Tomorrow, Xbrane will host a Capital Markets Day:

"Stockholm, Sweden – Xbrane (Nasdaq: XBRANE), a late-stage clinical biopharma company is inviting analysts, investors and media to the company’s Virtual Capital Markets Day on May 17th, 2021 at 14.00-15.30 CET.

The event will feature presentations from Xbrane’s Board and Management team outlining the company strategy and the next steps in the company’s ambition to become a leading global biosimilar developer. The program will also include a virtual show of the recently established new development lab."

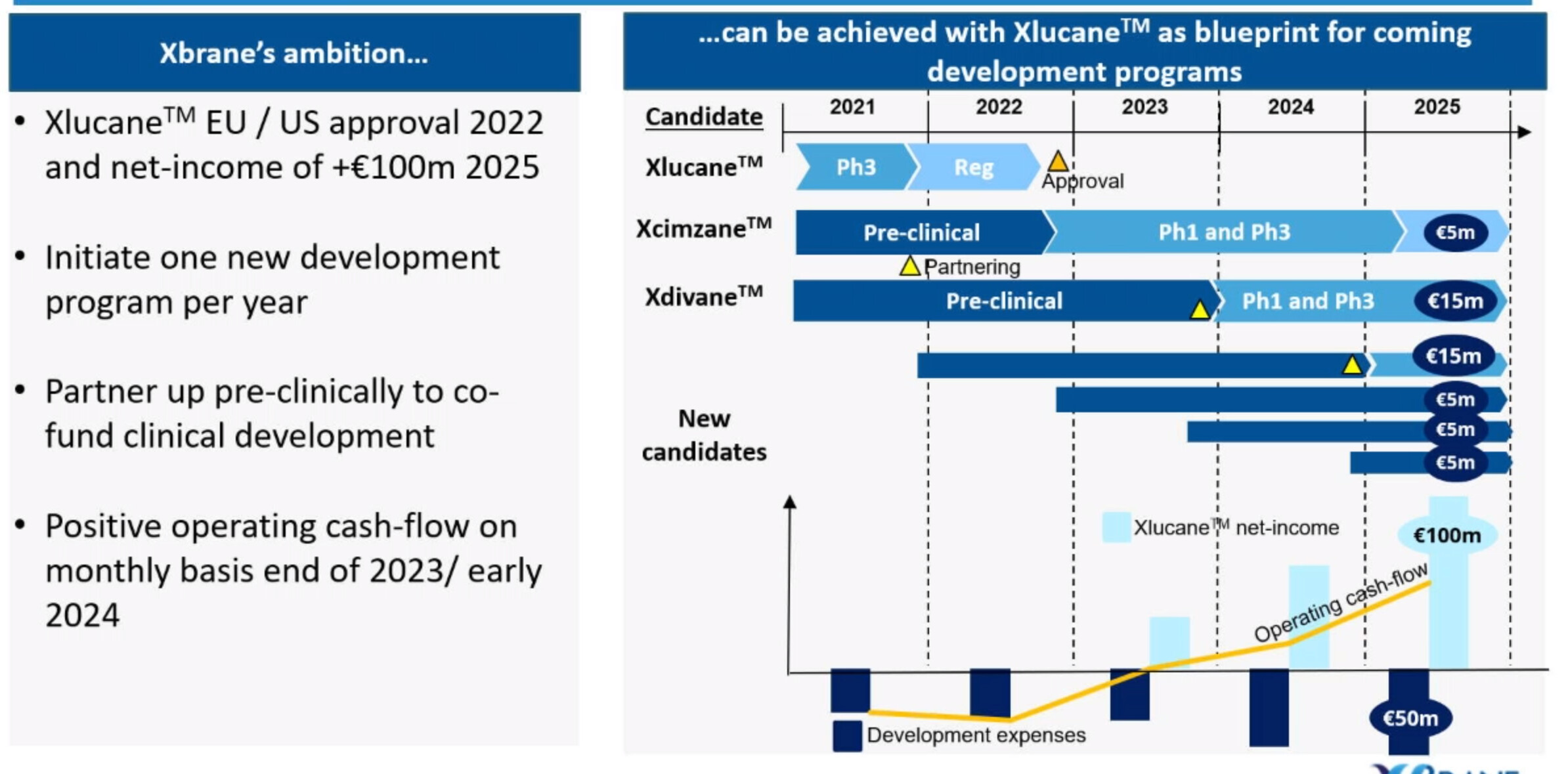

The current share price is just under 130 SEK, which I believe quite accurately reflects the current valuation, if Xbrane’s only valuable asset is considered to be Xlucane. As can be read above, the company’s main goal in the long run is to become a world-leading biosimilar developer, and tomorrow we will surely gain further insight into how Xbrane intends to implement this strategy. The company has preliminarily communicated that its current facilities enable the launch of one new biosimilar project annually.

Now, a stream of consciousness before tomorrow’s CMD, not an investment recommendation:

Currently, Xbrane’s market capitalization is 280 million euros, which can be seen as almost entirely derived from the Xlucane project, whose base case is an annual revenue level of 100 million euros by 2025. I do not believe the market is significantly discounting the Xdivane project, which is only expected to enter the market in 2026-2028. The Xcimzane project, whose patent expires in 2024, may currently be valued at 30-40 million euros, as Xbrane is currently the only competitor looking to gain market share in the 1.8 billion euro market.

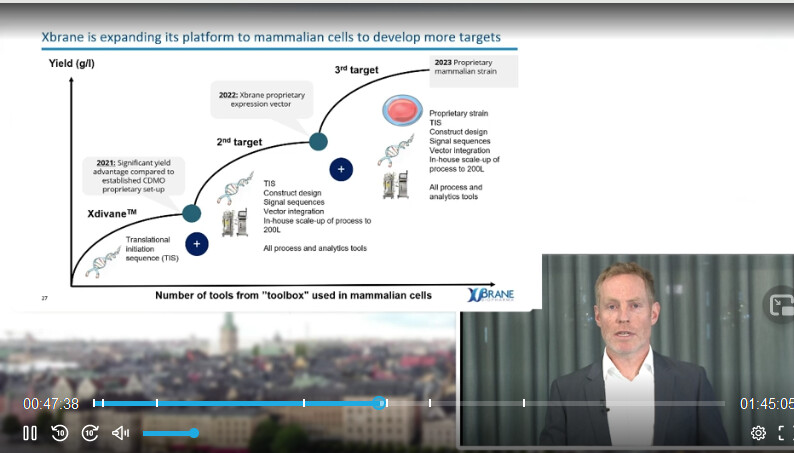

I would argue that each new project, once the Xlucane project succeeds, could be roughly priced at 40-100 million euros, depending on many factors, of course: the target molecule, interest rates, partners, drug reimbursement policies in different countries, etc. I trust Xbrane’s strategic ability to select hard-to-manufacture but sufficiently large market (at least 1 billion euro market and 1-3 expected biosimilar competitors) target molecules for its development pipeline, where the developed manufacturing platforms can yield the greatest benefit. It will be interesting to see if Xbrane will also elaborate on the competitiveness of its mammalian cell platform tomorrow.

Despite strong share price performance, I still believe there is an exceptionally attractive risk-reward ratio here, when future potential projects are added to the valuation; four years from now, the company’s revenue could be 100 million euros, in addition to having four new projects valued at 40-100 million euros in the R&D pipeline, as well as the already approved Xcimzane. In the Xcimzane project, Xbrane’s negotiating position might be exceptionally strong with partners due to the lack of competition. With 50% market penetration, a 50% partnership agreement, and a 50% price reduction, Xcimzane could generate approximately 200 million euros in revenue a few years after market entry (1.8 billion * 0.5 * 0.5 * 0.5). In the scenario mentioned, Xbrane’s R&D costs before 2024 would likely be around 75 million euros (average biosimilar project approx. 150 million euros / 2).

Although the case has been practically the same since 2018 when the partnership with Stada was initiated, the value has only been reflected in the share price during the last year. Of course, along the way, uncertainties in financing have been tackled and non-core assets have been pruned, but in a technological sense, the company’s case has remained very stable and intact ever since the 30 SEK bottom prices of the 2019 rights issue. This may still be a difficult investment for the market to grasp, due to the following reasons:

- Market Cap excludes the biggest players

- The Swedish market is partly out of reach for, e.g., US analysts

- A loss-making company with zero revenue based solely on financial figures does not look attractive

- Investor caution towards drug development companies/misunderstood risk-reward ratio

- Illiquidity for institutions and pension funds awaiting subsequent financing rounds

- The company has not actively communicated the launch of future projects before tomorrow’s CMD

Finally, let me state that Xlucane’s Phase 3 results are due in about 60 days, which is the most important single catalyst event in the short term. After that, the investment case will increasingly focus on the prospects of future projects, and perhaps even more risk-averse investors will dare to invest in the company thereafter.

I will write more tomorrow based on the points raised from the presentation.

E: Corrected Xoncane —> Xdivane