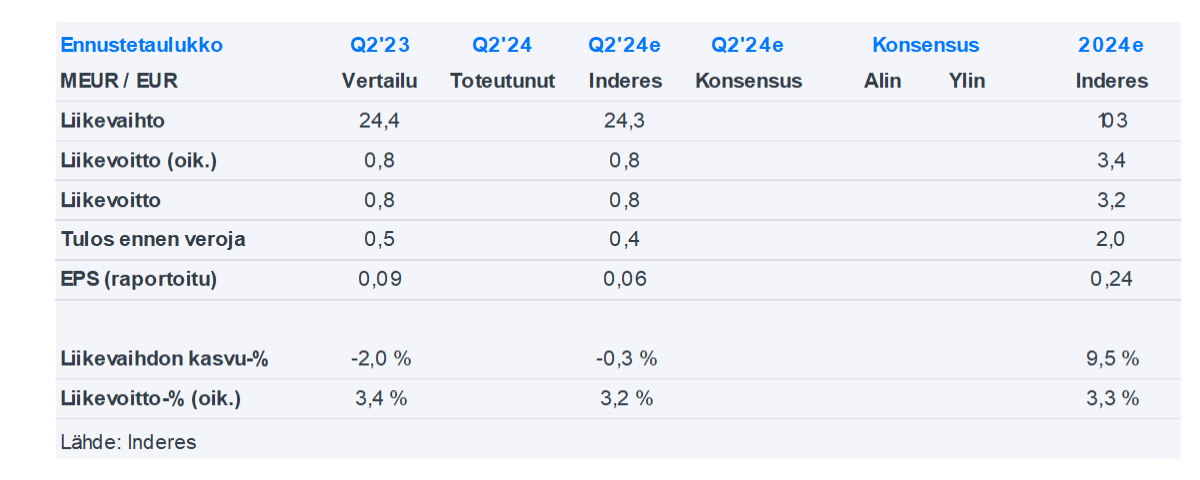

Revenue was EUR 25.5 million (24.4), revenue grew by 4.6%

EBITDA was EUR 1.7 million (1.3) and comparable EBITDA was EUR 1.7 million (1.3)

Operating profit (EBIT) was EUR 1.2 million (0.8) and comparable operating profit (EBIT) was EUR 1.2 million (0.8)

Earnings per share (EPS) was EUR 0.15 (0.09) and comparable earnings per share (EPS) was EUR 0.15 (0.09)

Equity ratio was 39.4% (42.1)

We are raising Wulff’s target price to EUR 3.00 (previously EUR 2.70) and our recommendation to accumulate (previously reduce) following a good Q2 report. Second-quarter revenue and earnings exceeded our forecasts and indicate that Wulff is performing well in the challenging workplace products market. In the service business, Wulff Works has progressed well and turned profitable by the end of the quarter, which, together with other services, creates good opportunities for growth this year. There are still uncertainties regarding market development and the progress of Wulff Works, but the moderate valuation and improved earnings outlook make the stock attractive to accumulate.

Quoted from the report:

Acceptable valuation

In our valuation, we mainly utilize the absolute valuation level we have defined for the company. We primarily price Wulff’s stock through earnings-based valuation multiples. In the valuation, we especially favor EV/EBIT and P/E multiples. For Wulff, we use an acceptable valuation range of 10-12x P/E and approximately 8-10x EV/EBIT. We are currently leaning toward the lower end of the multiples.

Kopsa is previewing; here are the comments for Wulff’s Q3 results to be published next Monday.

We expect revenue to show clear growth in Q3 and the result to increase accordingly. A weaker workplace product market dampens growth opportunities, but the school supply trade, which partly falls into Q3, as well as the growth of Wulff Works and the service business, raise both revenue and result in our forecasts. In the report, we will follow the progress of Wulff Works and the development of the company’s financial position, in addition to the result and outlook.

And here are Olli’s quick comments on the Q3 results.

Wulff-Yhtiöt published its Q3 report on Thursday, which was slightly better than our expectations. Revenue grew strongly from the comparison period and was slightly stronger than our forecasts. Earnings also increased from the comparison period in line with our expectations. Guidance remained unchanged and the outlook for workplace products remains challenging, but accounting services and Wulff Works are now supporting Wulff’s growth and earnings very well.

And here is some analysis, i.e., more comprehensive thoughts from Olli after Q3.

Wulff’s revenue growth was strong in Q3 and profitability rose from the comparison period thanks to service operations. Following a good Q3 result, we believe Wulff has good opportunities for earnings growth this year despite the challenging workplace product market. In the coming years, earnings growth will be supported by a recovering market, efficiency measures, and the increasing share of profitable services, but considering the risks, we believe the valuation has reached a neutral level.

Quoted from the report:

No significant changes in the outlook

Wulff made no changes to its guidance and expects 2024 revenue to grow (2023: EUR 93.8 million) and comparable operating profit to be at a good level (2023: EUR 3.5 million). Growth is expected from service operations this year, but the outlook for product operations remains challenging due to the general weakness of the economic situation. However, the improving performance of Wulff Works, the realization of synergies from acquisitions, and savings from change negotiations should, in our assessment, support the result.

Wulff advances its growth strategy: WULFF ACCOUNTING SERVICES SERVICE NETWORK GROWS

Wulff-Group Plc continues to implement its growth strategy with a business acquisition that strengthens Wulff Accounting Services’ operations. Toda Consulting Oy is an accounting firm serving its clients personally in Hyvinkää. In connection with the acquisition, its personnel will become part of Tilitoimisto Lundström Oy, which operates in Uusimaa and was acquired as part of Wulff Accounting Services’ business in February 2024. The business acquisition brings Wulff Accounting Services more than 250 new financial management customers, three top professionals, and approximately EUR 250,000 in annual net sales.

Wulff Accounting Services strengthens its position in the industry by acquiring the business operations of Ab Bokföringsbyrå Esse Tilitoimisto Oy. Esse, based in Porvoo, is especially known for its personal service to its Swedish-speaking customers and high customer satisfaction. With the acquisition, Tilitoimisto Esse’s personnel will become part of Wulff Accounting Services’ overall service offering.

The business acquisition brings Wulff Accounting Services over a hundred new customers, five financial administration professionals, and an annual turnover of nearly 400,000 euros. The company’s professionals’ strong expertise and ability to serve customers in both national languages strengthen Wulff’s position especially in Eastern Uusimaa and the Helsinki metropolitan area.

Wulff Group expands its services into the consulting sector. The company believes there is room and demand in the growing market for a new enhancer of sustainable competitiveness. Wulff Consulting starts with a team of nearly ten experienced and visionary professionals, aiming to double the number of consultants during 2025 and achieve a strong position in the Finnish market.

Wulff continues to diversify in workplace services. The market conditions are indeed weak for these businesses at the moment, but I do see great opportunities if and when customers (companies) start recovering their businesses in the coming years. The risks are also quite clear, of course, when trying to dabble here and there instead of focusing on core competence, but I suppose there are also some cross-selling potentials between different services. The valuation is moderate if growth can be achieved in the coming years.

A move from Wulff that surprised even me a little. A difficult economic climate, a competitive industry, and the business would have to be built from scratch. In my opinion, a risky move, even if the size of the business won’t be significant in the coming years. According to our preliminary estimate, the revenue per person for such consulting firms is sometimes less than 100k but at best over 200k. It’s unlikely to reach the upper limit, at least in the initial phase. There might be small synergies with Wulff’s customer base. The press release gave little information about this new venture, but more conclusions will follow in tomorrow’s morning report.

Kopsa’s comments on how Wulff is establishing a consulting firm.

Wulff announced on Wednesday that it is further expanding its business into workplace services by establishing a consulting firm called Wulff Consulting. According to the press release, Wulff believes the market is growing and there is ample room for a “sustainable competitiveness enhancer.” According to the press release, Wulff Consulting will focus its services on, among other things, strategic business development, organizational coaching, and executive mentoring.

Wulff’s strategy-driven growth in the accounting firm sector continues with the acquisition of Aktiva Redovisning Åland Ab made on December 11, 2024. The joining of Aktiva Redovisning, operating in Mariehamn, Åland, with Wulff Accounting Firms elevates the Wulff Group to a key player in our country’s Swedish-speaking accounting firm market.

Aktiva Redovisning is known for its versatile services: in addition to accounting firm expertise, clients acquire business consulting and commercial law services from the company. The acquisition brings Wulff Accounting Firms nearly 150 new clients, five financial administration professionals, and an annual turnover of approximately 350,000 euros.