In my opinion, this summarizes well why the company’s stock price has plummeted. EBITA%, ROCE% and cash conversion have decreased quarter after quarter, and revenue growth has been solely inorganic. Additionally, reflecting on this, the company was run with an excessively high debt level, which led to a share issue made at a dismal valuation.

The share issue raised 457 MSEK (with warrants potentially raising an additional 172 MSEK in a year), in which insiders also participated, and in recent months they have also bought shares from the stock exchange. Net debt at year-end was approximately 1,435 MSEK, so the issue itself improves the net debt to 12M EBITDA ratio (3.8X at year-end).

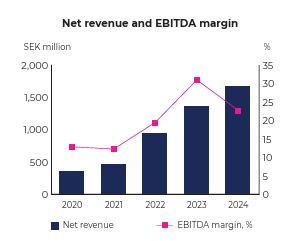

Management itself has explained the weak FY24, mainly by an excessively good FY23.

Without taking a stand on how various tariffs might affect Addvise Group, I believe the current valuation includes a fair margin of safety.

- Based on Quart’s data, Market cap is 233 MSEK and EV 1.7 BSEK; if the consensus estimate of two analysts materializes, EV/EBITDA is 3.9X based on FY25 figures (13.3% EBITDA growth). If EBITDA remains the same as FY24, the multiple would be ~4.5X.

Have others been following the company’s activities recently or bought shares?