Valmet has been selected for the Dow Jones Sustainability Index (DJSI) for the tenth consecutive year. The company was listed in both the Dow Jones Sustainability DJSI World and DJSI Europe indices.

The Dow Jones Sustainability Index evaluates companies’ performance from environmental, social, and governance (ESG) perspectives, as well as their ability to continuously improve their sustainability practices. Valmet received particularly high ratings especially for innovation management and its reporting regarding resource efficiency, circular economy, emissions, and water.

Valmet is investing in the latest process equipment technology at its roll service center in Columbus, Mississippi, USA. The investment expands the range of process coatings manufactured by Valmet.

The value of the investment will not be disclosed. The installation and commissioning of the main equipment took place during the third quarter of 2023, and the new process is already fully operational.

I wonder if Valmet will benefit from Biden’s IRA; doesn’t it (the Inflation Reduction Act) subsidize all kinds of production capacity investments in the US?

Valmet’s climate program – Forward to a carbon neutral future – was launched in 2021. The program covers the entire value chain and includes four main targets focused on Valmet’s supply chain, the company’s own operations, and the use phase of technologies in customers’ production. In 2023, two significant achievements are being realized within the program.

Carbon-free production possible for all pulp and paper industry customers

The majority of Valmet’s value chain carbon footprint originates from the use phase of technologies, and this specific area of the program has two targets: to enable fully carbon-neutral production for all pulp and paper industry customers by developing new process technologies and to improve the energy efficiency of the existing offering by 20 percent by 2030. Valmet has now achieved the first of these two targets.

Procurement of 100 percent carbon-free electricity achieved in Finland and Sweden

Valmet’s target is to reduce carbon dioxide emissions from the company’s own operations by 80 percent by 2030. Emissions from fuels, heating, and electricity use have already decreased by 50 percent from the baseline year 2019. A new significant achievement will be the procurement of fully carbon-neutral electricity in Finland and Sweden by the end of 2023.

The order was included in Valmet’s third quarter 2023 orders. Delivery and start-up will take place in 2024. The value of the order will not be disclosed.

On December 21, 2023, Valmet entered into an agreement to acquire Demuth. Demuth is a Brazilian company specialized in wood handling solutions for the pulp industry. The acquisition strengthens Valmet’s wood handling technology and services, as well as its presence in South America.

The value of the acquisition will not be disclosed. The transaction is subject to approval by competition authorities and is estimated to be completed during the second or third quarter of 2024.

Demuth is a family-owned company founded in 1981. The company has two production facilities in Southern Brazil, in the state of Rio Grande do Sul. Demuth’s net sales are approximately EUR 20–30 million per year, and the company employs around 300–400 people. Demuth consists of the companies “Demuth Máquinas” and “Estruturas Metálicas Demuth”.

In addition to the benefits mentioned there, they have acquired an equipment base for the service business along with a workshop & presumably skilled employees, who can likely be used for servicing other lines (at the workshop as well as on-site) in South America. Maintenance and especially refurbishments tend to be a local game. Seems like a pretty good bolt-on acquisition; not significant, but it all adds up.

Almanakka has done a pretty good analysis of Valmet, in my opinion.

As an engineering company in fierce global competition, you can only succeed if you do things exceptionally well, even in the eyes of your customers. From this perspective, I think Valmet’s strategy is good. It focuses on refining its processes to perfection so that customers choose Valmet more and more often. Too often, strategies are described with empty buzzwords. In Valmet’s case, I think an investor can clearly understand what the focus is on. It would be great to get to interview Valmet employees and ask whether they feel this is also reflected in the corporate culture.

When a company has long-term ROIC >15%, then it must be really good at something, even though it does not produce iphones. Valmet is on my watch-list, although the entry point seems still a little expensive, my entry at around 20ish Eur.

Valmet or, for example, Nokia are not company clients, which is why there is no extensive report on them. Extensive reports are only produced for company clients (available for everyone to read).

These types of companies that are followed, for example, in the form of company reports (only for Premium members ) but are not company clients, are essentially only found among these larger firms. Company clients receive a more comprehensive “package”, such as an extensive report.

OP raises target price to €32 (prev. €30), we reiterate Buy rating.

Key highlights

Strong market shares in a growing market, fiber-based solutions are growing, strong financial position

Drivers:

Increasing wood usage, stable business development, profitability performance.

Risks:

Investment cycles, sharp decline in customers’ end products, project business risks.

Valmet has received an order from Yueyang Forest & Paper Co., Ltd. for the delivery of a Valmet IQ Web Inspection System for the company’s PM 8 paper machine. The system to be delivered will replace an existing system from another supplier. A Valmet IQ Web Monitoring System was already installed on Yueyang Forest & Paper’s PM 8 in 2019. After the implementation, Valmet’s machine vision systems will improve operational efficiency and optimize the quality of the paper produced on PM 8.

The order is included in Valmet’s orders for the fourth quarter of 2023. Delivery will take place in July 2024. The value of the order will not be disclosed.

Valmet will supply key technology for Shandong Jin Tian He Paper’s food-grade PM 13 folding boxboard line in China. The delivery includes headboxes, a wire section and press section, finishing technology, automation systems, and services.

There’s metal outside the stock exchange, of course, but since new orders in the sector have been in decline for a long time (e.g., 11/23 almost -20%), could investors just be “playing the earnings” based on the orders companies have reported for the quarter?

Since, for example, Cargotec has continued to rise — and the entire industrial sector already rose for a few months before the New Year — perhaps they are deducing who might end up holding the “Black Peter” this time (Q4). Another point of comparison for Valmet investors is surely Andritz — have they secured deals better in the sectors where they compete?

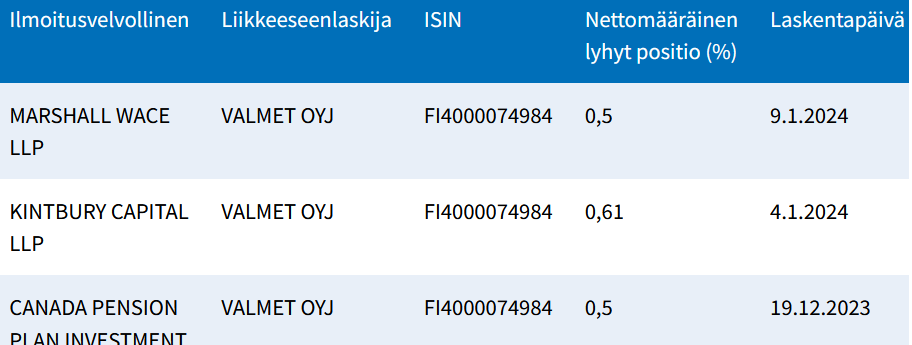

I do remember one summer from a few years back when short sellers took a bit of a hit in a similar situation — when Valmet announced quite a bunch of orders with a slight delay.

But as for Q4, besides today’s, have any other deals been announced with a price estimate?