Adobe is an American software company known especially for its applications related to creative content production and publishing. Its most well-known products include the Photoshop image editing program, the Illustrator vector graphics tool, and Acrobat Reader and the PDF format. Adobe also offers the Creative Cloud subscription service, which covers a wide range of tools for photography, video editing, etc.

The company was founded in 1982, and its PostScript technology played a key role in the desktop publishing revolution. Adobe has expanded into animation, multimedia software, and digital marketing. Despite criticism related to Creative Cloud pricing, Adobe has remained a leading player in creative industries.

The company has over 26,000 employees globally, including development centers in the United States and India.

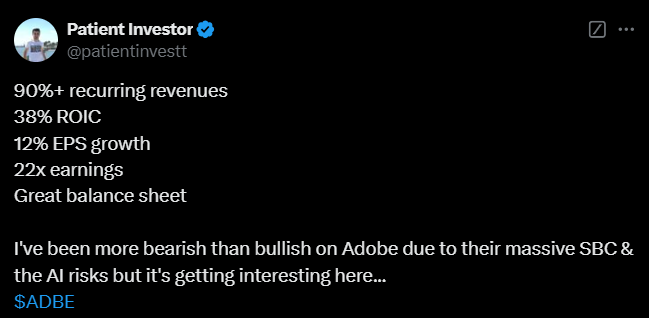

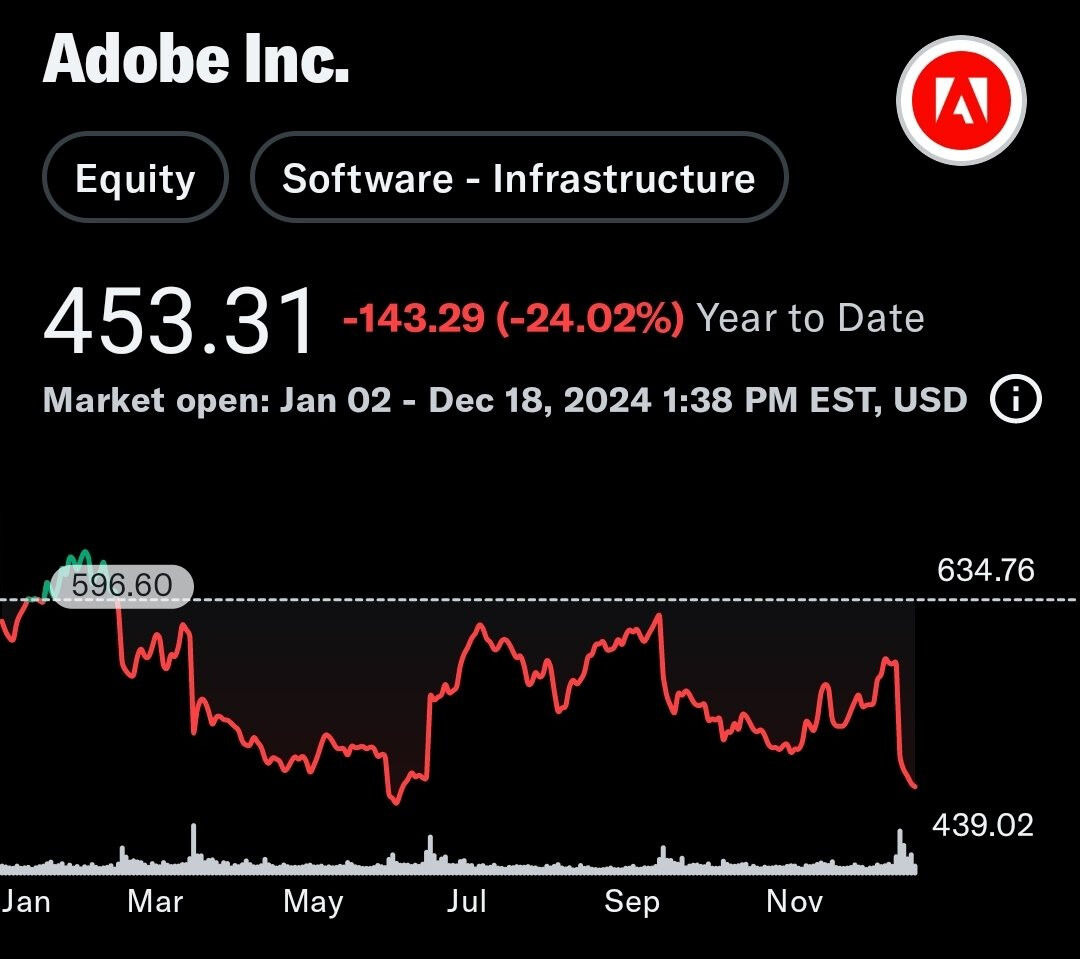

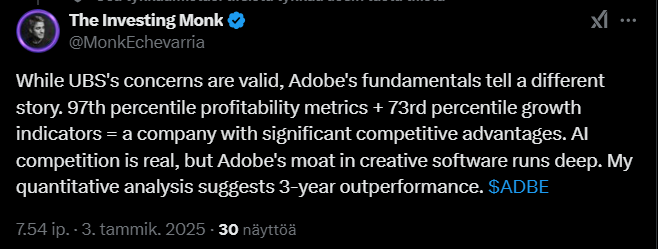

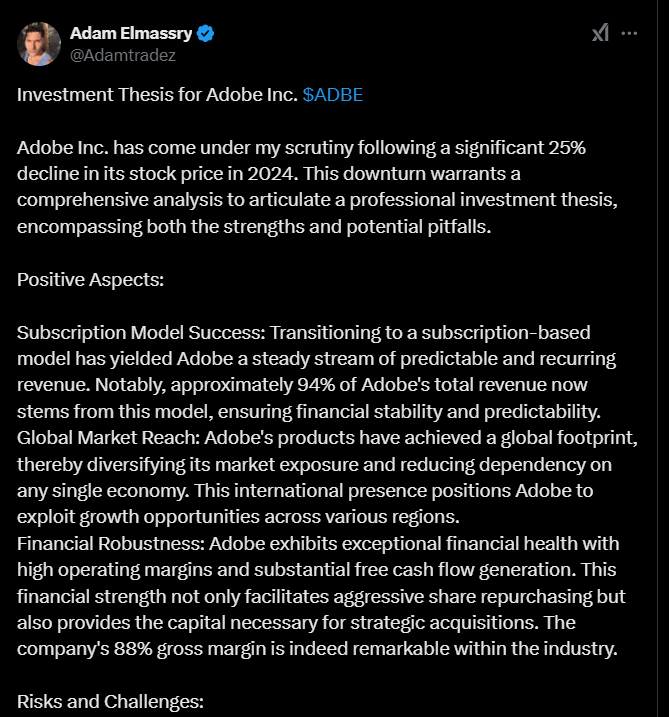

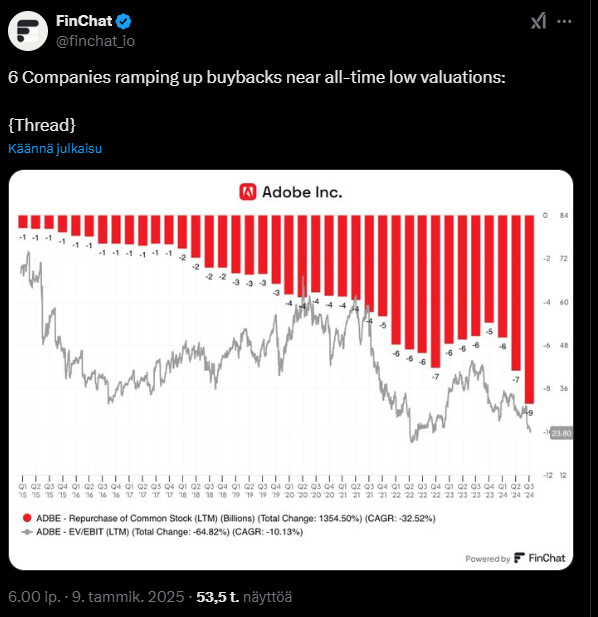

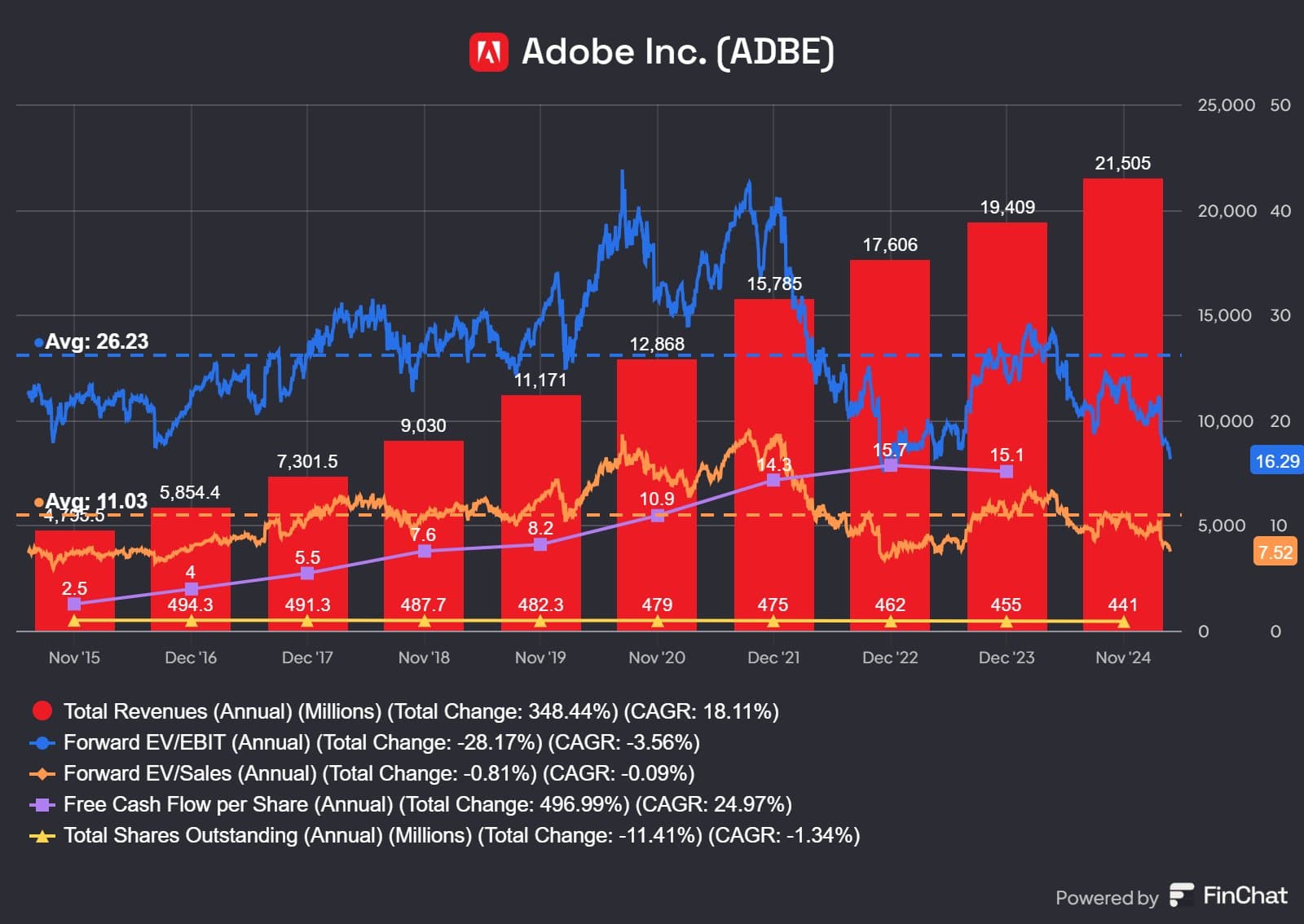

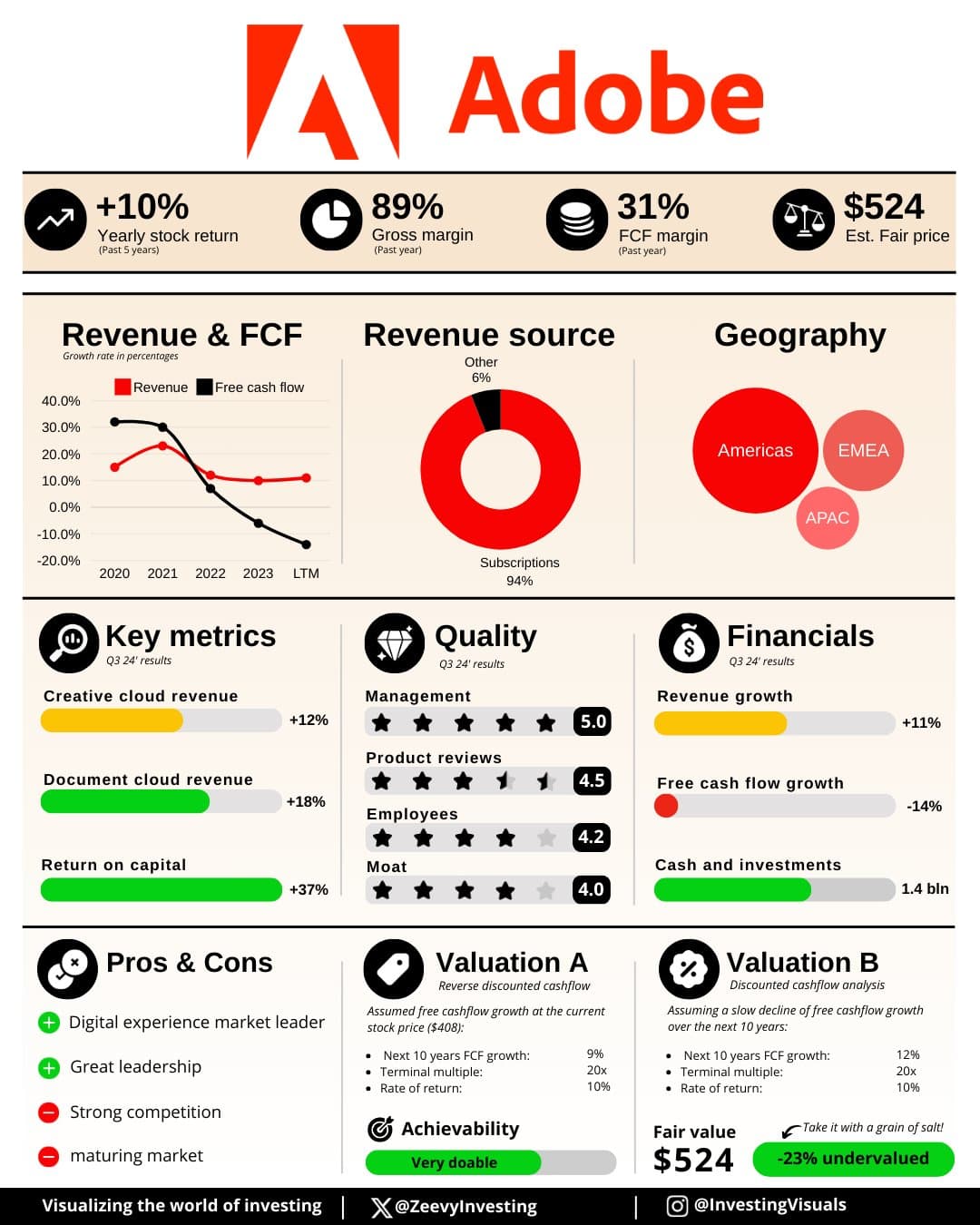

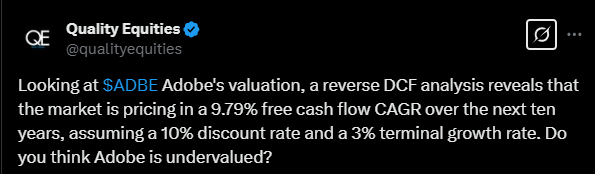

As an investment, Adobe benefits from stable cash flows and competitive margins, although revenue growth has slowed in recent years. The integration of generative artificial intelligence (GenAI) into Adobe’s products has increased demand, but industry competition may limit long-term growth opportunities.

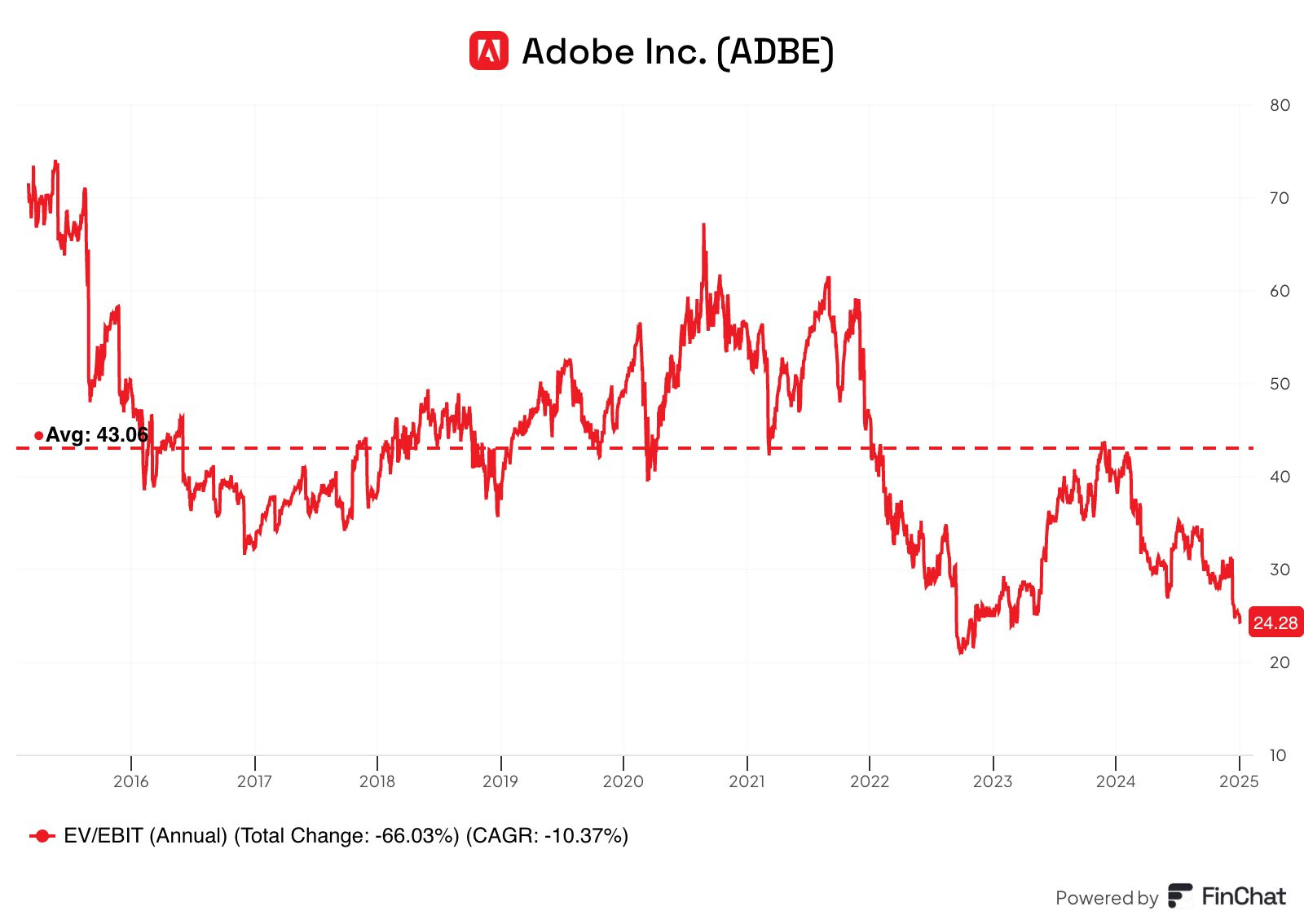

Adobe’s P/E ratio is currently below its five-year average, which for some offers an attractive buying opportunity, even though the company faces challenges such as exchange rates and market saturation. Overall, Adobe offers stable but moderate growth in high-margin software markets.

However, it should not be forgotten that revenue growth has slowed and that competitors also offer AI solutions, and I have no information, at least, that Adobe would be superior in this regard. No clear “resurrection” of margins is visible in the future either.

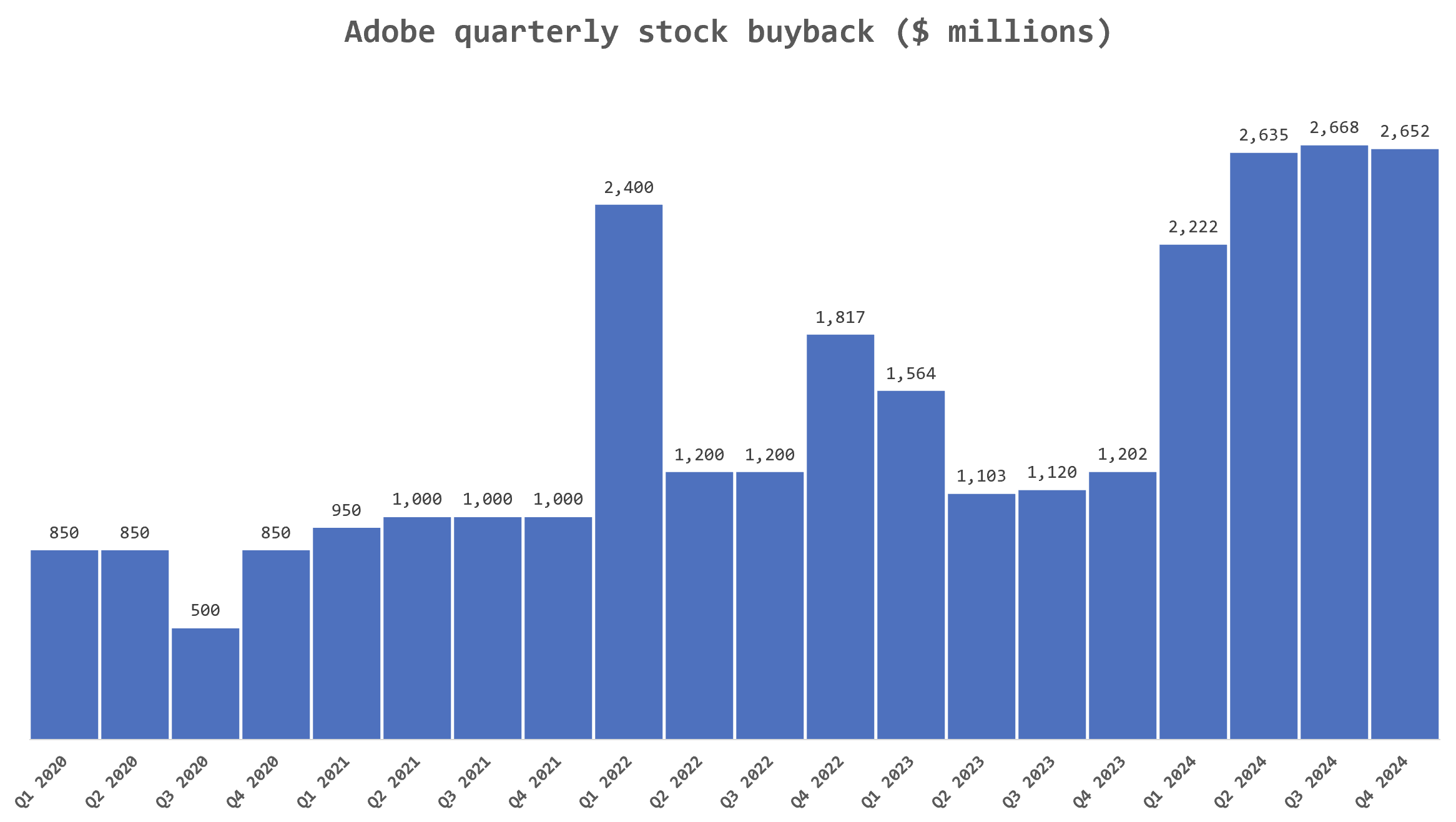

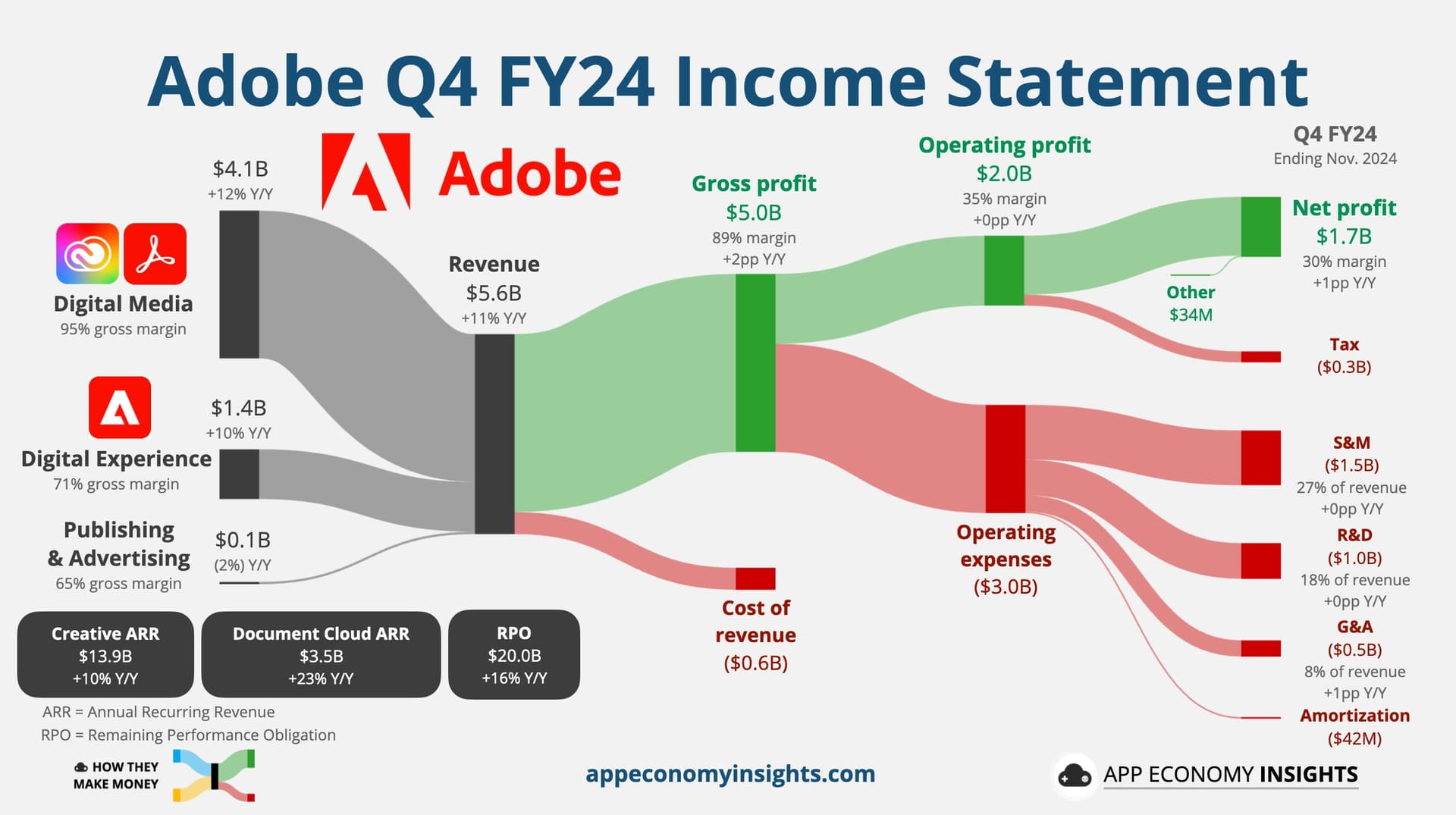

Adobe’s Last Quarter (published 11.12.)

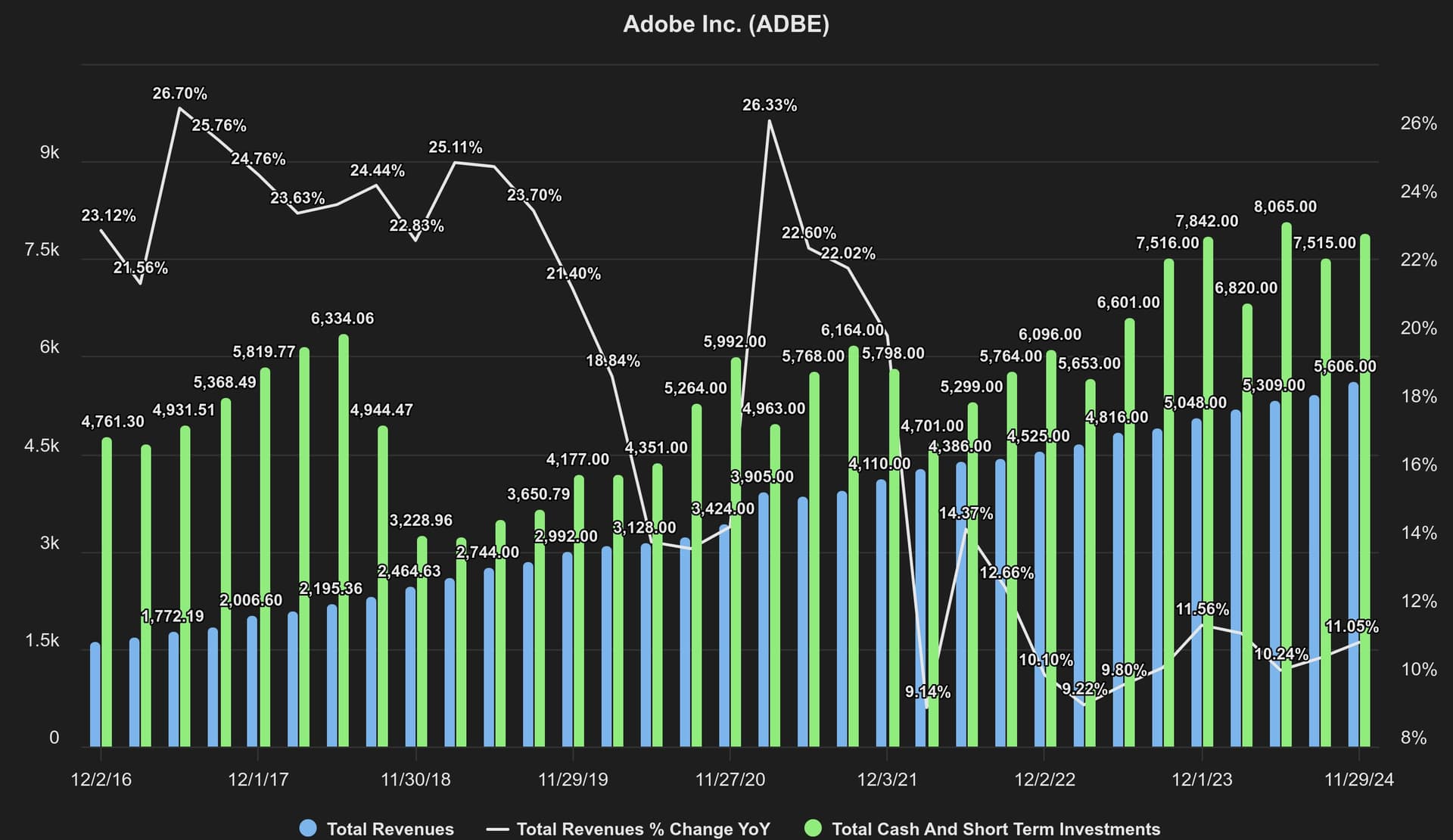

Adobe achieved record revenue in fiscal year 2024, highlighting strong demand and the importance of Creative Cloud, Document Cloud, and Experience Cloud solutions in the AI ecosystem. According to CEO Shantanu Narayen, the company’s “technology foundation,” rapid innovation, and cloud service integration create a strong basis for the coming year. CFO Dan Durn emphasized that strategy, AI innovation, and cloud service opportunities will support long-term growth. The drivers for these aforementioned aspects would include, among others, a diverse marketing strategy and technological distinctiveness.

Then some other things:

https://x.com/ConsensusGurus/status/1867213226230051295

https://x.com/MarceloPLima/status/1867259769540817130