I wonder if gentlemen @lucas.mattsson or @jesper.hagman are heading to Aira’s Capital Markets Day tomorrow? As far as I can see, online participation isn’t possible, and as a salary earner with a large family, I can’t even get to the bathroom in peace, let alone Stockholm.

Upsales is certainly facing some very exciting times right now. The struggles of recent years are coming to an end, and the “culprits” are mostly becoming clear.

Culprit number one was poor sales performance. Management already held their hands up regarding this at least a couple of years ago when revenue and ARR growth stalled. It seems the sales team was rebuilt almost entirely, and sales operations underwent a fairly massive reform as well. Now, a year or two later, growth is starting to show again and they even dare to provide guidance (as far as I understand, Upsales hasn’t given guidance before). According to management, the growth problems were never due to the market, which has apparently been quite good the whole time.

Culprit number two appears to have been the AI investments, which have now hatched into a new listing company, AI Revenue Assistant Software Stockholm AB (publ), more familiarly known as Aira, Aira app, or AI sales agent. The name says it all: it’s a sales software built for salespeople and teams, which you buy from an app store, sync with your calendar and email, and then just start selling.

I haven’t worked as an actual salesperson a day in my life, but perhaps a salesperson could weigh in on whether there’s potential here or not? Apparently, the product is so good that it was born as its own listed firm almost by accident. It simply had to be built from an internal startup into a product for sale, because no one else had realized to do this yet and the need is obvious.

Now, a month or two later, the roadshow has been run, pilot customers gathered, and the first release to the app store has been made (apparently for Apple). The price is 149 euros per head per month, and the first paying customers have already been acquired. There is no sales team; no active sales efforts are being made. If someone buys, they do it themselves from the app store, and onboarding happens without consulting. The company size is 10 people and the product is ready.

If I’ve understood correctly, Aira will be spun off from Upsales during Q2, and trading of its shares will begin then. No new capital is being raised; instead, the company will take enough cash from Upsales so that by the time that money runs out, they should be able to manage on their own revenue. As far as I understand, no one is committed to any share sales in this situation; rather, every owner who held Upsales shares by May 21st will receive one Aira share for every one Upsales share. The price will be determined by the market in due course.

Personally, I don’t assign any value to Aira in my portfolio yet, but I will of course accept it as a very interesting option. These days, you never know what kind of price tag the market will slap on any AI-hyper-super-boom-shakalaka.

But one can always try to bracket the value a bit.

When the deadline to qualify for Aira shares via Upsales shares (record date May 22nd) passed last week, Upsales’ share value dropped by about ten percent, i.e., 50 MSEK. If I interpret the situation correctly, that was the price tag given to Aira at that moment. In reality, I suspect a large part of the market didn’t even notice the situation, given how flimsy the grounds for trading seem to be nowadays. So, not a very strong confidence in this conclusion.

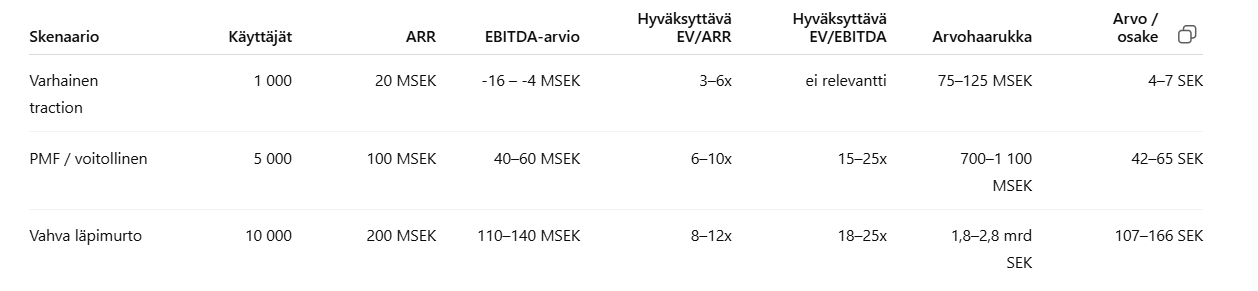

Well, if we calculate that one user brings the company that €149 / month, which is nearly €1,800/year, the ARR could look like this:

- 1,000 paying users: ARR 20 MSEK

- 5,000 paying users: ARR 100 MSEK

- 10,000 paying users: ARR 200 MSEK

It could, of course, be that the whole thing flops hard and they get 16 users, all of whom quit before Christmas. And by no means will all buyers pay full price for the product, as there are always various team discounts, launch campaigns, and other offers.

With a very rough estimate, Aira’s cost base could be, for example, 20-40 MSEK per year. But it’s naturally difficult to estimate from the outside what kind of growth investments will be made in the future, how fixed costs will grow as a listed company, etc. However, you can use that to bracket the number of users needed to move toward a profitable business. It’s not impossibly large.

By testing different assumptions, I came up with this:

It’s possible that all my assumptions—and thus everything printed in the table based on them—are completely unrealistic. Take it with a grain of salt.

But then, the remaining Upsales.

That is the truly interesting investment in this whole thing. But since I’ve written at such length about the seemingly interesting Aira, I’ll leave the ex-Aira-Upsales talk for next time.

I will say this, though: the company has finally returned to growth (guidance 10-15 percent for the year 2026) and ex-Aira-Upsales’ profitability is guided to be 35 percent EBITDA starting from the Q2 quarter. That makes for some quite attractive multiples for this year (2026e): EV/EBITDA 8, P/E 13, EV/S 2.7.

There’s cash, the product is ready, the cost base has been tightened, and they are reportedly on the winning side of the AI revolution (of course—has anyone ever declared themselves a loser in the AI transition?)