I was just about to write about that. There’s a webcast coming later today, which will probably have more on this. I didn’t quite understand what’s behind all this. Does Bausch + Lomb want a better deal for themselves, or do they not want Xbrane on the market at all, or what? Or has something unexpected come up with the FDA, causing them to withdraw from the agreement?

1 Like

This timing is indeed strange, now that the FDA application has finally been successfully submitted. However, I don’t believe there could be any new FDA surprises at this stage. Xbrane would have had to disclose any significant ones.

Could it be that since the start of US sales has been delayed, Bausch+Lomb sees the market potential as smaller than before and no longer wants to commit to the milestone payments, etc., agreed upon in 2020? In other words, they might have wanted a more favorable deal. With biosimilars, it is essential to be the first or among the first to market. The only competitive advantages are time-to-market and price. Xbrane may have a slight price/cost advantage, but margins will suffer if they try to gain market share through pricing while lagging behind.

1 Like

Surprising and unfortunate news. A distribution agreement for North America was signed with Bausch + Lomb in 2020, which has now been terminated for one reason or another. The reason wasn’t really explained in the release, but there is a webcast this morning where more information will be provided. I don’t think it’s about the FDA approval; matters related to the permit should be announced immediately. It’s likely that the agreement was no longer profitable for one of the parties and they couldn’t reach a mutual understanding. It’s a frustrating situation in that there is currently no commercial partner/distributor in North America.

4 Likes

Surprising and unfortunate news, of course; Bausch + Lomb seemed like a really good partner for the US, at least on paper, but they don’t have a single biosimilar on the market. I bought the dip with both hands, and Åmark was convincing in his presentation and also managed to calm some of the market uncertainty. Apparently, there are 10–15 potential partners for the US, and there’s still plenty of time before the marketing authorization arrives, so I’m quite confident that Xbrane will have a new partner before getting the marketing authorization—and in the best case, with a better deal than the previous one. The CEO also speculated this, as the drug and the marketing authorization case are much further along than in 2020 when the B+L deal was negotiated. According to Åmark, this will not delay the US schedule.

The reason for canceling the partnership turned out to be Bausch + Lomb’s new CEO and a new strategy to not focus on biosimilars in the future.

10 Likes

The biosimilar field is only just developing, and this is reflected in the fumbling behavior of marketing companies. For some time now, so-called Big Pharma has been divesting biosimilar businesses, and B&L is no exception to the big picture, even though it isn’t a very large company—roughly the size of Stada, for whom a drug like Ximluci would be relatively significant.

Pure-play biosimilar companies are still missing from the field; there are only a handful of them. Biosimilars tend to have turnover that is too small for originator companies, yet they are usually drugs for relatively serious diseases, such as Ximluci, which require a sales team capable of handling them. Consequently, they do not necessarily fit into the portfolios of companies selling traditional generic chemical drugs, let alone OTC pharma firms. Stada seems to be a good exception, playing the long game with biosimilars.

The entire US saga, with its FDA delays and B&L messes, underscores how challenging the US market is from the perspective of a European innovative development company. The most important thing would be to find a long-term and stable partner with a clear strategy for selling the product cost-effectively. In the US, Biogen currently appears strongest with Ranibizumab, as Coherus has severely destroyed its company value over the past couple of years while management has been wandering with its strategy.

In Europe, however, Biogen appears to have sold practically nothing. This is a good sign for Stada, as Stada and Biogen won the UK tender, Teva was left out, and in France, Ranibizumab is available from Teva and Stada, while Biogen is not currently on the lists. These are truly exciting times with more twists to come; hopefully, the new US partner will be cooperative, and the Opdivo biosimilar can also be licensed with a good deal to a long-term partner.

9 Likes

The market eventually practically closed the gap caused by this news, from which we can conclude at least that some investors believe a new distributor for ranibizumab can be found easily. Of course, Xbrane ended up with Bausch and Stada for a reason, so in theory, there should be previously unsuccessful alternatives still available. After reflecting on this for a few days, I believe that a year from now, once we are wiser about the whole US situation, last year’s FDA news will prove to have been more serious than this week’s turn of events, which was surely largely due to that delay. At this stage, the deal was still easy for both parties to terminate.

Notable this week was the all-time high volume, and it will be interesting to see if there are new names among the top 10 owners when the July shareholder lists are updated. Of course, there have been just as many sellers, so that is also of interest.

Despite practically three setbacks over the last two years (Primm, FDA, Bausch), very interesting times lie ahead and some preliminary positive signals have also been received. It must be remembered that the upside in Brane’s case comes from the company’s relatively small size. We are in a transformational year, as cash flow is presumably negative for the last time before turning positive next year. If preliminary indications that Xbrane has the most competitive supply for ranibizumab hold true, this should be reflected in strong share price performance. Interest in the company is building; well over a dozen questions were asked in Tuesday’s Q&A session.

8 Likes

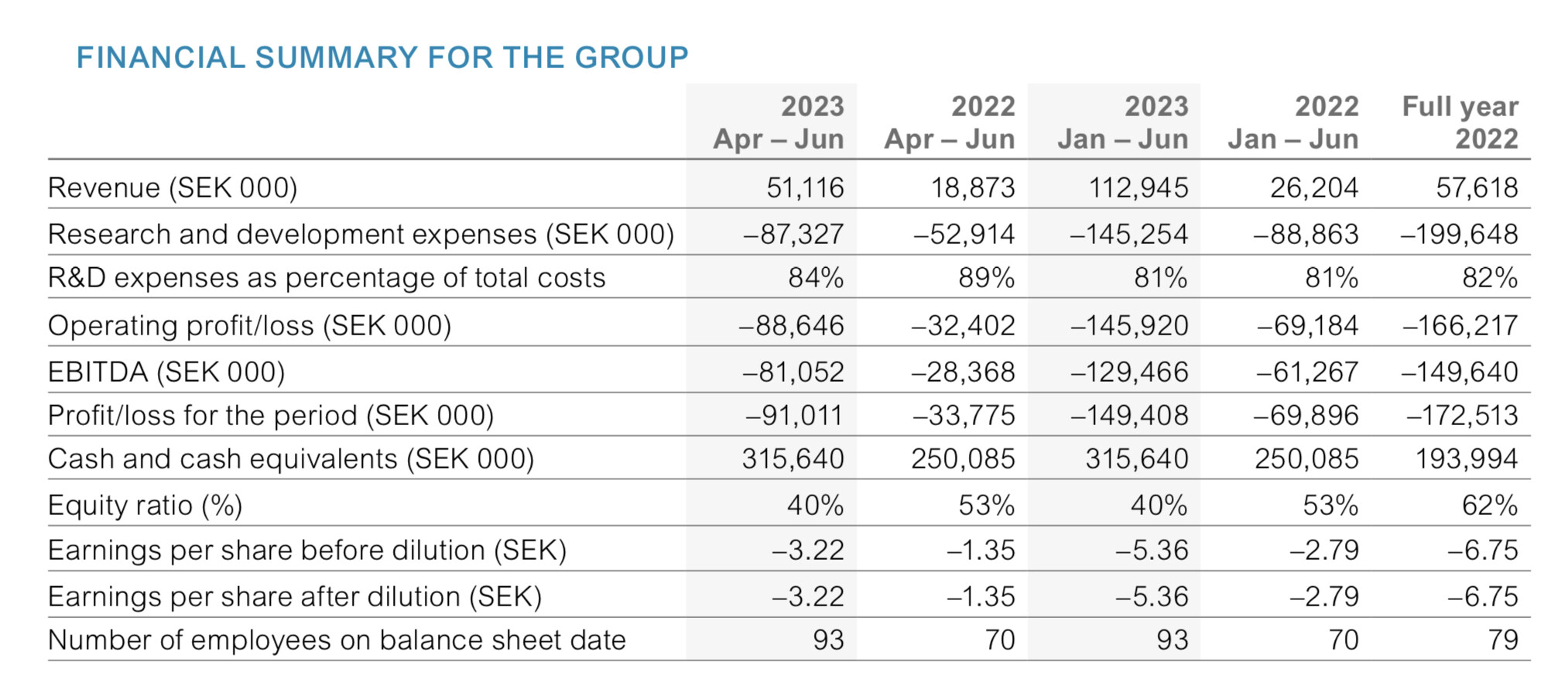

Xbrane’s Q2 2023. Quite weak sales, the target for cash flow positivity is pushed back to Q1 2025. Ximluci sales were only SEK 37m. In Q1, they were SEK 48m.

Edit: Share price reaction accordingly, -37% to start with.

6 Likes

I will highlight a few more unstructured observations here. It’s a pretty catastrophic quarter regardless, and management’s credibility is now being tested. This was supposed to be quite de-risked in many ways, at least for a pharmaceutical company. In the short term, this has become one of the worst investments of my investing career. In the longer term, the situation could of course still change.

Highlights:

- Ximluci launch in March '23; Q1 sales SEK 48m

- Total Q2 Ximluci sales SEK 37m

- In the Q1 conference call, it was implied that production capacity would be the limiting factor for sales in 2023

- Bausch + Lomb’s withdrawal was explained by everything other than lower-than-expected sales in Europe. The market was rather reassured; everything is fine.

- Q2 presentation:

→Uptake of all ranibizumab biosimilars slower than anticipated due to requirements for education of stakeholders

- Products delivered & invoiced every 2-3 months

One more highlight from Redeye’s Q1 (not Q2!) update. Boldings are mine.

We highlight the company’s comparably low risk owing to the higher probability of success in the clinical development for biosimilars – and the potentially high profitability –

…

We’ll see what they think of Q2.

This doesn’t necessarily change the big picture yet, but after Q1, the trend is definitely completely wrong, and forecasts for sales growth and market share based on earlier biosimilars can be scrapped, at least for the time being.

Edit: After the conference call, a clarification on that Ximluci sales trend. (Tired-sounding) CEO Åmark stated in the Q&A that the income statement doesn’t give a completely accurate picture of sales development due to the distribution agreement, etc. Although sales are low, more is sold every month than the previous one. So, in that sense, the trend is at least in the right direction.

8 Likes

Insider trades after the Q2 release and the stock price crash. According to Insiderscreener, purchases totaled 447,357 SEK, sales 1,738,708 SEK. Net -1,291,351 SEK.

Insider trades in an illustrative format here: https://www.insiderscreener.com/en/company/xbrane-biopharma-ab and in a less illustrative but more official format here.

According to Xbrane, the sales were made for tax purposes.

2 Likes

Tender from Denmark for the year 2024.

As a Google translation:

II.2.4)

Description of the procurement:

The tender number includes the following medicines:

Tender no: 1,

ATC code: S01LA04,

Generic name: Ranibizumab,

Dosage form: Solution for injection,

Packaging: Vial/pre-filled syringe,

II.2.5)

Award criteria

Criteria below

Price

II.2.6)

Estimated value

Value excluding VAT: 288,000,000.00 DKK

II.2.7)

Duration of the contract, framework agreement or dynamic purchasing system

Start: 1.1.2024

End: 31.12.2024

This contract can be renewed: yes

Description of renewals:

Amgros I/S may extend the framework agreement a maximum of 2 times for each lot under unchanged conditions for a maximum of 6 months, if Amgros notifies the supplier of this by 30.9.2024, 30.3.2025 at the latest.

What I think is good there is that the only criterion is price. The problem from Xbrane’s perspective is that they only have the vial, and the pre-filled syringe won’t arrive until 2025. In the conference call, Åmark didn’t properly answer the question of how it’s possible that it will take until '25 before this desired packaging is brought to market. The value of the tender is approx. SEK 447M. Ximluci sales in Q2 were SEK 37M.

6 Likes

There are a few interesting potential takeover plays on the market, Xbrane Biopharma being one that would fit perfectly in a competition portfolio, but I suspect they won’t materialize during low valuations; instead, owners are waiting for the pace to pick up.

Can someone explain in simple terms how today’s news regarding the share issue and options works?

I understood it roughly like this: if you do nothing → 98% dilution. If you sell the subscription rights → you realize the current losses/situation and after that, your ownership is non-existent. If you subscribe to everything possible → you maintain the same potential (as you had yesterday) for the future. And for the last one, of course, you’d need your cash pile to be in order for it to work. So, it seems to be a load of crap all in all.

1 Like

I haven’t really followed this, but big gainers and losers are always interesting.

So, a 343Mkr rights issue is being proposed for a company whose market cap fell 75% today (at the time of writing) to a market cap of 57Mkr.

The rights issue will only take place after the Extraordinary General Meeting (EGM) in late February, meaning the subscription rights will be detached only after that. Presumably, bad news regarding the sales outlook was also shared today, and while additional financing was expected to be needed, it was even more than the market anticipated—quite a slaughter.

1 Like

The share price has started to wake up in recent days. Apparently in anticipation of FDA approval in April.

1 Like

Quite a struggle. A trainwreck, as they would say across the pond. Once again, additional information must be provided to the FDA, and the BLA has been withdrawn. An additional delay of approximately 6–12 months is expected AND even more capital may potentially be needed.

For fun, I compiled a small timeline of the press releases (the dates are links to the respective press releases, summaries below). During this time, investors who joined before the latest share issue have practically lost everything. Xbrane serves in many ways as a case study for the risks associated with biotech investing.

Xbrane announces ambition to generate positive operating cash flow monthly by late 2023/early 2024

At the beginning of 2022, the XIMLUCI (LUCENTIS) BLA was submitted to the FDA. This was not published as a separate press release.

Xbrane Biopharma AB has withdrawn the BLA (Biologics License Application) for its investigational biosimilar candidate to LUCENTIS® after receiving feedback from the FDA

Based on the time required to complete the BLA as per FDAs comments and recommendations, Xbrane plans to resubmit the BLA during 2022.

The delivery of a critical report required for the re-submission has been delayed and therefore the re-submission of the BLA has been postponed to first quarter of 2023.

Xbrane has submitted the BLA for its investigational biosimilar candidate to LUCENTIS® (ranibizumab) to the FDA. Within 60 days, FDA is expected to validate and decide to initiate the review of the BLA. Thereafter, Xbrane expects a 10 month review process and hence an approval could take place during the first half of 2024.

XBRANE UPDATES AMBITION TO GENERATE POSITIVE OPERATING CASH FLOW ON AN MONTHLY BASIS BEFORE END OF FIRST QUARTER 2025

Xbrane provides regulatory update on FDA review of its ranibizumab biosimilar candidate. Xbrane will work closely with the agency to submit as quickly as possible responses to the issues raised, which relate primarily to the reference standard and pre-approval inspections of manufacturing partners’ sites. Xbrane will request a meeting with FDA, expected to be held within 30 days from request, to clarify further requirements related to above issues and will after that announce a planned date for resubmission of the BLA.

A reasonable base case estimate would be that the new BsUFA could span anywhere from 6-12 months from today, which to us implies a potential H1 2025 launch in the US.

Regarding financing, numerous factors contribute to a range of potential outcomes where Xbrane could require more capital or not.

7 Likes

XBRANE AND STADA PARTNER WITH VALORUM BIOLOGICS TO COMMERCIALIZE RANIBIZUMAB BIOSIMILAR CANDIDATE IN THE US

Based on this, could one think that obtaining FDA approval looks quite promising?

4 Likes

It’s hard to see any profitable future for this Ximluci. From what I’ve researched, off-label Bevacizumab is still cheaper, and on the other hand, aflibercept and faricimab are better and longer-acting. There simply isn’t a market niche.

1 Like

How have you handled your holdings in this stock, @Zolt? I only just came across this company and the slide has been quite significant, especially since August 2023. Heavy dilution and high cash burn, but could 2025 finally be their year? Market cap is now approx. €30m.

Xbrane warns that it will be insolvent in a couple of months if the desired financing solutions are not reached and the company does not manage to out-license the Xdivane™ and/or XB003 candidates by the end of October.

As communicated on 1 August 2024 and given the previously communicated delay in FDA

approval of Ximluci® and the unforeseen termination of the license agreement with Biogen,

Xbrane Biopharma AB (publ) (“Xbrane” or the "Company”) has initiated a process to out-license

both Xdivane™ and XB003 for purposes of ensuring financing until envisioned positive

operational cash-flow in Q2 2025. It has now become obvious that the company needs to

finalize one of the above-mentioned license deals at satisfactory terms prior to the end of

October 2024 to fulfill the Company’s working capital requirements from beginning of

November 2024 and onwards.

3 Likes