Valmet Oyj’s Board of Directors has, in its meeting on September 28, 2023, decided on the record and payment dates for the second installment of the dividend to be paid for 2022, based on the authorization given by the 2023 Annual General Meeting.

The second installment of the dividend, EUR 0.65 per share, will be paid to shareholders who are registered in the company’s shareholder register maintained by Euroclear Finland Oy on the record date of October 2, 2023. The dividend will be paid on October 12, 2023.

So there’s no need to wonder why the share price will dip tomorrow (ex-dividend date).

Valmet will supply an automation system for Fingrid’s Jylkkä substation in Kalajoki as part of Destia’s overall delivery. The project involves building Finland’s first synchronous compensator to balance the main grid.

The order was included in Valmet’s orders received for the second quarter of 2023. The value of the order will not be disclosed. The end customer will take delivery of the automation system in March 2025.

Sofidel America has decided to invest in a Valmet Advantage DCT tissue line for the company’s Circleville mill in Ohio, USA. The investment includes a comprehensive automation package, flow control valves, and Industrial Internet solutions. The objective of the investment is to meet the growing demand of American consumers for high-quality and environmentally friendly tissue products. The start-up is scheduled for the second half of 2025.

The order is included in Valmet’s third quarter 2023 orders. The value of the order will not be disclosed.

Information about the client Sofidel Group

Sofidel Group is a privately owned company and one of the world’s leading producers of paper for hygienic and household use. Founded in 1966, the group has subsidiaries in 13 countries and more than 6,900 employees. The group’s turnover is 2.8 million euros and its annual production capacity is over one million tonnes.

Quite a big firm, that Sofidel, with a turnover of almost three million euros… I wonder what the real figure is, but then again, can you trust any other figures or the text in general if the text is treated as so trivial that it isn’t worth checking before publication.

Valmet introduces the updated Valmet Rotating Consistency Measurement (Valmet Rotary) for pulp and paper producers. The measurement utilizes the latest technology, featuring a redesigned user interface and even easier maintenance. The device allows for highly accurate fiber consistency measurement in critical applications.

Reliable fiber consistency measurement

The mechanical design and electronic solution of the Valmet Rotating Consistency Measurement have been updated, improving operational reliability. Thanks to its high sensitivity, this third-generation measurement is just as accurate as its predecessor. The simplified design makes on-site maintenance easier and faster, reducing total lifecycle costs.

Based on shear force technology, the performance of the Valmet Rotating Consistency Measurement is excellent even in challenging environments with high temperatures, high process pressures, or abrasive pulp components. Thanks to its modular design, the measurement operates reliably in all types of applications across a consistency range of 1.5–16 percent.

New powerful user interface

The commissioning, calibration, and monitoring of the device are facilitated by the new Valmet Link user interface, whose flexible platform also supports secure remote connections. The graphical display and clear menu structure enhance installation and operation. The intuitive user interface and larger screen simplify calibration and provide an excellent overview of device data. The user interface is designed to support various communication protocols and can be updated with new functions in the future.

Valmet will deliver a biomass power plant to Göteborg Energi AB in Gothenburg, Sweden. Göteborg Energi is building a new plant to produce energy and district heating from renewable and recycled fuels by 2025.

The order is included in Valmet’s orders received for the fourth quarter of 2023. The value of the order will not be disclosed.

Valmet launches the Valmet Oil Monitor application for remote monitoring of oil lubrication in fiber processing equipment.

Various rotating equipment on the fiberline operate in extremely harsh and demanding conditions, making it often difficult to retrieve the necessary oil samples. Adequate monitoring of lubrication properties based on sampling and laboratory analysis can be very challenging.

Bearing damage in rotating equipment is mostly related to inadequate lubrication of the bearings. Typical fault conditions, such as bearing vibration and heating, are usually detected only when the failure has already progressed further. Oil condition monitoring provides an opportunity to anticipate future failures through the deterioration of the lubricating oil quality. Thanks to oil lubrication condition monitoring, corrective actions can be taken before an actual failure occurs, reducing the number of unplanned shutdowns and the need for the repairs they entail.

First application for pulp washers

The first Valmet Oil Monitoring application was installed to monitor the oil lubrication of roll bearings in a TwinRoll wash press at a pulp mill in Europe. The application detected contamination in the bearing oil circulation unit, and thanks to this observation, machine operators were able to react quickly with the necessary maintenance action.

Valmet’s reliability monitoring applications are part of Valmet’s Industrial Internet portfolio. They include effective tools that enable fiber producers to ensure equipment availability and improve process performance.

Swedbank has also included two Finnish companies among its five favorite stocks this week: Valmet and Kone.

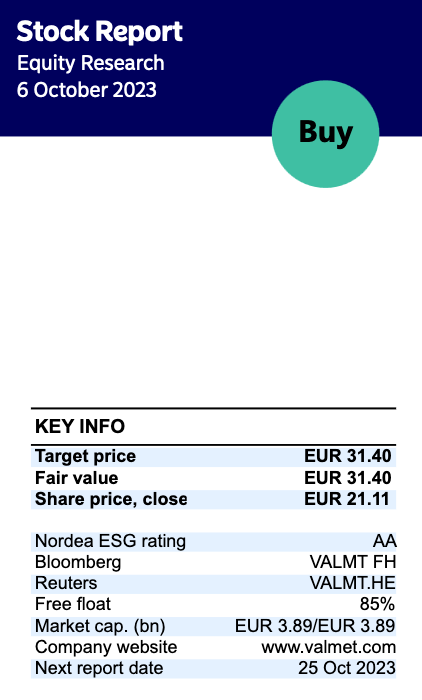

Kepler Cheuvreux has issued a buy recommendation for these stocks. Kone’s target price is 61 euros and Valmet’s is 37 euros, while the companies’ current share prices are around 38 and 21 euros.

At the moment, I see no reason not to buy more Valmet. Operational resilience is rock-solid, and the share of stable business is growing. Additionally, acquisitions seem to consistently hit the mark. Hopefully, more acquisitions will soon become available in cheap markets as companies with weak balance sheets are forced to sell off their profitable divisions.

The Körber Tissue deal will likely go through in November. Based on earnings figures alone, the price seems a bit on the high side. However, regarding Körber, one must also note the scale of its R&D department and patent portfolio relative to its revenue. Körber Tissue has about 1,000 patents, which corresponds to more than 20 years of Valmet’s pace. For this reason, the deal wasn’t made based on some basic “hot dog stand” cash flow calculation; buying pure expertise brings added value to Valmet.

The tissue business is not at any cyclical peak, but 36% of Körber’s business is on the service side, and its geographical distribution supports Valmet’s development. Once Körber’s revenue is factored into the 2024 estimates, Valmet will be back on a growth path.

The gas chromatography business bought from Siemens is a clear additional investment in expanding the profitable automation segment into new fields. Where the next area of core expertise will emerge will likely become clear in the form of new acquisitions in 2024.

I wonder if the profit warning is already priced into this downward slide? I would be grateful for a thorough response that proves my viewpoint wrong. I’d learn something new, save my money, and buy some beer instead.

I’d expect a profit warning to come out before Q3 if things look bad. However, by July, they had already slightly exceeded their guidance, at least in terms of revenue. Just my own gut feeling.

It’s worth remembering that Valmet is much more than just a company supplying paper machines to Europe. Not all market areas have as big problems as Europe.

Valmet supplies its solutions to forest industry companies that have issued profit warnings earlier this year, and these companies are still struggling with falling demand.

In Valmet’s case, the collapse in demand from forest companies naturally shows up with a lag, of which some (small) signs were seen in the Q2 figures.

First, the order backlog collapses, followed by revenue and earnings, etc.

These will start to rise only when forest companies begin investing again, and that too happens with a lag.

At the moment, factories are mostly being closed, and some deliveries started during the boom period are being finalized. Valmet hasn’t announced many new orders during Q3 .

In this market, it has been observed that profit warnings are not priced into the stock; instead, a steep downward trend begins even if the price has already dropped dozens of percent.

Summa summarum, the collapse of the forest companies has not yet flowed through (AT ALL) to Valmet, where it will surely hit partly already this year and also next year.

It’s probably true that forest industry investments are the result of long-term consideration, and the impact through end-product demand indeed comes with a delay. But it must be remembered that Valmet is more than just an equipment supplier for the paper and pulp industry. Valmet recently absorbed the flow control company Neles. Similarly, Valmet supplies equipment to the energy sector, where investments are not as sensitive to economic cycles. Generally, for engineering companies, equipment deliveries are low-margin and partly cyclical. For the resilience of profitability, the share of recurring business (such as services) is more critical, and this has increased at Valmet, for example, through Neles. Orders, which due to their size are mostly equipment deliveries, have been coming in quite sluggishly for all engineering companies; Valmet also announced only one in Q3 and recently one for Q4. Public announcements are also affected by customer consent. I await the interim report with peace of mind and am happy to continue as a Valmet shareholder, also because the valuation has already decreased significantly as the weakening outlook has been priced into the stock.