityksenä olonsa aikana kerännyt kehitysputkeen suunnitteluprojekteja yli 40 mtpa:n edestä, joista yli 20 mtpa tuli vuoden 2023 aikana.

Yhtiö onkin alkavana vuonna mielestäni tähänastisen historiansa mielenkiintoisimmassa vaiheessa. Ensimmäiset oikeat laitokset, jotka toimittavat samalla referenssilaitosten virkaa, ovat valmistumassa tänä vuonna: Twencen jätteenpolttolaitoksen CCU Hollannissa on käynnistysvaiheessa ja Brevikin sementtilaitoksen CCS Norjassa on suunnitelman mukaan valmistumassa kesällä. Vaikka tekniikkaa on mobile test unitin avulla testattu useammalla eri savukaasutyypillä ja toimivaksi havaittu, antaa kokonaisten laitosten toimittaminen yhtiölle ihan uudenlaista uskottavuutta.

Käyn alla läpi yhtiön projekteja, joilla on lähitulevaisuudessa mahdollisuus saada lopullinen investointipäätös, mikä käytännössä tarkoitaa vain olemassaolevia FEED-sopimuksia.

USA

Yhtiö kiinnostui IRA-paketin 2022 myötä parantuneista toimintaedellytyksistä ja perusti toimiston Houstoniin sekä solmi yhteistyösopimuksen MAN Energy Solutionsin kanssa Yhdysvaltojen markkinapreesensin edistämiseksi. Joitain FEED-tutkimuksia menossa, mutta ei todennäköisiä FIDejä vuodelle 2024 (tieto Q4 webcastista).

UK

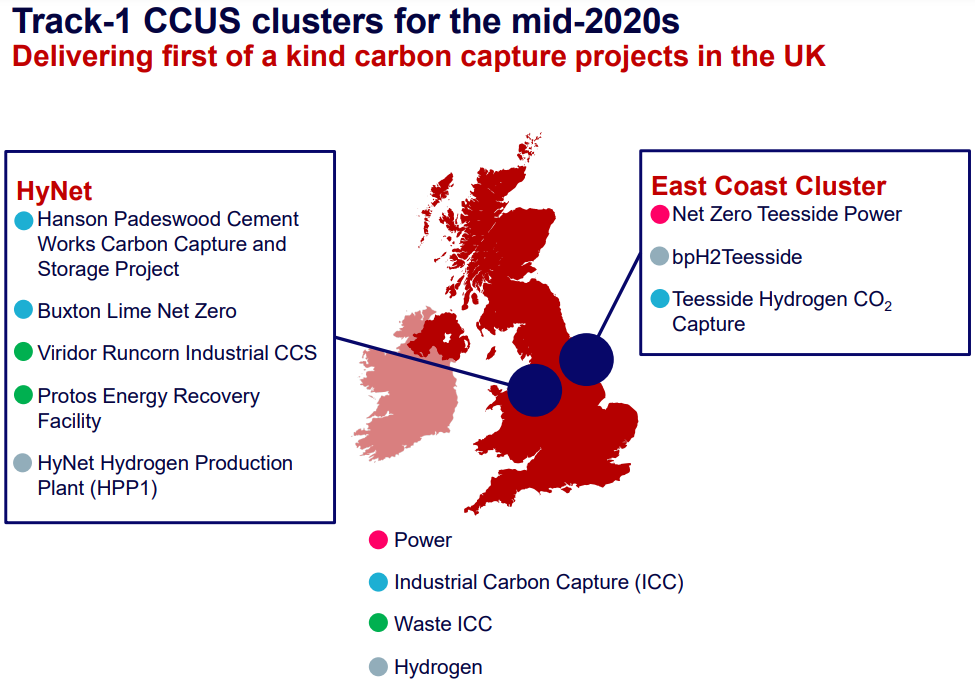

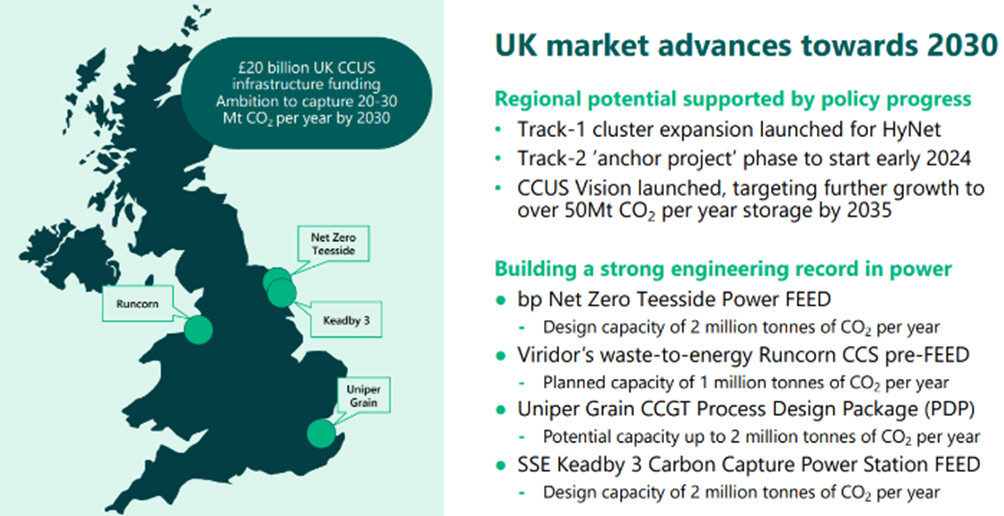

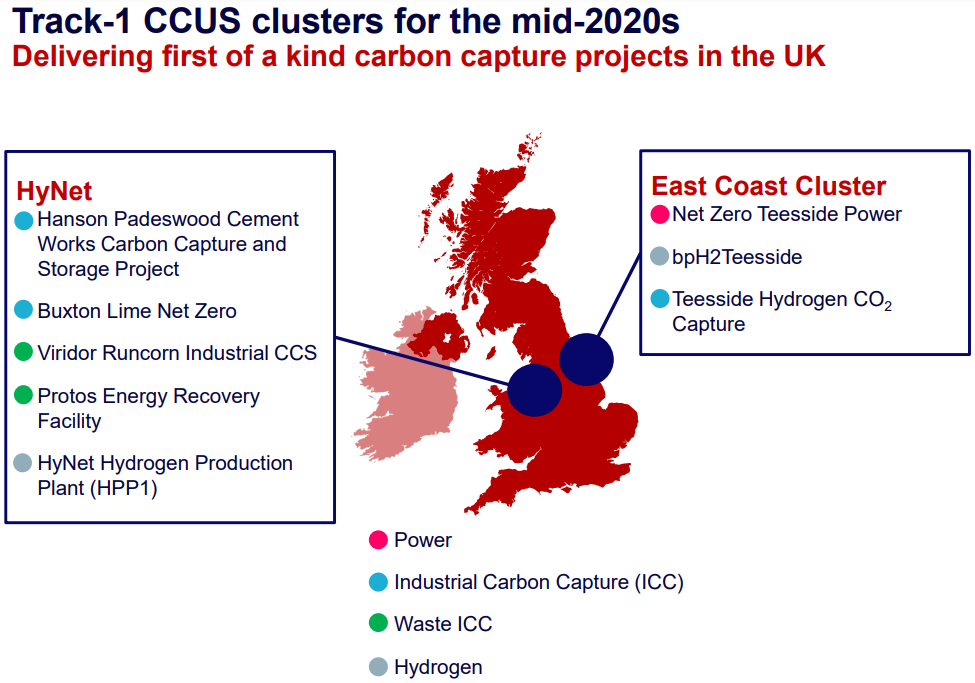

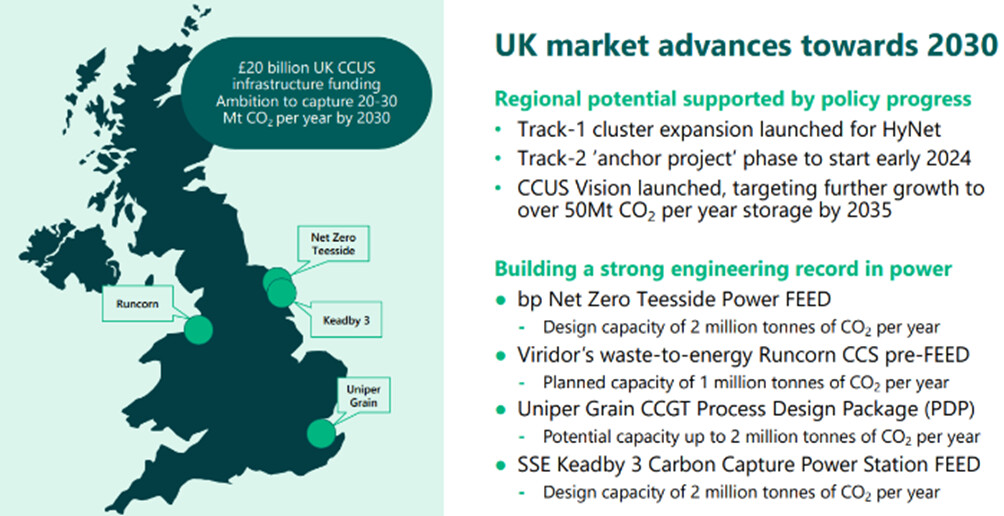

Britanniassa on meneillään hallituksen käynnistämä laaja ja taloudellisesti tuettu CCUS-projekti, johon päästäkseen yritykset lobbaavat ankarasti. Sen tarkoituksena on saattaa CCUS käyttöön minimissään kahteen teollisuusklusteriin vuoden 2025 puoliväliin mennessä (projektinimeltään Track-1) ja neljään muuhun vuoteen 2030 mennessä (Track-2). Tähän väliin on perustettu vielä Track-1 Expansion. Koko projektin suuruusluokka on 20-30 mtpa CO2 vuoteen 2030 mennessä ja sille on myönnetty 20 miljardin punnan tuki. Britannian teollisuusklustereista HyNet sekä East Coast Clusterien on vahvistettu kuuluvan Track 1:een, joka on ensimmäinen toteutettavista aalloista. Sen jälkeen tulee mahdollisesti Track 1 expansion ja ainakin Track 2. Projektin käynnistys on hieman viivästynyt, mutta Q4 webcastin mukaan ensimmäiset ACC:hen liittyvät FID:t tullaan näkemään syksyllä 2024.

Alla vielä FID-lotto Britannian projektien osalta perustuen löytämiini tietoihin.

| Projekti | FID-veikkaus | Peruste |

|---|---|---|

| bp Net Zero Teesside (G2P) | Syksy 2024 | Kuuluu UK Track 1 & Webcast Q4 Q&A |

| SSE Keadby 3 (G2P) | Syksy 2024 | Kuuluu UK Track 1 & Webcast Q4 Q&A |

| Uniper Grain (CCGT) | 2025-2026 | https://newsweb.oslobors.no/message/606430 & PDP menossa, jonka jälkeen vielä FEED, joka yleensä kestää noin vuoden. |

| Viridor Runcorn CCS (W2E) | 2024-2025 | Kuuluu UK Track 1, joten FID voi tulla jo syksyllä 2024, mutta nyt vasta pre-FEED käynnissä. Tarvitaanko lisäsuunnittelua? |

Näistä pienimmänkin laitoksen EPC-sopimuksen voittaminen toisi kaikkien kolmen työn alla olevan CCUS-laitoksen verran uutta kapasiteettia. Yhteensä Britanniassa voitettujen suunnittelusopimusten kautta voisi olla tulossa jopa 7 mtpa:n verran uutta kapasiteettia verrattuna kolmen jo voitetun sopimuksen myötä nyt rakenteilla olevaan 1 mtpa:an.

Eurooppa

Eurooppa, etenkin Pohjois-Eurooppa, on yhtiön päämarkkina-aluetta, jossa sillä onkin jo kolme projektia työn alla. Näiden lisäksi listalta löytyy neljä FEED-vaiheessa olevaa projektia.

| Projekti | FID-veikkaus | Peruste |

|---|---|---|

| Söderenergi Igelstaverket (BECCS) | 2024-2025 | FEED aloitettu 26.06.2023, joten FID periaatteessa mahdollinen 2024 loppupuolella. |

| Hafslund Oslo Celsio (W2E) | 2025 | FEED aloitettu 24.11.2023. Q4 raportissa mainittu, että FID tavoitteena 2024 kesällä. |

| Nordbex AB (BECCS) | 2025 | FEED aloitettu 08.02.2024, joten FID tuskin tulee vielä 2024 aikana. |

| Eurooppalainen toimija, CCS yhteensä 4:ään BECCS- ja W2E-laitokseen. | Aikaisintaan 2025 | Feed aloitettu 22.02.2024. Neljä laitosta, iso kokonaisuus. Luultavasti tehdään osissa, laitos kerrallaan, monta FID:ia. |

Yhtiön menestysmahdollisuudet tullaan lähivuosina mittaamaan voitettujen projektien määrällä. Se joutuukin nyt tarjouskilpailujen myötä testaamaan teknologiansa ja hintatasonsa alan muita toimijoita vastaan. Esimerkiksi Net Zero Teesside -projektissa on kaksi kilpailevaa konsortiota:

- Aker Solutionsin johtama konsortio, johon kuuluu Aker Solutions, Doosan Babcock sekä Siemens Energy. CC-teknologia ACC:lta.

- Technip Energiesin johtama konsortio, johon kuuluu Technip Energies ja General Electric. CC-teknologiana Shellin CANSOLV CO2, joka myös amiiniliuottimeen perustuva.

Tekniikan TAM on ihan järkyttävän suuri, koska tulevaisuuden tavoitteena on olla hiilinegatiivinen. USA:ssa IRA:n tuomien lisätukien myötä CCUS:n kapasiteetin on arveltu voivan kasvaa 2030 mennessä vuotuiseen 200 mtpa:an. EU:n tämänhetkinen tavoite on, että vuosikymmenen loppuun mennessä sidotaan 50 mtpa:n verran ja vuoden 2040 lopulla jo 280 mtpa. Tuista tarkemmin seuraavassa kappaleessa.

Julkisuuden keskustelu vihreästä siirtymästä on värittynyttä, koska useimmilla on siihen liittyvä agenda tai ideologia: (vain hieman) karrikoiden vihreän siirtymän puristit, joiden mielestä ainut oikea vihreä siirtymä on suoraan fossiilisista täysin uusiutuviin, eikä välimuotoja hyväksytä, koska CCUS:kin on vain kakkosluokan ilmastotoimi, keino olla tekemättä välttämättömiä muutoksia. Toisella puolella öljy-yhtiöt ovat perinteisesti ja keskimäärin olleet CCUS:n puolella, koska sen käyttö vaatisi yhtiöiltä pienempiä rakennemuutoksia tulevaisuudessa ja mahdollistaisi lähes entisenlaisen toiminnan.

Olen kuitenkin viime aikoina internetin teelehdistä tulkinnut etenkin EU:n puheidensa kautta myöntäneen, että Pariisin ilmastosopimuksen tavoitteita ei saavuteta ilman hiilensidontaa, ja EU on tähän liittyen tehnytkin uusia CCUS:a puoltavia keskustelunavauksia. Tulkintani mukaan CCUS on siis tulossa yhä vahvemmin osaksi ilmastotyökalupakkia, enkä näe tässä ongelmaa, jos sitä käytetään sitomaan päästöjä vaikeasti korvattavilla teollisuudenaloilla, kuten yhtiö on tekemässä.

Elefantti olohuoneessa: hinta (ja tuet)

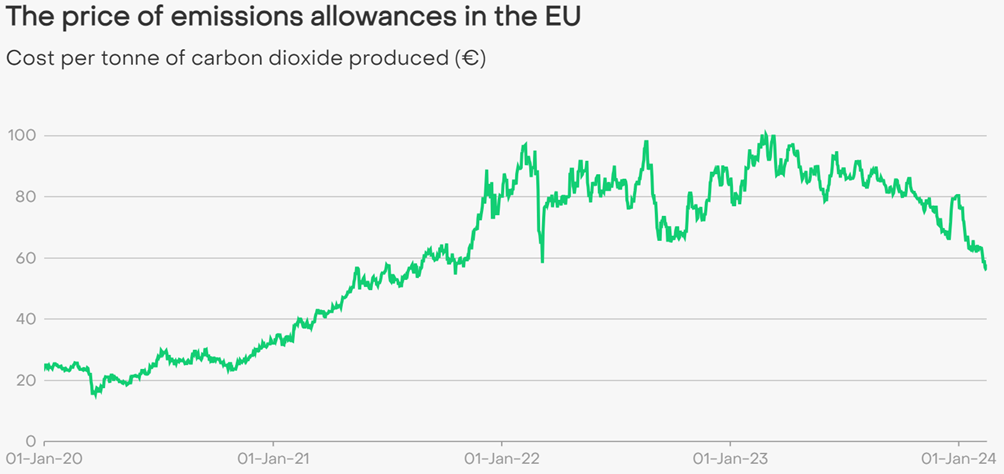

Teen heti selväksi, että CCUS ei tule isossa mittakaavassa realisoitumaan ilman rahallista keppiä ja/tai porkkanaa. Hinnalla on kaikista tekniikkaan liittyvistä tekijöistä varmasti merkittävin vaikutus hiilensidonnan tulevaisuuteen ja se on ollut pitkään yleistymisen esteenä yksinkertaisesti siksi, että yhden hiilidioksiditonnin sitominen on maksanut enemmän kuin sen vapauttaminen taivaalle. EU on luomallaan päästökauppajärjestelmällä luottanut enemmän keppiin kuin porkkanaan. Mekanismi, jolla päästökauppajärjestelmä on rakennettu, on viime vuodet vähentänyt vuosittain sallittujen hiilidioksiditonnien maksimimäärää 2,2 prosentilla, mikä pikkuhiljaa nostaa hiilidioksiditonnien keskimääräistä hintaa. Vuosittainen vähennys on tästä vuodesta (2024) alkaen kiristetty 4,3 %:iin. Vuonna 2018 hiilidioksiditonnin hinta oli keskimäärin 8€, kun se vuonna 2023 oli jo yli 80 €, joten nousu on vuositasolla ollut huomattavaa. Viime aikoina hinnat ovat taas hiipineet alaspäin, johtuen ainakin osittain Euroopan hiipuvasta taloudellisesta aktiviteetista. Päästökauppajärjestelmälle ei ole saatu sovittua alarajaa, joten taantumien aikaan, tuotannon hiipuessa, myös päästöoikeuksien hinnat laskevat, kun tupruttelijoilla tulee vähemmän päästökiintiöiden ylityksiä. Kaikille toimijoille on kuitenkin selvää, että keskimääräinen hinta on mekanismista johtuen pitkällä aikavälillä nouseva, mikä tekee hiilensidonnasta vuosi vuodelta houkuttelevampaa.

W2E-sektori ei vielä kuulu EU:n päästökauppajärjestelmään, mutta EU on jo tuonut julki aikeensa senkin integroinnista. Vuoden 2024 alusta W2E-toimijat joutuvat mittaamaan ja raportoimaan jätteenpolttolaitosten päästöt. 2026 alussa komission on määrä julkaista raportti, jossa W2E-sektori määrätään vuoden 2028 alusta mukaan päästökauppajärjestelmään jonkinlaisella kahden vuoden siirtymäajalla, eli viimeistään 2030. Toteutuessaan tämä tulisi olemaan merkittävä ajuri kohti CCUS:n käyttöönottoa Euroopassa.

EU:n porkkanaleiriä edustaa Innovation Fund, joka keskittyy suuria päästövähennyksiä tuottavien innovatiivisten teknologioiden ja lippulaivaprojektien tukemiseen. Esim. Twencen CCU-projekti on saanut rahastolta 14,3 MEUR tuen.

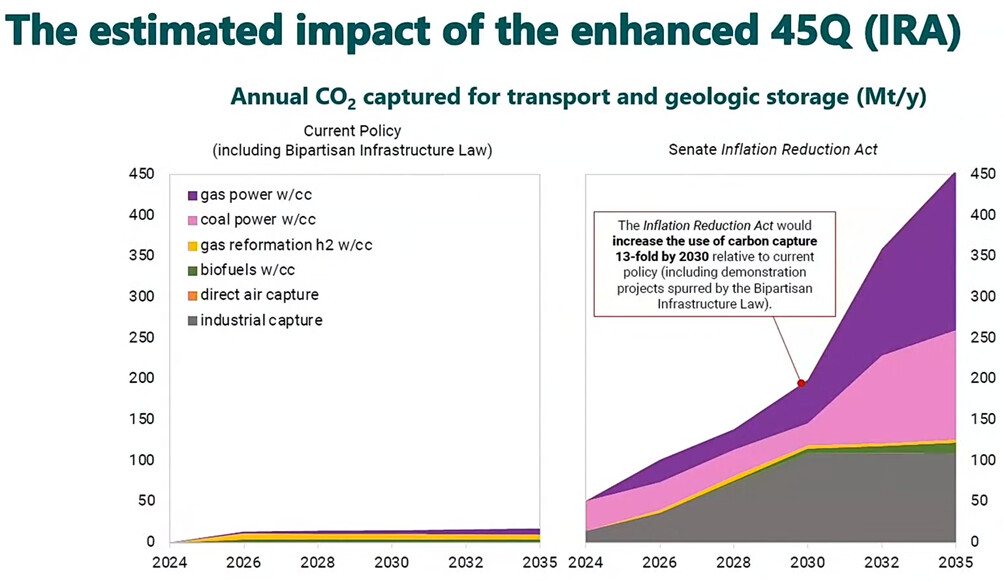

USA:ssa keppi on jätetty puuhun ja tarjolla on ainoastaan pussillinen porkkanoita. 2022 hyväksytty Inflation Reduction Act (IRA) nosti jo aiemmin voimassa olleen 45Q tax credit kannustinjärjestelmän korvauksia. Päivitetyssä 45Q:ssa CCU-projektille maksetaan 65$ per sidottu ja hyötykäytetty CO2-tonni. CCS-projekteille maksetaan 85$ per lopullisesti varastoitu CO2-tonni. Tämän lisäksi Bipartisan Infrastructure Investment and Jobs Act tarjoaa rahallista tukea CCUS-infrastruktuurin rakentamiseen. Lisäksi löytyy osavaltiokohtaisia kannustimia. Hidastavana tekijänä useimmissa osavaltioissa luvansaanti lopulliselle varastointisijainnille kestää 3 vuotta.

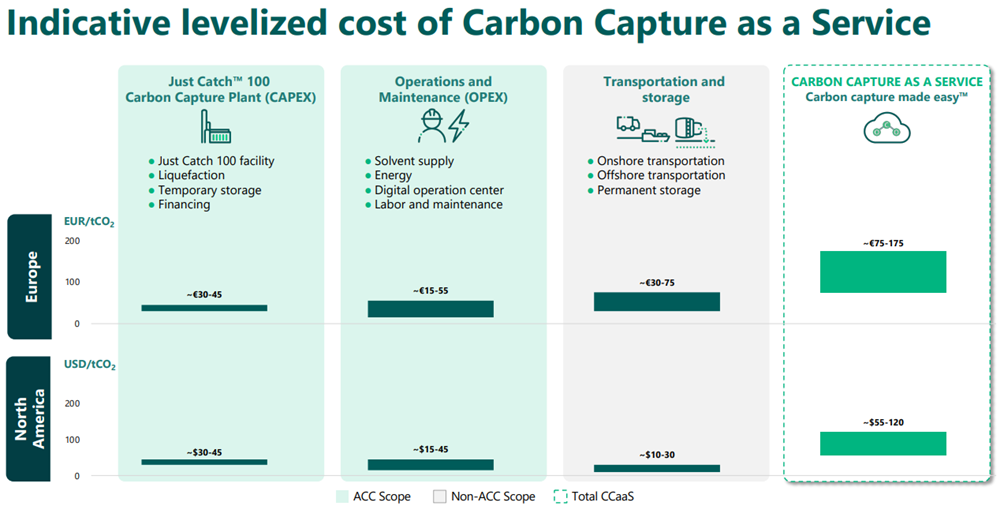

Alla olevassa kuvaajassa on vasemmassa ikkunassa CCUS arvioitu tilanne ennen IRA-pakettia ja oikeassa ikkunassa arvio ajasta IRA-paketin hyväksymisen jälkeen.

Alla ACC:n arvioimat hinnat toiminnan eri tasoille ja käyttöoikeuspalvelulle. Riippuen laitoksen integrointimahdollisuuksista ja toimitustason laajuudesta, alkaa CCUS olla etenkin USA:ssa erittäin houkutteleva vaihtoehto. Päästöoikeuksien hintojen trendi huomioiden myös Euroopassa uusien laitosten kannattaa ehdottomasti integroida CCUS jo suunnitteluvaiheessa. Hiilensidontayksikköjen toimitusaikojen ollessa lyhyimmilläänkin 2 vuotta, kannattaa vanhojenkin laitosten aloittaa suunnittelutyö jo nyt, koska päästöoikeuksien hinnat nousevat vuosi vuodelta. Alla vielä ACC:n arvioimat hintahaarukat per siepattu CO2-tonni eri toimitustasoilla.

Rahahommelit ja muita lukuja

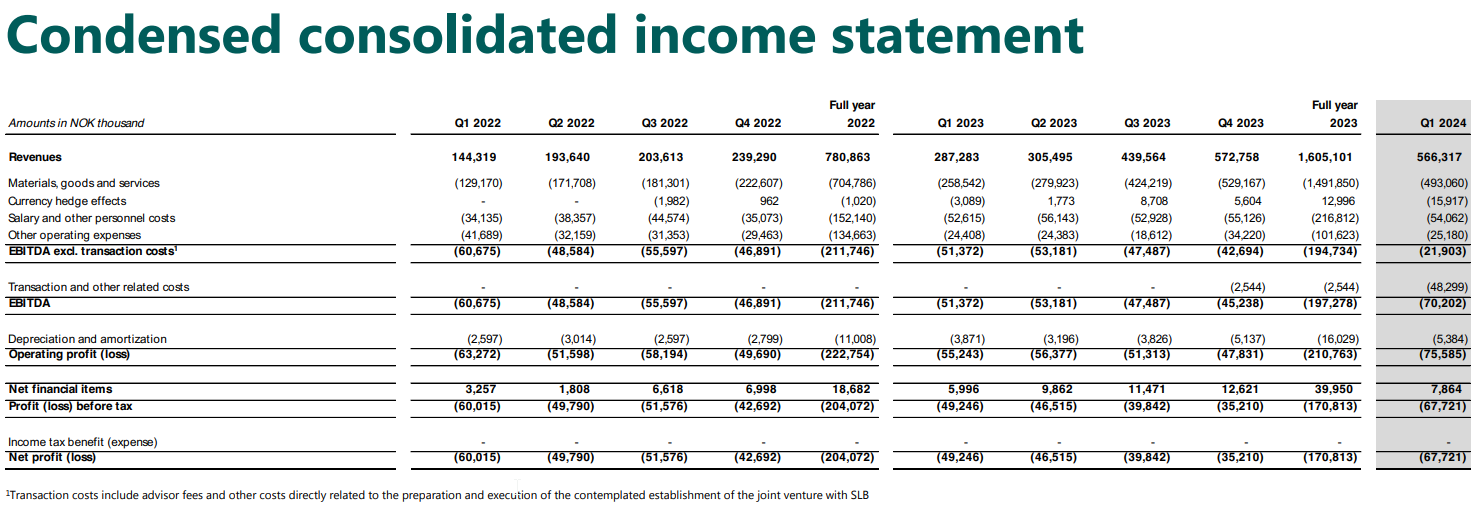

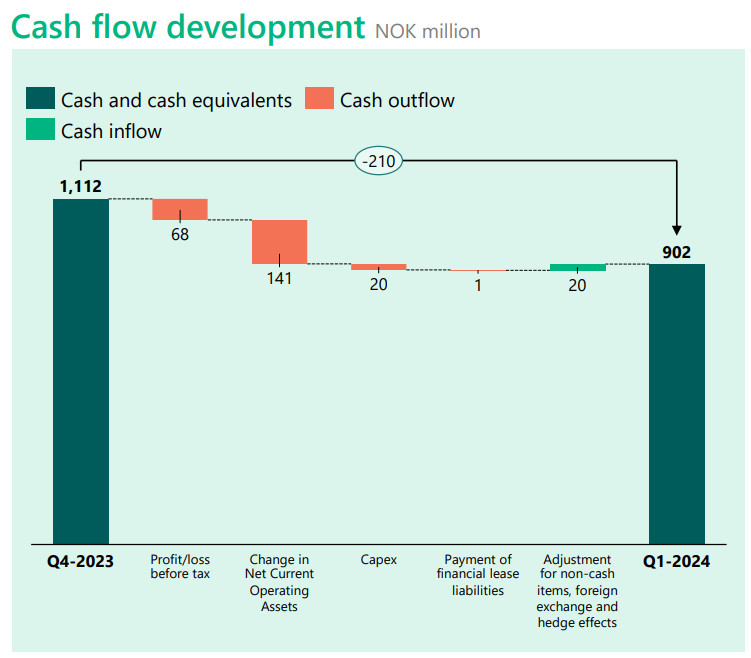

Yhtiö hoiti rahoituksensa balanssiin järjestämällä 2021 elokuussa 840 MNOK osakeannin hinnalla 22 NOK per osake, mistä lähtien se onkin ollut nettovelaton. Annin jälkeen 2021 Q3 lopussa yhtiöllä oli käteistä noin 1,4 miljardia NOKkia, eli noin 120 MEUR. Reilu kaksi vuotta myöhemmin, 2023 Q4 lopussa yhtiöllä on noin 1,1 miljardia NOKkia (~97 MEUR). Se ei ole tehnyt vielä kertaakaan voittoa, mutta rahanpolttelu on pysynyt aika hyvin hallussa, eikä akuuttia kassakriisiä ole näköpiirissä.

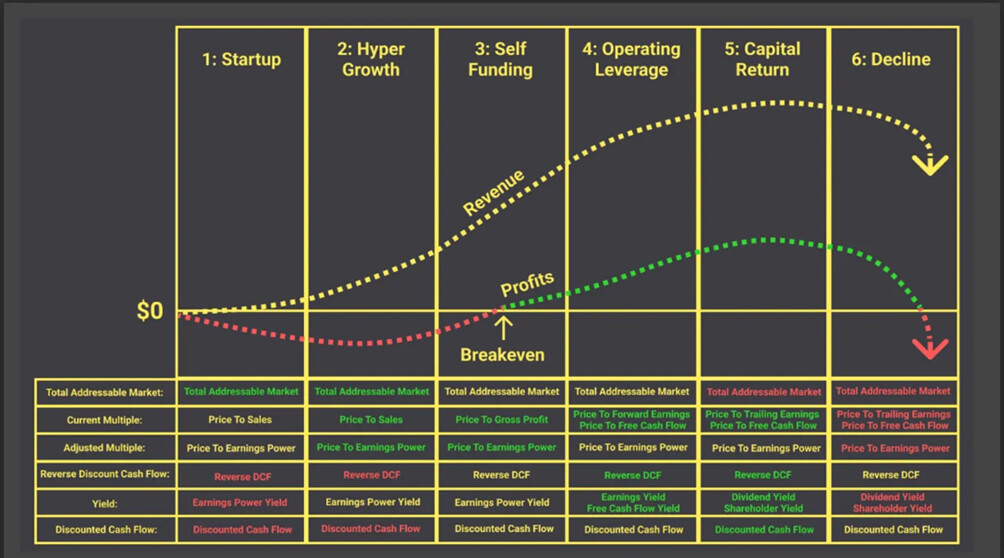

Yhtiö on alempana näkyvässä kuvaajassa tällä hetkellä tukevasti kakkosvaiheessa. Olen tunnuslukujen kautta arvioinut sitä ainoastaan EV/sales -multippelin kautta, joka on viime aikoina pyörinyt edelleen noin 3,5 – 5,0 kertoimilla, vaikka osakkeen hinta onkin maltillistunut reilusti alkuinnostuksen jälkeen. Nähdäkseni hinnan voidaan edelleen olettaa pitävän sisällään odotusta tulevasta kasvusta. Toisaalta on kasvua myös tullut, koska yhtiö on onnistunut tuplaamaan liikevaihtonsa kahtena edellisenä vuotena, ja jos edes osa nykyisistä kilpailutuksista päätyy ACC:lle, en pidä liikevaihdon tuplaamista tänäkään vuonna mahdottomana tehtävänä. Tällöin EV/sales olisi nykykurssilla noin 2. Viime vuoden Q4:ään verrattuna myös order backlog on vuoden aikana tuplaantunut.

Yhtiön merkittävämmät rahavirrat syntyvät tällä hetkellä vielä aika pienestä määrästä projekteja, joten odotan voitollisuuteen pääsyn tapahtuvan hieman pomppien, tosin en vielä ainakaan tämän vuoden aikana. Yhtiön pääsyä voitolliseksi tulee luonnollisesti seurata, mutta uskon sen olevan lähinnä seuraus voitettujen projektien runsaslukuistumisesta, minkä vuoksi oma mielenkiintoni kohdistuu tällä hetkellä uusiin voitettuihin projekteihin.

Yhteenveto

Nähdäkseni sen verran moni asia tuntuu olevan yhtiön kannalta kohdallaan, tai ainakin menossa oikeaan suuntaan, että löydän yhtiölle selvästi enemmän positiivisia kuin negatiivisia ajureita. Johtuen projektien pitkistä toimitusajoista, jätän kuitenkin rakettiemojit myöhemmälle. Uskon enemmän hitaampaan ja hieman epätasaiseen kasvuun. Jos tämä kuitenkin menee odotukseni mukaan, saa yhtiö jo tänä vuonna mukavan potin uusia projekteja, minkä pitäisi katkaista kurssin pitkä pulkkamäki. Aion alkuvaiheessa seurata yksittäisten tarjouskilpailujen voittajia nähdäkseni onko ACC:lla riittävät mahdollisuudet bisneksen rakentamiseen. Osakkeen pidempiaikainen suunta on kieltämättä hieman mietityttänyt, koska on yleensä melko epätodennäköistä, että näkisin tilanteen markkinaa selvemmin. Tämän vuoksi toivoisin myös toisenlaisia näkemyksiä, mutta toisaalta tiedostan yhtiötä seuraavien silmäparien pienilukuisuuden.

Aika on ikävä kyllä ruuhkavuosina rajallista, joten tekstistä jäi puuttumaan vielä monta aihetta, joita olisin mieluusti sivunnut. Pidätänkin oikeuden päivittää tekstiä ainakin kilpailijoiden, karhuilun sekä plussat-miinukset -listan osalta, jos joskus saan uusia kappaleita aikaiseksi.